Author:Liam 'Akiba' Wright

Compile:Saoirse,Foresight News

The preferred shares issued by bitcoin reserve companies have long ceased to be purely income-generating assets; they have become a credit benchmark testing the balance sheet robustness of bitcoin enterprises. While market focus remains concentrated on Strategy, data disclosed by Strive, the seventh-largest bitcoin-holding listed company globally, directly demonstrates the real impact of risk spillover: another bitcoin reserve company holds Strategy preferred shares, and the value fluctuations of this holding have become a clear signal of market pressure.

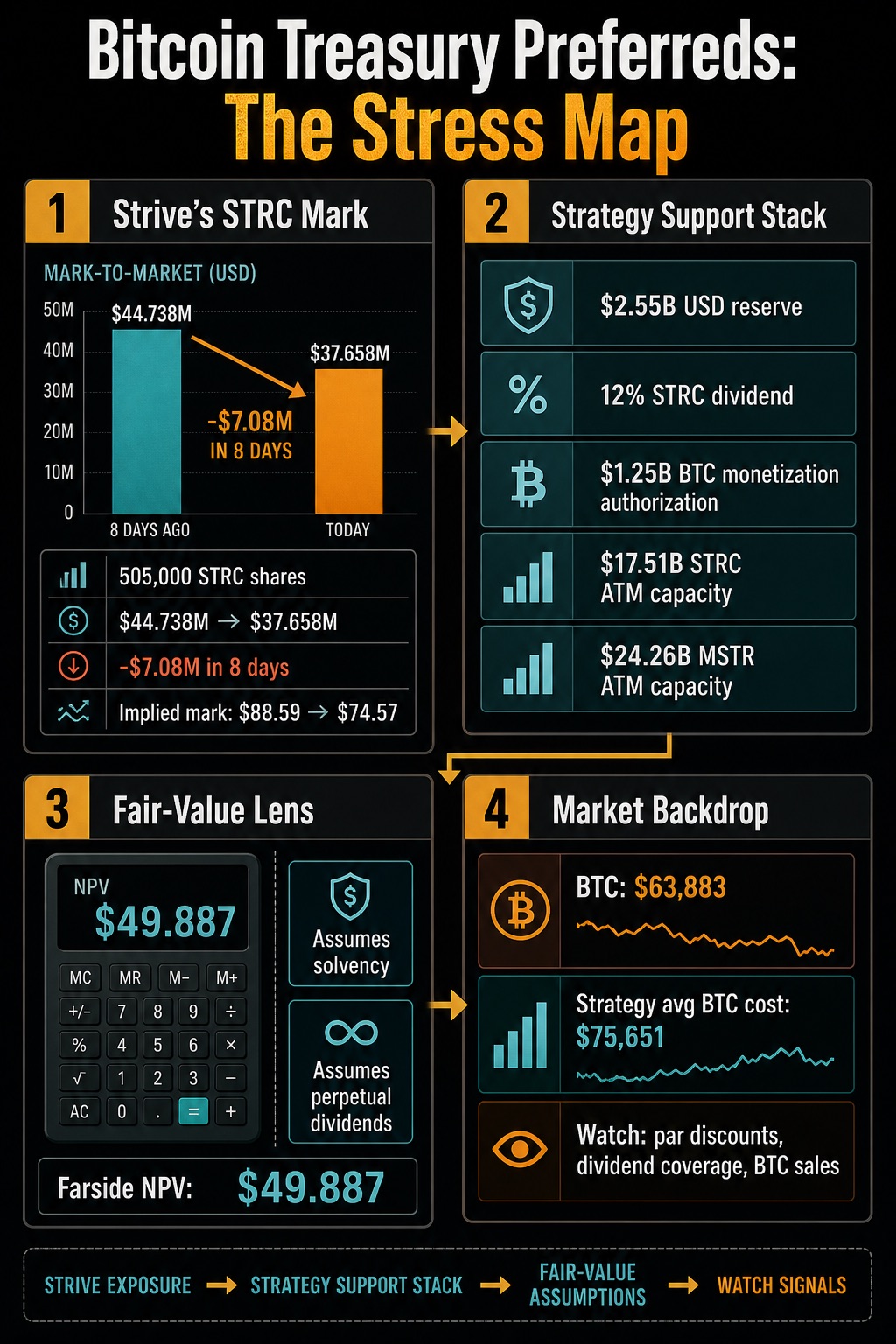

In an update document released on June 29, Strive disclosed that between June 18 and June 26, the number of its held 505,000 STRC shares did not change, but the fair value of this holding fell from $44.738 million to $37.658 million.

