Author: @BlazingKevin_, Blockbooster Researcher

Robinhood reached a turning point in its business model in 2025. By developing its wealth management business, including launching disruptive IRA retirement accounts with competitive rates, high-yield cash products, and comprehensive Robinhood Banking services, Robinhood successfully guided its young user base from high-frequency options and cryptocurrency trading towards long-term savings and investment.

In 2025, Robinhood's financial data fully validated the success of this strategy: full-year net revenue reached a record $4.5 billion, a 52% year-over-year increase; full-year net income reached $1.9 billion, a 35% year-over-year increase; retirement account Assets Under Custody (AUC) reached $26.5 billion by the end of Q4, a sharp 102% increase year-over-year; total platform assets reached $324 billion, a 68% year-over-year increase; full-year net deposits reached $68 billion.

This article will analyze the development trajectory of Robinhood's wealth management business in 2025 using data, and explore its strategic advantages across five core dimensions: customer acquisition and asset transfer mechanisms, evolution of the profit model, ecosystem flywheel, brand repositioning, and operational cost structure.

1. Customer Acquisition and Asset Transfer Mechanisms

Traditional wealth management typically relies on financial advisors for high-cost customer acquisition and relationship maintenance, whereas Robinhood adopted a highly internet-based subsidy and incentive mechanism to break down the barriers to asset transfer, thereby rapidly capturing assets under management.

