Written by: Joel John, Siddharth, Saurabh Deshpande

Compiled by: Saoirse, Foresight News

The crypto market's fear and greed index has hit a historic low. Yet, at the same time, the industry's profitability has reached unprecedented heights.

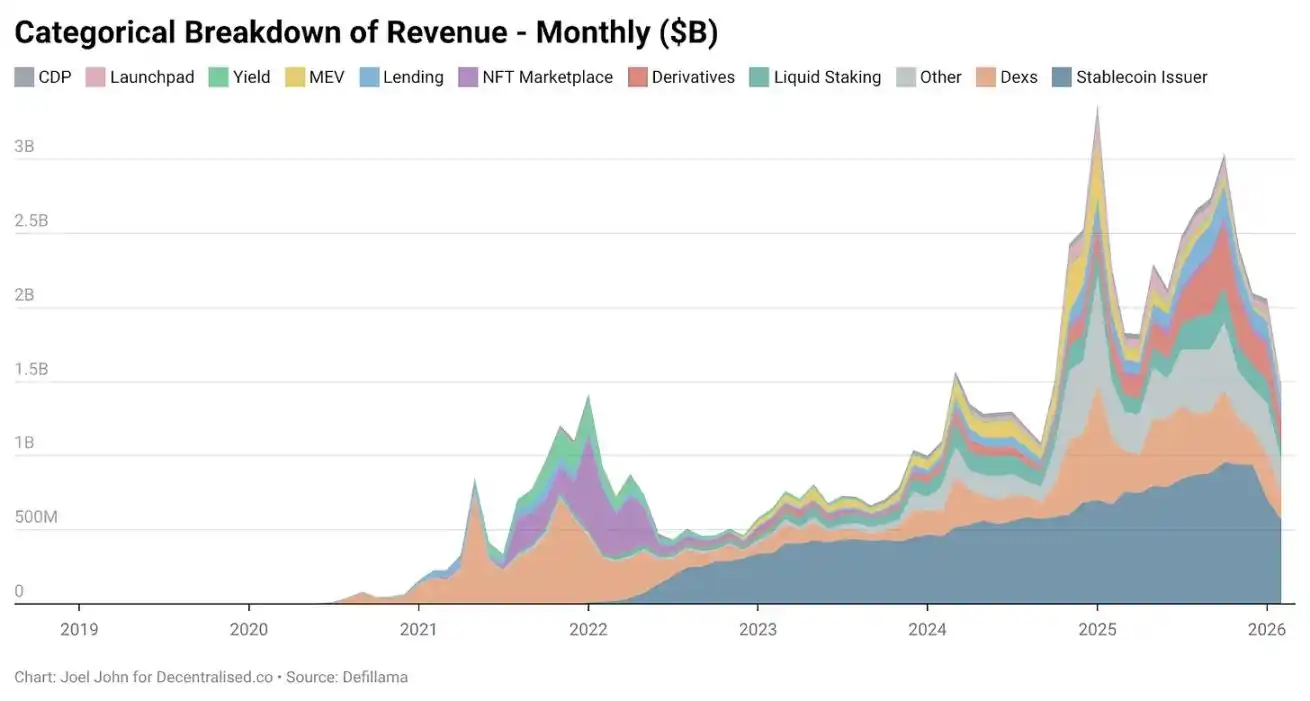

Since 2018, DeFiLlama statistics show that crypto-native protocols have collectively generated $74.8 billion in fees. Nearly half of that—$31.4 billion—was created in the 18 months from January 2024 to June 2025.

Why is everyone still so fearful when an industry is having its best quarters in eight years?

In the past two months, 12 projects have shut down directly: Entropy Protocol, Milkyway Protocol, Nifty Gateway, Rodeo, Forgotten Runiverse, Slingshot, Polynomial, Zerolend, Grix Finance, Parsec Finance, Angle Protocol, Step Finance. These are products built by passionate entrepreneurs we respect, who persevered for years.

OKX, Mantra, Polygon Labs, Gemini, and Binance have also conducted layoffs. Conference attendance is dwindling, VCs are pivoting to AI, developers are flocking to AI. The pessimism in the industry is real. "If you're in crypto, switch to AI quickly" has become the mainstream sentiment.

But should you really switch? We've been pondering this question for the past few weeks.

When a new technology emerges, the market initially gives it an extremely high premium due to its novelty and grand vision. In the 19th century, nearly 6% of the UK's GDP was invested in railway stocks. In 2026, the capital expenditure of hyperscale cloud providers will account for 2% of US GDP.

But when reality sets in, technology valuations rationalize.

What truly matters is: during this return to normalcy, can the industry prove itself useful.

In this article, I will break down:

- How the crypto industry's revenue has evolved;

- How sticky the generated funds are;

- What the industry's true moats are.

Ledger Study: Revenue Landscape Transformed

Since the industry's birth, crypto-native businesses have been making money.

Exchanges like Bitmex, Binance, and Coinbase have long been immensely profitable. But they are centralized, held by a few, and their revenues are not public.

DeFi-native protocols like Uniswap and Aave changed all that. You can verify daily how much a protocol actually earns. Token valuations should reflect the economic activity supported by these foundational components.

