Author: Top Innovation Block Research Institute

In early March 2026, Scott Kennedy, a senior fellow at the Center for Strategic and International Studies (CSIS), released a heavyweight 147-page report titled "The Power of Innovation: The Strategic Value of China’s High-Tech Drive".

Scott Kennedy, whose official Chinese name is Gan Side, is a renowned American political scientist and top China expert. The Center for Strategic and International Studies (CSIS) where he works is also critically important: among the hundreds of think tanks dotting Washington D.C., CSIS is公认 as being at the very top of the pyramid, often "guiding the US government on how to intervene in the world."

Scott Kennedy's style is pragmatic, rational, and he has an extremely deep understanding of how China operates. Think tank scholars like him often play the role of "unofficial diplomatic envoys" (track two diplomacy).

It is worth mentioning that Scott Kennedy, in September 2022 (a period when China's pandemic controls were still strict), was the first Western think tank scholar since the outbreak of the pandemic to personally travel to mainland China for several weeks of on-the-ground research and face-to-face exchanges with Chinese political and business circles,足以可见 his extensive network and weight in communication on both the Chinese and American sides.

This heavyweight report explores these questions:

How exactly is China's technological innovation being converted into geopolitical power? Why are some industries advancing by leaps and bounds while others struggle? In today's climate where "decoupling theory" is increasingly bankrupt, where is the global tech competition headed?

1. The Underlying Logic of the Great Tech Leap Forward

Over the past decade, China's technology policy has completed a paradigm shift from "trading market for technology" to "introduction, digestion, and absorption," and now to "independent innovation" and "security first." Particularly since the US initiated entity list sanctions against Huawei and other companies in 2019, the dramatic increase in external pressure has instead acted as a catalyst for China's technological self-reliance.

Kennedy lists a set of data in the report:

In 2023, China's R&D expenditure, calculated by purchasing power parity, reached $1 trillion, equivalent to the world's second-largest economy throwing over 2.6% of its GDP into the money-burning machine of R&D. In the most subsidy-crazy years, various industrial funds and policy倾斜加起来 totaled over $250 billion annually—enough money to buy all of General Electric and still have change left.

This "brute force" whole-nation system has brought obvious results:

First, the rise of innovation clusters:

