Author: Zuo Ye

Binance partners with USD1, exchanges no longer measure the effect of listing based on "trading volume." Binance is selling the largest real user base in the crypto space to projects. WLFI aims to promote the direct adoption of USD1, using it like USDT for interest accrual, pricing, and payments.

This is not an isolated case. OKX subsidizes USDG, Sun Ge's HTX subsidizes U—major exchanges are all finding their own ways out.

On-chain is different. Yield distribution has been homogenized into USDT and USDC. Collaboration between Vaults is decreasing and becoming less transparent, even less than partnerships with mainstream products.

This is happening at a time when even Bitwise is establishing Vaults to manage assets, upgrading the concept of non-custodial wallets to non-custodial vaults, and Kraken is leveraging Euler/Morpho/Aave to build an 8% APY wealth management product.

Does DeFi Lego only have theoretical value left, and how can pure channel value withstand the impact of exchanges?

DeFi Oddity: Scale Grows, Yields Decline

"Network effects are about human connections; tokens are just units of measurement.

In the future, tokens will no longer point to the crypto industry; history will more often use the AI industry as their载体.

When USDe and Binance jointly offered a 12% APY, many thought USDe would move from on-chain to mainstream exchanges and eventually become a real off-chain payment network.

After the October 11th event, Binance essentially abandoned Ethena as a partner,转而 supporting U and WLFI's USD1. Ethena turned to the Hyperliquid ecosystem and survives as a white-label platform.

The real revelation is that if on-chain stablecoins cannot reach truly mainstream industries, then more complex DeFi products must reach users through intermediary industries.

This is why Vault & Yield are hot now, but C-end users no longer choose to hold UNI and Aave. Their understanding of DeFi has collapsed into one thing—deposits.

- Ideal user flow based on DeFi Summer: Participate in BTC/ETH network nodes, obtain tokens -> Participate in DeFi protocols -> Use DeFi Lego blocks

- Actual user flow based on the 2026现状: Exchange for USDC via CEX or bank card -> Find Vaults with higher APY -> Spend using Neobank's U card

Yes, users will use Vaults directly, not caring whether the Vault is backed by Morpho or Euler, or even which Vault it is. They care more about Kraken and Coinbase's promotional partnerships.

Among 522 protocols, 709 assets, and 3489 active Pools, the nested relationships between protocols, assets, and Pools are no longer important. This is the end of DeFi Lego.

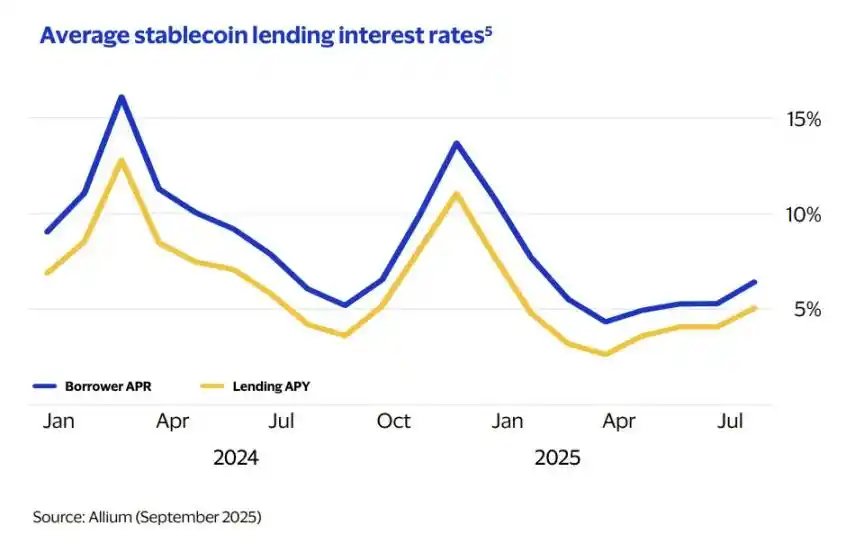

Caption: Average Borrowing Interest Rate

Image Source: @visa

The most直观 example of this end is that stablecoin Borrow APR has fallen to 6.4%. Considering the cumulative lending volume has grown to $670 billion over the past five years,庞大 scale but stable interest rates will become the norm.

