Original Author: Castle Labs

Original Compilation: AididiaoJP, Foresight News

69 trillion U.S. dollars—this is the estimated market capitalization of the U.S. stock market, which drives the total global stock market capitalization to 130 trillion U.S. dollars.

Opportunities to participate in the stock market are increasingly coming into the view of on-chain native participants, although they were initially not interested. The reasons are varied, but the general consensus is that cryptocurrency was once thought to offer faster returns. However, more and more investors are opting for diversification. The Wall Street Journal highlighted this trend, noting that funds are shifting from Bitcoin to gold or the "Magnificent Seven" (MAG7) tech stocks.

Until recently, the proposition in the cryptocurrency space was characterized by exclusive loyalty to digital assets and acceptance of the cyclical pattern where everything mysteriously crashes every four years—almost astrological in nature. Most crypto assets reached their all-time highs in the second quarter of 2025 and have not recovered since. Meanwhile, the stock market has repeatedly hit new highs, prompting investors to question: is loyalty to the blockchain merely an obsession disguised as conviction?

The true utility of tokenization is not "financial inclusion" or "democratization of access," but rather providing traders with a tool that enables them to short Tesla (TSLA) to the bottom, borrow Nvidia (NVDA) stock as collateral without KYC, trade pre-IPO stocks, or earn yield in Kamino vaults.

This article analyzes three different paths to on-chain tokenization:

- OndoFinance launched Global Markets in September, elevating tokenization on the Ethereum network to institutional-grade standards.

- xStocksFi (now owned by Kraken), under Backed Finance, emerged in June, targeting the retail market with multi-chain composability.

- HyperliquidX activated HIP-3 in October, enabling permissionless perpetual contract trading for any asset, including commodities and stocks.

This article will delve into the inner workings of each protocol, focusing on how they achieve asset "tokenization" on-chain.

We will provide a general analysis of the legal framework behind each protocol and its impact on investors.

Finally, we will explore where the broader tokenization trend is headed and what it means for the cryptocurrency ecosystem as we know it.

Ondo: The On-Chain BlackRock

Ondo was founded in 2021 by Nathan Allman and Justin Schmidt, both with Goldman Sachs backgrounds. For years, it focused on building tokenized treasury products (USDY for retail and OUSG for institutions). Before launching Global Markets in September 2025, its assets under management had already exceeded $2 billion. Currently, the Total Value Locked (TVL) across all Ondo products (including treasury bills) is $2.47 billion.

Ondo's tokenization model falls under what the industry calls indirect tokenization. It works as follows: an offshore Special Purpose Vehicle (SPV) purchases and holds the underlying stocks on behalf of the token holders, then issues on-chain structured notes. These notes pass through the economic risk but do not grant legal ownership. Token holders have a claim against the Ondo issuing entity, which is collateralized by the underlying stocks held in segregated accounts at U.S.-registered broker-dealers.

Ondo tokens are essentially debt instruments collateralized by stocks, not the stocks themselves. For example, token holders do not have the voting rights that holders of the underlying stock possess.

Its main features are:

- Uses institutional-grade tokenization standards, featuring bankruptcy-remote SPVs, daily Proof of Reserves, U.S.-registered custodians, and support for instant minting during market trading hours.

- If Apple Inc. (AAPL) stock is trading at $180 on NASDAQ, a user can instantly mint AAPLon with $180 worth of stablecoins and redeem it at any time. Arbitrageurs maintain a tight peg for the tokenized stock price by balancing between decentralized exchanges (DEXs) and Global Markets. The arbitrage loop is key to maintaining price stability. Ondo achieves atomic settlement: stablecoins go in, tokens are generated, all in one step. If AAPLon trades above $180 on a DEX, market makers mint new tokens on Global Markets and sell them on the market to suppress the premium; conversely, if the price is below $180, they buy the tokens on-chain and redeem them at face value, profiting from the difference.

Ondo tokens are fully collateralized by U.S. stocks and ETFs held at one or more U.S.-registered broker-dealers. Holders do not directly hold the stocks but gain economic exposure through the tokens; dividends are automatically distributed.

No fees are charged for minting and redeeming; Ondo profits from the spread.

The platform initially launched with over 100 assets on Ethereum, later expanded to BNB Chain and Solana, and recently announced the Ondo Chain. The Ondo Chain introduces a specific Proof-of-Stake (PoS) mechanism for staking Real World Assets (RWA).

The current product catalog is extensive:它包括 large-cap stocks (Apple AAPL, Tesla TSLA, Nvidia NVDA, Google GOOGL), exchange-traded funds (ETFs, like SPY, QQQ), and commodities.

However, its geographical restrictions are extremely strict: U.S. citizens or residents are not allowed to participate. Ondo tokenized stocks are only for accredited investors and require mandatory KYC.