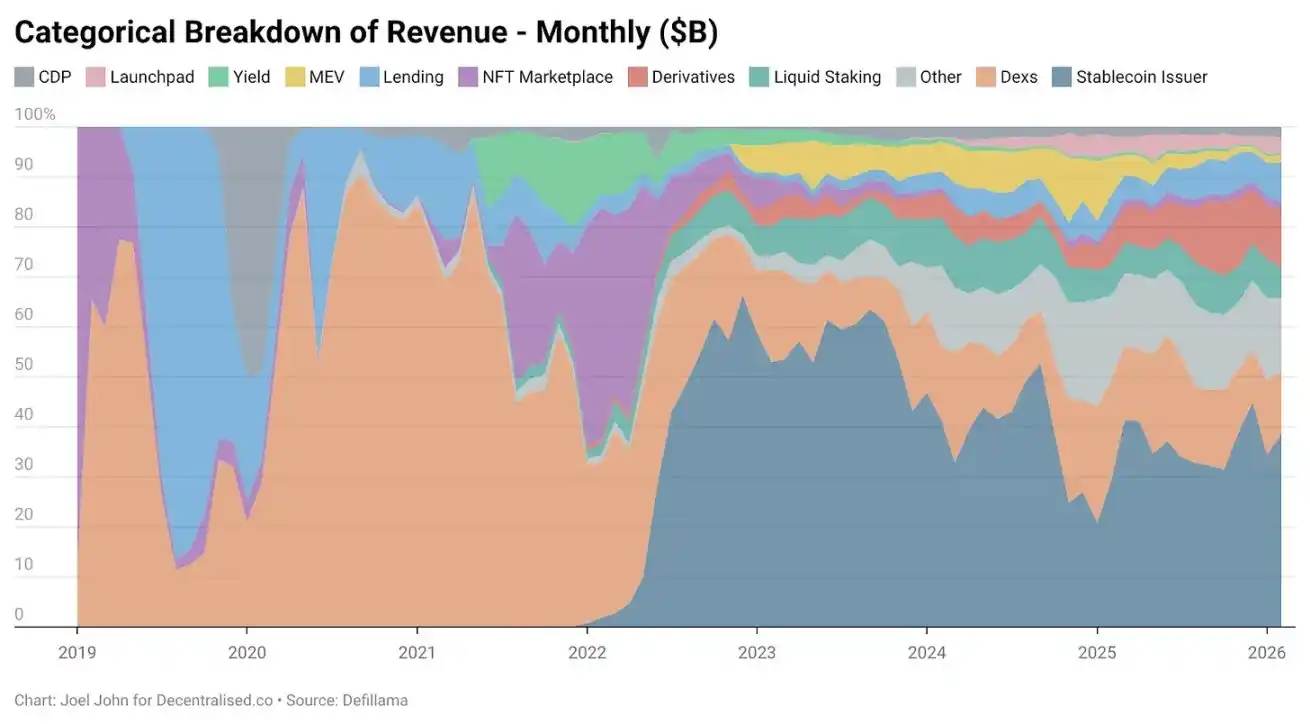

Until 2022, decentralized exchanges accounted for 28.4% of the industry's total revenue, generating $2.27 billion that year. The lending sector was also highly concentrated: Aave and Compound took 82% of lending fees. Back then, people believed: there are leaders in a sector, but long-tail protocols also have room to grow. The technology itself was novel enough to support high valuations.

Then came the phase of crypto expanding to the masses.

NFTs once represented a hopeful vision: cultural value priced on-chain. Celebrities changed their Twitter avatars, ordinary people thought this would bring mass adoption. OpenSea created $1.55 billion in revenue that year, capturing 71.7% of the NFT market.

In hindsight, its $13 billion valuation didn't seem outrageous—it had the potential to become a long-term monopolist.

But fate and the market had other plans.

By 2025, NFT revenue accounted for less than 1%. We experienced a bubble similar to "Beanie Babies," but in the end, we didn't even have physical souvenirs left.

(Note: Beanie Babies are a series of plush toys launched by American company Ty (founded by Ty Warner) in 1993, and were also a famous case of collecting frenzy and speculative bubble in the mid-to-late 1990s.)