The end of DeFi Lego has caused DeFi project governance tokens to completely lose value. The function of governance tokens is not in voting value but in long-term坚定 holding. 1 person creates BNB, 100 people hold BNB, 1000 people trade BNB, 10000 people will believe BNB has value.

The unit of measurement for vaults is not the power consumption of public chains, nor the governance standards of DeFi protocols themselves, but the standard dollar recognized by other vaults. In a sense, USDC/USDT directly取代了 the function of cross-chain bridges.

If USDT/USDC themselves become channels, then Pools/Vaults will not emphasize接入 specific cross-chain bridges and assets; they only need to support stablecoins to meet most people's needs.

People and their value are排斥ed out of the DeFi operating system. Human consumption value is the sole demand for economic operation, and stablecoins ultimately become the sole demand of Vaults.

Even Vaults themselves, as interest-bearing assets for stablecoins, also need users' USDT/USDC. But these stablecoins are not invested in other DeFi protocols, or even in the repurchase of treasury bonds; they lie idle in limited steps waiting for withdrawal.

Referring to the fact that the interest rates on large deposit products of some domestic rural commercial banks have fallen below 1%, we can expect to see the奇景 of stablecoin projects charging users fees in 2026.

Ultimately, all DeFi protocols become homogenized deposit products. Whether it's traditional spot DEX, lending, or Perp DEX, Cap even directly launches Stabledrop, with more airdrop value exchanged for stablecoin assets rather than the project's own tokens.