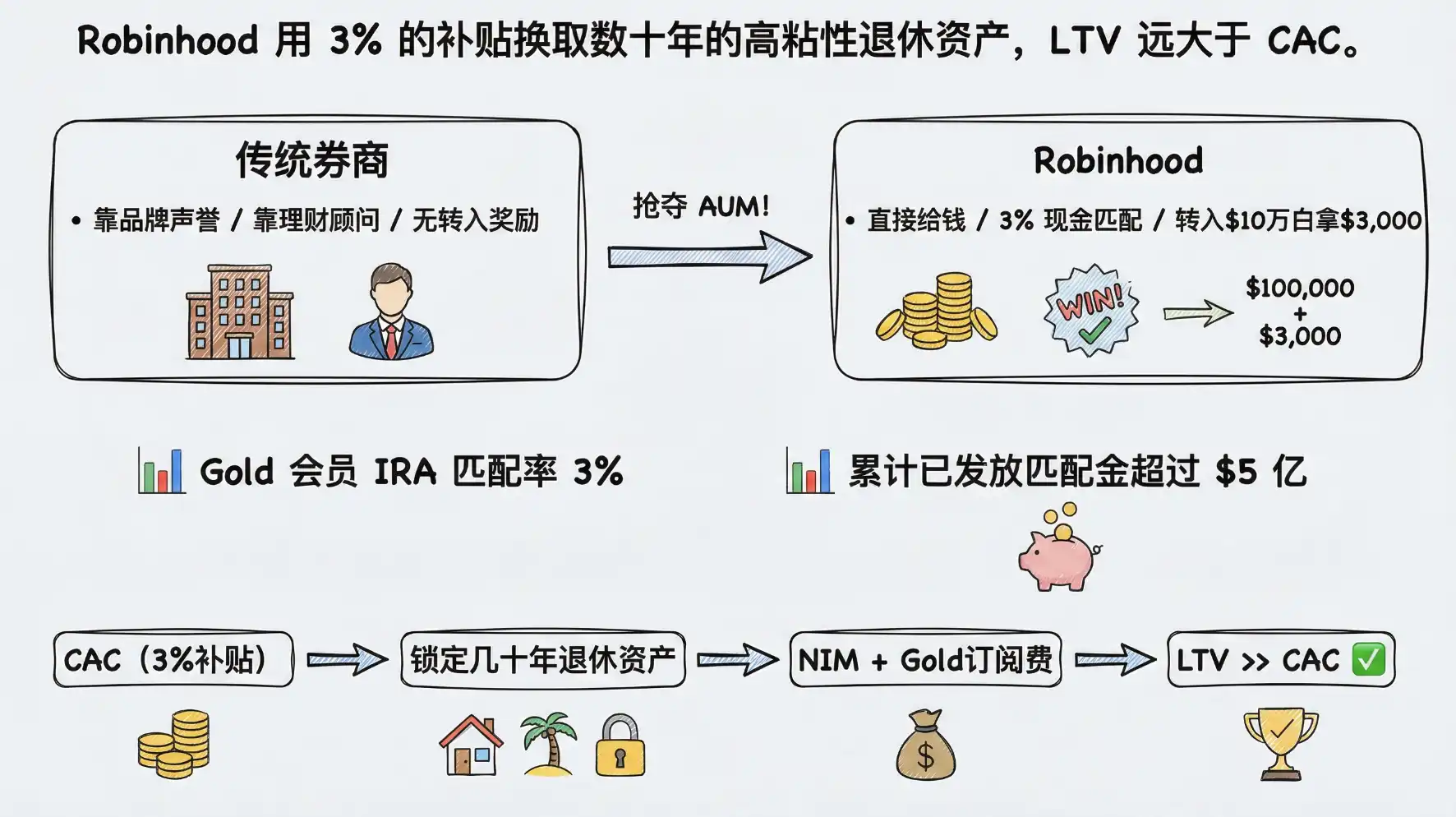

1.1 Match Subsidy: The Economics of "Buying AUM"

Traditional retirement account providers (e.g., Fidelity, Charles Schwab) typically rely on brand reputation and advisory services to attract clients, while Robinhood adopted a more direct and aggressive strategy: cash match subsidies. Using real monetary rewards to lower the psychological cost of user migration.

For Robinhood Gold members, the platform offers up to a 3% match on IRA deposits (1% for non-members). Based on the 2025 IRS contribution limit of $7,000 for individuals under 50, users could receive up to $210 in free matching funds annually. More aggressively, Robinhood also offers a match reward of up to 3% for 401(k) or IRA assets rolled over from other brokerages. This means a user transferring $100,000 in 401(k) assets into a Robinhood IRA could immediately receive a $3,000 cash reward.

Is this economically viable? We can analyze it from the perspective of Customer Acquisition Cost (CAC) and Customer Lifetime Value (LTV). By the end of 2025, customers had collectively received over $500 million in matching funds for retirement account transfers and contributions. This expenditure is treated by Robinhood as a customer acquisition cost. Given the extremely high stickiness of retirement accounts (typically held for decades), these assets not only generate long-term Net Interest Margin (NIM) and potential advisory fees but also lock users into becoming Gold members (annual fee $50). Compared to the often hundreds of dollars in CAC with high churn rates at traditional brokerages, Robinhood's 3% subsidy secures highly sticky assets for decades, with an LTV far exceeding CAC.