In just 8 days, with no adjustment to the share count, the holding value evaporated by $7.08 million. Based on a simple calculation of the declared fair value, the market's valuation of Strive's STRC holdings dropped from approximately $88.59 per share to $74.57 per share.

This disclosure document does not prove the company is insolvent, forced to sell assets, or that its capital structure has completely failed. However, it reveals a more critical fact: even before a major crisis erupts, the risk associated with bitcoin reserve preferred shares can transmit to other companies' balance sheets through cross-shareholdings.

As of June 26, Strive still holds 19,864 bitcoins, possesses $141.7 million in cash and equivalents, and has 7,829,502 of its own SATA preferred shares outstanding. But the core signal released by this financial report is not its own asset scale, but rather that its exposure to Strategy preferred shares has fundamentally altered investors' judgment logic for the entire sector.

The market has long debated the STRC issued by Strategy: whether investors would treat this product as a stable income instrument or as a high-risk credit asset tied to bitcoin price action, market liquidity, and Strategy's dividend payment capability. Strive's disclosure makes this question even more pressing.

Different bitcoin reserve companies cross-holding each other's preferred shares establish a clear and visible cross-company risk transmission channel. Once STRC trades at a discount, Strive will reflect asset losses in its financial report's fair value. If Strive's subsequently issued SATA preferred shares also face market skepticism, the market can intuitively judge whether the current pressure is a single-company issue or has spread throughout the industry via the preferred share financing model.

The initial marketing points for these reserve preferred shares were stable yield, fixed par value, and regular dividends, which strongly appealed to investors preferring stable returns. However, when market focus shifts to discount-to-par ratios, cash reserve coverage, dividend adjustment mechanisms, share buybacks, and potential asset sales, the trading nature of these securities completely shifts towards credit-like risk assets.

The core question investors now care most about is: Does the issuer have sufficient cash, smooth financing channels, and adequate bitcoin liquidity to guarantee the credibility of dividend payments?

Strive's $7.08 million unrealized loss on its STRC preferred shares in 8 days exposes industry cross-holding risk. Simultaneously listing Strategy's full toolkit for stabilization—cash reserves, high dividends, coin sales, share issuance, etc.—alongside the third-party estimated STRC fair value of only $49.887 and the current bitcoin price far below the company's average cost basis, the article highlights the need to closely track preferred share discounts, dividend coverage capability, and bitcoin selling actions to judge industry risk trends.

Strategy's New Operational Framework: Essentially Credit Risk Management

The regulatory filing submitted by Strategy on June 29 further confirms the aforementioned shift in logic. The company introduced a Digital Credit Capital Framework, accompanied by policies including US Dollar Reserve Management Rules, a revised STRC dividend plan, a preferred share repurchase program, a common stock repurchase program, and a Bitcoin Monetization Plan. This combination of tools is specifically designed to address stressed capital structures.

Strategy disclosed that as of June 28, its US dollar reserve size reached $2.55 billion. The board mandated that management must retain cash reserves sufficient to cover at least the next 12 months of annual preferred share dividends and interest expenses, unless specifically authorized by the board to lower this threshold. The document also stated that reserve funds could be replenished through selling tokens under the Bitcoin Monetization Plan or via other capital market operations.

This reserve is crucial because Strategy increased the regular annualized dividend for STRC to 12%, payable monthly in two installments, applicable to record dates on or after July 1. The company has announced a $0.50 per share cash dividend for the settlement periods ending July 31 and August 15, with specific payment conditions subject to the STRC issuance agreement.

While raising dividends can support this income product in the short term, it also raises new questions: if the security continues to trade at a discount, can this high-dividend policy be sustained long-term?

Strategy clearly outlined the policy linkage logic: the STRC dividend plan will comprehensively consider the STRC secondary market price, overall market yields, credit spreads, bitcoin price and volatility, reserve coverage, capital market environment, and the company's overall capital structure. The document also emphasized that STRC dividends are not guaranteed obligations and will not be unilaterally increased simply because STRC's market price is below par value.

The entire policy system follows an active credit management approach. The company also authorized up to $1 billion for repurchasing its own digital credit securities. If management judges that repurchases can enhance enterprise value and optimize the capital structure, STRC will be the priority repurchase target. An additional $1 billion was authorized for repurchasing Class A common stock. These repurchase authorizations do not obligate the company to execute them but clearly demonstrate all the tools management can employ if discount risks continue to worsen.

