TL;DR

Since June, South Korea's KOSPI index, dragged down by heavyweight semiconductor stocks, has fallen over 8% at one point, triggering a circuit breaker. Gold and silver also declined during the same time window.

The anomaly is that if it were merely a traditional decline in risk appetite, investors would typically sell stocks and buy gold. But this time, both risk assets and precious metals are being sold. The Korean market provides an extreme case: stocks like Samsung Electronics and SK Hynix, core players in the AI supply chain, fell, while gold and silver also faced simultaneous pressure. The market is not currently trading "where is the safest," but rather "the cost of holding uncertain assets has increased."

This cost is the real interest rate. Simply put, the real interest rate is the true price of money after deducting inflation expectations. When it rises, bonds and cash become more attractive, while assets like gold and silver that do not generate interest become less worthwhile; high-valuation tech stocks also see their valuations compressed because a higher discount rate makes future profits less valuable.

Therefore, the Korean circuit breaker is the surface-level shock, while gold's decline alongside is the more crucial signal. The narrative that supported the simultaneous rise of AI semiconductors and precious metals in 2025 is now being tested by the same macro variable. It does not necessarily mean the end of the AI bull market, nor does it prove that gold's safe-haven attribute has failed. However, it at least indicates that, following the hardening tone from the Federal Reserve under Kevin Warsh's leadership, interest rates and the dollar have regained short-term pricing power.

Gold Under Pressure: Opportunity Cost Trumps Safe-Haven Demand

Gold does not always rise during panic. Its greatest fear is not simply a stock market decline, but a strengthening dollar and rising real interest rates.

Following Kevin Warsh's swearing-in as Fed Chairman on May 22, the June 17 FOMC meeting kept the target range for the federal funds rate unchanged at 3.50%-3.75%. On the surface, this was a hold; but the statement continued to emphasize that inflation remains above the 2% target and mentioned that supply shocks, including energy, are pushing up some prices.

For the market, this is more important than an immediate rate hike. Previously, investors were betting on a dovish pivot; now they are once again facing the prospect of high rates persisting longer, with the risk of rate hikes even re-entering the pricing.