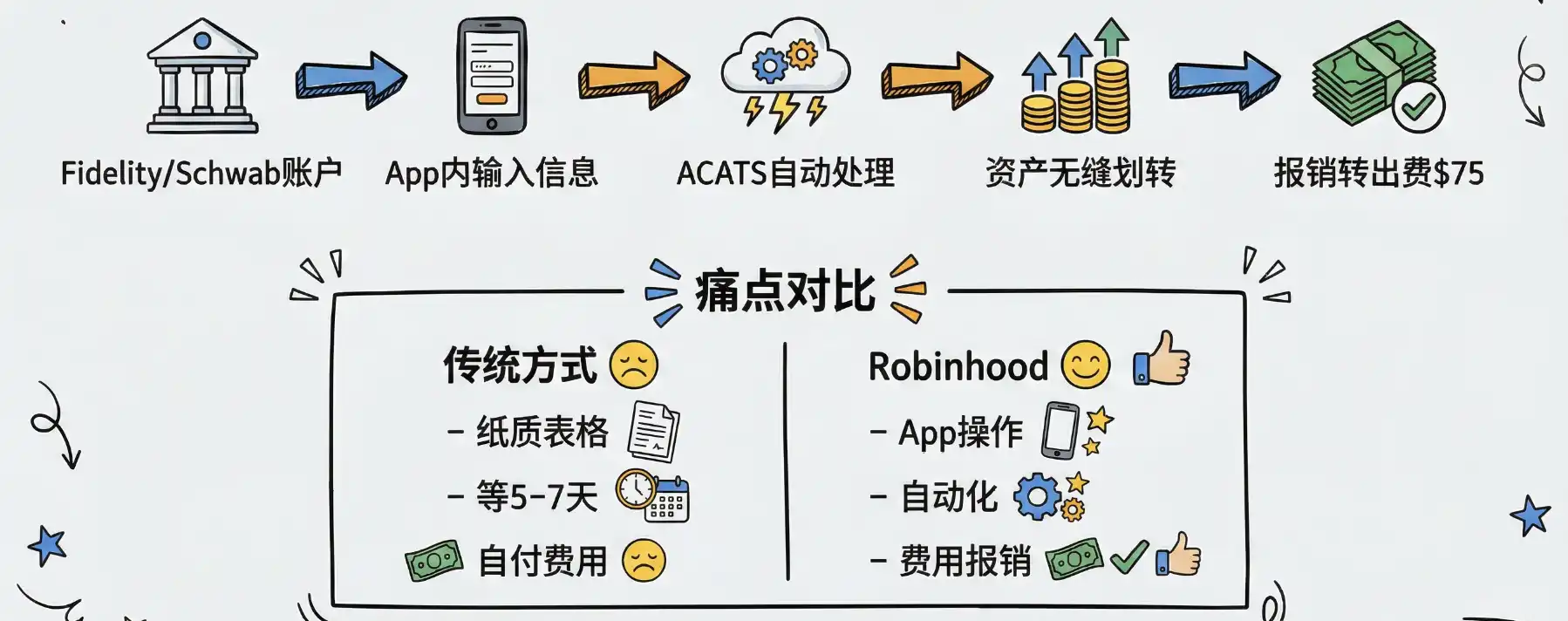

1.2 Frictionless Account Transfer: A Technological Overmatch

Subsidies alone are not enough; if the transfer process is cumbersome, users will still be deterred. Robinhood leveraged technology to significantly lower the barrier for users transferring from traditional brokerages.

By integrating the Automated Customer Account Transfer Service (ACATS), Robinhood enabled seamless cross-brokerage asset transfers. Users simply need to enter their previous brokerage account information within the app, often without manually liquidating existing assets, and Robinhood's clearing system automatically handles the asset transfer in the background. For outgoing transfer fees charged by some brokerages (typically $75), Robinhood also reimburses them if conditions are met. This "one-click move" experience completely dismantles the asset transfer barriers traditionally built on cumbersome processes.

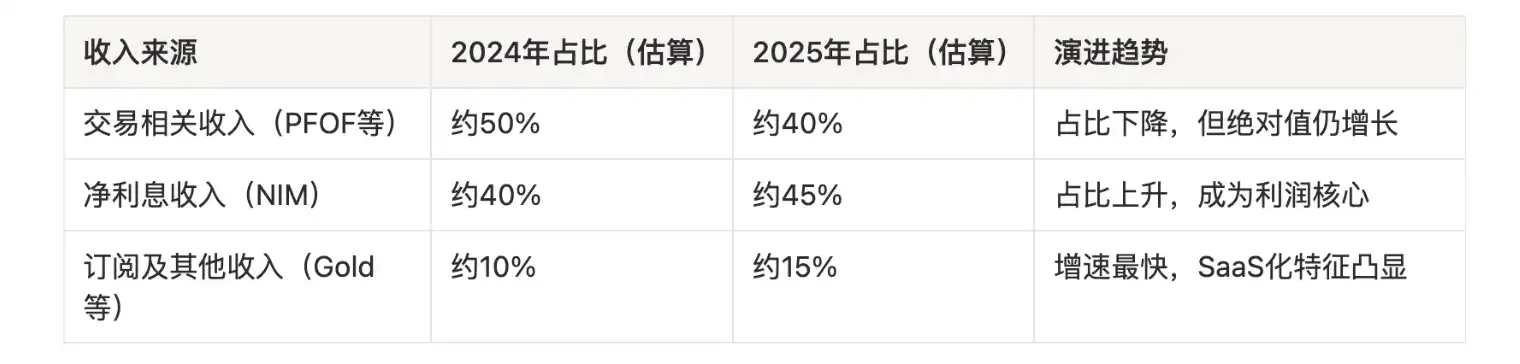

2. Profit Model Evolution: From PFOF to Recurring Revenue

Previously, Wall Street's skepticism about Robinhood focused heavily on its reliance on Payment for Order Flow (PFOF) and high-frequency trading. This model is highly lucrative in bull markets but extremely fragile in bear markets. In 2025, Robinhood successfully evolved towards a more stable asset management profit model.

