Original|Odaily Planet Daily(@OdailyChina)

Author|Wenser(@wenser 2010)

Just after the fervor over SK Hynix's "sky-high 6.1 million bonus," South Korea's financial scene took a sharp turn for the worse:

On May 18, the Korean stock market triggered a circuit breaker as the KOSPI 200 futures fell 5%, suspending algorithmic trading for 5 minutes; Samsung Electronics was caught in a dilemma due to the "major union strike" incident. This was compounded by the stock market plunge triggered by South Korean Presidential Policy Chief Kim Yong-beom's proposal for an "AI tax universal dividend." Meanwhile, the crypto market, once a key sector of South Korea's finance, continues to bleed, with Upbit's parent company Dunamu's Q1 net profit plummeting by 78%.

The South Korean financial market, where bubbles and dividends coexist, and speculation and hype dance together, has enjoyed the dividends of the AI era but has also stepped into a new era of chaos.

Samsung Strike Storm: From an Injunction to Continued Negotiations, Strike May Still Occur

Let's start with Samsung Electronics, the prestigious "barometer of the Korean stock market."

Previously, Odaily Planet Daily mentioned the root cause of this major strike event in "AI Bull Market Reprices Everything, Including the 'Male Valuation System' in the Dating Market": the union hopes the company will increase the bonus ratio and remove the bonus cap mechanism. At that time, according to JPMorgan estimates, this planned 18-day strike could cause losses of 4 trillion won, while also reducing production of DRAM and NAND chips.

But the negative impact of this strike goes far beyond that.

According to South Korean Prime Minister Kim Min-seok: "Just one day of shutdown at Samsung Electronics' semiconductor factory is expected to cause direct losses of up to 1 trillion won (approximately $668 million). More worryingly, a brief halt in the semiconductor production line could lead to an inability to resume production for months. If materials must be discarded due to the strike, market concerns are that economic losses could expand to as high as 100 trillion won." In other words, this is a strike event whose potential losses are too great for Samsung Electronics and the entire South Korean financial market to accept.

In light of this, South Korean Prime Minister Kim Min-seok first stated: he would seek all options to avoid a Samsung Electronics strike; subsequently, this morning, a South Korean court partially approved Samsung Electronics' request for an injunction against the union's planned strike. Affected by this news, the KOSPI index turned positive; after Samsung Electronics and its largest union resumed high-stakes wage negotiations, Samsung Electronics' stock price also rose by up to 6.7%.

Just as the market thought the "Samsung major strike" event was about to take a favorable turn, news from the union side raised the hearts of South Korean investors to their throats again: around 12 o'clock, the Samsung Electronics union stated that despite the district court partially approving the company's injunction application, they still plan to proceed with the strike on May 21. The general meaning was: "They respect the court's injunction, which requires the union to ensure that any strike action does not interfere with production."

Last Sunday, the South Korean government stated it would invest 170 billion won (approximately $113.3 million) to support SMEs covering advanced semiconductors and related industries. This also reveals the South Korean government's new plans and development intentions for the financial market and economic industries. While Samsung Electronics has encountered development opportunities due to AI dividends, it also means a restructuring of profit distribution, accompanied by volatility and risk in South Korea's financial markets like the KOSPI index.

Behind the "AI Communism" Discussion: The South Korean Government Wants to "Take AI Dividends to the End"

Last Friday, May 15, the KOSPI index touched 8000 points for the first time, hitting a record high.

At the same time, the Korean stock market also experienced a historic level of "foreign capital flight" last week.

On May 15, affected by the Samsung strike event and profit-taking, foreign investors sold KOSPI stocks worth 1.6 trillion won in morning trading. According to Goldman Sachs statistics, overseas investors withdrew about $17 billion from Asian emerging markets excluding China last week, marking the second-largest weekly outflow on record. South Korea accounted for the vast majority, with an outflow scale of $13.2 billion.