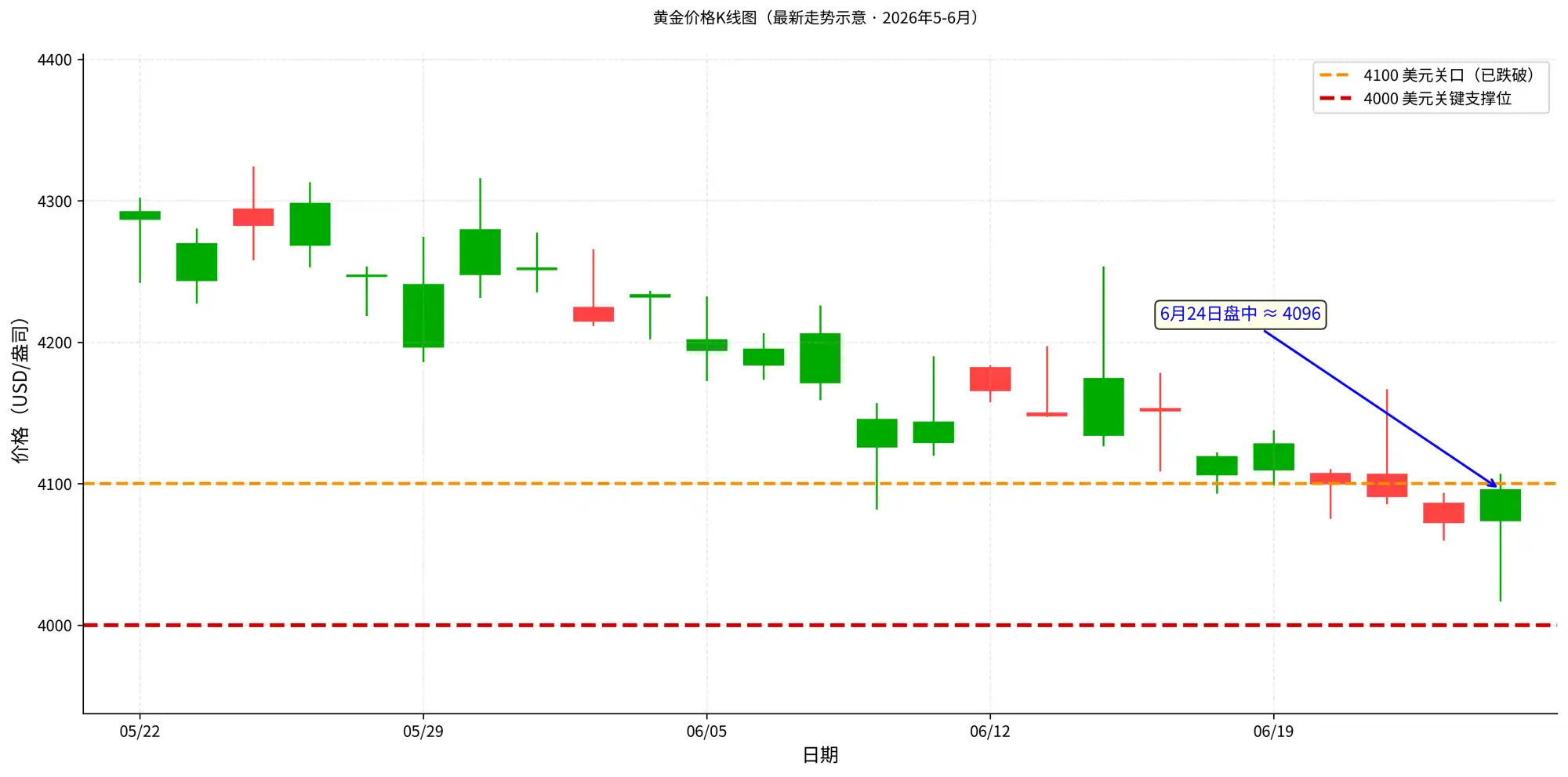

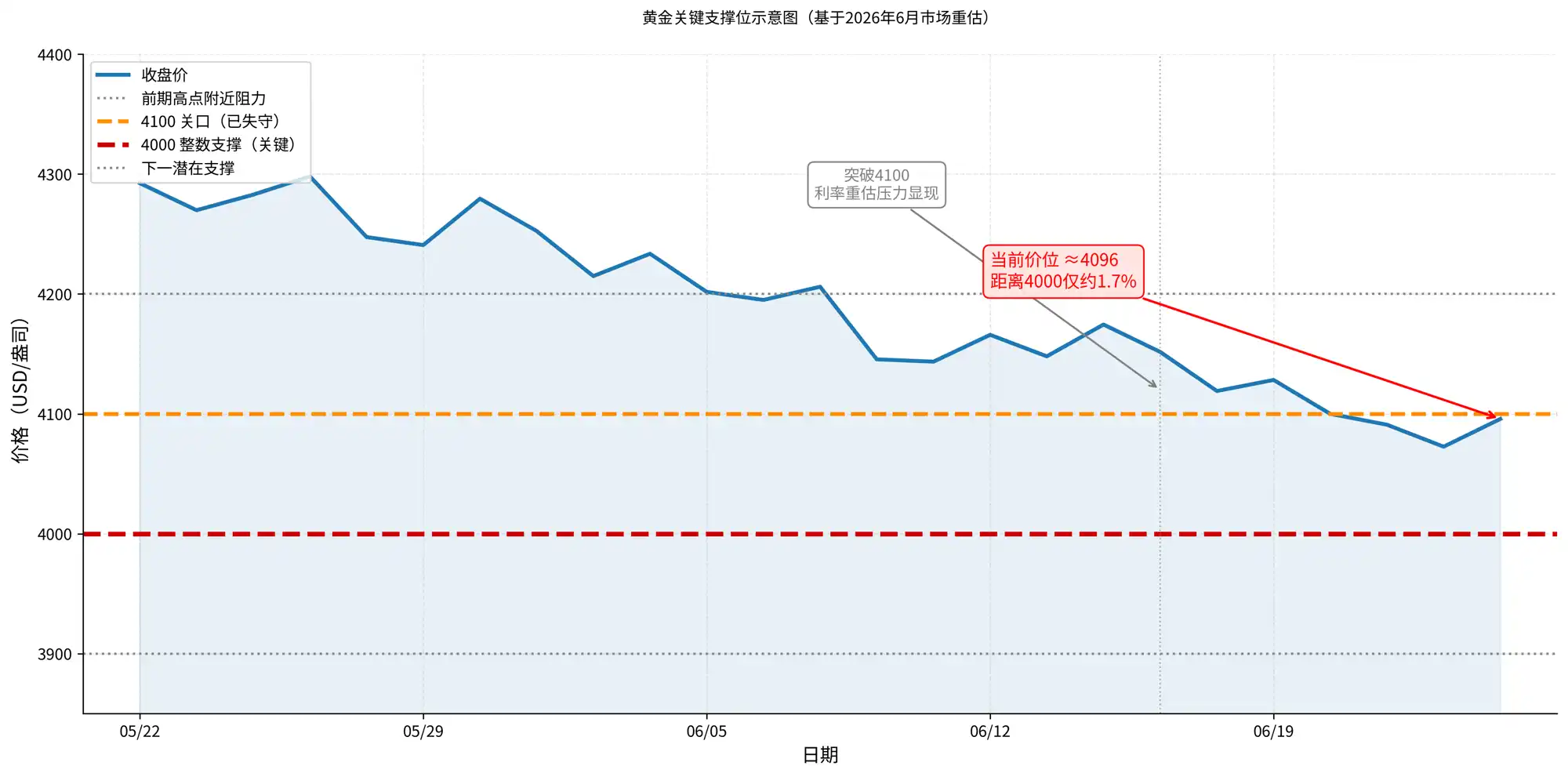

The decline in gold and silver occurred after this shift in the macro anchor. By June 24, major data sources showed gold had fallen below $4,100 per ounce, with Trading Economics' intraday quote around $4,069 at one point, leaving only about 2% to the key psychological $4,000 level. This level is significant not only because it's a round number, but also because several technical analyses identify $4,000 as a key support zone for this pullback. After losing $4,100, the market is no longer just trading an ordinary retracement, but whether gold is formally testing the $4,000 support.

If $4,000 is decisively broken, the issue is not simply how much lower the price might go, but assessing whether the correction could amplify into a sharp sell-off. Gold has seen significant gains and holds substantial profit positions. Once a key integer level is breached, simultaneous selling pressure from short-term stop-losses, trend fund de-risking, ETF outflows, and margin calls could emerge. In such a scenario, gold would still have long-term supports like central bank purchases and safe-haven demand, but the short-term price would first obey liquidity and risk controls. Market confidence in "gold's defensive capability" might be tested anew.

This is not to say that geopolitical risks, central bank buying, or industrial demand are unimportant. Gold's strong rally in 2025 was indeed supported by multiple factors including central bank purchases, a weaker dollar, and safe-haven demand. Silver's even larger gains were also related to its industrial attributes and supply-demand expectations. But when interest rate expectations are suddenly revised upward, precious metals are first revalued as non-yielding assets.

The reasons for holding gold haven't disappeared for investors; they are just being temporarily suppressed in the short term by higher opportunity costs for capital. Risk events will stimulate safe-haven buying, while high interest rates increase the cost of holding gold. When the latter dominates, gold can fall alongside stocks.

