Editor's Note: As the stock market quickly recovers its wartime losses and approaches historical highs, a narrative that "the risks have been cleared" is once again taking hold. But this article reminds us that if we only look at the equity market, it is easy to misjudge the current real environment.

The signals from bonds and crude oil are inconsistent: rising interest rates and high oil prices point to sticky inflation, limited room for the Federal Reserve to maneuver, and geopolitical conflicts that have not yet truly subsided. In contrast, the stock market is simultaneously pricing in low inflation, the restart of rate cuts, controllable costs, and eased conflicts—a highly idealized set of premises.

The author believes that this round of rebound is driven more by momentum than fundamentals. Driven by trading behavior of "not wanting to miss the rally," prices can deviate from reality in the short term, but ultimately they must return to the range determined by macroeconomic variables.

When divergences occur between different asset classes, the real risk often lies not in who is right or wrong, but in how this divergence is resolved. The current question is not whether the market is optimistic, but whether this optimism has already outpaced the data.

Below is the original text:

"Rule 2: Excessive volatility in one direction often triggers excessive reversals in the opposite direction." — Bob Farrell

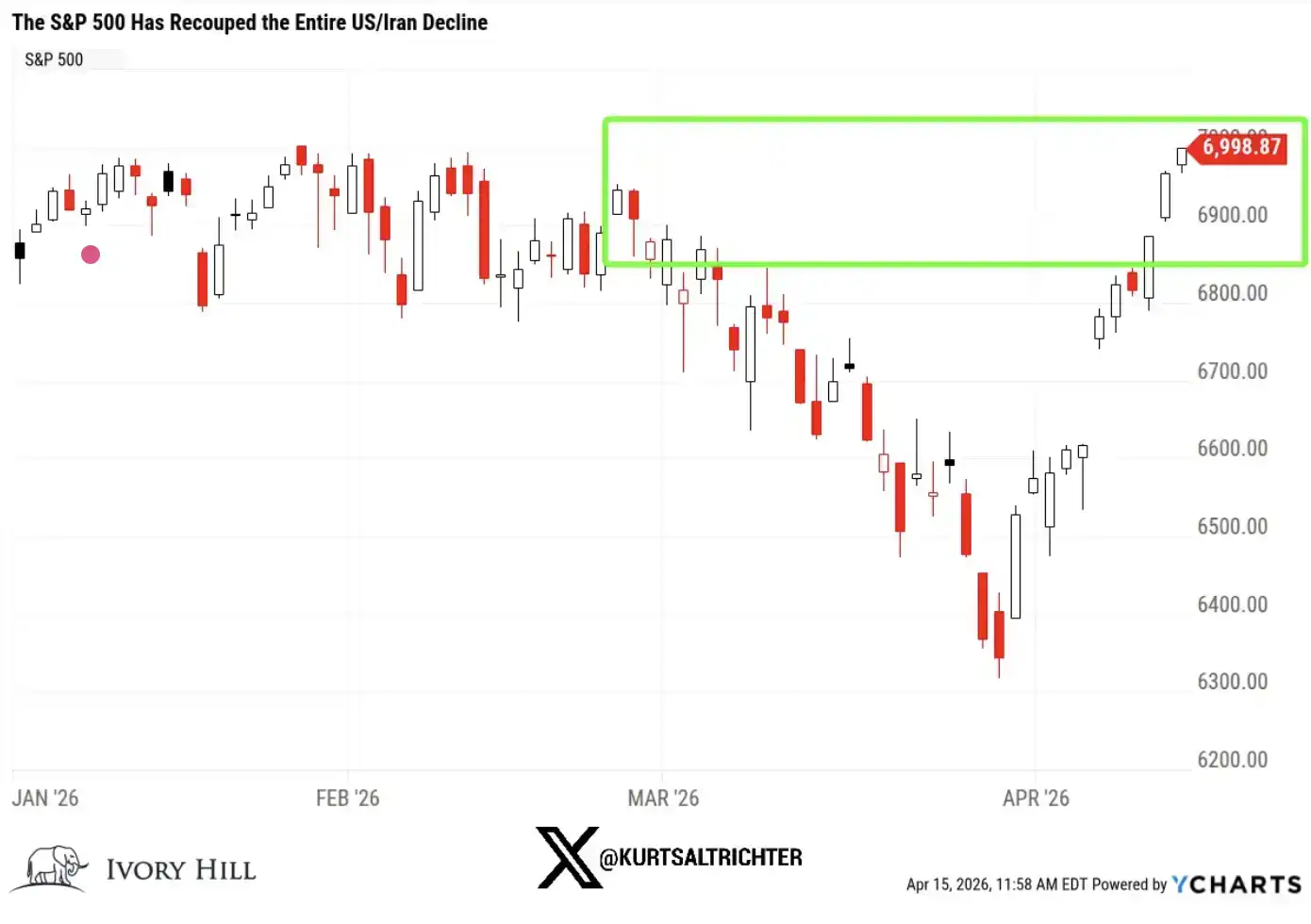

The S&P 500 has completely recovered all its losses during the U.S.-Iran conflict. As of yesterday, the index was 1% higher than on February 27 (the day before the first strike on Iran) and is just one step away (less than 1%) from its historical high.

In just 10 trading days, the market has completed a full round trip.

Let me be blunt: if you only look at the stock market now, everything seems to be "back to normal." The war broke out, the market fell, then quickly rebounded, everything returned to normal, and everyone moved on.

But if you broaden your perspective, this is not what is really happening.