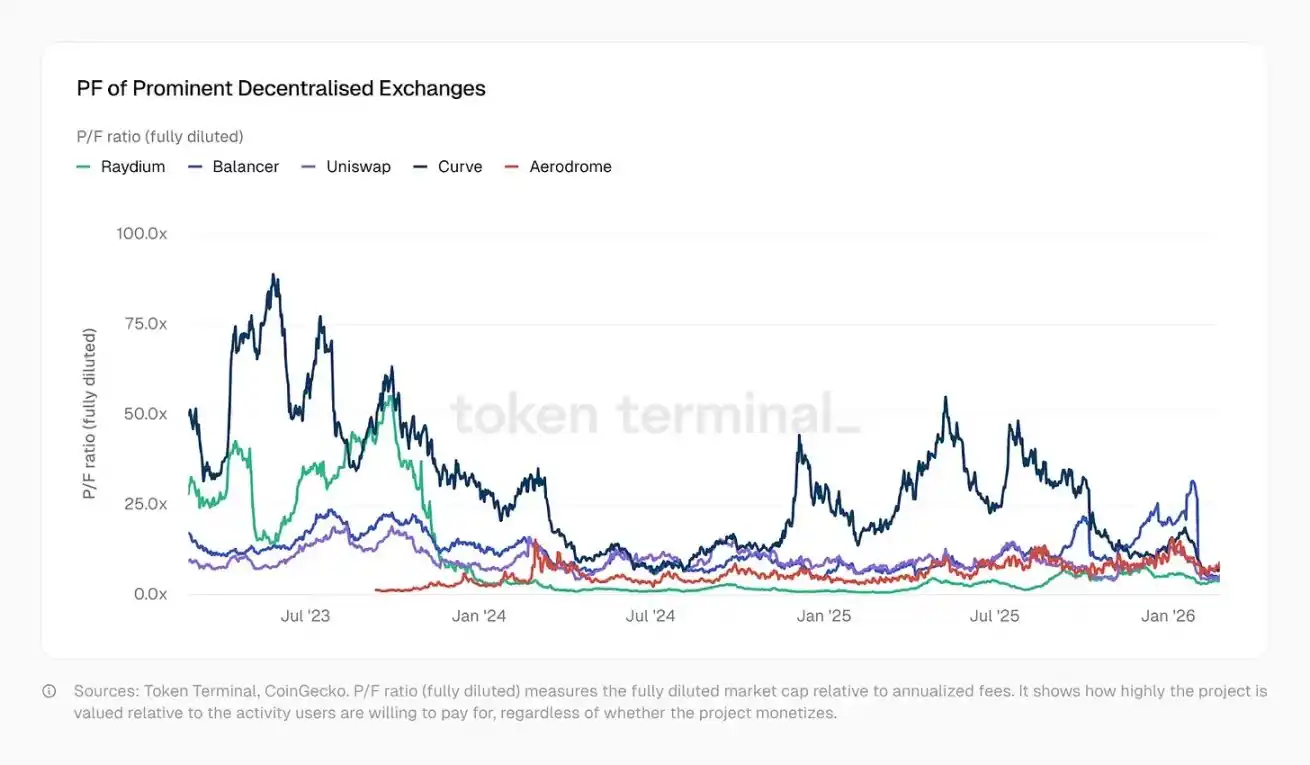

In contrast, decentralized exchange revenue is growing, but valuations have plummeted. Last year, DEXs generated $5.03 billion in fees, lending platforms $1.65 billion. Combined, they accounted for 22.9% of total fees, far below the 33.1% in 2022. Their economic activity constitutes a smaller share of a larger pie, and valuations have shrunk dramatically.

So what is growing?

How has the crypto-native business model evolved from 2022 to the present? The answer lies in the data:

In January 2026, stablecoin issuers Tether and Circle took 34.3% of the entire industry's fees. In other words: for every $1 earned in the industry, 34 cents went into the pockets of these two companies. Their revenue nearly doubled from $4.95 billion at the beginning of 2023 to $9.89 billion in 2025, almost entirely from US Treasury yields.

This is a banking-level financial product, yet it's growing at startup speed. Tether's revenue is almost three times that of Circle's.

Their rise stems from two forces:

- Demand

The Global South has long needed tools to hedge against local inflation and transfer funds freely. The US dollar, even a digital one, fills this gap—local currencies cannot. Capital flight is a necessity, not an add-on feature.

- Cost Structure

Blockchain handles the operational aspects of the stablecoin business. Unlike traditional banks or fintech companies, Tether and Circle don't need to hire proportionally more people as issuance scales. Issuing another $1 billion on-chain, transferring $100 billion between addresses, has near-zero marginal cost.

Demand pulls, costs are pushed extremely low. The combination makes stablecoin issuance one of the most capital-efficient businesses in financial history.

The moat for stablecoins lies in: liquidity, compliance, and the time advantage. Very few issuers survive multiple cycles.

Tether and Circle take nearly 99% of stablecoin issuance revenue. Why? Because they started early. The network effects from being integrated into multiple exchanges create a legitimacy that technology alone cannot achieve. Tether initially launched on the Omni sidechain, slow and clumsy, but it was accessible in OTC desks and exchange touchpoints.

This is a distribution barrier, not a technology barrier. This is a moat that crypto-native entrepreneurs find hard to replicate with code alone.