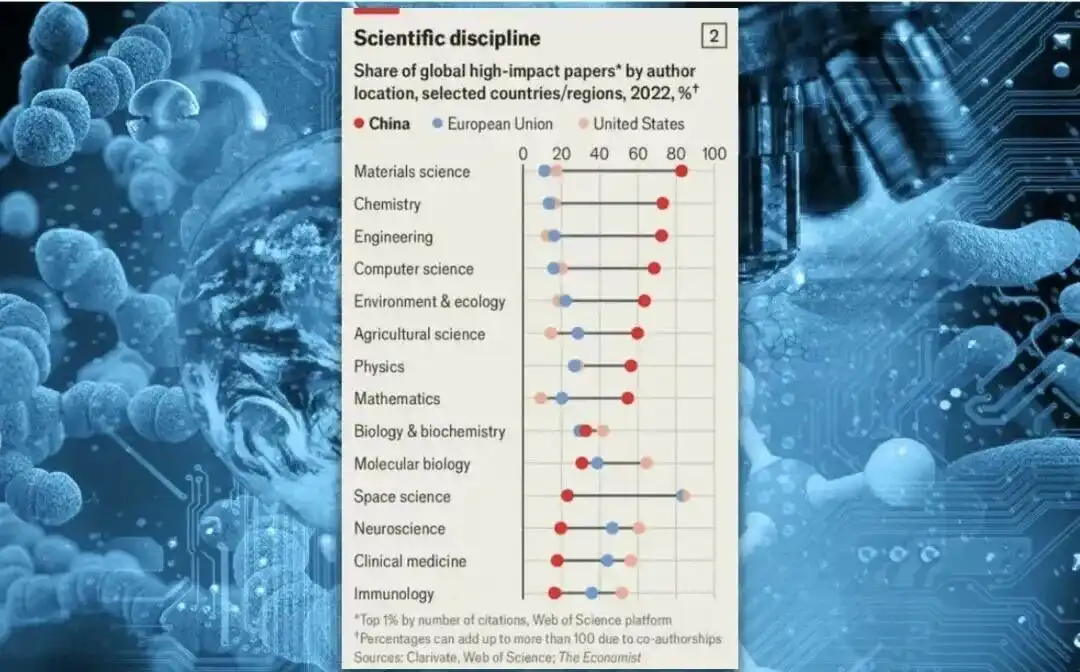

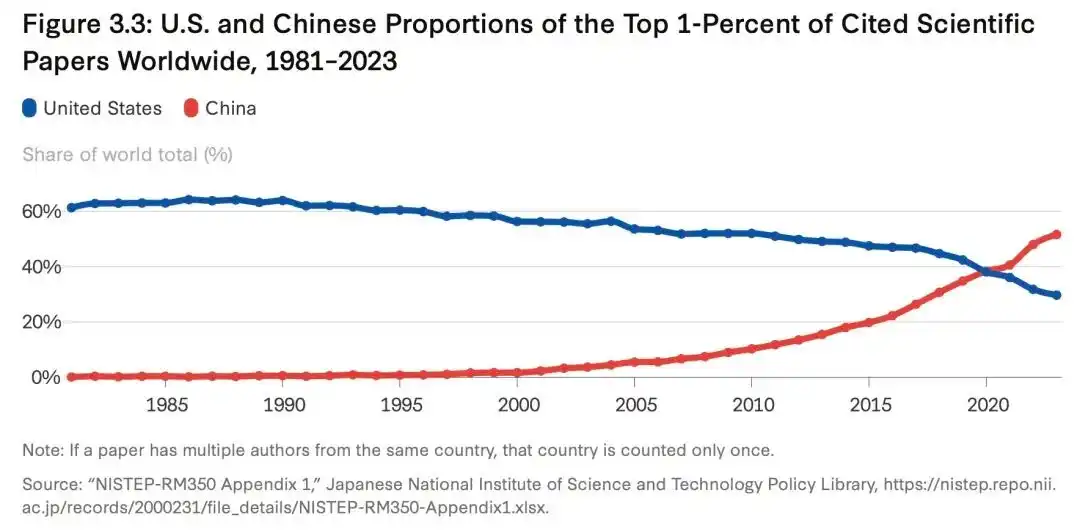

In the 2025 Global Innovation Index (GII), China jumped to 10th place, possessing 24 of the top 100 innovation clusters (with the Pearl River Delta ranking first globally).

The patent numbers also look good: 13.3 patents per 10,000 people.

But if you take a stroll through the Yiwu small commodities market, you'll find that some "innovations" are nothing more than changing the color of a screwdriver handle. Kennedy's team显然也注意到了这一点, they委婉地提到 in a footnote: "There are significant differences in patent quality."

But numbers don't tell the whole story.

However, the acumen of Western think tanks lies in the fact that they were not completely intimidated by these grand numbers. The report points out that China's tech ecosystem still has significant structural shortcomings:

For example, Total Factor Productivity (TFP)—an indicator that measures the real contribution of technological progress—is almost stagnant in China. In other words, you poured so much money in, but the efficiency of the output did not increase correspondingly. Large-scale subsidies often lead to inefficient resource allocation and serious overcapacity.

A deeper problem lies in the断层 of the talent structure. China has 4 million STEM graduates every year (a huge demographic dividend of engineers), but there is still a gap in top-tier frontier breakthroughs and rural education/basic talent cultivation.

And then there's that old, often-talked-about but永远绕不开 topic: intellectual property.

China's innovation ecosystem is too good at "scalable diffusion" and "engineering iteration"—give it a sample, and it can replicate it in one-tenth the time and one-hundredth the cost, and maybe even make it better.

But when you need to create a completely new paradigm from scratch,需要那种 "extremely free trial-and-error space" and "global top-tier interdisciplinary talent network," the inertia of the system becomes a shackle.

However, the situation is definitely improving.