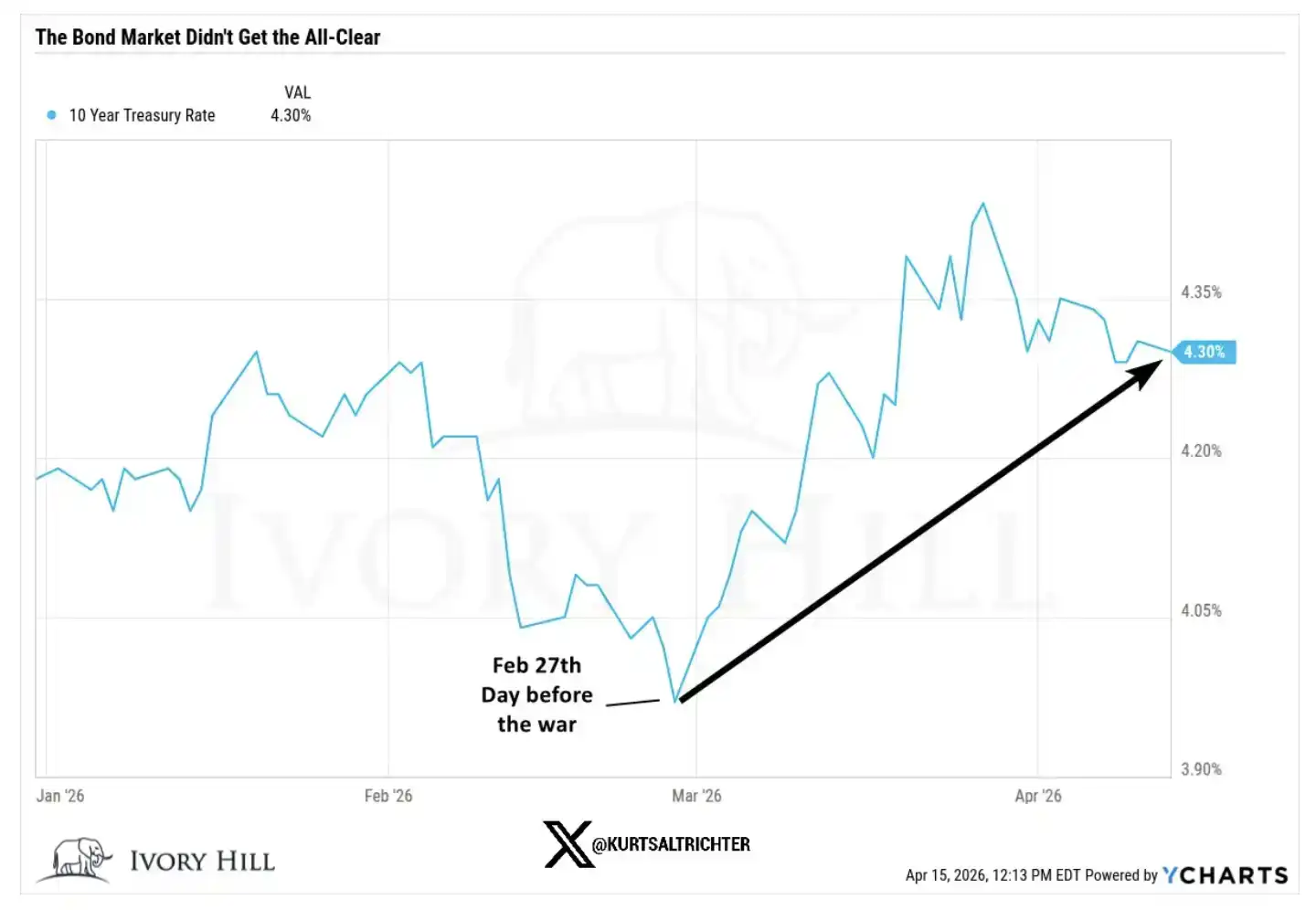

The bond market has not confirmed this rally.