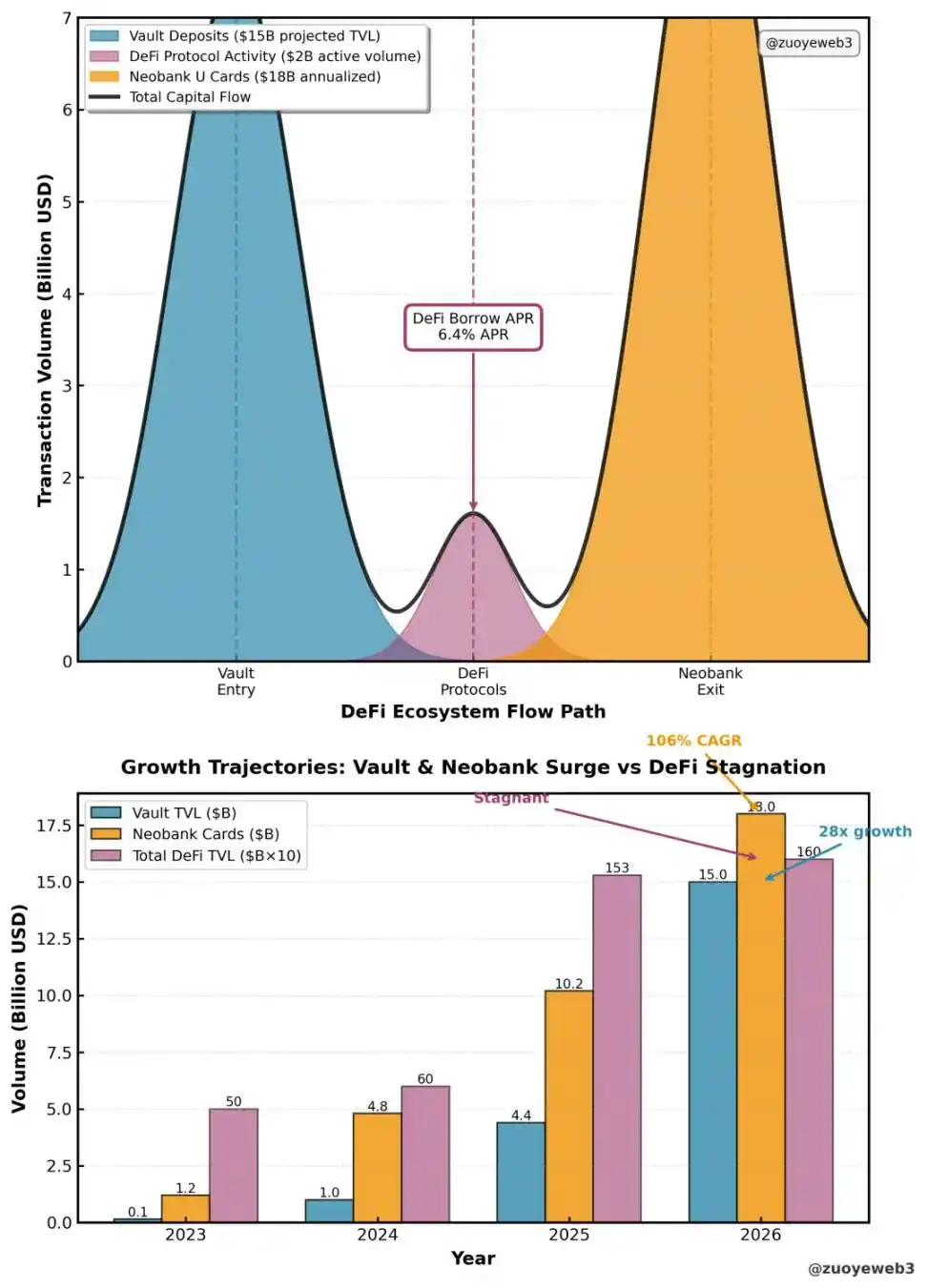

If you carefully map the current shape of DeFi, it would be a semi-finished product with a "big head, big tail, and hollow middle"—countless DeFi Vaults compete for user deposits, but Vaults no longer intertwine to increase leverage. They even wary of each other to avoid deposit outflows, and the underlying assets are all U.S. bonds,最终 flowing to numerous Neobanks.

Caption: DeFi Circulation Pattern

Image Source: @visa @artemis @DefiLlama

Neobanks collectively rushing towards U cards has caused their monthly transaction volume to soar from $100 million in 2023 to $1.5 billion. The main users of current Neobanks are still the on-chain群体, proving their considerable spending power, but the decline of DeFi is also a major reason for capital outflow.

This leads to a one-way interaction between users and protocols, but Vaults are彻底扁平化. The few connections are private activities, and users only perceive disputes and fear afterwards, just like the old story of xUSD.

From the history of DeFi and stablecoins, the real scenarios are only three tracks: trading, yield, and consumption. Trading is divided among CEX, Spot DEX, and Perp DEX. DeFi has completely shifted to a Vault model focused on yield. Consumption is split between USDT represented by Tron and emerging NeoBanks.

Frankly, when retail deposits flow into Vaults, stock tokens, Perps, prediction markets, and Meme coins, the disappearance of the altseason is理所应当. In a world where retail has nothing to buy or sell, only deposits have not brought prosperity to DeFi.

TradFi启示: Satisfy People, Don't Persuade Them

Learn from AI, then learn from banking; earn money uprightly.

It can be very clearly stated that current stablecoin yields are Features of individual protocols, not a赛道!

A赛道 requires protocols to push the entire industry forward through competition, like Perp DEX or the AI race. But current DeFi Vaults are all acting as entry points without the配合 of process and exit. They are all competitors with no coordination.

Refer to Taobao's Double Eleven event—the details are becoming increasingly变态; even Alibaba's Qianwen might not be able to calculate the best strategy.

Vaults are the same. The strategies set by various Curators are becoming more complex. Users can do nothing but deposit. When a Vault has problems, users can only face off against the professional litigators from law firms.

From the development needs of DeFi, once ordinary users can only consume passively and cannot participate in the production环节, so-called institutionalization occurs, and ordinary retail investors turn to more alternative, freer financial markets.

- Retail疯狂 bought GME to battle Wall Street

- Retail疯狂 bought Meme, rejecting altcoins

A clear trend is that while DeFi is developing towards institutionalization, traditional banking is actively seeking transformation, embracing newer market demands. The most typical example is Revolut's valuation reaching $75 billion.