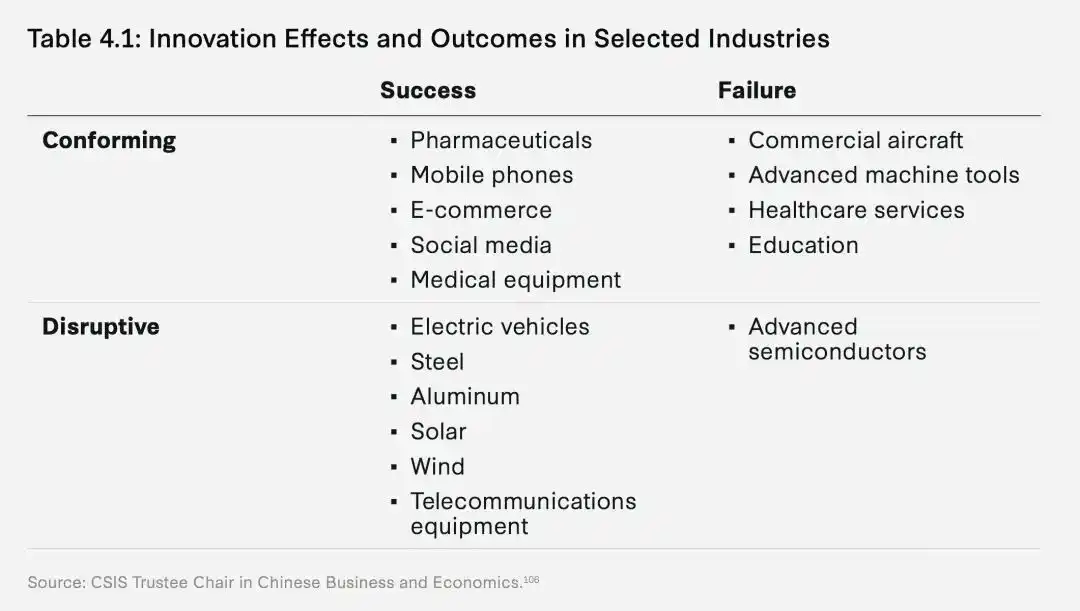

2. The Four-Quadrant Framework

The report includes a four-quadrant chart,

which we find to be the smartest part of the report.

Too many people see Chinese technology as a monolith—either rising comprehensively or about to collapse, but that's not the real world.

The report proposes an "Industrial Differentiation Framework," dividing the successes and failures of Chinese tech into four quadrants based on "the completeness of the domestic ecosystem" and "the degree of coupling with the global market."

Quadrant One:

Disruptive Success

BYD poured $21.9 billion into R&D in 2024, employing 110,000 engineers, which is equivalent to the total number of engineers in the entire Detroit auto industry, and then some.

But money and people aren't the whole story. What really allows BYD and others to横行霸道 on the global market is the "meat grinder" nature of China's EV market.

When Kennedy's team researched in Shenzhen, they found that the average time from concept to mass production for a new car model was only 18 months, while in Germany, that number is 36 to 48 months—In 2024, there were over 100 EV brands fighting it out in the Chinese market, with price wars driving profits down to just a few hundred dollars per car.