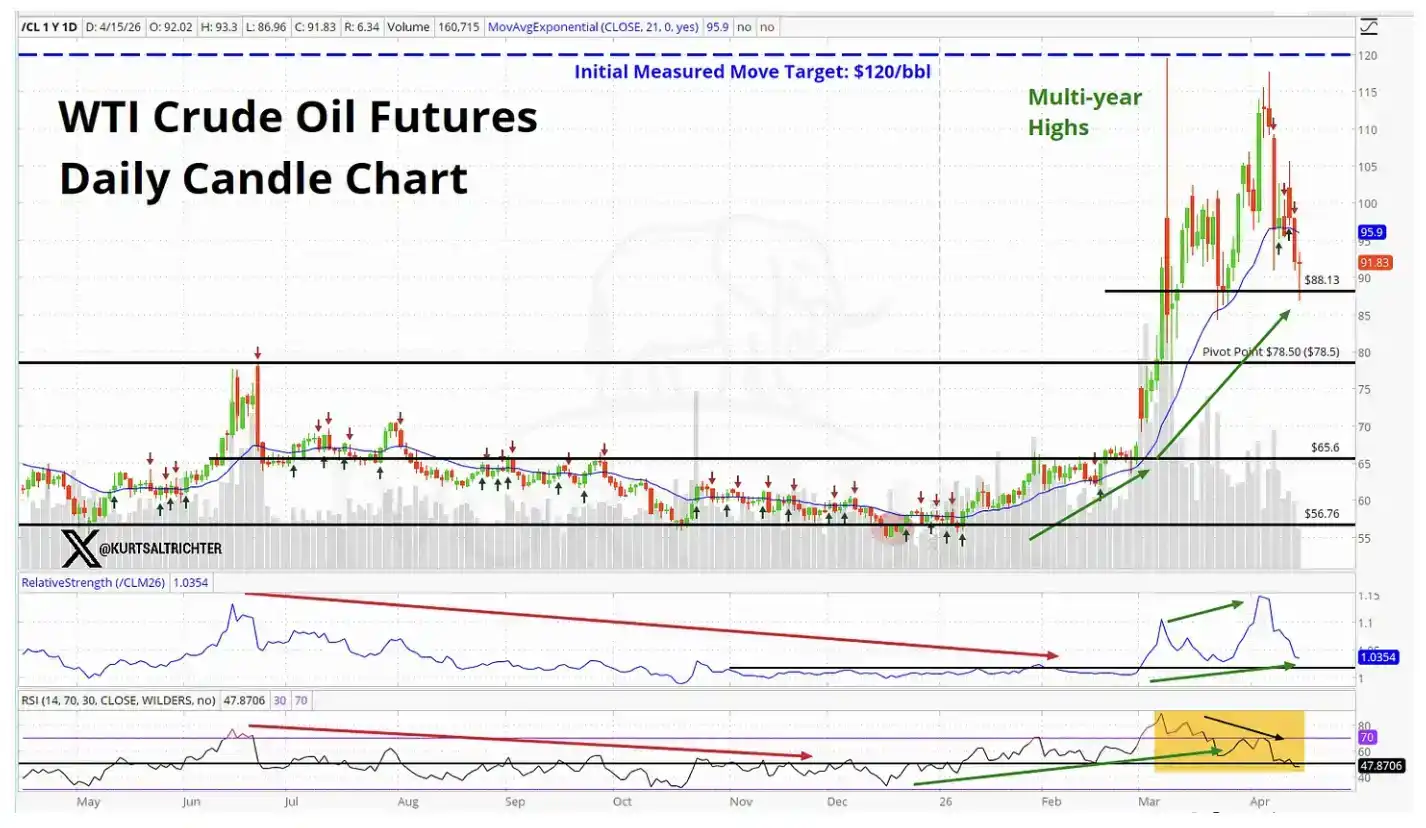

The crude oil market has not confirmed this rally either.