Gold and Silver Falling Together Indicate the Market is Selling Liquidity

The simultaneous decline of gold and silver cannot be simplistically interpreted as "safe-haven assets failing." More accurately, the market is repricing liquidity.

When dovish expectations are strong, gold can benefit simultaneously from a weaker dollar, falling real rates, and safe-haven demand. Silver adds industrial attributes and supply-demand expectations on top, giving it greater elasticity. But when the Fed signals a renewed hawkish tilt, the pricing logic reverses: a stronger dollar weighs on dollar-denominated gold and silver, rising real rates increase the opportunity cost of non-yielding assets, and the market actively reduces positions in more volatile assets.

This is also why gold and silver fall alongside stocks. On the surface, they belong to different asset classes, but in short-term trading, they both depend on the same variable: the price of money. If money becomes more expensive, the market will first sell the most crowded, most profitable, and most liquid positions, rather than first distinguishing whether these assets' long-term narratives still hold. Silver is more sensitive because it also carries industrial attributes; once risk assets correct in unison, industrial demand expectations are also discounted.

Therefore, the core of this decline is not "why isn't gold acting as a safe haven," but rather that the direction of market safe-haven flows has changed. In an environment of higher interest rate expectations, the short-term safe-haven assets chosen by capital may be the US dollar, cash, and short-term bonds. Gold remains a long-term safe-haven tool, but during a phase of rapid interest rate repricing, it will first face the impact of opportunity cost.

Korea is a Magnifying Glass, Not the Cause of Precious Metals' Decline

The reason the Korean market's sharp drop is observed alongside gold is not because Korean semiconductors directly determine gold prices, but because it amplifies the pressure from the same macro trade.