The tokenization process of each protocol has its own characteristics worth noting.

U.S.-based self-clearing broker-dealer Alpaca currently custodies over 94% (by value) of tokenized U.S. stocks and ETFs, including Ondo's products. Alpaca's instant tokenization network provides physical minting and redemption channels. This means the underlying stocks are transferred via book entry between brokerage accounts, rather than being liquidated and repurchased, eliminating slippage and maintaining token price stability. Ondo recently also filed a registration statement with the U.S. Securities and Exchange Commission (SEC); once effective, Global Markets will become the first transferable tokenized stock issuer subject to SEC reporting requirements. The SEC concluded a two-year investigation in November 2025 without recommending charges against Ondo. Subsequently, Ondo acquired the SEC-registered broker-dealer Oasis Pro Markets to accelerate its development in the U.S.

Ondo believes that institutions value regulatory clarity and operational efficiency more than ideological purity.

xStocks: A Handy Tool for Retail Users

xStocks finds an ideal balance between cryptocurrency and traditional finance: it is more accessible than Ondo, more compliant than HIP-3, and open to all users.

xStocks launched in June 2025, offering over 60 tokenized stocks and ETFs. Each is backed 1:1 by securities held under the supervision of Swiss regulators by Swiss or U.S. custodians. Its tokens follow the SPL or ERC-20 standard and can be freely transferred across different blockchains.

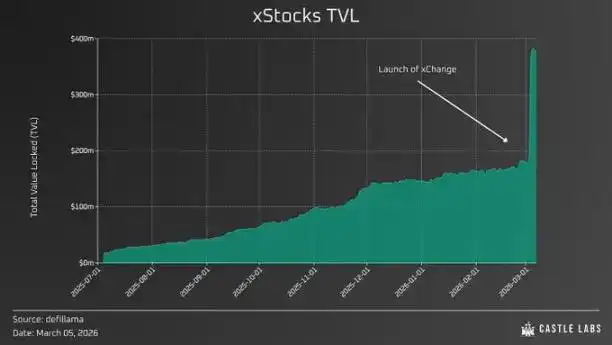

Its timely success prompted Kraken to acquire Backed in 2025. Currently, xStocks holds publicly listed stocks worth $250 million, with Tesla stock accounting for over a quarter.

In this model, token holders do not own the stock itself but have a claim against the issuer. Each xStock is backed 1:1 by the underlying stock. Dividends are automatically reinvested, similar to Ondo's model: when the underlying stock pays a dividend, the holder's wallet receives an airdrop of additional xStock tokens equivalent to the dividend amount.

Its tokenization mechanism compresses the traditional structured finance model onto the blockchain. Legally, each xStock is a tracking certificate, classified as a bearer debt instrument. It is issued by the Jersey-registered SPV—Backed Assets Limited, a wholly-owned subsidiary of Swiss Backed Finance AG. The token's financial value tracks a specific underlying stock or ETF but does not grant ownership or voting rights. Token holders are creditors of the issuer, not shareholders of the underlying company. This is the same indirect tokenization model used by Ondo, but the specific legal structure and post-issuance mechanics differ.

The issuance process is as follows:

- An Authorized Participant (AP) submits a minting request via Alpaca's API, specifying the stock ticker, quantity, target blockchain, and receiving wallet address.

- Alpaca, as a U.S.-based self-clearing broker-dealer, verifies the request and transfers the corresponding stocks from the AP's brokerage account to the issuer's account.

- After Backed confirms receipt of the underlying securities, it mints an equivalent amount of xStock tokens on-chain and sends them to the AP's wallet.

The redemption process is the reverse: the AP burns the tokens, Alpaca confirms the burn, and the corresponding stocks are transferred back to the AP's brokerage account. This physical transfer mechanism keeps the token price tightly linked to the underlying stock.

On March 5th, xStocks launched xChange—a swap engine designed to directly pull capital market liquidity into DeFi during trading hours, while retaining on-chain liquidity pools on weekends for price discovery.

The system consists of three parts:

- On-chain liquidity, supporting price discovery during non-trading hours.

- xChange itself, responsible for connecting DeFi and traditional finance during trading hours.

- xPort, used to bring assets on-chain.

xChange is powered by Chainlink oracles, is already live on Solana's aggregator, and will soon launch on CoW Swap and 1inch on Ethereum. Integrations with PancakeSwap, LiFi, DFlow, and Kamino Swap are also underway.

Vertically, off-exchange liquidity is pulled into the blockchain through arbitrage, tightening spreads in on-chain trading pools; horizontally, it opens access to xStocks' vast product range without the need to pre-seed liquidity for each stock ticker.

Its regulatory framework spans three jurisdictions:

- The issuing entity is in Jersey, regulated by the Jersey Financial Services Commission under the Borrowing Control Order.

