Author: Ma He, Foresight News

Original Title: Funding a Bugatti with Polymarket? Someone is Playing 'Self-Directed' Insider Trading

On March 10, X user @Euanker posted an exposé alleging that renowned combat sports champion Andrew Tate was involved in insider trading on Polymarket, profiting by manipulating markets related to the quantity of his personal tweets. Euanker pointed out that Tate created and controlled at least 7 Polymarket accounts, accumulating profits of $52,286 across six 'Weekly Tweet Count Prediction' markets. These markets essentially depend on Tate's own actions, with the exposé bluntly stating his aim was to 'raise funds for a rented Bugatti sports car.'

Interestingly, this exposé included detailed on-chain evidence and profit charts, allowing us a glimpse into the specifics of this insider trading.

Detailed Explanation of On-Chain Address Records: Identical Deposit Paths

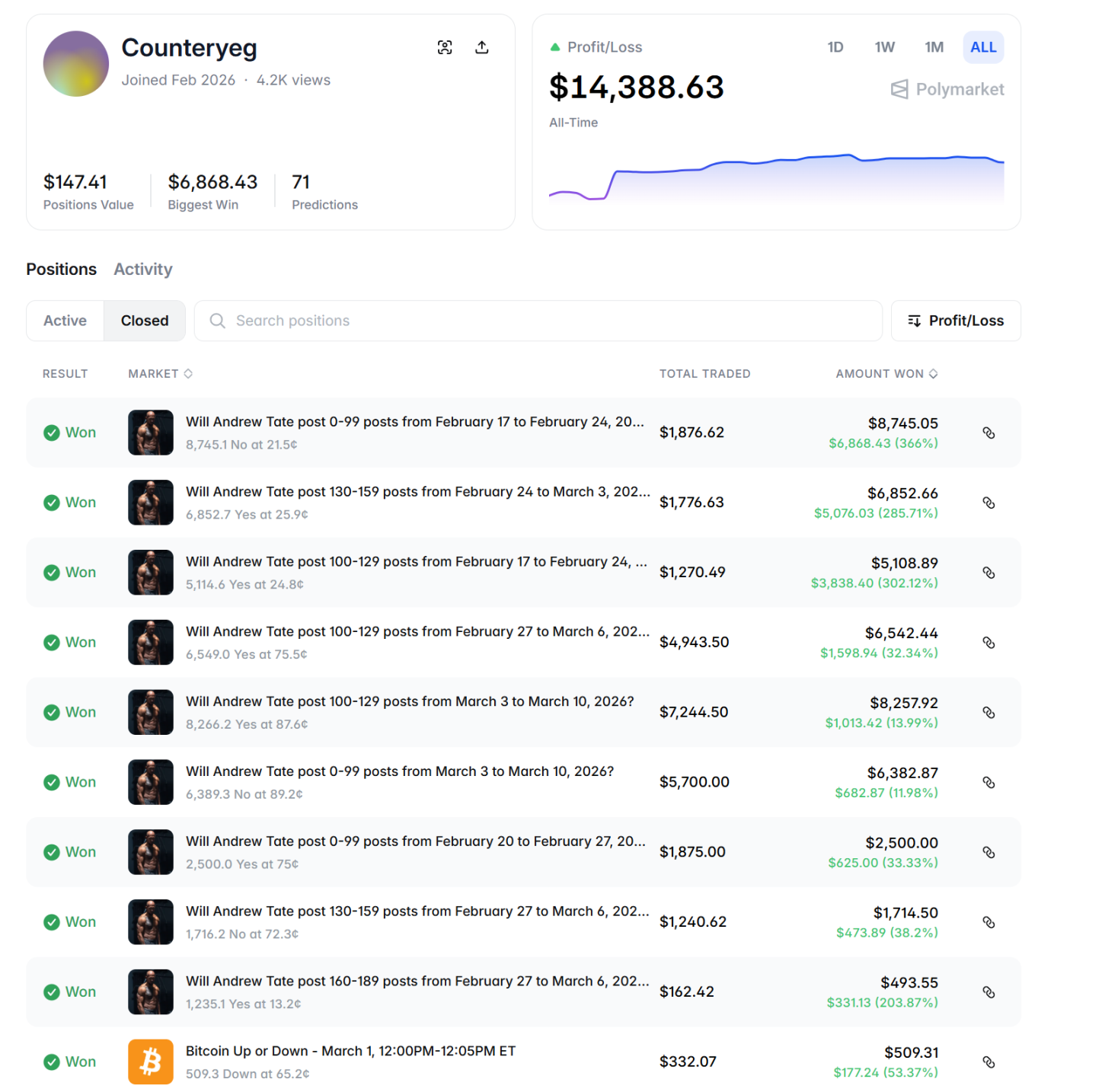

The evidence provided by Euanker shows that the 7 Polymarket accounts (@Tornados, @eterboh5, @Mellisacars, @AntonFuar, @wondernot, @Lindayko, @Counteryeg) were highly consistent in their deposit exchanges, fund paths, and betting habits. The first 5 accounts have been fully linked through on-chain transactions, with the subsequent 2 also showing the same pattern.

