Author: Darko, IOSG

ETF fund flows are often viewed as a "thermometer" of institutional big money's confidence in Bitcoin. But viewed week by week, they measure something else more: a hidden interest rate trade being turned on and off repeatedly. This article explains how to identify it, how large this trade really is, and why it is quietly unwinding.

TL;DR

-

Week to week, ETF flows are driven primarily by a hidden arbitrage trade, not conviction. Cash-and-carry arbitrageurs buy ETFs while simultaneously shorting futures on the CME, hedging away price risk, but appear indistinguishable from genuine bulls in the data. About half of the weekly flow volatility can be explained by the single variable of new hedge fund futures shorts, with a correlation of 0.70.

-

Bitcoin's weekly price change explains almost none of the flows. Using price returns to predict ETF flows yields a result statistically indistinguishable from zero. Weekly flows are not chasing price performance; they move in sync with a hedged interest rate trade.

-

Arbitrage dominates the weekly "volatility," but never the bulk of the "stock." Of the roughly $55 billion cumulatively flowed into ETFs, the arbitrage trade currently represents a net balance of only about $1 billion; the rest is stable, directional buying, averaging about $400 million per week, which compounded over two years constitutes nearly the entire "mountain."

-

The correct statement is: ETF flows overstate the "volatility" of conviction, not its "level." The weekly ups and downs are mostly "rented"—arbitrage capital coming and going; while the assets that truly settle are mostly "owned."

-

This trade is unwinding, and has been for two years. Leveraged funds' short positions grew from about $3 billion at launch to about $14 billion by late 2024, before steadily retreating to about $4.5 billion. Once the basis compresses to unprofitability, inflows and shorts retreat together—don't mistake the resulting outflows as the market passing judgment on Bitcoin.

I. That Number Everyone Watches

Every week, Bitcoin ETF ETF flows—how much money comes in or goes out—are published, and this number is often treated as a verdict. Large inflows mean institutions are piling in; outflows signal shaken confidence. Flow data has quietly become the market's headline metric for measuring faith.

The problem is, not everyone buying an ETF is betting on Bitcoin. Some of the biggest buyers don't care which way the price goes—and once you account for them, the weekly flow number measures their activity more than anyone's belief. To understand why, you first need to meet a completely different kind of buyer.