2.1 Net Interest Margin (NIM): Attracting Deposits with High-Yield Cash

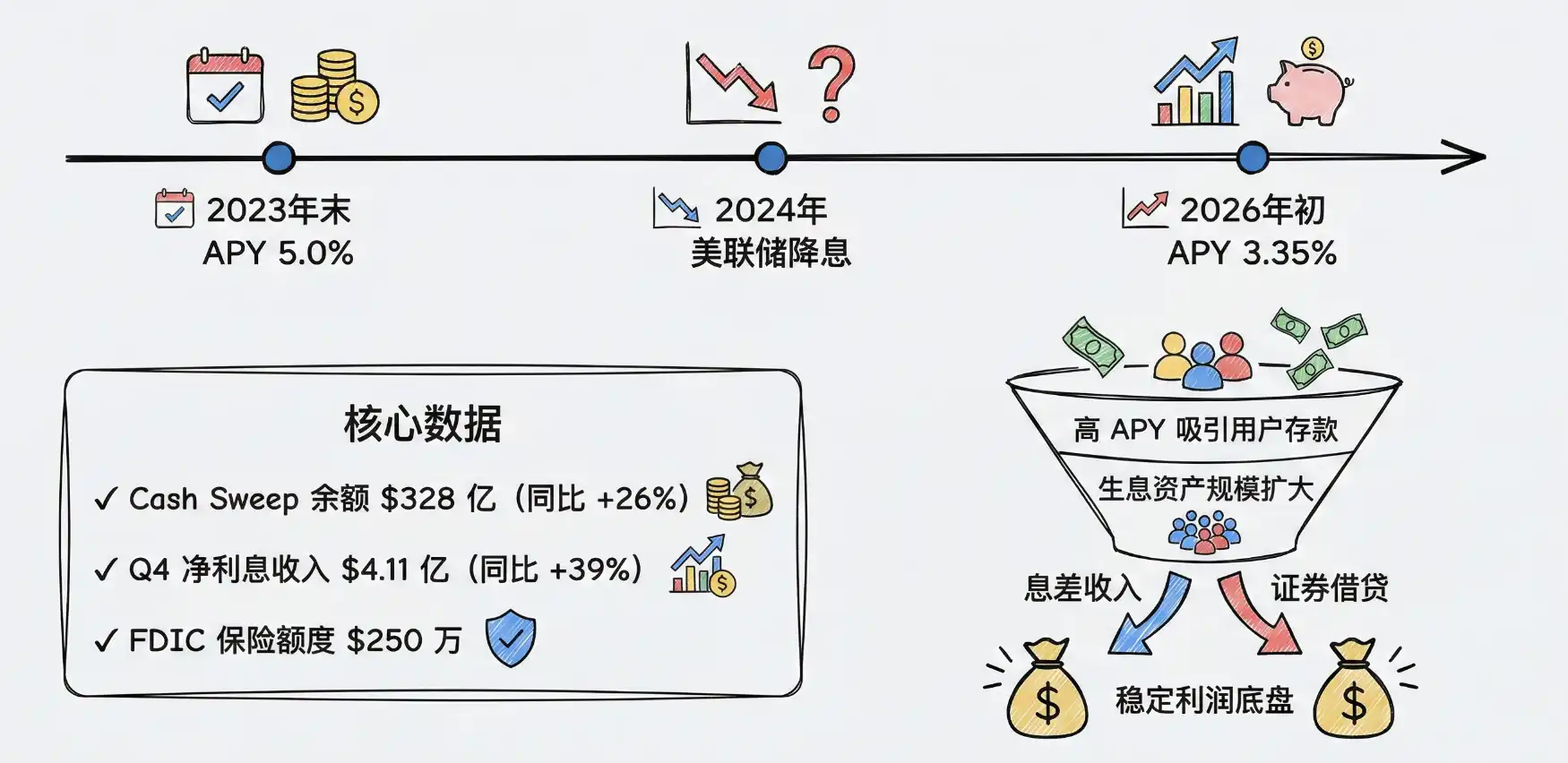

By offering highly competitive cash yields, Robinhood liberated "cash management" from the low-yield trap of traditional banks, thereby attracting massive deposits.

At the end of 2023, the APY for uninvested cash for Robinhood Gold members reached as high as 5.0%, far exceeding the national average savings account rate at the time. As the Fed cut rates, the APY was gradually adjusted (to 3.35% as of early 2026), but it still remained significantly higher than the checking account rates offered by major banks. In Q4 2025, Robinhood's Cash Sweep balance grew 26% year-over-year to $32.8 billion.

This massive pool of interest-earning assets generated substantial net interest income for Robinhood. In Q4 2025, its net interest income grew 39% year-over-year to $411 million, primarily driven by growth in interest-earning assets and securities lending activities. Under specific interest rate cycles, this "earning the spread" model provides a strong profit foundation.

