Doubao is also going to charge.

On May 4th, Doubao quietly updated the App Store page with a statement regarding its paid version services. The statement indicated that, in order to better serve professional users, Doubao will launch a paid subscription system with more value-added services while retaining the free version. It also disclosed three pricing tiers: Standard version at 68 yuan / month, Enhanced version at 200 yuan / month, and Professional version at 500 yuan / month.

Image source: Geek Park

The news immediately sparked heated discussions. Some are worried about the end of free benefits, some complain the pricing exceeds expectations, while others predicted this day would come long ago. After all, with 320 million monthly active users and 1.8 billion daily conversations, relying solely on a free model is not sustainable in the long run.

Essentially, this is something the entire industry has 'anticipated and is capable of' doing: the unsustainability of the free model for domestic large language models is a publicly acknowledged consensus. Leading players have long been experimenting in the paid subscription arena. ByteDance holds the absolute No. 1 user base for C-end AI in China. Launching a paid subscription was never a question of technical capability, but a matter of timing.

So, at a time when C-end subscription businesses are notoriously difficult in China and large model price wars have driven costs to the floor, can Doubao's commercialization effort succeed?

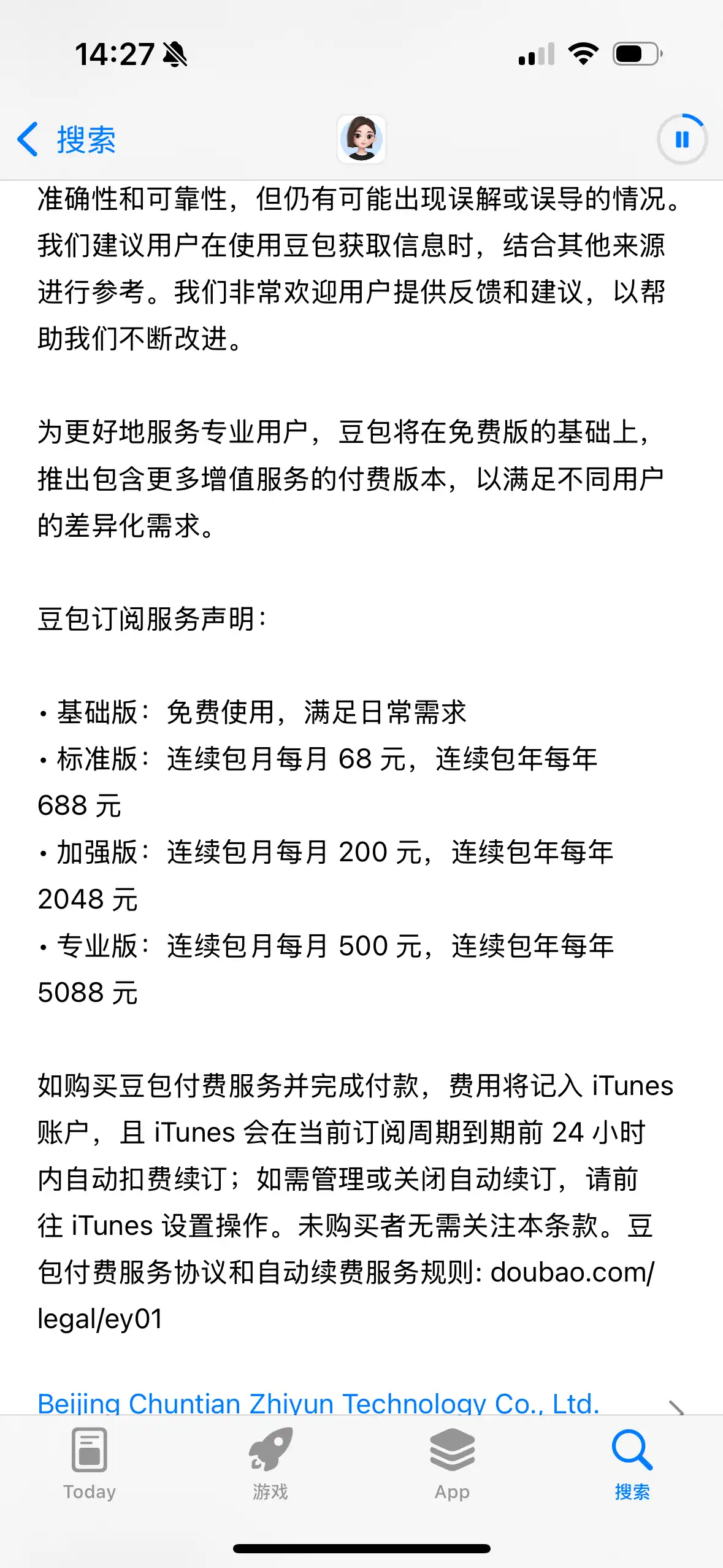

The Free User Base and Up to 5088 Yuan/Year

According to reports, Doubao's paid features will mainly focus on complex tasks and productivity scenarios, such as PPT generation, data analysis, and video production. As model capabilities continue to upgrade, the product can already fulfill an increasing number of complex, high-value tasks. However, such tasks consume more computing power and inference time, hence Doubao plans to launch paid services to better serve these complex scenario needs.

As for the free version, Doubao officially responded, 'Doubao will always provide free services. On top of the free services, Doubao is also exploring offering more value-added services to meet the differentiated needs of different users. Specific details of the relevant plans are still in the testing phase. Complete information will be released through official channels when formally launched.'

In other words, functions that users can currently perform for free with Doubao—like searching information, writing basic copy, daily Q&A, and learning assistance—will likely remain free in the future. The core logic of the paid version is to offer 'value-added services' and will not affect the daily user experience for the average user.

This strategy is not new. Global leading AI products like ChatGPT and Claude have adopted a tiered model of 'basic free + advanced paid': first using free features to penetrate user mindset and cultivate habits, then using higher-order capabilities to serve core users willing to pay for value.