A Buyer Who Doesn't Care About Price

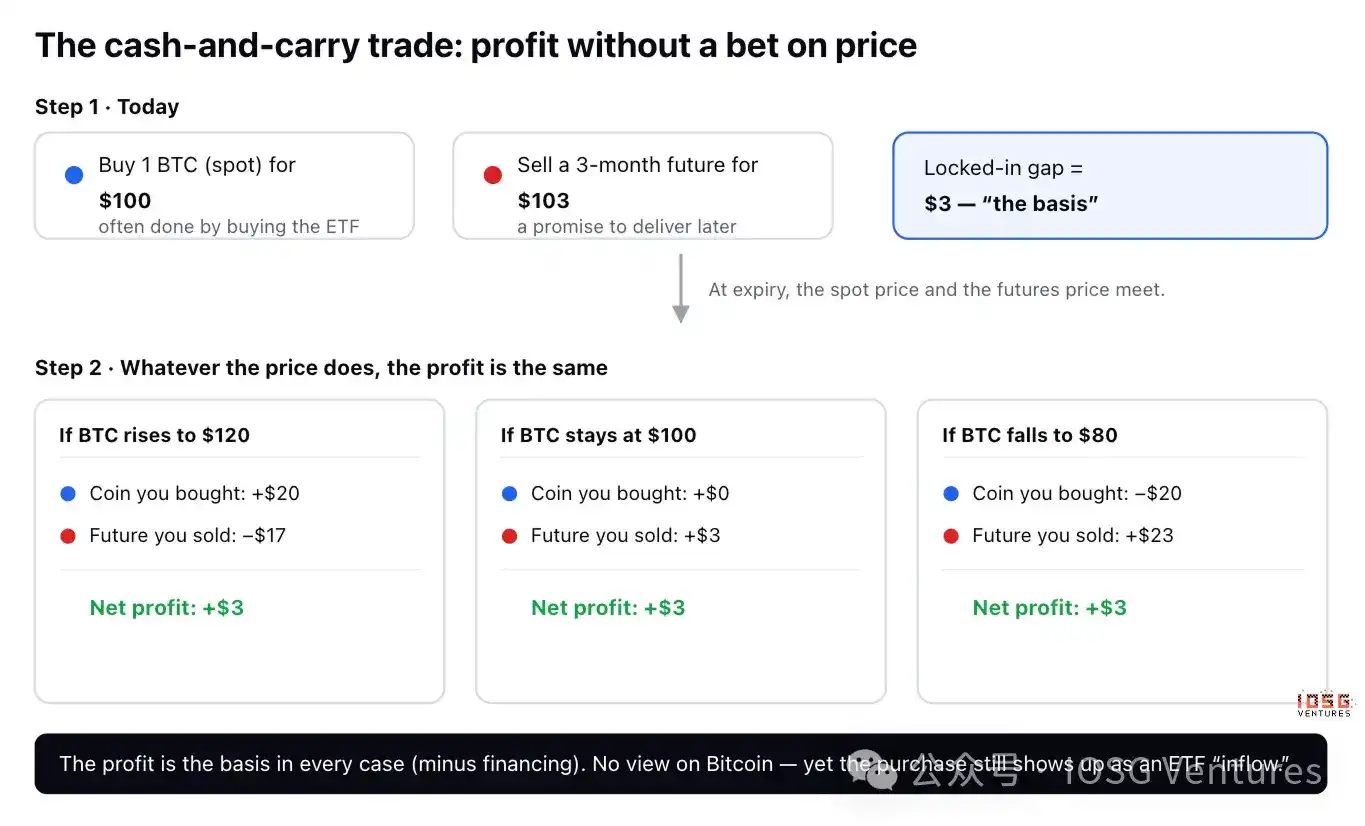

There is a classic, boring trade called cash-and-carry arbitrage. A Bitcoin "futures" contract is just an agreement to buy or sell Bitcoin at a set price on a future date, and most of the time, the futures price trades a bit above the current spot price—say Bitcoin is $100 now, but a contract expiring in three months sells for $103.

A trader can pocket that $3 difference without having any view on price:

-

Buy 1 Bitcoin today for $100 (often done by buying the ETF).

-

Sell a futures contract for $103, promising to deliver in three months.