The core tracking starts with the @Counteryeg account.

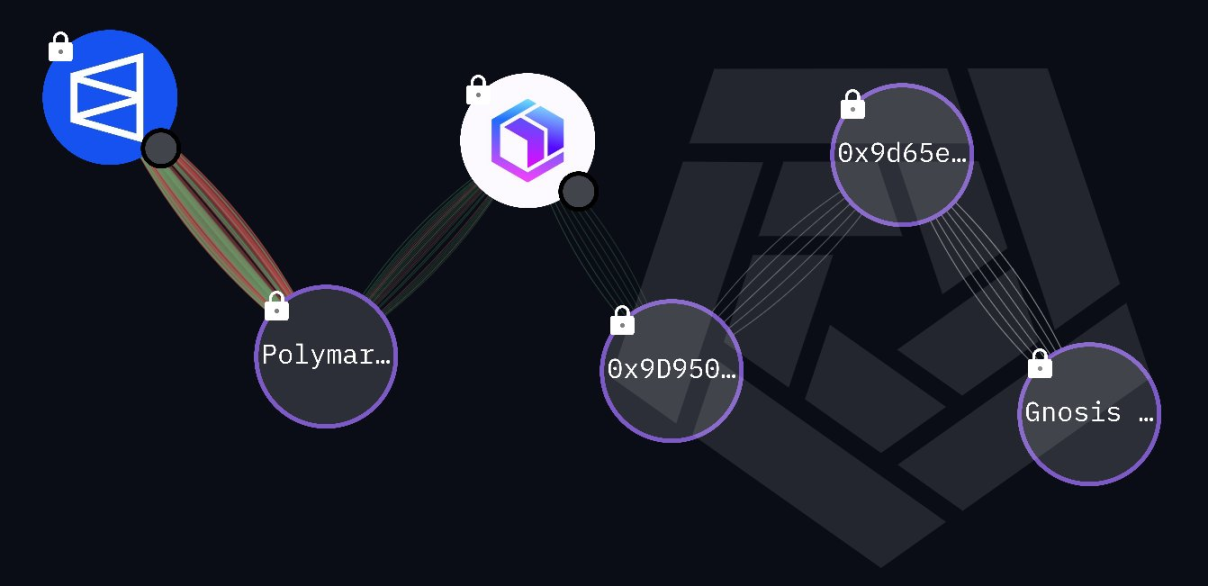

Its fund flow points to the bridging address 0xdae2844d5b3070aafb3638b80fa17e562d840dde. This address frequently conducted cross-chain transfers of USDC and USDC.e in the past week, primarily involving the Polygon and Ethereum networks. These funds were then transferred to the intermediary address 0x9D950Fb9D5F37a128bA0d4B82844DE96697fD83d.

Data from Arkham Intelligence for this address shows that in the past week, it received large USDC deposits from exchanges like Duelbits (a gambling platform), Changelly, and Bybit, accounting for 20%, 42%, and 26% respectively. Typical transactions include a 4000 USDC deposit from Duelbits, a 5700 USDC bridge withdrawal, and multiple transfers of 2500~6000 USDC to the upstream bridging address. The cumulative transaction volume of the address shows that the stablecoin flow rhythm highly coincides with Polymarket betting windows, presenting a unified pattern of 'large deposit first, precise betting second, profit aggregation after'.