When the two most important markets in the world are telling a different story from the stock market, this is by no means a signal to ignore.

So, what exactly is the stock market pricing in right now?

For the S&P 500 to stand above pre-war levels, the market essentially needs to believe in all of the following simultaneously:

Current oil prices are not yet high enough to substantially suppress consumption.

The Federal Reserve will ignore overheated inflation data and still choose to cut rates.

Higher raw material and transportation costs will not erode corporate profit margins.

The Middle East conflict will be sufficiently close to a resolution within six months and no longer pose a risk.

Maybe things will indeed develop this way. I’m not saying it’s impossible. But this is a rather aggressive set of premises, and the data released by the bond and crude oil markets do not support these assumptions.

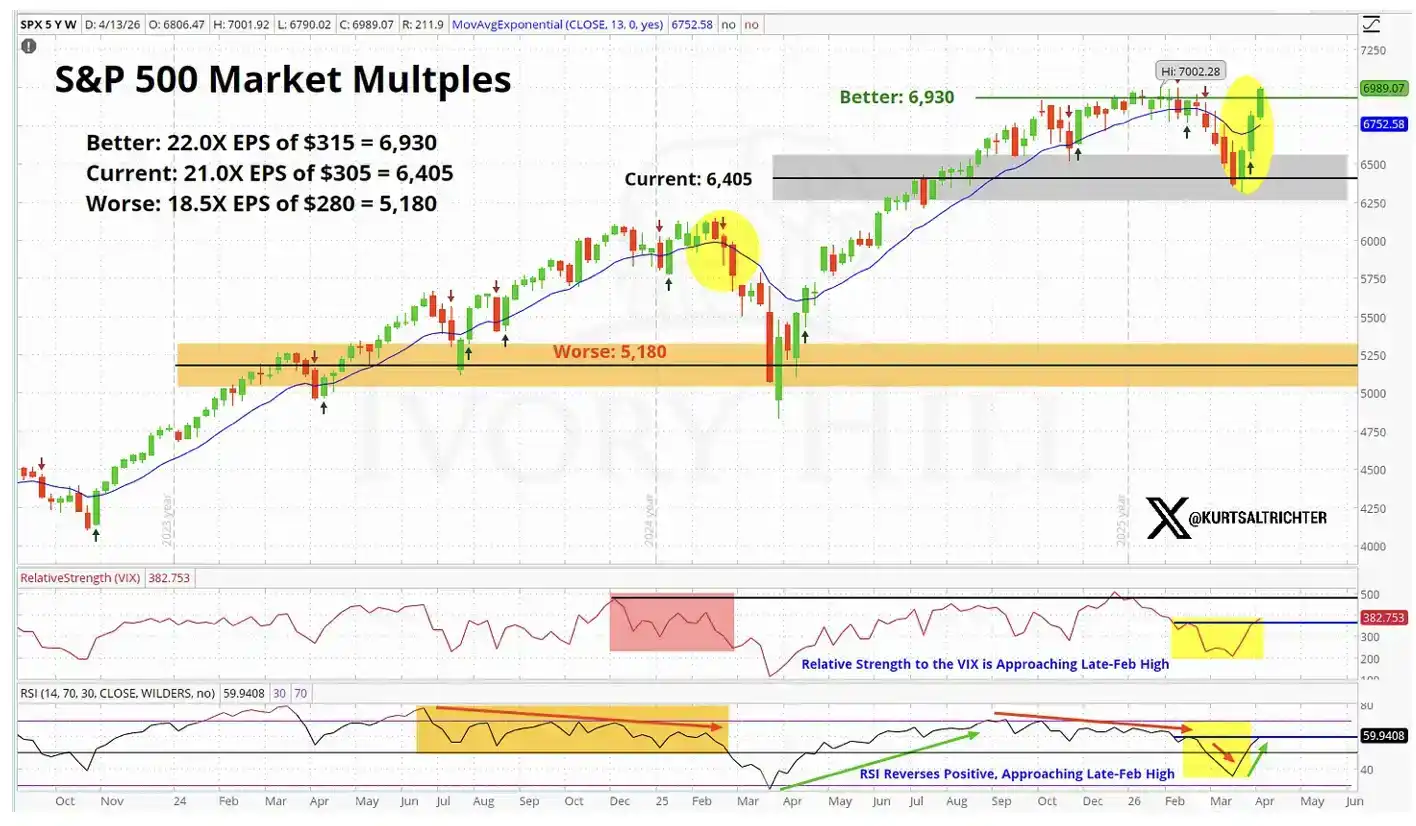

From a fundamental perspective, the stock market’s pricing is already close to a "perfect expectation."