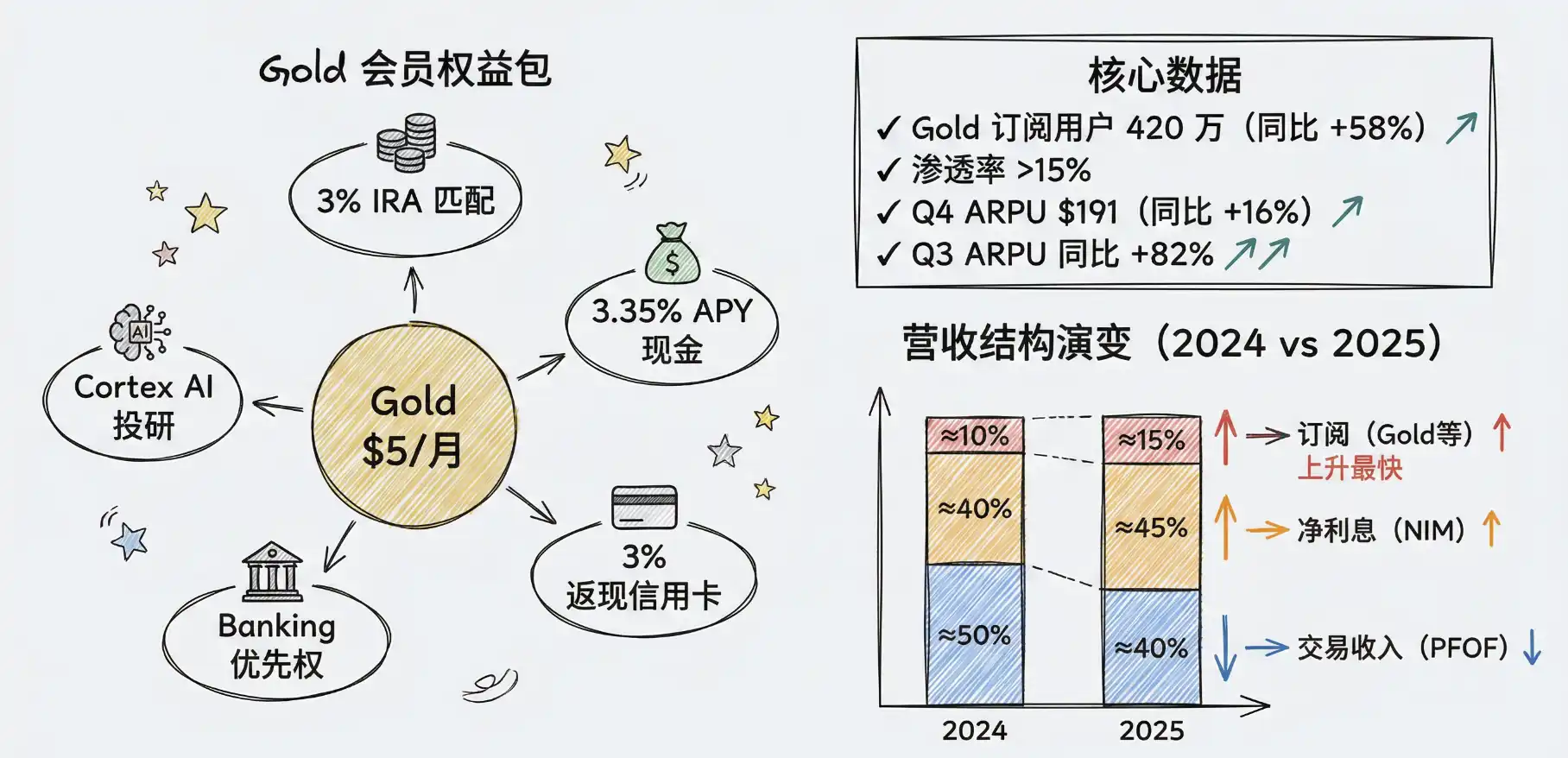

2.2 Subscription Economy (Robinhood Gold): The SaaS-ification of Financial Services

The Robinhood Gold subscription service ($5 monthly or $50 annually) is central to its profit model evolution. It exchanges a monthly fee for high interest rates, in-depth research reports, a 3% IRA match, and a 3% cash-back credit card on all categories. This is essentially an attempt to SaaS-ify financial services.

By the end of Q4 2025, Robinhood Gold subscribers reached a record 4.2 million, a 58% year-over-year increase, representing a penetration rate of over 15% among its 27 million funded customers. This subscription model significantly increases user stickiness and Average Revenue Per User (ARPU). Q4 ARPU increased 16% year-over-year to $191, and Q3 ARPU surged 82% year-over-year.