New Growth Engine: Trading Apps Explode

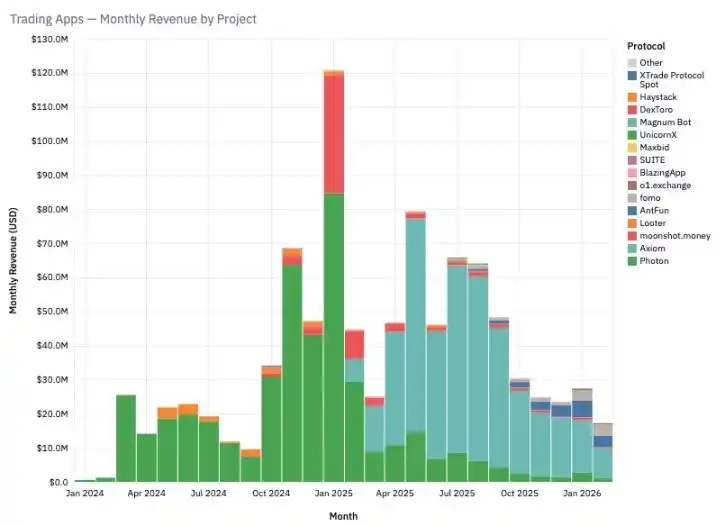

We mentioned in previous articles: crypto is essentially a trading economy. But we didn't anticipate then: products based on Telegram trading bots and trading interfaces would grow this fast.

In January 2025, these two sectors alone generated $575 million in fees in a single month. The reason is simple: this is what users actually want.

Meme coin trading, perpetual futures exchanges, allow users to profit quickly. In pursuit of high returns, they are willing to pay high fees.

From 2022 to 2025, this sector soared from 1% of total revenue to over 15%.

Products like TryFomo and Moonshot, focused on end-users, have made millions. Technically not complex, the key is: aggregating and packaging crypto-native foundational components to create a better user experience. As tools like Privy mature, developers no longer need to incentivize liquidity or worry about wallet management. The foundational components we were excited about in 2022 are now mature. Applications like BullX and Photon are built on top of them.

From January 2024 to February 2026, this sector created $1.93 billion in fees. But meme assets have a fatal flaw: they are lightweight applications, extremely seasonal.

Does this sound familiar?

NFTs and Web3 games also experienced similar explosions, then collapses. This cyclicality is both a bug and a feature of the industry.

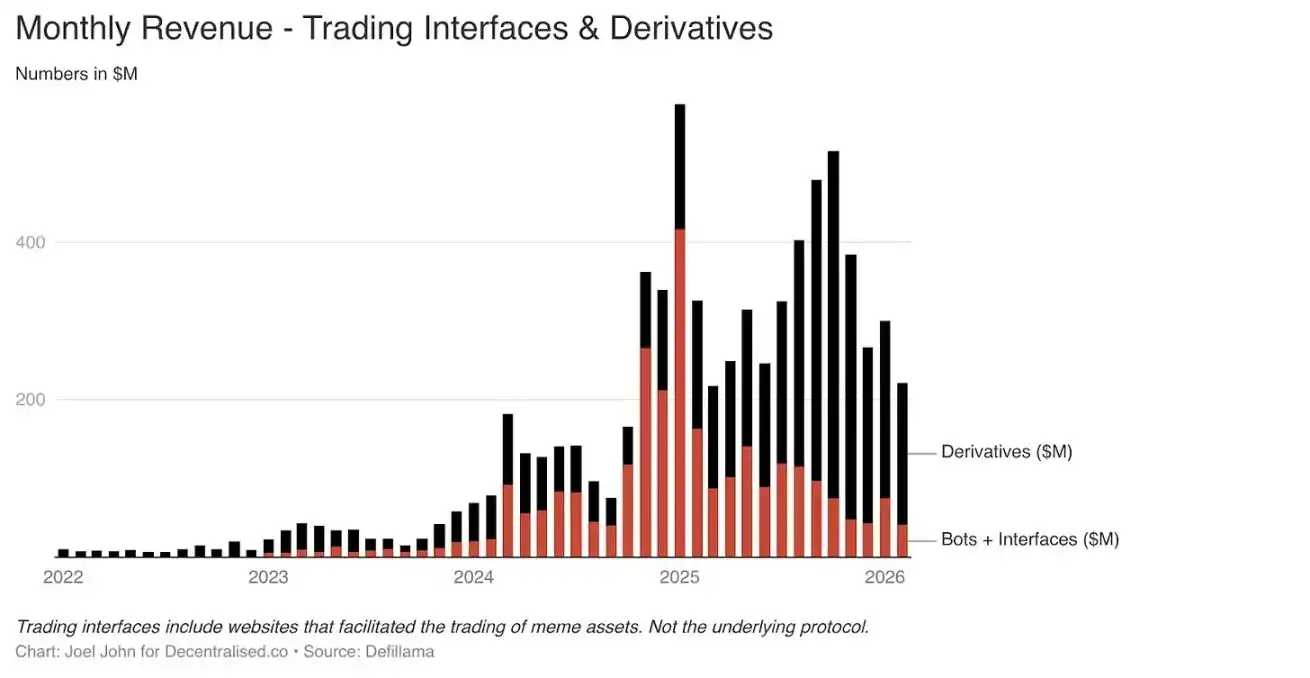

Perpetual futures exchanges (and later prediction markets) represent a more durable new direction.

PumpFun democratized asset issuance through meme coins, but the game wasn't fair. Eventually, the market woke up: meme coins die.

The dream of getting rich overnight by buying a funny token shattered. People don't want to manage a bunch of random tokens; they want risk exposure.

Perpetual futures provide that.

You can trade Bitcoin, Solana, Ethereum with high leverage. Market makers and traders needing alternatives to centralized channels flocked in. The core of this category is liquidity.