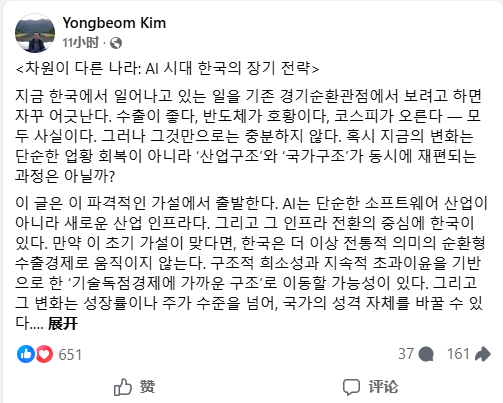

The "AI citizen dividend" proposed earlier by South Korean Presidential Policy Chief Kim Yong-beom was a major catalyst behind this.

On May 11, Kim Yong-beom posted on Facebook: "Excess profits generated in the era of AI infrastructure should be structurally returned to all citizens through institutional design"—a concept he tentatively named "citizen (national) dividend."

He also emphasized that in the AI era, excess profits naturally concentrate among a minority. Without institutional intervention, domestic wealth polarization will further intensify. Shareholders of memory chip companies, core engineers, and various asset holders are likely to reap substantial rewards, while the vast middle class may only feel indirect effects.

Though I don't understand why a government department spokesperson's opinion piece would be posted on Facebook?

The news caused an uproar: many interpreted his public remarks as the South Korean government planning to impose additional taxes on high-profit AI companies like Samsung Electronics and SK Hynix; the KOSPI index subsequently fell by over 5%.

Kim Yong-beom later clarified to the media: "The 'citizen dividend' from the AI industry will come from excess tax revenue, not directly from the profits of AI companies." South Korean President Lee Jae-myung also posted on X, stating that Kim Yong-beom's related remarks were discussing the possibility of "distributing national excess tax revenue generated by excess profits in the AI field in the form of a citizen dividend," not meaning directly using corporate profits to provide subsidies. Lee Jae-myung's wording was strong, characterizing the external interpretations as "fake news manipulating public opinion."

As one of the world's major economies, South Korea's industrial and social structure is highly distinctive: limited by domestic market size and past technological advantages, its economic industry exhibits the following characteristics—heavy reliance on exports, heavy reliance on the chip industry, and high concentration in a few conglomerates; socially, South Korea also possesses strong union culture and high social sensitivity. Therefore, as the AI industry becomes a "profit-making machine," South Korea has become the financial market where conflicts over "excess profit distribution" are most intense.

Companies with HBM (High Bandwidth Memory) mass-production capabilities are only a few like Samsung Electronics, SK Hynix, and Micron, holding the "key to AI storage." This is also a major reason why countless securities firms and institutions are flocking to stocks like SK Hynix and Samsung. Today, Nomura Securities published a report noting that AI-driven demand is growing exponentially, memory supply is limited, and memory stocks are expected to undergo a valuation reassessment. The firm significantly raised its target prices for Samsung Electronics and SK Hynix. Samsung's target price was raised from 340,000 won to 590,000 won, and SK Hynix's from 2.34 million won to 4 million won, both with "Buy" ratings.

"The Crypto Market Abandoned by Korean Finance": Exchange Revenue Plunge, Regulatory Scrutiny, and Asset Freezes

According to estimates by renowned investment bank Goldman Sachs, South Korean retail investors bought $14.1 billion worth of stocks last week; in contrast, as early as last year, the South Korean crypto market had already begun to bleed continuously.

According to statistics, the value of South Korean crypto investors' holdings nearly halved within a year: in January 2025, the size of the South Korean crypto market was approximately 121.8 trillion won ($83.3 billion); by the end of February 2026, this number had dropped sharply to 60.6 trillion won ($41.4 billion). The daily average trading volume of South Korea's top five crypto exchanges (Upbit, Bithumb, etc.) also plummeted from $11.6 billion in December 2024 to $3 billion in February 2026, a drop of 74%.

The main reasons for the continuous loss of liquidity are the ongoing decline of the overall crypto market and the continuous siphoning by the stock market. To put it simply, the external stock market keeps hitting new highs, while the crypto market itself is underperforming.