Within the same capital framework, bitcoin sales were also formally incorporated as a response measure. The board approved the Bitcoin Monetization Plan, allowing the company to raise up to $1.25 billion by selling bitcoin to supplement US dollar reserves. If management determines this method is preferable to issuing additional common stock or other capital market operations, proceeds from coin sales can be used to cover preferred share dividends and interest expenses and also provide funds for share repurchases.

The company explicitly stated that this plan does not mandate forced bitcoin sales. However, this authorization fundamentally changes the market narrative: this company, originally built around hoarding bitcoin as its core business, now has a formal channel to utilize its bitcoin assets to stabilize its credit system.

Fair Value Calculations: The Core Test is Dividend Sustainability

The STRC fair value calculator publicly available from third-party firm Farside explains why the market discussion has long moved beyond surface-level yields. CryptoSlate queried the tool's data on July 7. Under preset calculation conditions, STRC's net present value per share was only $49.887. The calculation model defaults to an initial coupon rate of 11.50%, which steps down to 3.60% starting from month 33.

This calculation has a key prerequisite assumption: the enterprise continues normal operations and permanently pays dividends in full. This valuation is not the official pricing provided by Strategy, nor should it be conflated with Strategy's announced 12% annualized STRC dividend policy. However, it clearly reflects the core variable that preferred share investors truly focus on: valuation is highly dependent on dividend sustainability, the discount rate, and the issuer's ability to continue making interest payments amidst bitcoin price movements and capital market fluctuations.

The broader bitcoin market environment further amplifies this credit test. CryptoSlate bitcoin price data shows that on July 8, bitcoin was quoted around $62,000, with a 24-hour decline of 1.8%, a 7-day gain of 5.5%, a total market capitalization of $1.24 trillion, and bitcoin's market share of the total crypto market at 58%.

However, Strategy's June 28 bitcoin holdings data shows the company holds 847,363 bitcoins with an average cost basis of $75,651. While the current market price being far below the average cost won't force immediate sales, it also explains why the market is highly focused on reserve policies, at-the-market (ATM) issuance mechanisms, and terms related to bitcoin monetization.

Strategy's ATM issuance data intuitively shows this business model still possesses ample financing space. Between June 22 and 28, the company did not issue additional preferred shares via the ATM channel. It only sold 12,669,017 shares of MSTR common stock, raising net proceeds of $1.1524 billion. Remaining issuance capacity stands at: $17.5108 billion for STRC preferred shares and $24.2575 billion for MSTR common shares, alongside other preferred share issuance programs.

The entire business model still has multiple cushioning tools. But the key question is: What price must be paid to deploy these tools when investors demand higher yields, securities trade at significant discounts, or stronger collateral assets are required?

Two Scenarios: Judging Whether Risk Has Fully Spread

The market's current judgment on the subsequent trend is divided into two core logics:

Scenario One: Risk Contained, Affecting Only Strategy

STRC discount narrows. US dollar reserves and dividend policies stabilize market sentiment. The Bitcoin Monetization Plan remains only a backup option. Strive's asset impairment is merely a one-off, short-term shock from cross-holdings. The rest of the industry's reserve companies remain unaffected. Pressure remains concentrated solely on Strategy itself.

Scenario Two: Risk Fully Spreads

STRC remains deeply discounted long-term. Raising dividends fails to placate the market. The company increasingly relies on the common stock ATM issuance channel. The Bitcoin Monetization Plan transitions from authorization to actual selling. Simultaneously, Strive's own issued SATA preferred shares come under pressure. They are no longer viewed as independent products but are grouped with STRC by the market as high-risk assets. At that point, bitcoin reserve preferred shares evolve from a single-company issue into a systemic risk for the entire sector.

Existing disclosure documents do not prove the second scenario is occurring yet, but they sufficiently explain the root of market concern: Strive's holding of STRC directly translates Strategy's discount risk into a fair value loss on another company's financial report.

Strategy's introduced framework integrates dividends, cash reserves, share buybacks, ATM issuances, and potential bitcoin sales into a unified risk buffer system. Meanwhile, the Farside valuation tool highlights that corporate viability and the assumption of perpetual dividends are the core determinants of preferred share value.

The core indicators for subsequent market observation are clear: whether the discount-to-par for STRC and SATA widens, whether dividend cash coverage capability is credible, whether companies increase the intensity of common or preferred share issuance, and whether bitcoin sales remain only at the authorization stage.

Future financial reports disclosed by Strive will become a critical signal to judge whether the loss on its Strategy preferred shares is merely an isolated case or the first public sign of bitcoin reserve credit risk spreading industry-wide via the preferred share model.