Let’s look at more specific data

On February 27, the day before the war broke out, the closing levels of key indicators were as follows:

10-year U.S. Treasury yield: 3.95%, while yesterday it closed at 4.25%, up 30 basis points from pre-war levels.

WTI crude oil: $67.02, currently about 37% higher than then.

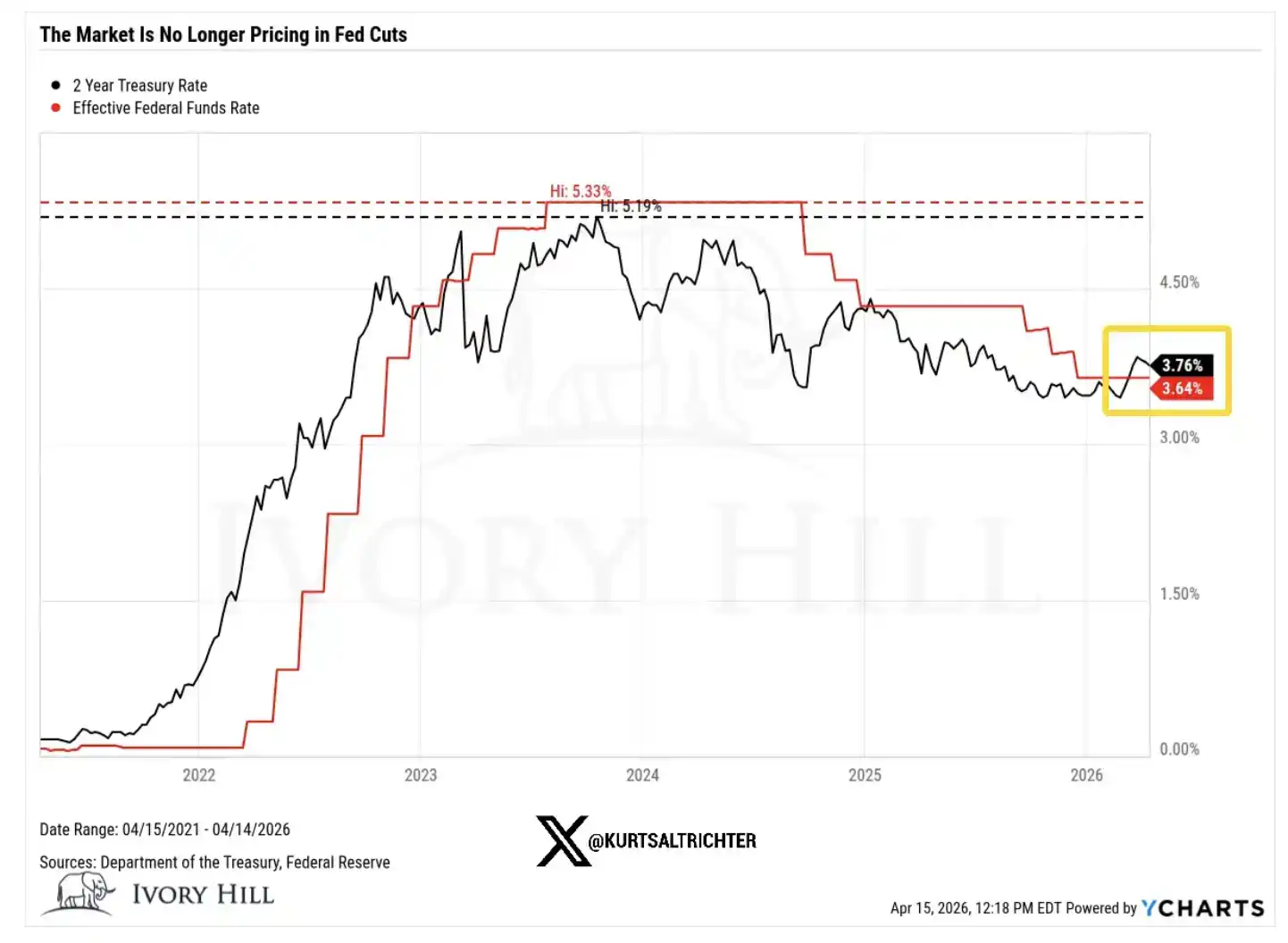

2-year U.S. Treasury yield: 3.38%, yesterday it closed at 3.75%, up nearly 40 basis points from pre-war levels.