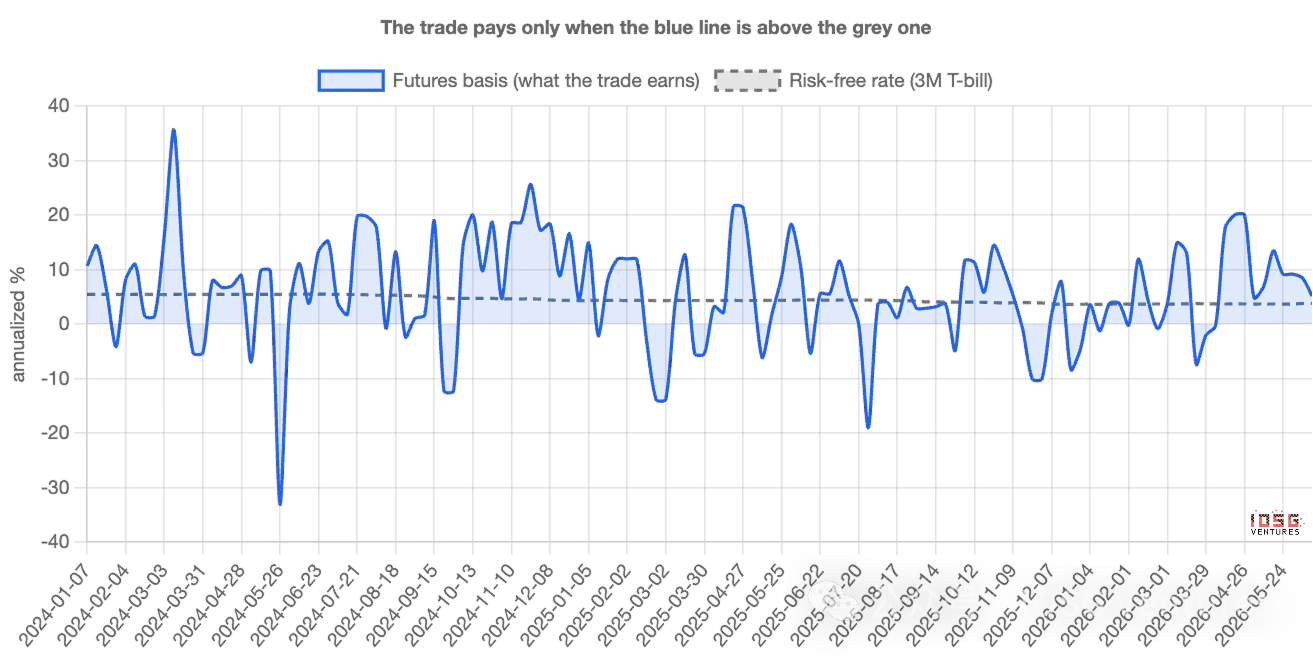

See what happens at expiration. If Bitcoin surges to $120, the trader makes $20 on the coin but loses $17 on the contract—a net gain of $3. If it crashes to $80, they lose $20 on the coin but make $23 on the contract—still a net gain of $3. If it stays flat, still $3. In every scenario, the profit is the same. The direction is hedged away; traders call this "delta neutral." This $3 price difference, expressed as an annualized rate, is the basis—essentially an interest rate earned for parking capital in this trade; it's worth doing as long as it exceeds the risk-free return one could get putting money in US Treasury bills (T-bills).

Why This Pollutes the Headline Number

The key is here. The first leg—buying 1 Bitcoin—is very commonly done by buying the ETF. Therefore, a trader with no view on Bitcoin, running delta neutral, appears in the data as an ETF inflow, indistinguishable on the surface from a true believer.

When lots of cash-and-carry is being set up, inflows look robust, and the narrative of "institutions are loading up" writes itself—even though these funds are hedged and will reverse the moment the trade ceases to be profitable. In other words, the flow number measures not just faith; it measures the activity of arbitrage desks. The challenge is separating the two—and how big each actually is.

How to Tell Them Apart

Cash-and-carry traders leave a second footprint. For every $1 of Bitcoin they buy, they short $1 of futures on the CME (the regulated US exchange where institutions trade Bitcoin futures). True believers leave only the first footprint; arbitrageurs leave both.