Hyperliquid became the leader because its order book depth rivals centralized exchanges. Without this parity in experience, users have no reason to migrate. Over the past three years, Hyperliquid and Jupiter took the majority of fees in this sector.

Perpetual futures exchanges and trading platforms tear off the industry's fig leaf: the real way to make money is by taking small fees from high-frequency trading. Meme trading platforms and perpetual exchanges are "dopamine machines" that package and sell risk. Some of these will mature into core financial infrastructure—allowing the world to trade commodities, stocks, and digital assets even on weekends in the future.

Blockchain-native applications replicate what Robinhood and Binance already provided: access to risk.

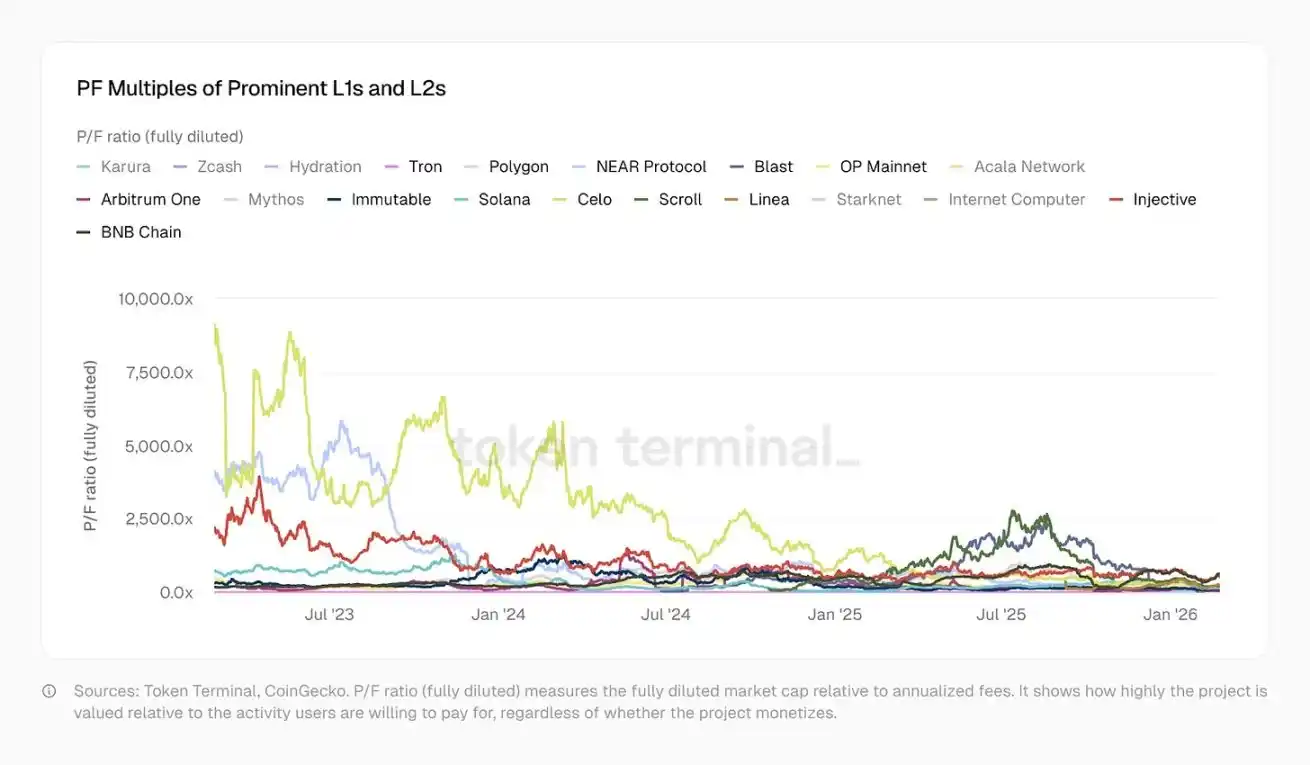

Hungry Fat Protocols: Public Chains & DeFi Valuations Plummet

So far, I haven't mentioned the underlying public chains. Because their story is completely different: they are victims of the novelty premium and are now moving towards a discount.

January 2023:

- Optimism Price-to-Fees (PF) Ratio: 465x

- Solana: 706x

- Arbitrum, BNB: ~206x

Today:

- Solana: 138x

- Arbitrum: 62x

- OP: 37x

- Polygon: only 20x, approaching traditional fintech companies

- Tron, which supports the stablecoin ecosystem, is only 10.2x

These public chains have supported more complex products over these years, with more users, better liquidity, and richer financial applications. But their Price-to-Fees ratios have significantly declined, reflecting a shift in market sentiment.