As for the 500 yuan / month pricing, is it expensive?

Looking at the number alone, the 500 yuan / month Professional version pricing does set a new upper limit for domestic general-purpose AI assistants. But placed within the global pricing system of AI products, the conclusion becomes quite different.

Comparing with the paid pricing of global mainstream AI products as of May 2026: First, the 68 yuan Standard version is only about 10 yuan higher than Baidu's ERNIE Bot and iFlytek's Spark, basically aligning with the mainstream benchmark for domestic AI paid services and not deviating from the acceptable range for mass users. Second, the 200 yuan Enhanced version falls within the same price range as ChatGPT Plus and Claude Pro's 145 yuan monthly fee, targeting users with high-frequency productivity needs comparable to global leading AI products. Third, the 500 yuan Professional version indeed reaches a high-end price tier for the first time among domestic general AI products, but does not touch the global pricing ceiling of products like ChatGPT Pro or Claude Max. Essentially, it's an exploration of the payment capability of heavy-duty professional users in China.

However, the perception of pricing as expensive or cheap has always been solely related to value alignment.

500 yuan / month might be just a month's worth of coffee or an ordinary meal for two for many people. For content creators, programmers, or small-to-medium business owners who interact with AI daily for core production work, a 24/7 online, all-capable assistant that can write, calculate, and analyze at a cost of 500 yuan per month is far cheaper than hiring staff. But for average users who only occasionally search for information or write emails, even the 68 yuan Standard version is unnecessary.

Entering at This Timing, ByteDance Has Calculated Two Accounts

Why now?

Before discussing whether Doubao's paid model can succeed, a more critical question is—why did ByteDance choose to enter at this timing?

After all, ByteDance hasn't been the fastest on the paid front. Players like Baidu's ERNIE Bot, Moonshot AI's Kimi, and iFlytek's Spark launched mature subscription systems as early as 2024, while Doubao didn't officially make its move until 2026. It's likely because, at this moment, ByteDance has clarified two calculations.

The first is the growth account: the marginal benefits of trading free service for scale have nearly run their course.

QuestMobile data shows that as of May 2026, Doubao's monthly active users have exceeded 345 million, with daily conversations reaching 1.8 billion, firmly holding the top spot among domestic C-end AI applications. It covers the full spectrum of users from students and office workers to creators and small-to-medium business owners.

The domestic internet user base is limited. Users who should have been exposed to AI are basically already covered. Relying on an entirely free model to burn money no longer brings new growth; instead, it incurs real computing power costs for every new conversation.