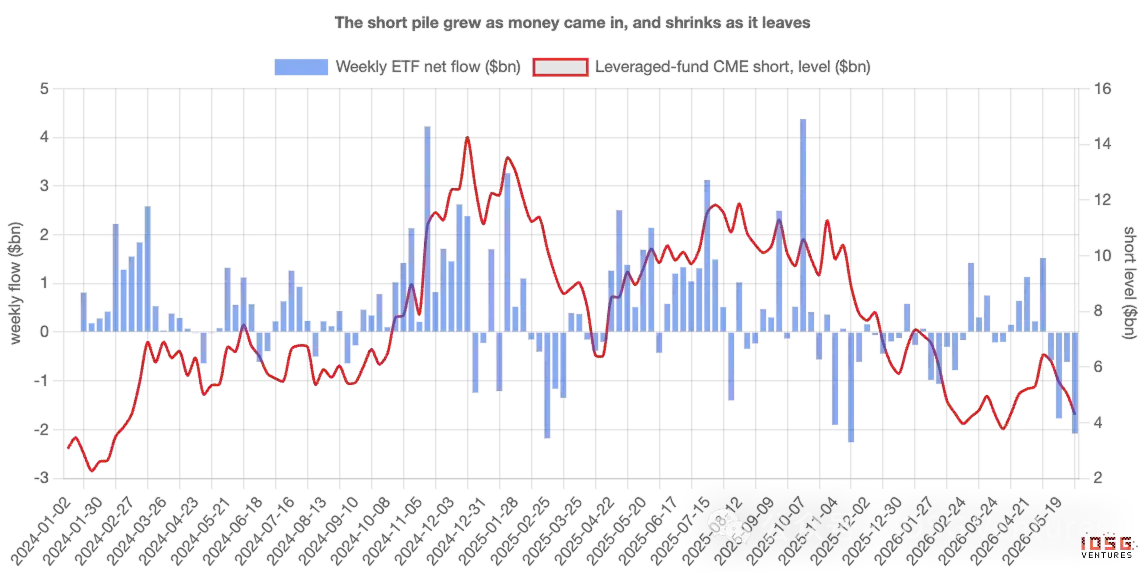

And the second footprint is public. The US derivatives regulator publishes a weekly report disclosing the size of long and short positions held by various trader types on the CME. One category—leveraged funds, essentially hedge funds—is precisely where the cash-and-carry crowd congregates. So you can take, week by week, the money flowing into ETFs and line it up against the new short positions these funds establish. If "demand" were truly conviction, the two shouldn't be closely linked; if a big chunk is that hidden trade, they should move together.

II. What the Data Says: Week to Week, Flows Follow Futures,Not Price

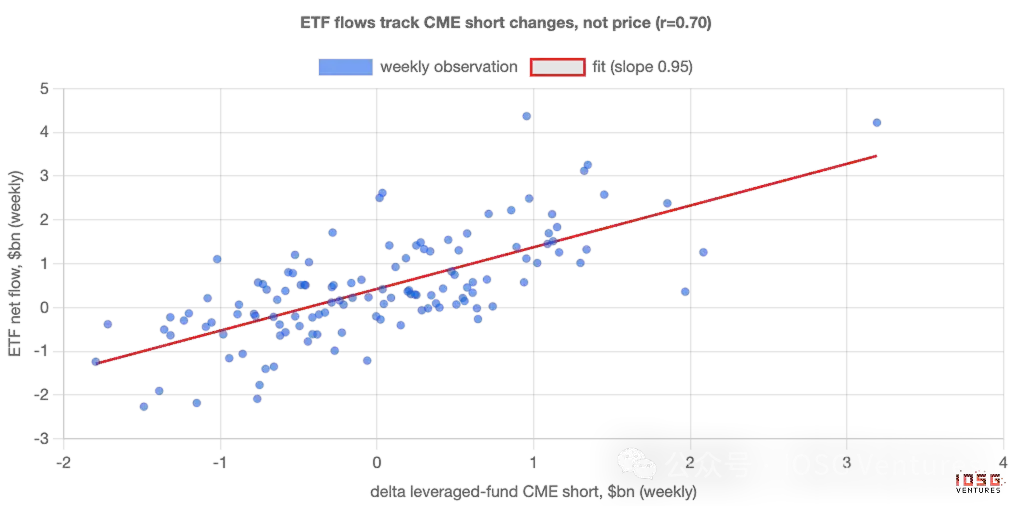

They move tightly together. Every single week since the ETFs launched, the weeks that saw more new futures shorting also saw more ETF inflows—almost one for one. About half of all weekly flow volatility can be explained by this single thing: how much shorting funds did. The correlation is 0.70, the kind of strength you see between two things that are clearly related, not coincidental.

The point that should most unsettle believers: price itself explains almost nothing. Testing whether weekly Bitcoin returns predict ETF flows yields an answer statistically indistinguishable from zero. Weekly money is not chasing performance; it moves in lockstep with a hedged interest rate trade.

So, as a weekly signal, ETF "demand" is mostly arbitrage. The flow number is a poor thermometer for faith because its gyrations are the result of a basis trade being switched on and off, not anyone changing their mind about Bitcoin.

But How Much of the Money Is This Trade?