Major Exchange Revenue Plunge: Upbit Parent Net Profit -78%, Bithumb Revenue & Profit -95%

According to news from the "Asian Daily," the Q1 operating revenue of Dunamu, the parent company of Upbit, was 234.6 billion won, down 54.6% year-on-year (YoY) from 516.2 billion won last year; operating profit was 88 billion won, down 77.8% YoY from 396.3 billion won last year; net profit also fell to 69.5 billion won, down 78.3% YoY from 320.5 billion won last year.

Bithumb's Q1 revenue was 82.5 billion won, down 57.6% YoY from 194.7 billion won last year; operating profit was 2.9 billion won, down significantly by 95.8% YoY from 67.8 billion won last year; net profit turned from a profit of 33 billion won last year to a loss of 86.9 billion won.

Anti-Money Laundering Rules, Crypto Taxation, and Acquisition Scrutiny

In August last year, the Korean Financial Supervisory Service officially implemented revised anti-money laundering rules, where transactions exceeding 10 million won per transaction on foreign exchanges/private wallets will be flagged as suspicious addresses.

Additionally, the South Korean Ministry of Strategy and Finance has confirmed that the 22% crypto capital gains tax will take effect as scheduled on January 1, 2027.

Moreover, the acquisition case of Upbit's parent company Dunamu has recently come under review by the Financial Services Commission—previously, Hana Bank announced plans to acquire approximately 6.55% of Dunamu's shares but did not consult with regulatory authorities; the transaction is suspected of violating the "separation of finance and virtual assets" regulatory rule.

According to the Virtual Asset Division of the Financial Services Commission, Hana Bank's indirect holding of Dunamu shares through the acquisition of Kakao Investment shares essentially constitutes an investment in a virtual asset trading platform, and therefore will be reviewed under the same regulatory standards. It is worth noting that since 2017, the South Korean government has restricted financial institutions from holding, purchasing virtual assets, or making equity investments in related companies through administrative guidance. If ultimately deemed non-compliant, Hana Bank's related transaction may not be completed.

Assets of Over 22.1 Billion Won Frozen for Korean Crypto Community

As early as 2024, a joint study by the Korean Financial Supervisory Service (FSS) and the Korean Financial Intelligence Unit (FIU) found that as many as 70% of cryptocurrency exchanges were unable to return customer investment funds after closing down.

Now, there is more detailed data on this scale—according to a Yonhap News Agency report, based on information obtained from the Financial Supervisory Service by People Power Party lawmaker Kang Min-guk, as of May 4, there are 15 virtual asset service providers in South Korea that have ceased operations, involving approximately 1.949 million users, with frozen assets amounting to 22.1 billion won ($14.87 million).

It must be said that with such a polarized regulatory environment, it's no wonder there are no new entrants to the crypto space.

The "Leverage Nation" Drinking Deeply from the Bubble

To this day, South Korean finance has experienced a "second spring" through the "AI bubble," although institutions like Goldman Sachs and Citigroup have explicitly stated they have taken profits at this stage, they remain highly optimistic about the subsequent trend of the South Korean stock market.

Having learned from past experiences like the Asian financial crisis and the 2022 Lotte debt crisis, South Korean financial regulatory authorities have their own plans for risk control.

Recently, the Financial Services Commission and the Financial Supervisory Service announced plans to tighten liquidity supervision standards for domestic securities companies, intending to extend liquidity ratio regulatory rules to cover all domestic securities firms; they plan to optimize the calculation method for liquidity ratios, applying discount factors to assets and including contingent liabilities such as debt guarantees, to enhance crisis response capabilities. Additionally, they plan to increase the risk weight for net capital ratios corresponding to real estate-related exposures and set an overall investment limit. For securities firms with higher systemic importance, specific capital supervision rules will be introduced.

On one side are aggressive investors who favor "leveraged trading," and on the other is the heavy hand of strict supervision. A new era of financial turmoil in South Korea has begun.