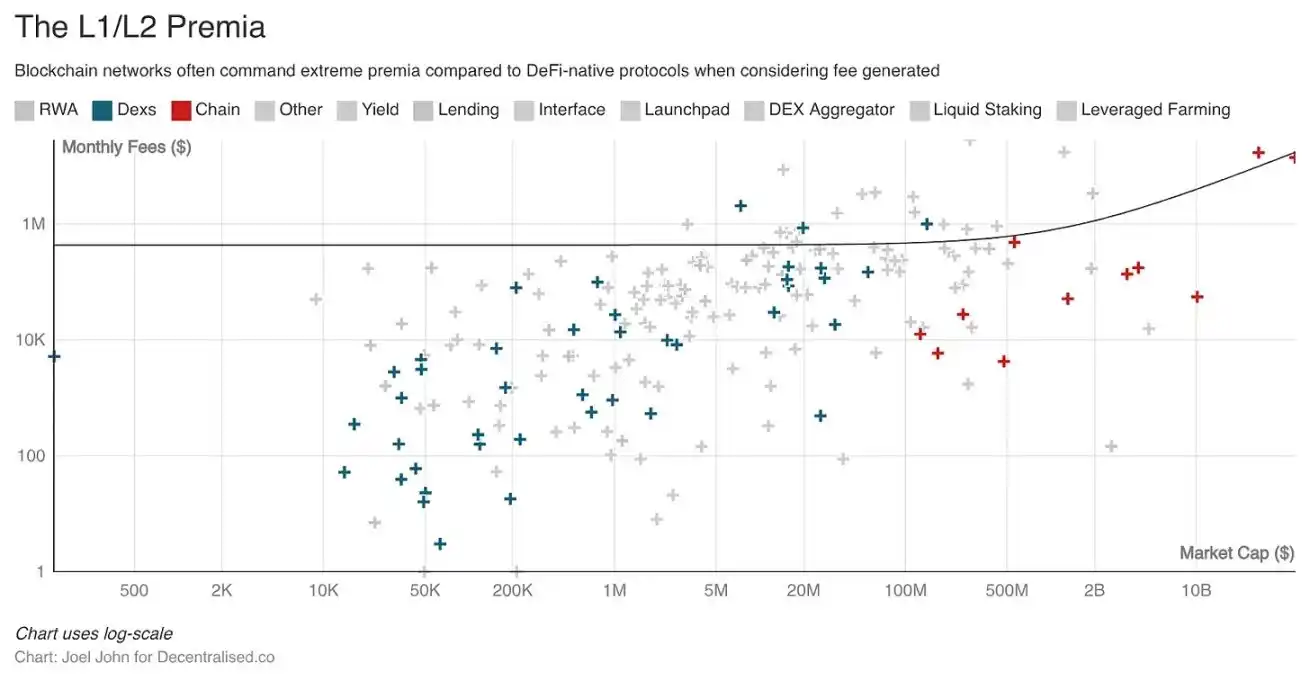

Historically, Layer1s and Layer2s had extremely high valuation premiums compared to standalone infrastructure. This premium, if used well, could have created new economies and funded developers to build truly useful applications. But open source + tokenization made it too easy, leading to fifty homogenized projects on thirty public chains, with poor interoperability.

The fate of DeFi foundational components is even worse.

Investors have too many choices, novelty has faded, and even as economic activity increases, valuations are halved.

Kamino, Euler, Fluid, Meteora, PumpSwap have entered the scene, all with Price-to-Fees ratios far lower than 2022. Some DEXs have even seen their P/F ratios drop to 1x.

That is, the market values them at less than the fees they are expected to generate in the next year.

A strange paradox emerges: underlying protocols (DeFi components, public chains) see falling valuations, but applications built on top of them are making more money in less time.

- 英伟达:人均 520 万美元

- 苹果:240 万美元

- 谷歌:200 万美元

Tether 的效率,可能是企业史上最高。尽管整体 170 倍 P/S 看起来疯狂,但市场对真正赚钱的协议并不非理性 ——定价等于甚至低于传统金融基础设施。

这就引出下一个问题:代币到底有什么用?

在很多品类里,代币是协调资本走向共同愿景的强大工具。加密现在进入双寡头固化的阶段。

传统上,创始人必须借债或股权融资,才能为金融产品注入资金。Hyperliquid、Uniswap、Jupiter、Blur 证明:有代币激励,个人就愿意为新产品提供资本。

如果代币附带治理权,这些人还能深度参与治理。

对比:

- Nvidia: $5.2 million per capita

- Apple: $2.4 million

- Google: $2.0 million

Tether's efficiency is perhaps the highest in corporate history. Even though the overall 170x P/S seems insane, the market is not irrational towards protocols that actually make money—pricing them at or below traditional financial infrastructure.

对比:

对比:

- Nvidia: $5.2 million per capita

- Apple: $2.4 million

- Google: $2.0 million

Tether's efficiency is perhaps the highest in corporate history. Even though the overall 170x P/S seems insane, the market is not irrational towards protocols that actually make money—pricing them at or below traditional financial infrastructure.

This leads to the next question: What is the token actually for?

In many categories, tokens are powerful tools for coordinating capital towards a common vision. Crypto is now in a stage of duopoly solidification.

Traditionally, founders had to raise debt or equity to inject capital into financial products. Hyperliquid, Uniswap, Jupiter, Blur have proven: with token incentives, individuals are willing to provide capital for new products.

If the token comes with governance rights, these individuals can also deeply participate in governance.