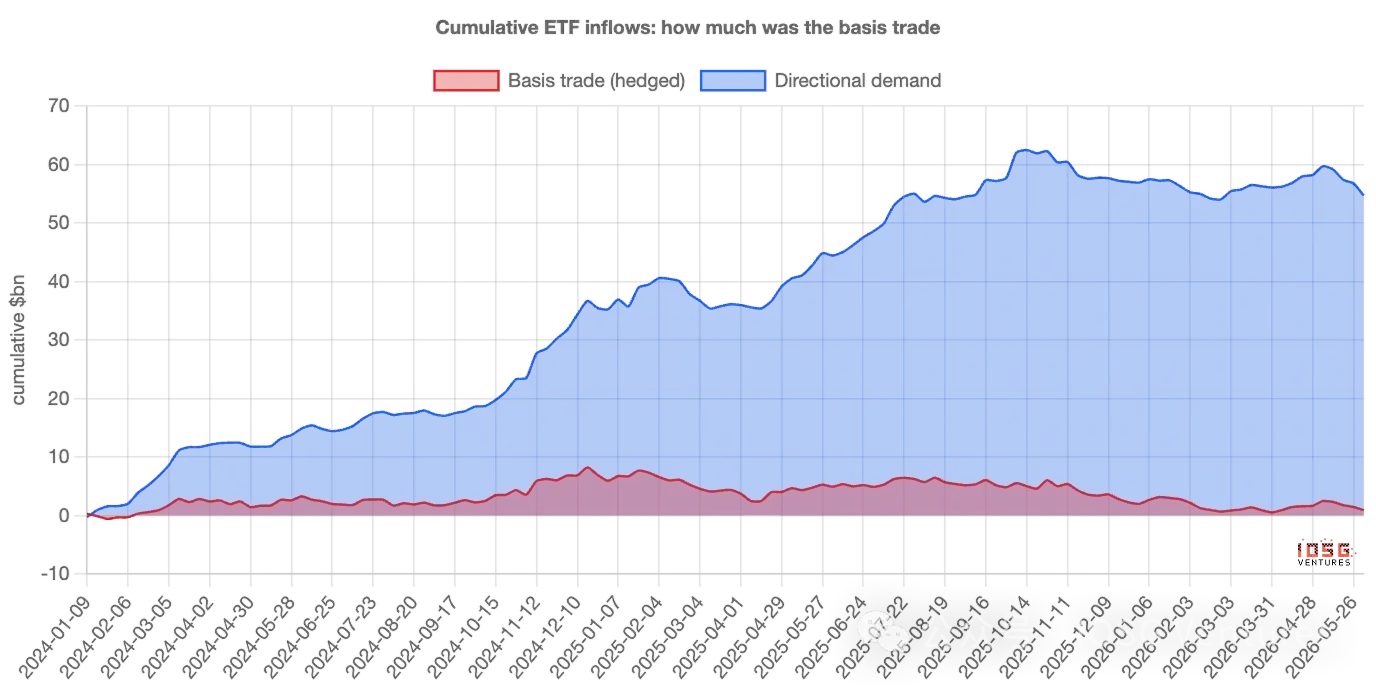

This is where the simplistic narrative—"it's all fake"—falls apart, and the real story gets more interesting. The basis trade dominates weekly volatility, but it never was the bulk of the stock of money.

Breaking weekly inflows into the part explained by futures shorts (hedged) and the rest (directional), and accumulating since launch: of the roughly $55 billion cumulatively flowed into ETFs, the basis trade currently represents a net balance of only about $1 billion—the rest is stable, directional buying. This buying averages about $400 million per week, week after week, regardless of basis or price, and compounded over two years, it is nearly the entire mountain.