The table below shows the evolution of Robinhood's revenue structure:

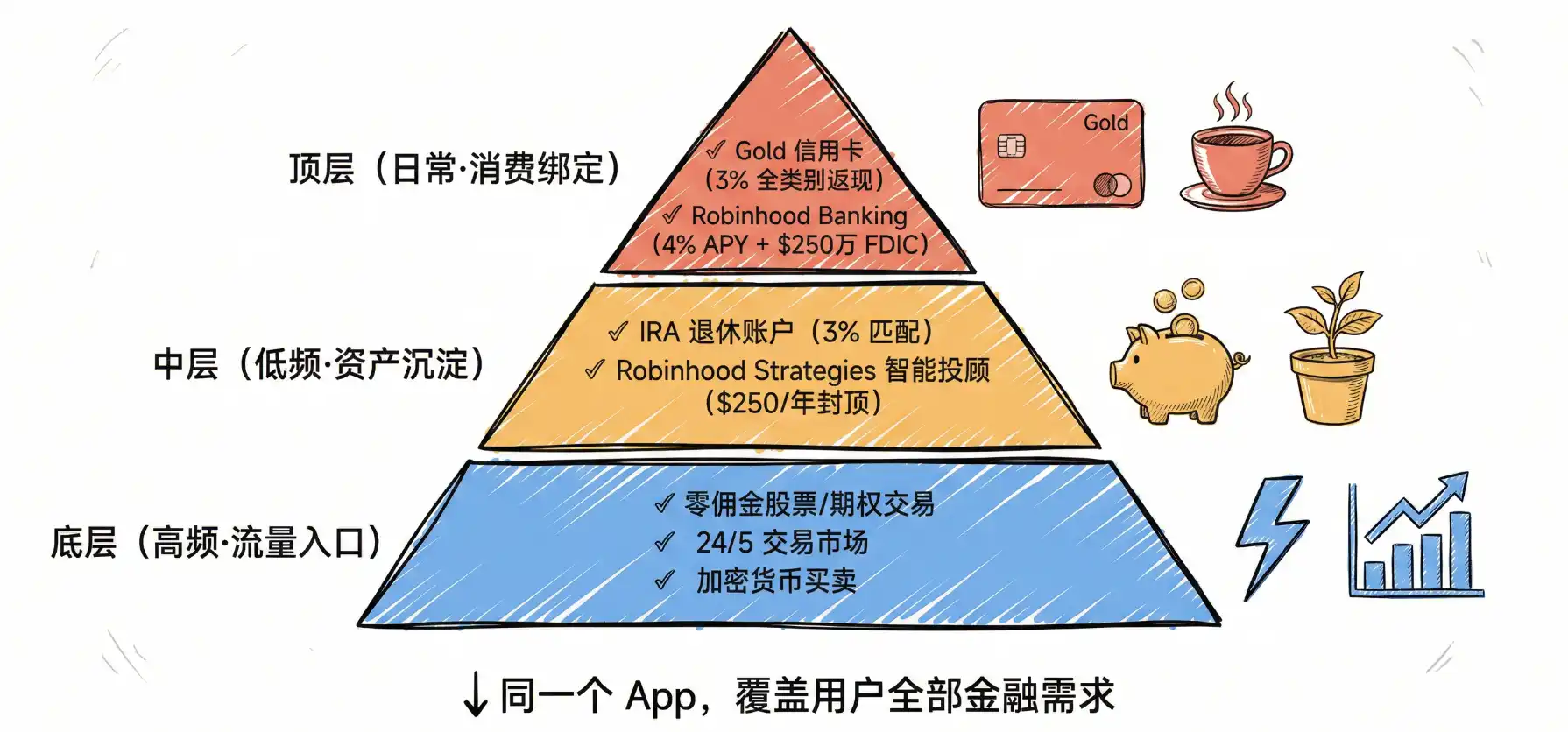

3. The Ecosystem Flywheel

Young users dislike downloading multiple apps to manage their finances. Robinhood deeply understands this and is building a super-app encompassing investing, saving, spending, and borrowing.

3.1 One-Stop Experience: Seamless Integration of High and Low-Frequency Scenarios

In 2025, Robinhood launched or upgraded several products, forming a complete ecosystem flywheel:

- High-Frequency Scenarios: Zero-commission stock/options trading, 24/5 trading hours, cryptocurrency buying/selling.

- Low-Frequency Defensive Scenarios: IRA retirement accounts (3% match), Robinhood Strategies robo-advisory (capped at $250/year management fee for Gold members).

- Daily Spending Scenarios: Robinhood Gold credit card (3% cash back), Robinhood Banking (4% savings APY, FDIC insured).

Seamlessly integrating high-frequency speculative activities with low-frequency retirement investing and daily spending within the same app is Robinhood's killer feature.

3.2 Traffic Conversion: Smooth Cross-Selling from "IPO Investing" to "Retirement Planning"

Robinhood possesses the massive user traffic traditional asset managers dream of (27 million funded accounts by end of 2025). Its core strategy is: use high-frequency trading (e.g., meme stocks, crypto) and high-yield cash as traffic entry points, then smoothly cross-sell low-frequency but high-value wealth management products.