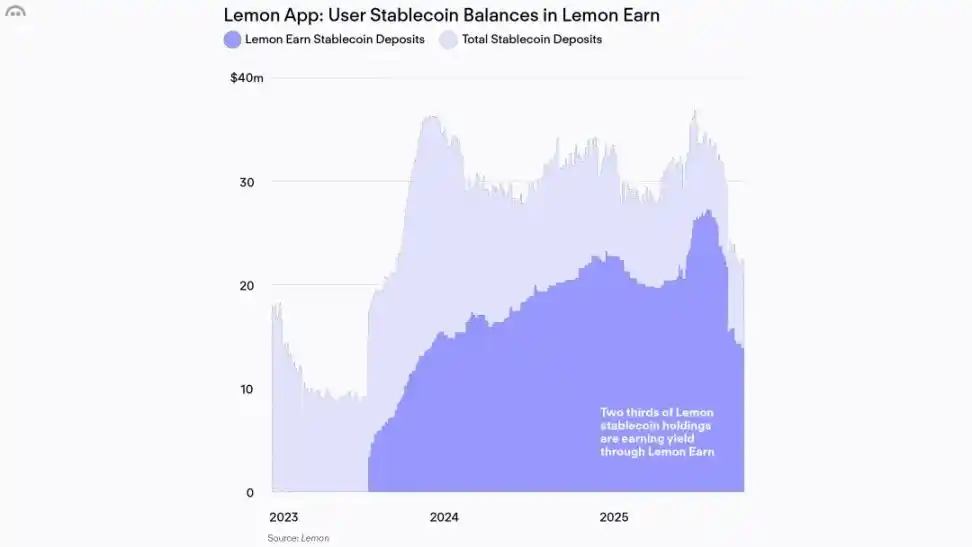

Caption: Off-chain Users Are Worthless

Image Source: @lemonapp_ar

In contrast, the token market cap of Aave, the largest DeFi bank, is only $2.5 billion. Measured by deposits, it would even be among the top 20 banks in the U.S. This is not an isolated case; most DeFi Vault products themselves are worthless.

Refer to Aave's approach in Latin America, embedding itself into younger, more financially underserved populations. Taking the Argentine wealth management product Lemon as an example, it brought 130,000 wealth management users to Aave, but only $40 million in deposits were imported.

Compare this to Aave's on-chain addresses: only 170,000 addresses support its $32 billion TVL. This itself shows that the network effect of retail investors can greatly support project valuation. If only pursuing the scale effect of capital, there is certainly no future for DeFi tokens.

Moreover, as the voice of Vaults within lending protocols increases, the brand value of the traditional protocols themselves decreases. Morpho introduced Sky Vault Curators to "balance" the dominance of Stakehouse. The essence of Aave V4 is also modularization. Eventually, the entire DeFi will become a backend product.

The launch of Aave's mobile app signals anxiety, not greater ease.

In this context, it is not shameful for DeFi to learn from banking. According to a McKinsey report, the global banking industry achieved $1.2 trillion in profits in 2024 alone.

But a crisis has emerged. In 2018, 25% of users would directly choose their开户 bank when spending, but by 2025, this number had dropped to 4%.扪心自问, which Vault has a loyalty rate of 25%?

The疯狂 competition over APY is the consequence of恶性 competition among Vaults. In traditional banking, large banks serve large clients, and small banks serve small clients. Especially younger generations need to gradually build credit scores to gain access to services from high-level banks.

Now is the time for DeFi Vaults to regain the trust of retail investors. Alliances with CEXs are also a beginning. Various Vaults constantly compete for the entry effect of CEXs, making CEXs the upstream of Vaults.

Although they need to actively share profits with CEXs, Vaults can thereby reach tens of millions of real users. Users are not completely passive either;经过 CEXs, they will also seek higher and safer yields, forming a new interaction model.

Conclusion

Products should serve the network, not roles.

When retail investors no longer participate in protocol governance (voting, holding, trading), their remaining awareness of the protocol will also be lost, ultimately leading to the absence of people on-chain.

Now that Vault & Yield has become the mainstream on-chain model, how to rediscover human value in a network without Tokens? DeFi needs to放下身段 and learn from the ever-present TradFi.