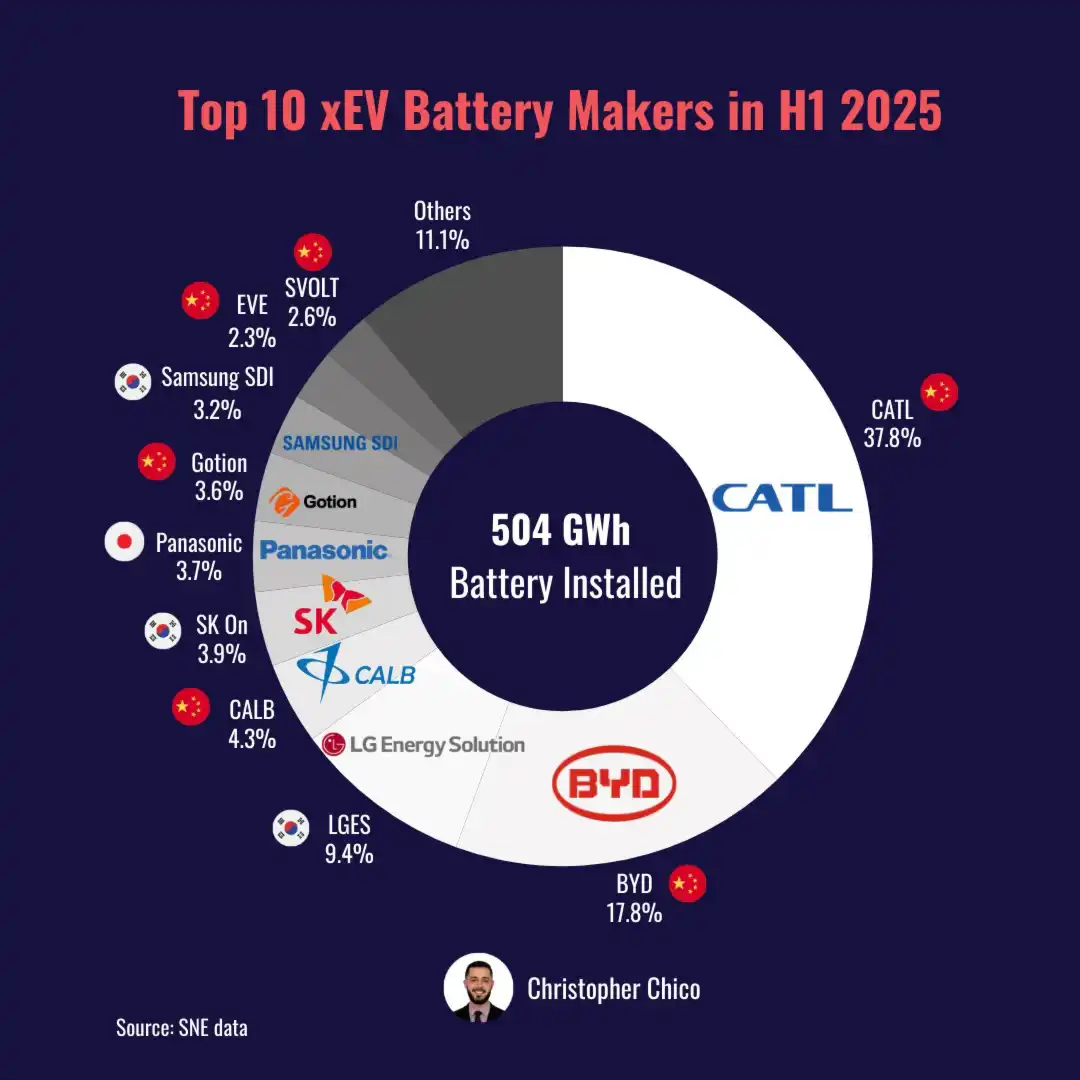

The story of CATL is similar.

They hold 38% of the global battery market share. The government did not "set targets" for them to do this; rather, driven by the market themselves, they built factories next to lithium mines and set up R&D centers next to automakers, forming an近乎偏执的 vertical integration.

When you can turn a battery from raw materials to finished product in 24 hours, and your competitor needs two weeks, the rules of the game change.

"Those who survive are the species that evolved, not those that were designed,"

Quadrant Two

Conforming Success

If electric vehicles represent "overtaking on a curve," biopharmaceuticals took another path—

"Deep Embrace of Globalization."