For example, when a 22-year-old Gen Z user downloads Robinhood to trade Dogecoin, they might be attracted by the 5% cash yield to sign up for Gold membership; subsequently, the app will use targeted notifications to inform them, "As a Gold member, you can get a 3% free match by opening an IRA"; when their assets grow to $100,000, the system might recommend "a robo-advisory service for only $250 per year."

This conversion path from "traffic funnel" to "asset沉淀 (precipitation/sedimentation - meaning accumulation)" allows Robinhood to acquire high-net-worth clients at extremely low marginal cost.

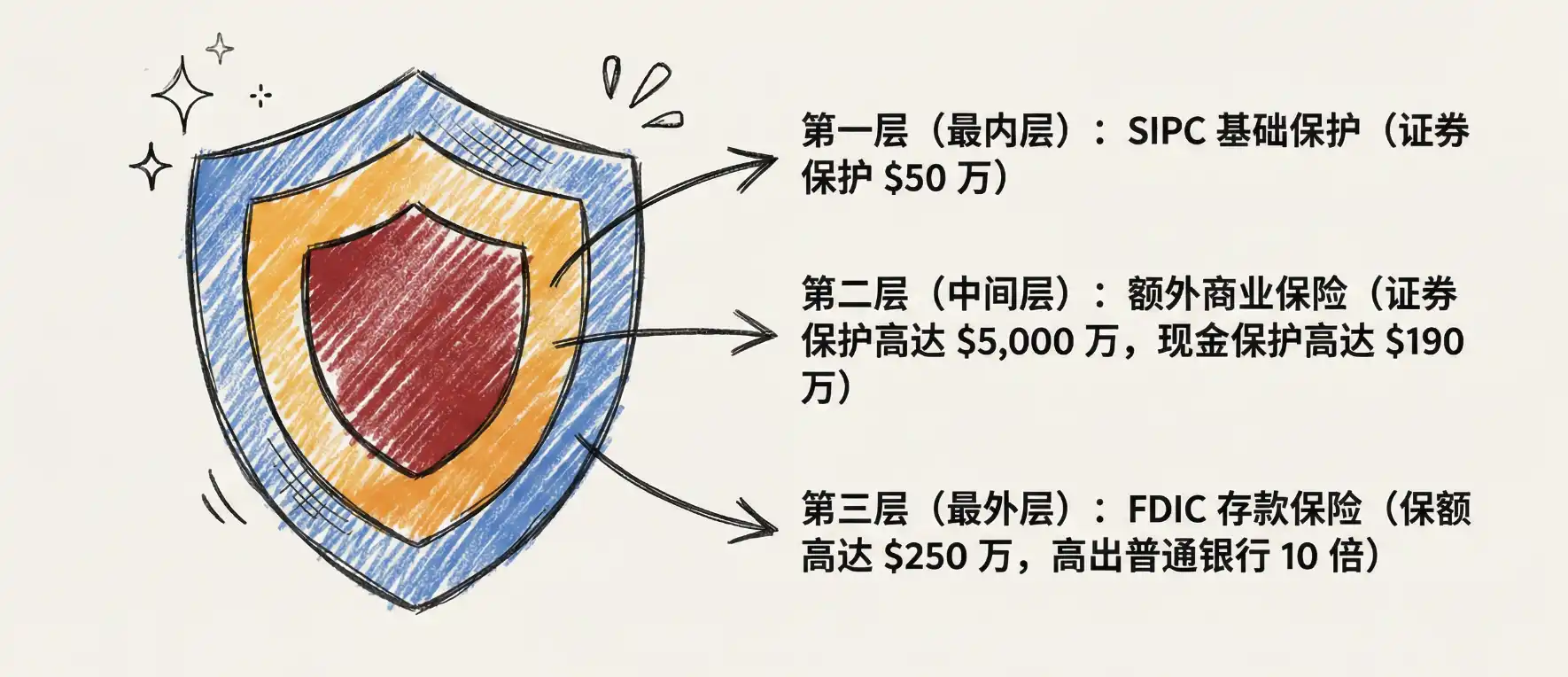

4. Building Trust

4.1 Compliance and Security Endorsement: Leveraging Traditional Finance's Safety Net

To reassure users entrusting their life's retirement funds, Robinhood cleverly leveraged traditional finance's safety net to endorse its innovative products.

SIPC Protection & Additional Insurance: Robinhood emphasizes its status as a SIPC member (providing $500,000 in basic protection) and has purchased additional commercial coverage, offering up to $50 million in securities protection and $1.9 million in cash protection per customer.

FDIC Deposit Insurance: When promoting Cash Sweep and Robinhood Banking, the platform, through partnerships with multiple banks, provides users with FDIC insurance up to $2.5 million, far exceeding the standard $250,000 coverage at ordinary banks.