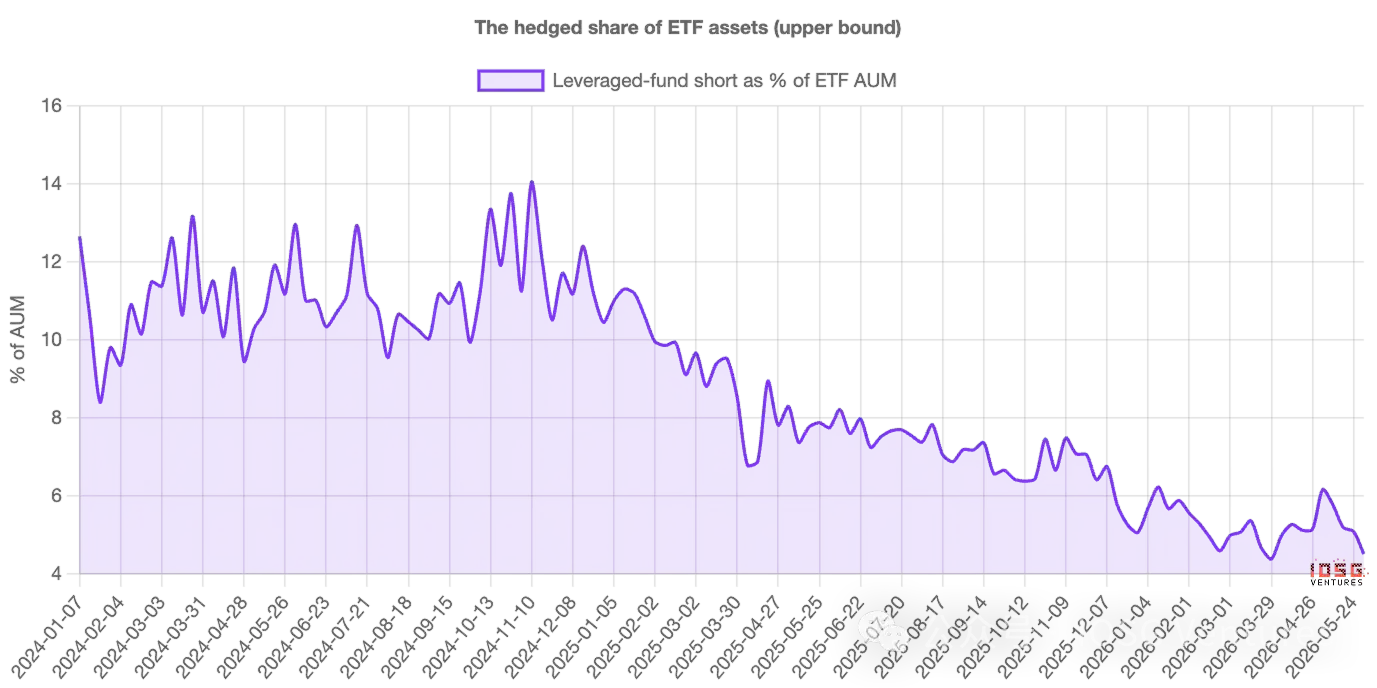

Looking at asset share rather than flows, the picture is the same: the hedged portion once neared 14% of ETF assets in 2024, and is now about 4%-5%. At its peak, it was a non-negligible minority; now it's a sliver.

So, the more precise statement is: ETF flows overstate the volatility of conviction, not its level. The weekly ups and downs are mostly "rented"—arbitrage capital coming and going; but the assets that truly settle are mostly "owned." This trade churns through the flow data but was never the bulk of the balance.

And This Trade Is Unwinding

The hedged portion hasn't just always been small—it has been shrinking for two years. Leveraged funds' short positions grew from about $3 billion at launch to about $14 billion by late 2024, before steadily retreating to about $4.5 billion. This arbitrage trade has been unwinding across the entire period, not just recently.

This matters for reading the present. Entering June, hedged positions roughly halved again—funds' shorts fell from about $6.4 billion to $4.3 billion—while ETFs saw daily outflows of $300-$500 million. On the surface alone, that looks like panic capitulation. But paired with the futures data, it's just the routine cleanup of an interest rate trade that's no longer profitable. The same outflow number, two very different stories.