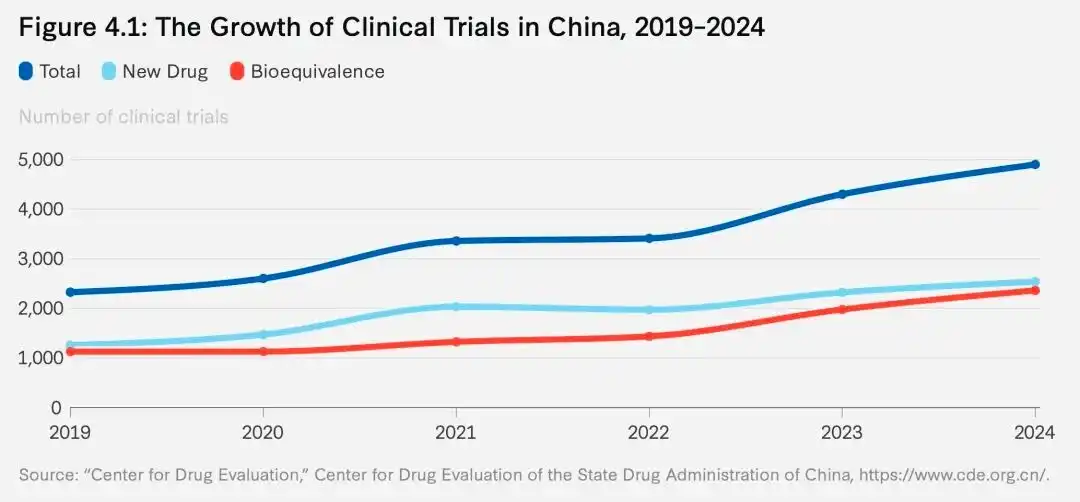

In 2023, China accounted for 39% of global clinical trials. Mainly because China's hospital system can recruit enough patients within three months, a process that might take a year in the US. Time, in the pharmaceutical industry, is money; it's the length of the patent period.

The story of Hengrui Pharmaceuticals is quite representative.

They did not try to invent a completely new cancer mechanism—that requires breakthroughs in basic research. Instead, they chose to引进海归人才, directly benchmark against FDA standards, and embed themselves in the global innovation network.

In 2024, China saw about 1,250 new drugs emerge, most were not "first-in-class" but "me-too" or "me-better" (follow-on improvements). But commercially, this is completely valid.

Quadrant Three

Disruptive Failure

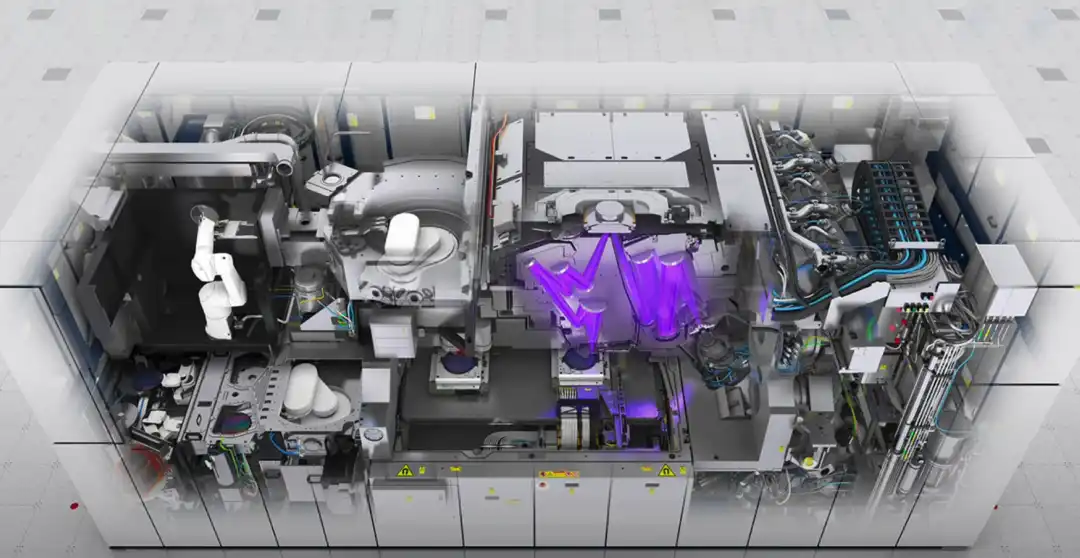

This is the most唏嘘 part. The National Integrated Circuit Industry Investment Fund (Big Fund) invested hundreds of billions of funds; SMIC and YMTC received resources they couldn't have dreamed of.