This narrative strategy of being "safer than traditional banks" greatly alleviates young users' trust concerns about emerging Fintech platforms.

5. Operational Cost Structure

Robinhood's ability to offer a 3% IRA match and capped $250 advisory fees stems not only from confidence in LTV but also from its far superior employee efficiency and underlying technology costs compared to traditional institutions.

5.1 Technology-Driven Automation and High Efficiency Ratio

Robinhood lacks extensive physical branches and teams of financial advisors. All its advisory services (e.g., the ETF portfolios recommended by Robinhood Strategies) are highly automated, relying on algorithmic models for asset allocation and rebalancing.

This "asset-light" model results in an impressive efficiency ratio. Based on public data, Robinhood's total headcount was approximately 2,900 by the end of 2025. Calculating based on the full-year revenue of $4.5 billion, its revenue per employee is as high as $1.55 million. In contrast, traditional financial giants with tens of thousands of employees often have revenue per employee half of this or even lower.

5.2 Decreasing Marginal Costs: The Power of a Proprietary Clearing System

Robinhood freed itself from reliance on third-party clearing agencies (e.g., Apex Clearing) as early as 2018 by building its own proprietary clearing system. This infrastructure investment demonstrated massive operational leverage during the asset explosion of 2025.

When AUC surged from $193 billion to $324 billion, the marginal cost for handling additional transactions and asset transfers was almost negligible because the clearing system is proprietary and highly automated. According to macro trend data, Robinhood's total annual operating expenses for 2025 were $2.379 billion; despite revenue surging 52%, the growth in operating expenses was relatively controlled, directly contributing to a full-year GAAP net income of $1.9 billion and a significant increase in adjusted EBITDA margin.

6. Evolving User Profile

The core driver behind the success of Robinhood's wealth management business is the profound shift in the investment behavior of its young user base.

6.1 Youthful User Base: A Structural Advantage

According to research by ARK Invest, Gen Z and Millennials make up a high 63% of Robinhood's user base, compared to just 14% at Charles Schwab and relatively limited proportions at Vanguard. The median age of a Robinhood user is approximately 32-35 years old (2025 data), while the average client age at Schwab and other traditional brokerages is over 50.

This structural advantage is also reflected in platform asset density. Currently, Schwab's average Assets Under Custody (AUC) per client is around $250,000, far higher than Robinhood's current level of approximately $12,000. However, the essence of this gap is an age gap. As Robinhood's young user base gradually enters their peak wealth accumulation years, this gap will narrow.

6.2 From "Meme Stocks" to "Long-Termism": A Profound Shift in Investment Behavior

Robinhood CEO Vlad Tenev noted a trend occurring in late 2025: 19-year-old Gen Z individuals are actively opening retirement accounts.

This trend is supported by data. According to the latest savings data cited by USA Today, Gen Z's retirement savings rate has risen for several consecutive years, reaching 6.2% in 2025, up from 5.9% in 2024, while the savings rates for all other age groups are declining. Data from Fidelity shows that Gen Z investors allocate a high 95% of their IRA contributions to Roth accounts, indicating a clear understanding of long-term tax optimization.

6.3 Capturing the "Largest Wealth Transfer in Human History"

Over the next few decades, an estimated $124 trillion in assets is expected to transfer from the Baby Boomer generation to Millennials and Gen Z. Given Robinhood's dominant market share among young people, when these young users inherit wealth, they are highly likely to choose to keep the funds within the familiar and user-friendly Robinhood ecosystem rather than transferring them to the traditional brokerages their parents used.

Conclusion: The Rise of a Financial Super-App

2025 was a watershed year in Robinhood's history. It successfully shed the label of a "casino for retail speculation" and transformed into a comprehensive, mature, and highly competitive "financial super-app".

The core logic of this transformation lies in Robinhood's deep understanding of its user base's lifetime value. A 22-year-old Gen Z user might only buy a few ETFs on Robinhood today; tomorrow, they will open an IRA account and enjoy a 3% match; the year after, they will roll over their workplace 401(k) into Robinhood; a few years later, when their asset size grows to $100,000, they will activate Robinhood Strategies for capped-fee professional advisory; ultimately, when they inherit assets from their parents, they will naturally deposit them into Robinhood Banking.

Through aggressive acquisition mechanisms, a stable recurring revenue model, a one-stop ecosystem flywheel, a repositioned brand of trust, and an ultra-efficient cost structure, Robinhood has perfectly prepared its infrastructure to capture this "largest intergenerational wealth transfer in human history."