The Korean stock market benefited from AI memory demand in 2025, with semiconductor heavyweights like Samsung Electronics and SK Hynix driving a significant index rally. By 2026, the question became: if too much capital is crowded into the same trade, once macro rates rise, who sells first and how much they sell may impact prices more than short-term changes in company fundamentals. The KOSPI falling over 8% and triggering a circuit breaker in June is the result of such a crowded trade being re-examined.

However, the causality needs clarification. Current public evidence does not prove that "Korean deleveraging directly spilled over to global precious metals positions." A more prudent judgment is that Korean semiconductors and precious metals are simultaneously bearing the same macro pressure: rising interest rates, a strengthening dollar, and more expensive liquidity. The Korean market shows a more violent price reaction due to index concentration and crowded AI positioning; gold and silver are directly exposed to interest rate repricing due to their non-yielding and dollar-denominated nature.

In other words, Korea is not the cause of gold's decline, but rather a display screen for market risk appetite and leverage levels. It tells investors: when expectations for higher rates resurface, assets that have seen significant gains and heavy positioning over the past year will be inspected first. Precious metals, while not tech stocks, also face repricing when the cost of capital rises.

AI Volatility Affects Sentiment, But Gold and Silver Still Look to Interest Rates

AI semiconductor volatility affects market sentiment and assets like silver that possess industrial attributes, but it is not the main driver explaining gold and silver price movements.

If the key variable for gold and silver is the real interest rate, then the key variable for AI semiconductors is order fulfillment. Micron's earnings can serve as a window into risk appetite because they influence the market's judgment on "whether high-valuation assets can still withstand high rates." If AI chain earnings remain strong, risk appetite may find support, and silver's industrial attributes could be more easily re-priced. If guidance falls short, the market may further reduce growth asset positions, and contracting risk appetite will continue to pressure high-beta assets.

But the core pricing factor for gold must still return to the Fed, the dollar, and real interest rates. No matter how strong AI earnings are, they can hardly directly offset the pressure from rising real rates on gold. Similarly, weaker AI earnings do not necessarily drive gold higher unless they simultaneously trigger expectations for rate cuts, a weaker dollar, or stronger safe-haven demand.

This is the difference between market repricing and fundamental disproval. Repricing means the discount rate has changed, and investors are willing to assign a lower valuation to the same profits. Disproval means demand itself has a problem, and future profits must also be revised downward. For precious metals, the former is more important now: the market is first revaluing gold and silver based on higher capital costs, not changing the long-term safe-haven logic due to isolated changes in a specific industry chain.

Interest Rates and the Dollar Are Validating This Decline

The easiest overstatement to make now is to equate the synchronous decline directly with the end of a trend. Gold falling does not mean the end of the gold bull market; a Korean circuit breaker does not mean AI demand has already collapsed. A more reasonable assessment is that the market has entered a validation window: interest rate pressure first compresses valuations and non-yielding asset prices, followed by waiting for data to confirm whether this is a correction or a reversal.

The Fed under Warsh's leadership is the first validation line. If subsequent inflation and employment data continue to show strength, and energy prices maintain their pressure, the FOMC's hawkish tone may further translate into more explicit rate hike expectations. Then, gold and silver would face not just a short-term technical correction, but more sustained real rate pressure.

The dollar is the second validation line. Gold and silver are priced in dollars. A stronger dollar directly increases holding costs for non-US dollar investors and weakens short-term demand for precious metals. If dollar strength coincides with rising real rates, precious metals typically find it harder to reverse the pressure relying solely on a single safe-haven narrative.

Silver has an additional validation line: industrial demand expectations. It is more susceptible to risk asset sentiment than gold and more prone to amplified volatility when growth expectations change. If AI, semiconductors, and other high-beta assets remain under pressure, silver may face a double revaluation of both its precious metal and industrial attributes.

The simultaneous decline of gold, silver, and AI stocks sends investors a straightforward reminder: seemingly different assets in a portfolio may be exposed to the same risk from a single macro variable. The winning trades of 2025 will not necessarily lose their fundamentals simultaneously in 2026, but they will simultaneously face more expensive capital costs. The variables that will truly land on precious metals prices going forward are how long the pressure from interest rates and the dollar can persist, and whether safe-haven demand, central bank purchases, and industrial demand can arrive quickly enough to offset this pressure.