But the reality in 2026 is:

In mature process nodes (Legacy Chips, meaning 28nm and above "old antiques"), China确实占据了相当的产能; but in advanced processes below 7nm, TSMC and Samsung are still far ahead.

The current EUV lithography machines capable of 3nm, costing about $200 million each,

are currently only made by ASML.

The problem is, semiconductors are not an industry that can be solved by throwing money at it. An EUV lithography machine (Extreme Ultraviolet Lithography) has 100,000 components, sourced from over 5,000 suppliers globally.

ASML can build this machine not because the Dutch are特别聪明, but because they integrated German optics technology, American laser sources, and Japanese special materials.

This is an extremely complex system requiring精细分工 from hundreds of global "hidden champions."

Quadrant Four

Conforming Failure / Inefficiency

The case study in this quadrant is the C919:

In an industry dominated by the Boeing and Airbus duopoly for half a century, good airplanes cannot be built on protectionism and national sentiment alone.

In 2024, COMAC delivered only 16 C919s.

By comparison, Boeing delivered 348 aircraft, and Airbus delivered 735 in the same timeframe.

Furthermore, among those 16 C919s, the engines came from GE (CFM International), the flight control systems from Honeywell, the avionics from Rockwell Collins—the import dependency on core components is as high as 90%.

In reality, policy subsidies can only help you get on the horse. What truly forms a moat is either极致工程效率 forged in the crucible of a red ocean (like EVs), or an open attitude that actively integrates into the world's most advanced innovation networks (like pharmaceuticals).

闭门造车 is a major taboo for technological innovation.

3. Innovation is Power: Converting Technological Potential into Geopolitical Leverage

Technology is never neutral—this sounds like a cliché, but Kennedy spends a full 30 pages arguing it.

In his view, the deep strategic value of China's high-tech drive lies in its ability to substantially reshape the international power structure. The spillover of this power is mainly reflected in two core dimensions:

The hard power of Military-Civil Fusion (MCF) and the soft power of international standards.

1. Military-Civil Fusion

Between 2010 and 2024, China invested approximately $105.8 billion in the Military-Civil Fusion domain.

Where did this money go?

iFlyTek's speech recognition technology is used for military intelligence analysis; the BeiDou Navigation System moved from civilian use to become the cornerstone of precision guidance; DJI's drones—the little things sold on Amazon for filming weddings—became standard for reconnaissance and strikes on the modern battlefield.

The反哺 of commercial technology to China's military strength is real.

But this反哺 is "Supplemental" rather than "Transformative." Inherent trust barriers within the system and interest compartmentalization between departments limit the seamless transfer of disruptive civilian technology into the military-industrial system.

Thus, China has gained asymmetric tactical advantages in areas like AI and drones, but has not fundamentally颠覆 US military technological hegemony.

Why?

Because of trust barriers within the system -- this won't be elaborated on further.

2. Standards Power

Influential without being monopolistic

"Third-rate enterprises make products, first-rate enterprises set standards."

This phrase, widely circulated in Chinese business circles, has another meaning in tech diplomacy: whoever controls the code and protocols controls the rules of the game.

By 2025, China participated in 780 ISO (International Organization for Standardization) technical committees and led 19 working groups in 3GPP (the communications standards body). Huawei's IP share in the 5G field remained around 20%.

Simultaneously, China can leverage its huge domestic market (85% domestic standard adoption rate) to反哺 international standards (e.g., the deployment of HarmonyOS on 36 million devices, the promotion of NearLink technology).

But there is a delicate balance:

International standards organizations are "consensus-driven."

You want to push a standard? Fine, but you must convince other member states. Past lessons are clear—WAPI (China's wireless LAN standard) and TD-SCDMA (3G standard) both became expensive white elephants because they were incompatible with the global ecosystem.

"China has enhanced its 'veto power' and 'agenda-setting power' in global科技治理," Kennedy writes, "but it does not yet possess the ability to unilaterally set the rules of the game."

The subtext of this sentence is:

China can阻止 some things from happening,

but it cannot yet make some things happen according to its own will.