Tokens may evolve two main functions in the future:

- Coordinate capital and resources from the right people

- Grant them the power to govern the protocol

Tokens alone are no longer valuable. Even stocks can be tokenized. These tools must possess economic activity收益权 + governance steering power. Many Layer1 and Layer2 tokens fail at both.

Teams and VCs hold most of the tokens, ordinary holders are fragmented. Ordinary person has no reason to care about newly listed assets. The industry is now分裂. MetaDAO allows investors to get a full refund if the team makes false statements. No large protocol has adopted this yet.

The core reflection in crypto is: traditionally, tokens gave holders too few rights. Now protocols are answering an ancient question: Why should people hold these things?

Crossroads: Crypto's Next Era

Over the past two decades, capital markets have become increasingly intertwined, largely thanks to technological advancement.

We can trade commodities, foreign indices, digital assets, and in the future, even compute power (GPU). Blockchain allows these markets to trade globally, 24/7. The move by Nasdaq and NYSE towards 24/7 trading is an example of technology changing the zeitgeist.

We live in a highly financialized world.

For founders, this means rethinking: what to build and how to build it. The data is clear: all blockchain products ultimately make money through only two models:

- Taking small fees from high-frequency trading

- Taking large fees from transactions requiring verifiability and trust

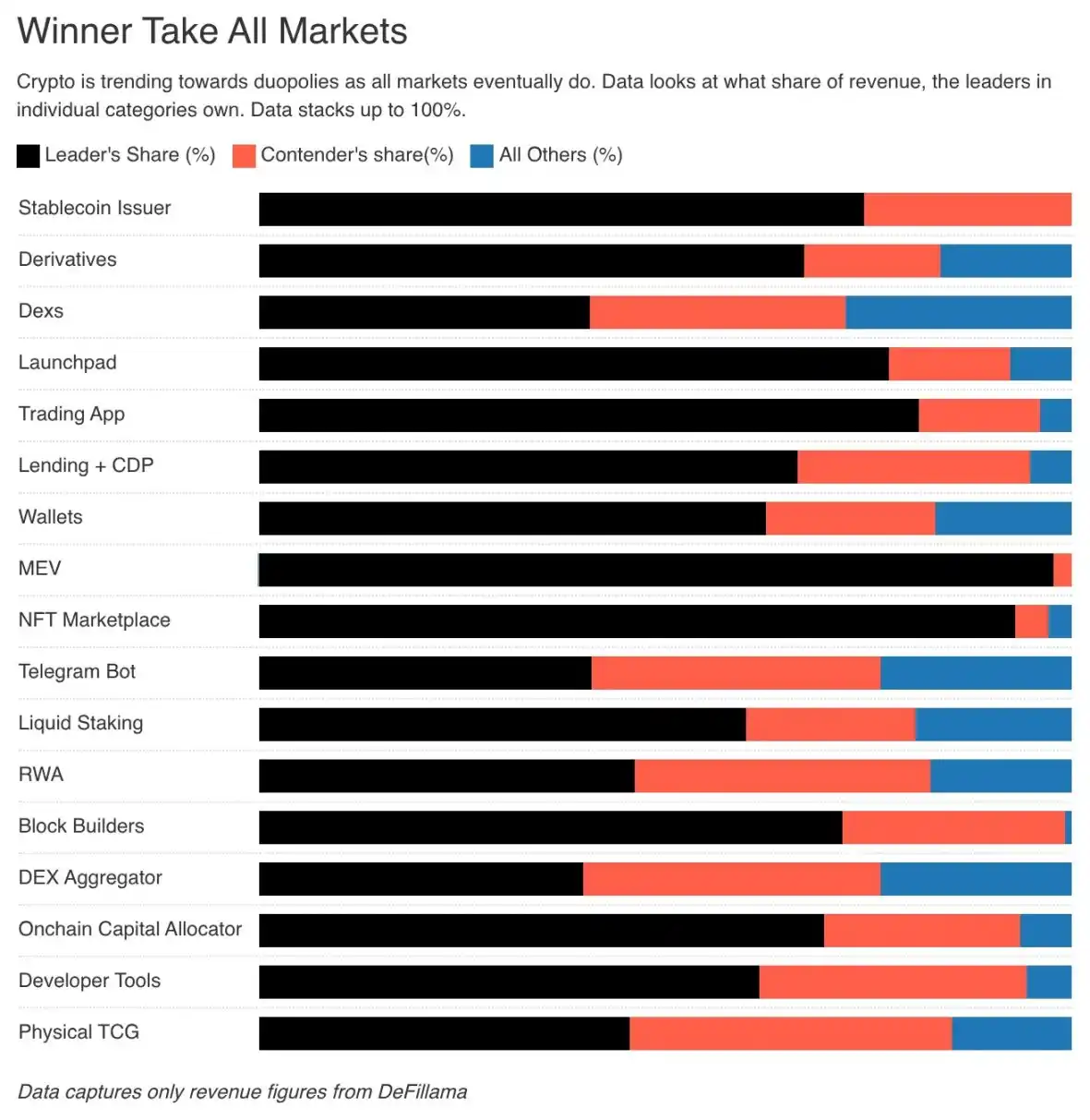

The core competency is either transaction speed or verifiable transparency. Profit-seeking is the purest motive for capital market participants. Markets eventually move towards extreme efficiency. We see 70% of份额被两家头部拿走 in multiple sectors, proof of this.

For founders: the capital that once flowed into your tokens will now转向 volatility更高、资本回报率更高的资产. Long-term capital still exists, even willing to pay a premium, but only for real business value.

Investors in Google and Amazon don't need to panic and flee because the business itself is valuable. In an era where the value of software itself is questioned, blockchain-native applications must find new ways to create value.

We can重构代币, even have startup equity circulate on-chain. But this is not just a token problem, it's a business model problem.

The vast majority of long-tail blockchain applications, like Web3 social, identity, games, have failed to achieve scale or effective differentiation from traditional products. It's not that these experiments lack value, but that we failed to commercialize them effectively.

The infrastructure era of crypto is over. In the future, it will be deeply integrated with the internet.

No one talks about "online business" anymore, you just exist on the internet. No one is called a "mobile app developer" anymore, you are just a developer.

The era of blockchain enthusiasts has ended. We are just ledger maximalists, thinking about the best uses of these ledgers.

Criptomoedas em alta

Perguntas relacionadas

QAccording to the article, what is the main contradiction in the current state of the crypto industry?![]()

AThe main contradiction is that the crypto industry's profitability has reached unprecedented heights, with nearly half of all cumulative fees generated in the last 18 months, yet the market's fear and Greed Index has hit a historical low, and there is widespread pessimism and fear among participants.

QWhat are the primary drivers behind the massive revenue growth of stablecoin issuers like Tether and Circle?![]()

AThe massive revenue growth of stablecoin issuers is driven by two primary forces: 1) Strong demand from the Global South for tools to hedge against local inflation and transfer capital freely, and 2) An extremely efficient cost structure where the marginal cost of issuing more stablecoins or facilitating transfers on the blockchain is nearly zero, making it one of the most capital-efficient businesses in financial history.

QHow has the valuation of Layer 1 and Layer 2 blockchains changed, and what does this signify?![]()

AThe valuation of Layer 1 and Layer 2 blockchains, as measured by the fee-to-price ratio, has dramatically decreased. For example, Solana's ratio fell from 706x to 138x, and Arbitrum's from ~206x to 62x. This signifies a market shift where these foundational protocols are moving from a high 'novelty premium' to a discount, reflecting a more realistic assessment of their value as the technology matures and novelty wears off.

QWhat are the three main types of moats for blockchain-native businesses identified in the article?![]()

AThe three main types of moats are: 1) First-mover Advantage (e.g., the network effects of Tether and Circle), 2) Liquidity Moat (e.g., deep, cross-cycle liquidity like Aave's), and 3) Distribution Moat (e.g., the ability to acquire and retain users during hype cycles, as seen with meme coin trading platforms).

QWhat core issue does the article raise regarding the value proposition of tokens for their holders?![]()

AThe article raises the issue that tokens often provide holders with too few rights, primarily just governance, without direct economic rights to the protocol's profits (like dividends or buybacks) that are standard for traditional equity holders. This makes their valuation appear cheap but is justified by the unprecedented scale and efficiency of the revenue these small teams generate, leading to a re-evaluation of what utility tokens should provide.

Leituras Relacionadas

Trading

Artigos em Destaque

Como comprar ROCK

Bem-vindo à HTX.com!Tornámos a compra de Rock Dao (ROCK) simples e conveniente.Segue o nosso guia passo a passo para iniciar a tua jornada no mundo das criptos.Passo 1: cria a tua conta HTXUtiliza o teu e-mail ou número de telefone para te inscreveres numa conta gratuita na HTX.Desfruta de um processo de inscrição sem complicações e desbloqueia todas as funcionalidades.Obter a minha contaPasso 2: vai para Comprar Cripto e escolhe o teu método de pagamentoCartão de crédito/débito: usa o teu visa ou mastercard para comprar Rock Dao (ROCK) instantaneamente.Saldo: usa os fundos da tua conta HTX para transacionar sem problemas.Terceiros: adicionamos métodos de pagamento populares, como Google Pay e Apple Pay, para aumentar a conveniência.P2P: transaciona diretamente com outros utilizadores na HTX.Mercado de balcão (OTC): oferecemos serviços personalizados e taxas de câmbio competitivas para os traders.Passo 3: armazena teu Rock Dao (ROCK)Depois de comprar o teu Rock Dao (ROCK), armazena-o na tua conta HTX.Alternativamente, podes enviá-lo para outro lugar através de transferência blockchain ou usá-lo para transacionar outras criptomoedas.Passo 4: transaciona Rock Dao (ROCK)Transaciona facilmente Rock Dao (ROCK) no mercado à vista da HTX.Acede simplesmente à tua conta, seleciona o teu par de trading, executa as tuas transações e monitoriza em tempo real.Oferecemos uma experiência de fácil utilização tanto para principiantes como para traders experientes.

159 Visualizações TotaisPublicado em {updateTime}Atualizado em 2026.06.02

Discussões