The final fund chain points to a Gnosis Safe multi-signature address (confirmed by the exposé and transaction graph as belonging to Tate). Arkham records show this Safe holds over $1.3 million in assets, with recent large USDT/USDC withdrawal operations.

The entire chain forms a closed loop: exchange deposit → bridging address transfer → Polymarket betting → profit aggregation to Tate's controlled Gnosis Safe.

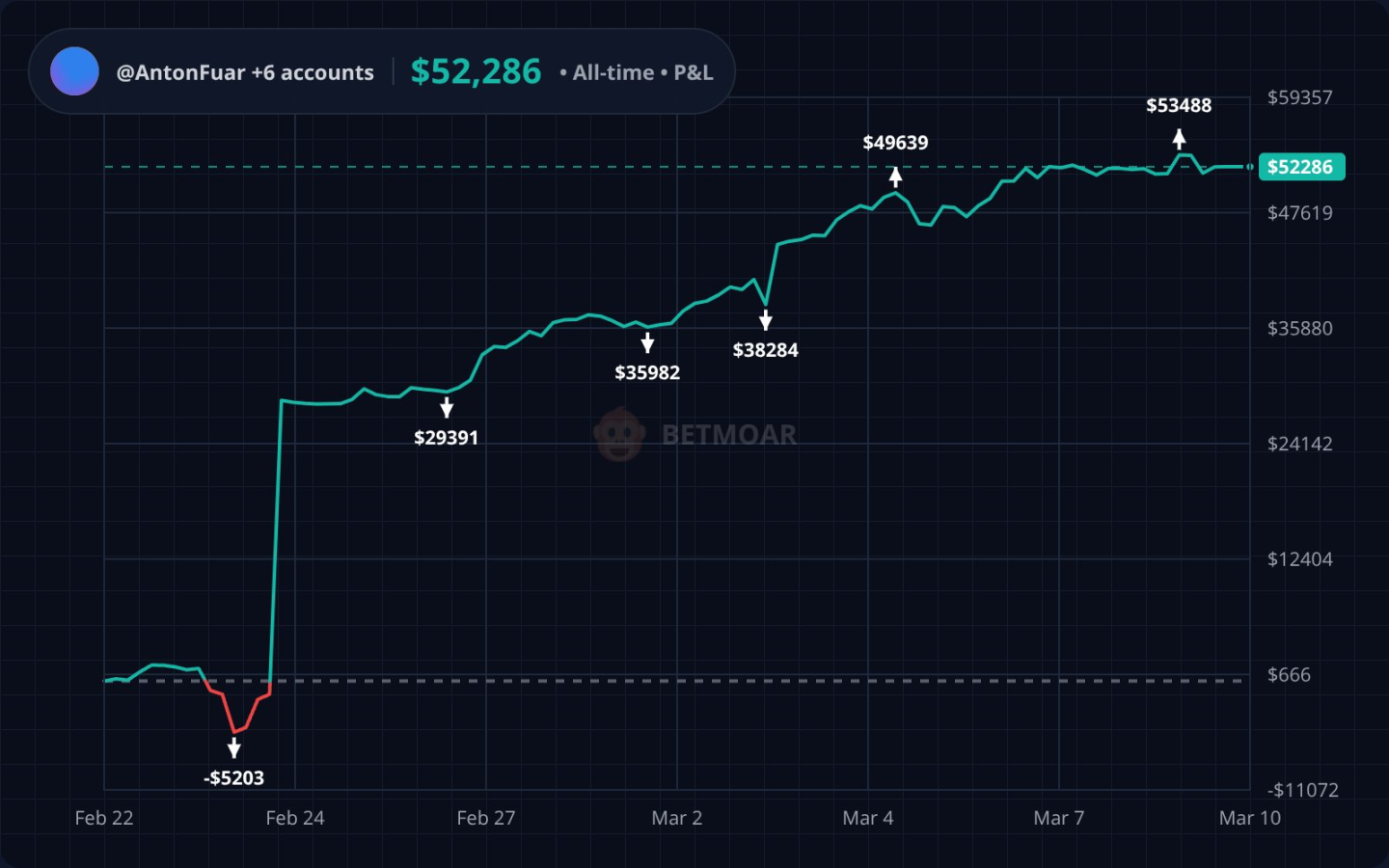

The fund flow chart attached by Euanker clearly marks the Polymarket icon and the Gnosis Safe endpoint. A profit chart of the 7 accounts further corroborates, showing a rapid climb from an initial loss of $5,203 on February 22 to a cumulative peak of $52,286 on March 10, with multiple instances synchronized with Tate's public tweet timings. This level of consistency far exceeds coincidence. The identical combination of exchanges, same USDC bridging scale, and operational patterns precisely matching market settlement times constitute the core on-chain basis for the exposé's insider trading allegations.

From Luxury Cars and Mansions to Meme Coins, Fans Become Tools for Monetizing Influence

Andrew Tate (full name Emory Andrew Tate III), born in 1986, is a public figure, businessman, and former professional fighter with dual US and UK citizenship. Tate began his professional kickboxing career in 2005, winning multiple championships in the late 2000s to early 2010s, including the ISKA British Full-Contact Cruiserweight Championship (2009) and the ISKA World Championship (2011), claiming to be a four-time world champion. He is about 1.91 meters tall, with the nicknames 'Cobra Tate' or 'Top G'.

Andrew Tate has long presented a luxurious lifestyle; his名下 (owned) or rented multiple Bugatti sports cars and numerous mansions have long been the core of his personal brand. The term 'rented Bugatti' in the exposé恰好吻合 (perfectly matches) Tate's publicly flaunted pattern of luxury consumption.

He has repeatedly showcased high-end assets on social platforms, using this to reinforce his 'alpha male' persona and attract young male fans globally. After retiring, he shifted to online business and content creation, launching paid course platforms (like Hustler's University and War Room), teaching topics like wealth building, entrepreneurship, and mindset training, primarily attracting young male audiences.

