Author: Bu Shuqing

Source: Wall Street Insights

The U.S. bond market is facing potential selling pressure from overseas official investors, a development that has raised high alert in the market.

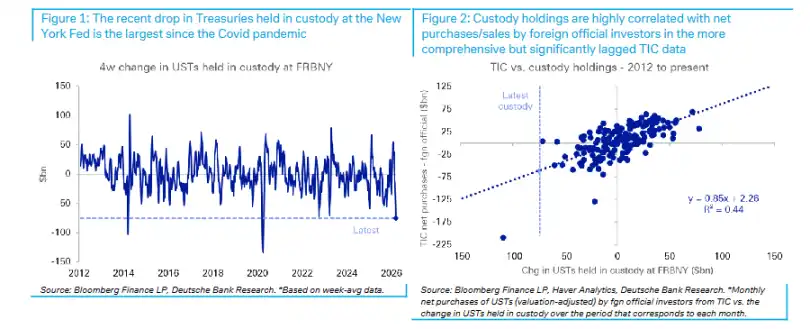

According to the Trading Desk, a research report released by Deutsche Bank on March 23 shows that the U.S. bond holdings of foreign official accounts custodied at the New York Fed plummeted by $75 billion over the past four weeks, marking the largest monthly decline since the impact of the COVID-19 pandemic in 2020. Based on historical data models, this change implies that foreign official investors actually net sold approximately $60 billion in U.S. bonds, also the largest since the pandemic.

This data aligns with the recent sharp rise in U.S. bond yields, particularly the abnormal upward movement in mid-term (belly) yields—a segment where foreign official investors' holdings are concentrated. Deutsche Bank warns that if overseas demand continues to shrink, the "convenience yield" advantage of U.S. bonds will be eroded, posing a substantive upside risk to long-term yields.

Custody Data Reveals Selling Signals

The most authoritative data source for tracking the movements of foreign official investors in U.S. bonds is the U.S. Treasury's TIC (International Capital Flows) report, but this data has significant lag—the March data will not be available until mid-May at the earliest.

As an alternative indicator, the New York Fed's weekly H.4.1 report includes a memorandum entry recording the face value of securities custodied for foreign official and international accounts, with a lag of only one day. Deutsche Bank strategists Matthew Raskin, Steven Zeng, and Andrew Fu noted in the report that the latest H.4.1 data shows, based on weekly averages, that the U.S. bond holdings of foreign official custodied accounts fell by $75 billion over the past four weeks, not only the largest decline since March 2020 but also the second-largest single-week drop in the past decade.

Notably, unlike a similar situation in March 2023, the scale of FIMA repo operations did not rise simultaneously this time, indicating that this round of reduction was due to direct sales or non-renewal at maturity, rather than liquidity financing through repo operations with the Fed. Foreign reverse repos, foreign official deposits, and FIMA securities lending also showed little change over the past month.

High Correlation Between Custody Data and TIC Data

To what extent can custody holding data represent the overall changes in U.S. bond holdings by foreign official investors? Deutsche Bank conducted a systematic verification.

The report shows that over the past 15 years, the correlation between changes in custody holdings and the net purchases by foreign officials in TIC data has been significant, with the former explaining about 50% of the latter's changes. Even when shortening the sample to post-2019 to eliminate potential interference from changes in reserve management models, this relationship remains robust.

Based on this historical relationship, a $75 billion decline in custody holdings corresponds to a net sale of approximately $60 billion by foreign official investors. Deutsche Bank pointed out that this would be the largest net sale by foreign official accounts since the COVID-19 pandemic; to find a comparable case, one would need to go back to December 2018.

Shift in Capital Flows Amid Foreign Exchange Intervention

The decline in U.S. bond custody holdings is highly consistent with recent market dynamics observed by Deutsche Bank's foreign exchange strategy team.

According to a previous report by Deutsche Bank's foreign exchange strategy team, despite the outbreak of the Iran war and soaring oil prices, the U.S. dollar failed to strengthen as expected, partly due to large-scale foreign exchange interventions by several Asian central banks. Meanwhile, the team's high-frequency ETF monitoring data also showed a significant slowdown in foreign investors' purchases of U.S. dollar assets.

The combination of these two clues leads to a conclusion: foreign official investors are reducing their allocation to U.S. dollar assets, and the sale of U.S. bonds is a direct manifestation of this trend.

Sustained Selling Could Push Long-Term Yields Up by Over 100 Basis Points

Deutsche Bank's analysis reveals a structural concern: U.S. bond yields have long benefited from the "convenience yield" brought by the U.S. dollar's reserve currency status, and this advantage is now being tested.

The report cites previous Deutsche Bank research, indicating that the current 10-year U.S. bond yield is more than 100 basis points lower than the reasonable level implied by the U.S. net international investment position (NIIP). Another recent academic working paper estimated that the U.S. dollar's reserve currency status keeps long-term U.S. interest rates about 90 basis points lower than "normal levels."

Deutsche Bank warns that if foreign demand continues to decline, this convenience yield will face regression pressure, and the term premium and overall yield of U.S. bonds will have substantive upside space, posing a direct impact on investors holding U.S. bonds.