When the Basis Compresses, Demand Fades

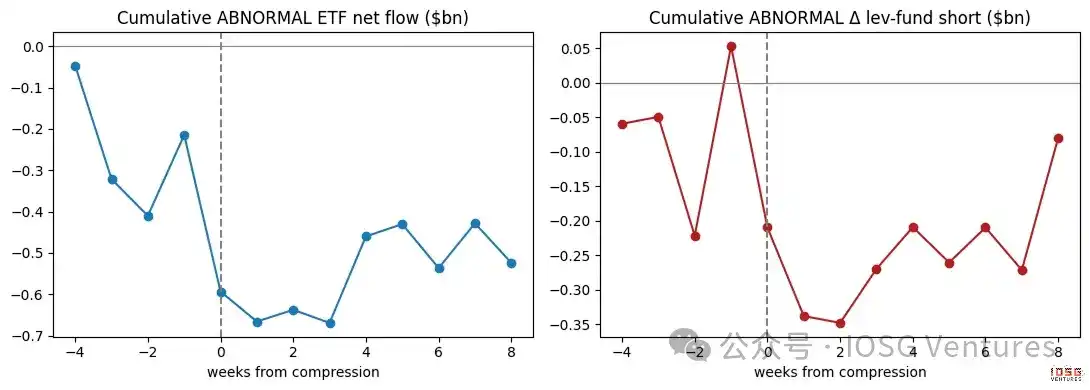

The cleanest proof is what happens when the trade becomes unprofitable. When that $3 price difference narrows to approach what traders could earn risk-free, the trade isn't worth doing. If a big chunk of weekly demand really is this trade, then weekly demand should weaken precisely when the basis compresses—and it does. Stripping trend from each series and looking at moments around a compression: ETF inflows break below their usual rhythm, and funds simultaneously cover shorts, both moving in sync. Demand breathes with the trade.

True believers wouldn't care about futures basis. And this weekly "demand" clearly does.

III. Which Comes First, and Who's Really Operating

First, the relationship is contemporaneous—strongest within the same week, with no clear lead or lag; and the slight directional evidence actually points the opposite way: it's ETF flows that seem to drive shorts, not the other way around. This fits the logic of a paired trade: buy the ETF first, and the futures hedge follows, rather than shorting magically "creating" an inflow. Second, the arbitrage crowd isn't the only driver. Flows follow leveraged funds' shorts most tightly, but they also resonate with directional institutional positions—both types of buyers are active. This article's claim is not that every inflow is hedged; rather, the hedged trade is the tightest, most reliable driver of week-to-week volatility.

Ethereum: The Same Trade, But the Math Hardly Works

Applying the same test to Ethereum ETFs reveals the signature, but weaker—a looser link to futures shorting, and that underlying stable directional buy flow is almost nonexistent. The reason is clear. Holding spot Ethereum instead of futures means forgoing the staking yield Ethereum offers, about 3%–4% annually. After netting this out, Ethereum's basis is often negative—the arbitrage trade often can't even clear its hurdle rate. So Ethereum ETFs have neither strong conviction buying nor robust arbitrage positioning to support them; they are just smaller, noisier cousins of Bitcoin's.

IV. How to Read ETF Flows From Now On

The point is not a call on price, but a method for reading flows. When the basis is rich, expect "institutional demand" to look strong, and largely hedged—don't mistake that strength for faith. When the basis compresses, expect inflows and shorts to retreat together—don't mistake the resulting outflows as the market passing judgment on Bitcoin. The two numbers worth watching are: the level of annualized basis returns relative to T-bill rates, and the net short position of leveraged funds in the weekly CME report. They'll tell you how much of the next "demand" headline is real.

How We Measured It

A few honest limitations. The basis is built from the nearest-month CME futures contract versus spot, excluding the final days before each expiry (where its extremely short tenor turns rounding errors into artificial spikes); building series contract by contract sharpens exact numbers but doesn't change conclusions. The link between flows and shorts is a strong contemporaneous relationship, not proof one causes the other—the key is they are two halves of the same trade. The futures short number is an upper bound on the proportion of ETF buying that is hedged, because some shorting hedges coins held elsewhere.

None of this changes the main story. Week to week, Bitcoin ETF "demand" is primarily a hidden interest rate trade, not faith—flows measure the activity of those arbitraging far more accurately than they measure belief. And that real buy flow is real, patient, and now the vast majority of what remains, because the "rented" part has been going home for two years.