Now, let’s break down the implications behind these changes one by one.

The 30-basis-point rise in the 10-year yield after the war broke out is not because the bond market is more optimistic about economic growth. Consumer sentiment is weakening, and confidence remains fragile. This rise in rates is essentially the bond market "quietly" pricing in inflation.

The signal it sends is clear: higher oil prices are transmitting to the overall price system, and the Federal Reserve’s future policy space may not be as accommodative as the stock market assumes.

A 37% rise in oil prices over 6 weeks is not the performance of a market that believes a real, lasting agreement between the U.S. and Iran is imminent.

If traders were truly confident in a stable ceasefire agreement, oil prices should have already fallen back to the $70 range and continued to decline. But that is not the reality. Oil prices remain high, meaning the crude oil market is not pricing in the same "conflict nearing resolution" expectation as the stock market.

And the 2-year U.S. Treasury yield is still 40 basis points higher than pre-war levels, which is itself a direct challenge to the narrative that "the Federal Reserve is about to cut rates."

The 2-year yield is the most sensitive indicator for observing interest rate expectations; it reflects the Federal Reserve’s policy path more directly than any other asset. Right now, it is sending a signal: the Fed’s room to maneuver is smaller than the market imagines. This affects almost all the valuation logic supporting the current stock market rally.

So, who is right?

The stock market might be right, I’m willing to admit that. If a substantive ceasefire agreement truly emerges, bond yields could quickly fall back; once supply issues are credibly resolved, oil prices could also drop significantly. This wouldn’t be the first time the stock market leads, with other markets "catching up" or following later.

But there is another explanation that I believe is currently underestimated.

A large part of this rally is not driven by fundamentals but by momentum. Traders are reluctant to short in an upward trend, and this behavior itself continuously pushes the market higher. Such buying can indeed sustain the trend longer than it should.

But it doesn’t change the underlying logic.

And the underlying reality is: oil prices remain high, interest rates are still rising, and the Federal Reserve’s room for rate cuts is more limited than what the bulls need.

Rallies driven by fundamentals are often more sustainable; those driven by momentum are typically more fragile and shorter-lived. When considering whether to add positions near historical highs, this difference is particularly crucial. As the market valuation chart above shows, the current stock market is already pricing in a "perfect scenario."

My actual judgment

Over the past 10 days, the situation has indeed improved, I won’t deny that. I’m not someone who sings doom without reason.

But there is still a clear gap between the stock market’s pricing and the reality reflected by bonds and crude oil, and this gap has not narrowed. I am closely watching this.

Currently, the stock market is at the most optimistic end of the range; bonds and crude oil are closer to the middle, reflecting a world where inflation still exists, the Federal Reserve’s policy space is limited, and the conflict is not truly resolved.

This divergence will eventually be resolved, and there are only two paths:

Either a real ceasefire agreement is reached, oil prices fall back to around $70, the Federal Reserve gains clear room to cut rates, ultimately proving the stock market right;

Or none of this happens, and the stock market falls back, moving closer to the levels currently reflected by bonds and crude oil.

And right now, bonds and crude oil show no signs of moving toward the stock market; it seems more like the stock market needs to decline to "align" with them.

The next inflation data will be released on May 12. If my judgment is correct and the CPI is above 3.5%, the 2026 rate cut narrative will basically be over.

If you continue to add positions at this level, you are essentially betting that everything develops in the most ideal direction: the war ends smoothly, without interference from "Trump’s sudden remarks"; inflation remains controllable; the Federal Reserve cuts rates as planned; corporate profits hold steady. These four things must all happen simultaneously. If any one of them deviates significantly, the market’s downward adjustment process could be swift and severe.

In comparison, I prefer to remain patient rather than chase a rally that is "quietly denied" by two key asset classes. If long-term signals point to buying, we will naturally gradually increase positions according to our strategy.

And don’t forget—the only certainty is that everything will eventually change.