On‐chain data shows that in the days after joint US‐Israeli airstrikes on February 28, Iranian exchanges saw a sharp spike in withdrawals, with roughly 10.3 million dollars in crypto fleeing.

Iran’s Crypto Use Amidst Economical Collapse

Crypto has become a financial lifeline for both ordinary households and state‐affiliated networks in Iran, according to an article posted on our sister website NewsBTC. Years of US and EU financial and oil sanctions have strained the economy, cutting Iranian banks off from SWIFT and dollar funding, and now even targeting Iran‐linked crypto platforms through recent US Treasury designations. Add to this cocktail a runaway inflation and a collapsing rial, and it becomes clear why many Iranians increasingly look to Bitcoin and stablecoins as an alternative store of value and cross‐border payment rail.

A Lifeline Of Hope For Ordinary Folk?

Chainalysis has estimated that Iran’s crypto activity reached roughly 7.78 billion dollars in 2025, with usage spiking around protests, bombings and other security crises as people rush to move funds off local platforms and into self‐custody.

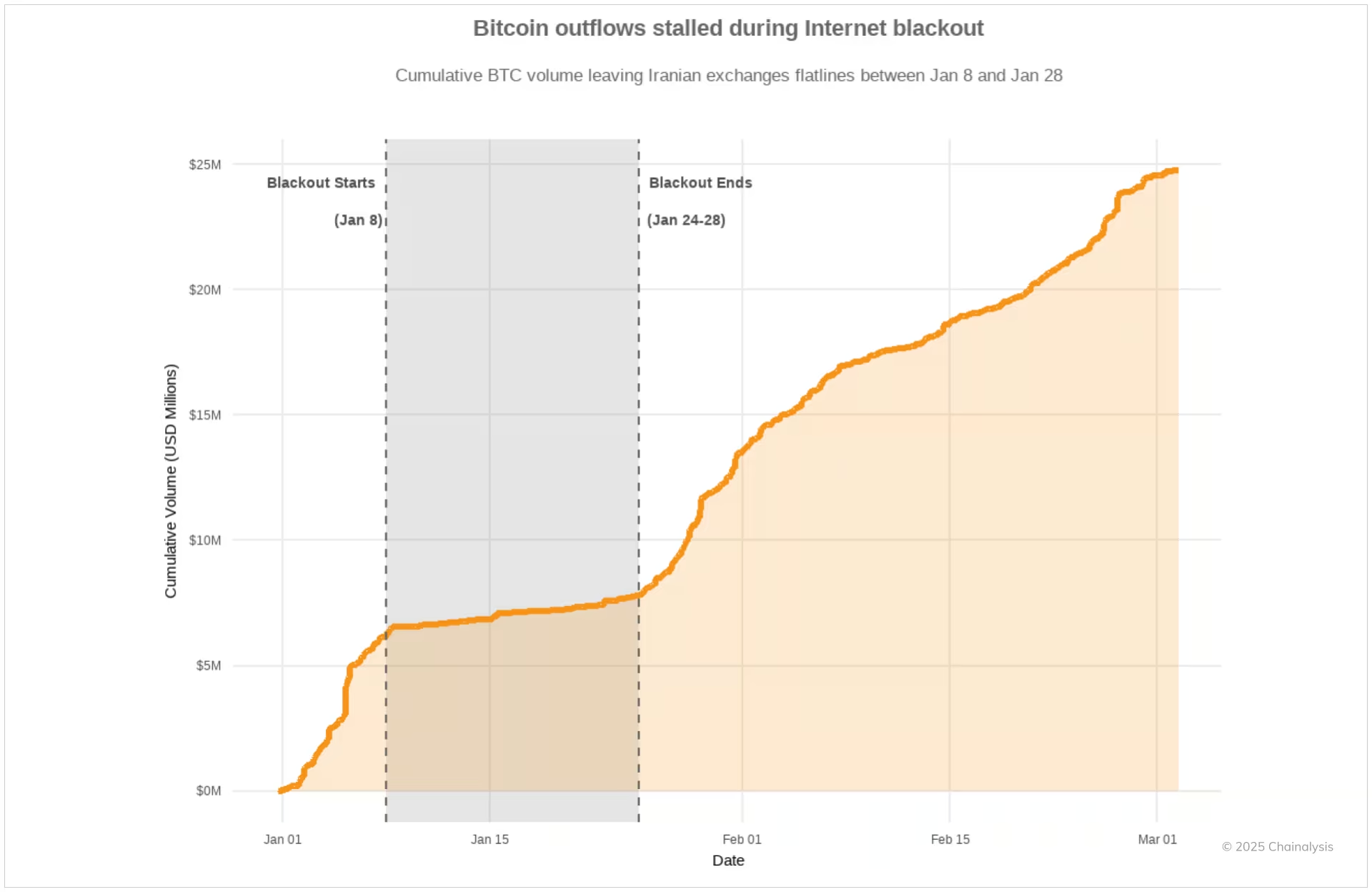

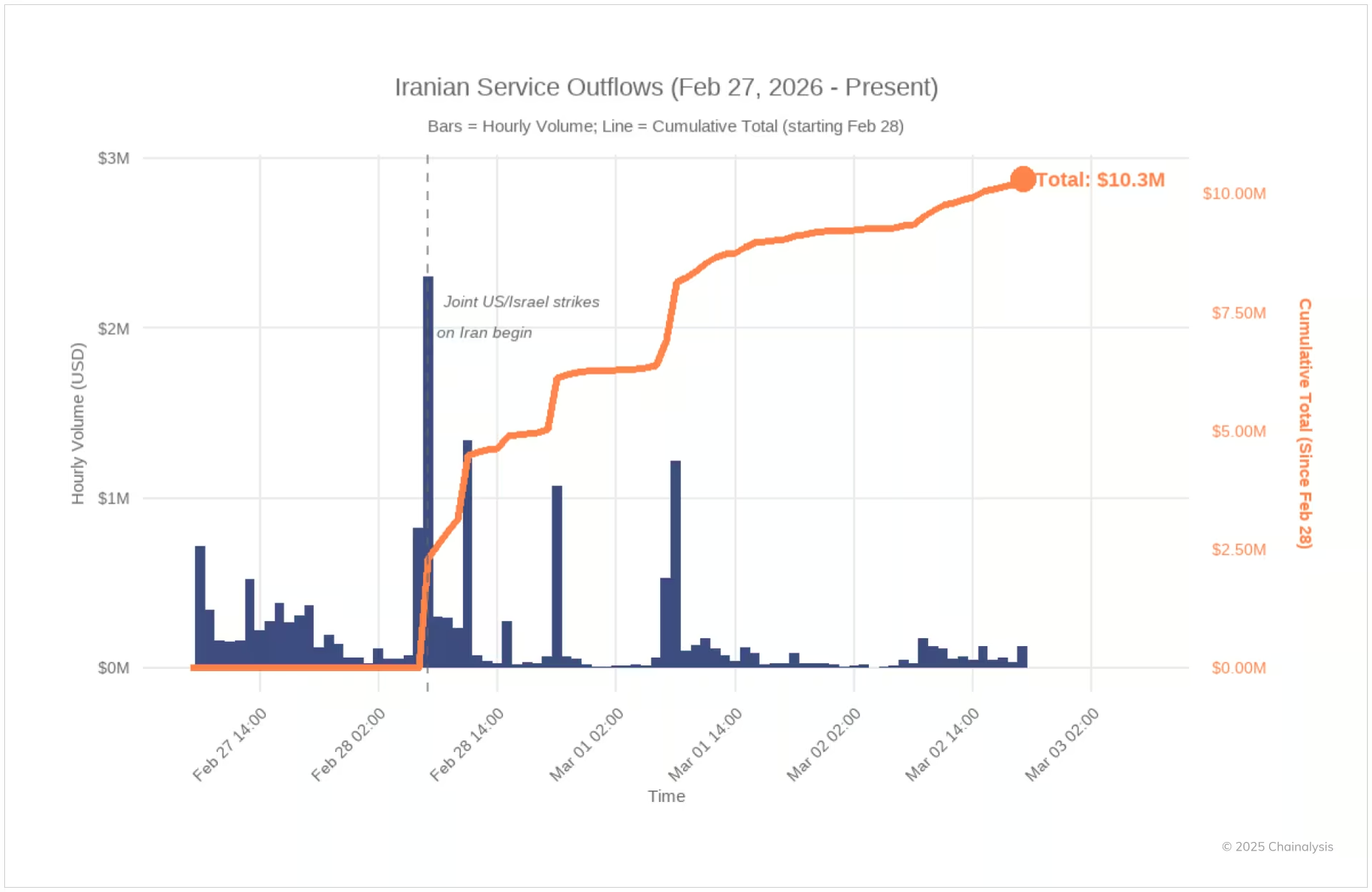

In its latest report, Chainalysis visualizes this idea with a series of charts that track hourly outflows from major Iranian exchanges before and after the February 28 airstrikes.

Bitcoin outflows stalled during Internet blackout. Source: Chainalysis

The graphs show relatively modest, choppy activity in the hours leading up to the strikes, followed by a sudden jump where hourly withdrawals approach or exceed roughly 2 million dollars and cumulative outflows climb to about 10.3 million dollars by March 2.

Iranian service outflows (Feb 27, 2026 - Present). Source: Chainalysis

For many ordinary Iranians, Bitcoin and stablecoins now function as a hedge against currency collapse and capital controls, while addresses tied to the Islamic Revolutionary Guard Corps (IRGC) account for roughly half of on‐chain activity, highlighting crypto’s dual role as both a survival tool and a sanctions‐evasion channel.

However, it is worth noting that while some observers praise Chainalysis for helping exchanges and regulators track hacks, scams, and sanctions evasion, civil‐liberties advocates criticize its tools as opaque and potentially overreaching in terms of financial surveillance.

What This Means For The Future Of Iranians

For ordinary users, digital assets may remain a pressure valve against inflation and capital controls, even as regulators tighten the screws on Iran‐linked platforms and wallets. For policymakers, the question now is whether new rounds of enforcement will meaningfully curb sanctions evasion or imply push more of Iran’s crypto activity into harder‐to‐track channels.

What is for sure is that the the latest spike in Iranian exchange outflows comes to show, once more, how quickly crypto reacts to geopolitical shocks and sanctions risk: the market is, after all, in the hands of the people.

BTC's price trends to the downside on the daily chart. Source: BTCUSDT on Tradingview

Cover image from ChatGPT, BTCUSDT chart from Tradingview