- The prospectus has been approved by the Liechtenstein Financial Market Authority (FMA), allowing the tokens to circulate freely in EU countries.

- Tokenization operations are performed by Backed Finance AG in Switzerland.

The underlying collateral is held in segregated accounts at regulated custodian banks in Switzerland and the U.S. (including InCore Bank and Maerki Baumann), subject to tri-party account control agreements. If token holders' rights are impaired, the security agent has the right to seize these collateral accounts.

Distribution channels are wide, with stocks available on centralized exchanges like Kraken, Bybit, and Gate. Kraken offers instant settlement, fractional share investing (minimum $1), and competitive fees (taker 0.1%, maker rebate -0.02%).

Unlike Ondo, xStocks' philosophy is to serve retail users where they are. There are no specific KYC or whitelist restrictions; anyone can buy stocks and freely transfer them between self-custody wallets.

On February 25th, xStocks' trading volume reached $25 billion.

Kraken has designated Alpaca as its preferred 1:1 source and custody partner for underlying stocks. Alpaca's instant tokenization network provides real-time minting and redemption services for institutions. In early February 2026, the 360X platform, owned by Deutsche Börse, began offering xStocks to its clients! This exchange, regulated by Germany's Federal Financial Supervisory Authority (BaFin) and the European Securities and Markets Authority (ESMA), is the gold standard in Europe.

The core idea of xStocks is that retail users value self-custody and multi-chain access more than institutional-grade custody. Naturally, they crave tools on par with institutions. Stock tokenization is the first step in bridging the information asymmetry gap: now, anyone can listen to an earnings call and immediately make buy or sell decisions before the market opens.

Hyperliquid: Everything is Tradable

Hyperliquid promotes a fundamentally different model, simplifying the concept of tokenization to its most basic form: traders gain price exposure by taking long or short positions on derivative contracts, nothing more, involving no economic ownership of any underlying asset.

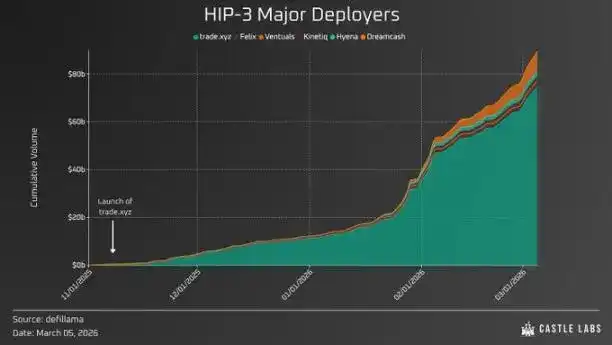

HIP-3, activated in October 2025, allows any user staking 500,000 HYPE to launch their own perpetual contract exchange on HyperCore. Deployers can set their own oracles, define leverage, manage risk, and earn 50% of the trading fees.

The operating mechanism here is fundamentally different from the aforementioned. In the Ondo and xStocks models, real stocks are held in custodial accounts, tokens are structured claims on these stocks, and when holders burn the tokens, the corresponding stocks are sold. The asset custody chain is:

NASDAQ → Broker → Special Purpose Vehicle (SPV) → Blockchain

In Hyperliquid's model, this chain is completely absent. HIP-3 markets are isolated cross-margin markets, not directly listed on Hyperliquid's main interface, but are entirely built and distributed by third-party builders. The oracle is the key variable: each deployer chooses their own price feed source and defines the rules for handling periods when U.S. markets are closed but perpetual contracts still trade 24/7. During market closure, exchanges rely on internally priced Exponential Moving Averages (EMA), protocol-set price limits, and specific trust tiers based on the liquidity depth of the asset.

This is not tokenized stock like Ondo Global Market. There are no stocks, no dividends, no redemption mechanism, and no SPV, only contracts that track prices via oracles and settle in stablecoins or HYPE.

For example, the XYZ100, deployed by trade.xyz, tracks the value of a "market-cap-weighted index of 100 large non-financial companies listed on U.S. exchanges, adjusted." It reached a daily trading volume of $72 million and open interest of $55 million within two weeks, ranking in the top ten on the Hyperliquid platform; its monthly volume is now in the billions of dollars.

Hyperliquid's strength lies in its decentralized market creation mechanism. Any builder meeting the 500,000 HYPE staking requirement can deploy three markets for free; more markets require acquisition through Dutch auctions.

This has spawned an explosion of niche markets:

- trade.xyz (offering XYZ100, NVDA, TSLA, AAPL, GOOGL, etc.)

- Ventuals (offering pre-IPO SpaceX perpetual contracts)

- Felix (collateralized with USDH, 20% lower taker fees)

- Kinetiq, a liquid staking protocol with monthly trading volume exceeding one billion dollars

Through HIP-3, Hyperliquid is becoming the AWS (Amazon Web Services) of perpetual contracts: instead of competing with every niche market, it provides the underlying infrastructure for builders to compete on top of it.