Starting in 2022, he and his brother Tristan were arrested in Romania, facing charges of human trafficking, rape, and forming a criminal organization (related to recruiting women using the 'loverboy' method to produce adult content); the case is still ongoing. After the Romanian travel ban was lifted in late 2025, the two returned to the US. Currently, he also faces a UK civil lawsuit (four women alleging sexual violence and coercion), which has been moved up to Summer 2026. He denies all criminal and civil charges, calling them a political witch hunt against him.

Upon entering the crypto space, Tate further monetized his influence. He has issued multiple meme coins, the most representative being the DADDY series directly tied to his personal IP, achieving rapid monetization through fan-driven hype. Bubblemaps exposed that he had promoted over 10 shitcoins within 24 hours; after Bubblemaps revealed the insider information about DADDY token supply, Andrew subsequently blocked Bubblemaps.

These operations form a complete闭环 (closed loop) with this Polymarket incident: first, gather traffic with controversial statements and lifestyle, then directly extract funds from fans' wallets through prediction markets or meme coins. Whether it's luxury cars and mansions or meme coin issuance, the essence is the same monetization logic—converting personal fame into quantifiable cash flow.

This exposé once again reminds the crypto industry that prediction markets and the meme coin ecosystem under celebrity influence still have significant governance gaps. This incident points directly to structural deficiencies in Polymarket's market creation review process. For example, markets like 'Andrew Tate's Weekly Tweet Count' are created without effective门槛 (thresholds) to verify whether the market has objectivity or is susceptible to manipulation risk. The core value of prediction markets lies in aggregating分散 (dispersed) information for price discovery, but when the subject is entirely controlled by a single entity, information asymmetry is放大至极端 (amplified to an extreme). Tate could simply adjust his tweet frequency to influence market outcomes, while retail investors bet based on public information, unaware of the internal manipulation.

Previously, the author wrote an article titled 'He Made $300,000 Counting Musk's Tweets'. The prediction market tracked Elon Musk's tweet count; Musk himself is the world's richest man, a hard tech entrepreneur with no motive to profit from insider trading, while Andrew Tate might not be. Polymarket currently does not allow any individual user to directly create prediction markets. All markets are ultimately created by Polymarket's market team. If Polymarket does not strengthen market审查 (review), similar allegations are likely to continue to发酵 (ferment).

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush