Original Author: Ye Zhen

Original Source: Wall Street News

The US private credit industry is facing a dual squeeze of liquidity contraction and asset revaluation. As investors rush to withdraw funds and major Wall Street financial institutions reduce credit lines, this massive market worth $1.8 trillion is teetering.

According to the Financial Times, private credit giants Cliffwater and Morgan Stanley have recently imposed redemption restrictions on their multi-billion-dollar funds. In the first quarter, these semi-liquid funds faced a surge in withdrawal requests, with the scale of outflows forcing management to trigger "gates" to avoid fire sales of underlying illiquid assets.

While the funding side is under pressure, private credit institutions are also facing tightening from large banks on the financing side. JPMorgan Chase recently notified relevant institutions that it has downgraded the collateral value of some software-related loans in their portfolios. Although this move did not immediately trigger margin calls, it directly reduced the future financing scale available to the relevant funds, marking a comprehensive reassessment of risk exposure in this sector by the traditional banking system.

The core of this two-way squeeze lies in the net asset value (NAV) arbitrage logic. As the value of related assets in public markets plummeted, private credit institutions failed to synchronously mark down their holdings, prompting investors to rush to cash out at the book value, which is higher than the market fair value. This chain reaction, similar to a bank run, not only intensifies the liquidity pressure on funds but also forces the market to re-examine the true pricing of private credit assets.

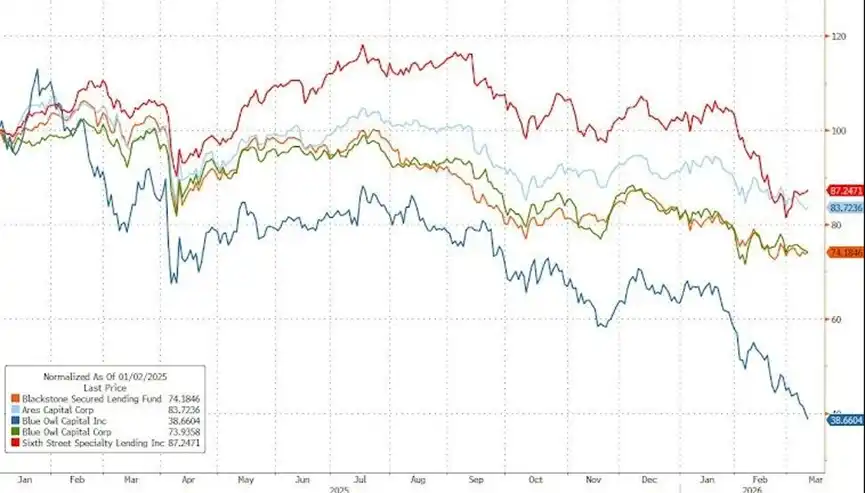

(Private credit company stock prices continue to decline)

Redemption Wave Spreads, Semi-Liquid Funds Face Major Test

According to the Financial Times, Cliffwater restricted redemptions from its $33 billion flagship fund (CCLFX) in the first quarter. The fund received redemption requests accounting for 14% of its total shares, ultimately approving only about half and repurchasing 7% of the shares.

Just hours after Cliffwater took action, Morgan Stanley also notified investors in its $7.6 billion North Haven Private Income Fund that it would limit withdrawals. The fund saw redemption requests jump to 10.9% in the first quarter, ultimately fulfilling only 45.8% of those shares.

This trend has been spreading across the industry in recent months. HPS recently set a 5% redemption cap for its flagship fund targeting high-net-worth clients. Blackstone's Bcred fund fully paid out after redemption requests reached 7.9% of net asset value, while Blue Owl and Ares previously also met high redemption requests, although Blue Owl has imposed a permanent redemption restriction on another fund this year.

Cliffwater raised $16.5 billion last year, expanding at a pace on par with industry giant KKR. However, this model, which relies on independent brokers to manage retail funds, makes it more vulnerable to market sentiment fluctuations.

To address the situation, the report stated that Cliffwater is raising $1 billion by selling loan portfolios and expects to attract $3 billion in new commitments this quarter to offset outflows. The company emphasized in a letter to investors that the fund generated an 8.9% return in 2025 and has a net leverage ratio of only 0.23x, far lower than most similar vehicles.

This capital outflow highlights the risks faced by many new semi-liquid funds, which were originally promoted as a way to invest in private credit but, because their underlying assets are rarely traded, can only offer selling opportunities occasionally.

Overvaluation Triggers Arbitrage, Run Risk Highlighted

The core driver behind investors rushing to withdraw is net asset value arbitrage.

According to a Bloomberg column analysis, software stocks and related debt in public markets have fallen sharply this year, but private credit institutions, which tend to hold loans to maturity, have not synchronously marked down their portfolio valuations.

This lag in pricing creates an arbitrage opportunity. If a fund claims its loan is worth $100, but investors believe its actual market value is only $98, investors will try to redeem and cash out at the $100 book value.

This operation logic triggers dynamics similar to a bank run: if the fund pays out at $100, the asset value of the remaining investors will be further diluted, prompting more people to join the redemption queue. This puts immense pressure on interval funds that promise partial liquidity when facing investors.

To alleviate concerns about opaque valuations, some institutions are trying to increase transparency. John Zito, co-president of the asset management division at Apollo Global Management, said the company is preparing to start reporting the net asset value of its credit funds monthly, with the ultimate goal of achieving daily NAV reporting and introducing third-party valuations.

JPMorgan Takes Proactive Action, Tightens Leveraged Financing

As internal funds drain, the external leverage sources for private institutions are also being tested. According to the Financial Times, JPMorgan proactively downgraded the valuation of some corporate loans in the portfolios of private institutions, primarily concentrated in the software sector, which is considered particularly vulnerable to the impact of artificial intelligence.

JPMorgan has a special clause in its private credit financing business that reserves the right to revalue assets at any time, whereas most other banks typically wait for trigger conditions like interest defaults before taking action. Media analysis indicates this move aims to preemptively compress the available credit lines to these funds, allowing for timely action if necessary, rather than waiting until a crisis erupts.

This tightening action was foreshadowed. JPMorgan CEO Jamie Dimon has repeatedly expressed a cautious stance towards the private credit sector publicly. The bank's executive Troy Rohrbaugh said in February this year that, compared to peers, JPMorgan is becoming more conservative regarding private credit risk. A fund manager also confirmed that JPMorgan has been "significantly tougher" in providing back-end leverage over the past three months.

Industry Expansion Logic Damaged, Subsequent Risks Questioned

The rapid expansion of the private credit industry heavily relies on leveraged financing provided by regulated banks. Since the end of 2020, private institutions have raised hundreds of billions of dollars, quickly gaining the ability to compete directly with banks for large-scale leveraged buyout financing.

However, a large number of underlying assets were formed during the work-from-home boom when software company valuations were high. As corporate cash flow expectations are revised downward, related debts will come due over the next few years, by which time the market environment will be vastly different from when they were issued.

Currently, private credit institutions insist that enterprise software companies are still growing and expect loans to continue performing normally. Although no other banks have explicitly followed JPMorgan's tightening stance, with major banks leading the reassessment of asset values and retail redemption pressure remaining high, the market's scrutiny of the industry's liquidity and valuation transparency is expected to continue intensifying.