Just as AWS rents computing, storage, and networking resources to users, who can then freely build applications on it, Hyperliquid replicates this model with financial infrastructure:

- HyperCore provides the order book, margin engine, and settlement layer.

- Deployers decide which assets to list, which oracle to use, what leverage to allow, and how to manage risk.

- The protocol itself doesn't care if a market tracks Tesla, pre-IPO SpaceX, gold, or a basket of GPU manufacturers. It collects its 50% fee share regardless. This is fundamentally different from the business models of Ondo or xStocks, which must individually structure, arrange custody for, and build legal frameworks for each tokenized asset. Hyperliquid delegates these functions to the builders, adopting a completely laissez-faire attitude towards tokenization.

The current market environment is extremely favorable for perpetual DEXs, with trading volume in 2026 showing no signs of slowing down. Crypto speculators value leverage and accessibility more than ownership. But as mentioned earlier, this is partly because the culture hasn't shifted yet, and accessibility was very poor until tokenization emerged in recent years.

However, the risks are much higher than with tokenized stocks. During periods of high volatility or market closures, oracle failures, mass liquidations, or market makers withdrawing to avoid losses can lead to complete loss of principal. Unlike tokenized stocks, once a position is liquidated, the funds are gone forever.

Institutional trading desks require auditable counterparties and clear regulatory classifications for derivatives, neither of which HIP-3 provides. For compliance-bound funds, trading stock perpetuals on Hyperliquid would immediately raise red flags with auditors and risk committees, especially regarding ISDA compliance. Hyperliquid's current user base remains predominantly retail, as it is open to the public. However, there are signs this is changing. Ripple has integrated Hyperliquid into its institutional prime brokerage platform, Prime, providing clients with access to perpetuals—another sign of the times. During the weekend of the Iran attack, gold, silver, and oil markets on Hyperliquid remained available, increasingly making it an important reference benchmark for tokenized asset prices during non-trading hours.

Tokenizing Everything

Hyperliquid proves that decentralized protocols can and will compete with traditional exchanges.

Other platforms are following suit. Binance relaunched its tokenized stock business on February 24, 2026, partnering with Ondo to list 10 tokenized U.S. stocks and ETFs on Binance Alpha. This is the first time Binance has offered such services since July 2021, when the UK FCA and Germany's BaFin raised compliance concerns, triggering subsequent events.

The current exclusion of the U.S. market is another point of contention. Once the SEC approves domestic tokenized securities (a near certainty given the momentum after the passage of the GENIUS Act), the on-chain RWA space will experience explosive growth. Regardless of crypto market downturns, the value of stocks (listed or not) generally trends upward.

The real competition is: who will control the infrastructure when the U.S. formally approves.

There is no direct competition between Hyperliquid and xStocks or Ondo, as they serve fundamentally different purposes. Ondo and xStocks provide economic exposure to stocks, their tokens are backed by real stocks, dividends are automatically reinvested, and there is a redemption mechanism pegged to the underlying asset. Their core value is "access": holding, collateralizing for loans, and composably using assets that were previously only tradable on traditional platforms like Schwab or Interactive Brokers. Hyperliquid's HIP-3, on the other hand, offers leverage and speculation tools: it is a synthetic contract tracking a price, with no claim on any underlying asset, no custody chain, and granting no creditor rights. In a sense, this might be the ultimate expression of financial freedom—anyone with a wallet and funds can instantly gain exposure to almost any asset.

For retail users, this is not an either/or choice, as each option leads to different outcomes. A trader might hold xTSLA in a self-custody wallet as a medium-term position, while simultaneously shorting TSLA-USDC on Hyperliquid to hedge against potential bad earnings, much like many traders arbitrage between Polymarket, pre-market markets, OTC points platforms, etc.

One is for long-term portfolio allocation, the other for short-term trading operations. The source of confusion is that both are accessed via crypto wallets, both are denominated in stablecoins, and both are broadly categorized under the concept of "tokenized stocks." But this comparison is flawed: xStocks and Ondo face issuer and custodian risk (the SPV must remain solvent, collateral must remain segregated), while Hyperliquid faces oracle and liquidation risk (price feeds must be accurate, margin must be sufficient, or the position is permanently lost). Therefore, although they fall under a broad category, these protocols are not directly comparable.

Hyperliquid's advantage over the former two is speed and flexibility. The permissionless nature of HIP-3 means the market *is* the product—any asset with an oracle price feed can have a corresponding perpetual market within hours, unlike the months-long legal structuring process required for tokenized stock issuance.

These are three protocols that are almost impossible to compare directly, each focusing on very specific areas and meeting the needs of different users: the competition between them is an illusion.

This ultimately boils down to a discussion about choice, autonomy, and the spirit of innovation.