4. The Bankruptcy of Comprehensive Decoupling Theory

Standing at the time node of 2026, you find an interesting phenomenon:

International top think tanks and policymakers have分化出 several截然不同的 camps, and the wind direction is undergoing profound changes.

1. The Anxiety and Counterproductiveness of Hawks/Restrictionists

Represented by some members of Congress and early ITIF (Information Technology and Innovation Foundation) reports, they view Sino-US tech relations as a zero-sum game. Their logic is simple:

If China is strong, the US is weak, so it must be封锁死.

However,越来越多的复盘报告 from think tanks like RAND (RAND Corporation) and Carnegie (Carnegie Endowment for International Peace) point out: overly broad export controls and the generalization of the "small yard, high fence" approach have had the opposite effect—

Cutting off supply not only harms the revenue of US companies (revenue that could have been used for next-generation R&D), more致命的是, it dispels the illusions of Chinese companies, forcing China to build local替代供应链 at an astonishing speed (the return of the Huawei Mate series is clear evidence).

2. The Awakening of the Pragmatists: Managing Interdependence

This is the core soul of the CSIS report and the new consensus of mainstream think tanks like the Brookings Institution: "Comprehensive decoupling" is extremely costly and unrealistic.

What does强行割裂 global supply chains lead to?

Severe inflation in the West—because they can't buy cheap Chinese manufacturing;

A delay in the global green energy transition—because China produces 80% of the world's solar panels and 60% of wind power equipment.

And, the West loses the window to洞察 China's technological evolution—when you stop doing business with your opponent, you also don't know how far your opponent has developed.

3. The Third Voice: The Global South

Reports from the Atlantic Council are极其敏锐地指出 that in the eyes of广大发展中国家 in Asia, Africa, and Latin America, China's 5G networks, affordable electric vehicles, and AI infrastructure represent "affordable development opportunities," not "national security threats."

If the West only peddles "security anxiety" without providing price-competitive alternatives, their narrative in the Global South will completely溃败.

5. The Way Forward: Calibrated Coupling

If "comprehensive decoupling" is poison and "unconditional embrace" is fantasy, then where is the way out?

From the US standpoint, the answer given by CSIS is:

"Calibrated Coupling."

Domestically: Strengthen the local innovation ecosystem (Economic Perspective).

The real confidence of the US lies not in how many Chinese companies it can suppress, but in its unparalleled "beacon effect"—the ability to attract the world's brightest minds, a deep venture capital network, and powerful basic scientific research.

They believe US government subsidies should be precisely targeted at极少数 strategic nodes like semiconductors, rather than开启普遍的 trade protectionism.

Externally: Establish "surgical" guardrails (Realist Perspective).

Abandon "one-size-fits-all" bans, strictly封锁 only key bottleneck technologies (Chokepoints) with direct military use, while restoring and maintaining normal commercial and academic exchanges in areas like consumer electronics, mature process chips, and basic open-source AI models.

In the standards-setting arena, Western governments cannot withdraw from international standards organizations out of fear of China's influence; instead, they should participate more actively, shaping rules conducive to an open system through alliance-building and consensus.

Transnational Cooperation: In areas like climate change, AI safety ethics, and global public health (pharmaceutical clinical trials), deep interdependence and cooperation can bring huge economic dividends and are key "shock absorbers" preventing great power competition from sliding into hot war.

6. Returning Technology to Human Well-being

This CSIS report, along with the密集发声 of major think tanks in 2026, sends an extremely clear signal:

China's high-tech drive strategy is multifaceted.

It has gained momentum in some areas—electric vehicles, batteries, 5G, biopharmaceuticals—that is rewriting the global industrial landscape; but in basic underlying ecosystems—advanced semiconductors, aircraft engines, top-tier basic research—it still faces long-term, structural challenges.

The future global technology landscape is an极其复杂的 "复合竞争与合作."

Whoever can attract global talent with the most open mindset,

Whoever can普惠 technology to广大发展中国家 with the most inclusive ecosystem,

Whoever can maintain restraint and rationality in competition,坚守务实与开放,

Will truly win the next decade.