The second is the market account: user education for domestic AI paid services is already complete.

When large models first exploded in 2023, domestic users' perception of AI was still at the 'novel toy' stage, with strong resistance to paying. But by 2026, the industry has completed a full user education cycle.

Industry data shows that in 2025, the paid conversion rate for domestic AI tool users increased from 8% in 2024 to 11%. Among them, frequent-using professionals and creators showed a willingness to pay exceeding 30%. Users have generally accepted the commercial logic of 'basic features free, high-value productivity capabilities paid.'

Entering at this timing, ByteDance no longer needs to do the heavy lifting of market education; it just needs to convert from the existing pool of paying users.

Chips and Challenges

The difficulty of C-end subscription business in China is evident to all: an annual renewal rate of 30% for tool-based products is considered top-tier in the industry; price war involution is the norm; and user switching costs are almost zero.

The core conflict in the large model paid business is balancing 'paid revenue' and 'computing power costs.' ByteDance holds top-tier technical advantages in China on this front.

The essence of large model commercialization is a calculation: can revenue cover computing costs?

This is an industry-level challenge. Users willing to pay are often the heaviest users; and high-frequency usage means higher computing power consumption.

ByteDance's advantage lies in having achieved first-tier domestic performance in model efficiency and cost control—according to publicly available technical data, Doubao 2.0 achieved a 43% improvement in inference efficiency. First token latency in long-context scenarios is reduced by over 25% compared to mainstream industry models. Request success rate in high-concurrency scenarios reaches 99.98%, with stability in the industry's first tier. Simultaneously, its cost per 10k tokens for inference is only 38% of that for the compliant domestic deployment of leading overseas models. This significant cost advantage allows it to better support the stable operation of high-computing tasks in the paid version.

Image source: Visual China

However, several structural issues in the domestic C-end subscription market remain unsolved by any player to date, and ByteDance might be no exception.

The first problem is that users are willing to pay, but not to keep paying. Over two decades of free internet culture in China are ingrained in users' bones, which is a core challenge all subscription products face.

Even today, an annual renewal rate of 30% for domestic C-end tool products is considered top industry level, while renewal rates for similar overseas products are generally above 60%. The core reason is that domestic users' payments are often 'emergency payments': they subscribe for a month to write a proposal or complete a project this month, then cancel immediately after use, lacking the habit of sustained long-term payment.

More crucially, ByteDance has no proven success in this area. ByteDance's past commercialization success relied primarily on advertising, e-commerce, and live-streaming gifts, not To-C subscription business. Even value-added memberships for products like CapCut or Douyin are supplementary revenue streams; they have never built a tiered subscription system for a national-level core product. Facing the industry-wide challenge of 'low sustained payment willingness' among domestic users, ByteDance has no ready-made solution. This is the biggest unknown.

The second problem lies in the 'replaceability' of the paid value.

Currently disclosed core paid functions for Doubao include in-depth long document reading, PPT generation, deep data analysis, and batch high-definition image generation. These are essentially industry-standard capabilities—most competitors' free versions in China can already provide basic services for these functions, and many can even be implemented completely for free via local deployment of open-source models.

If Doubao's paid version can only offer 'faster response speeds, more API calls, and slightly improved model capabilities' without delivering a crushing experience upgrade and irreplaceable exclusive value, users simply will not develop sustained payment willingness. Even ByteDance's ecosystem integration, if it's only shallow functional connectivity rather than a truly embedded, closed-loop experience within users' production workflows, cannot form a real payment imperative. The likely outcome is the industry-wide ailment: 'brisk initial-month trial payments, followed by high cancellation rates the next month.'

The third problem is the 'bottomless pit' of computing costs. This is the most central and hardest-to-solve contradiction.

Theoretically, more paying users mean higher revenue. But in the AI realm, more paying users might also lead to costs rising simultaneously or even faster. Without usage limits, paid revenue might not even cover costs, eventually forming a death spiral of 'more paying users, heavier losses.' If usage is limited, it directly damages the paid experience, triggering user dissatisfaction and reputational damage, trapping the product in the dilemma of 'limit frequency and lose users, don't limit and lose money on costs.'

This is an almost unsolvable balancing act. Even ChatGPT hasn't solved it—ChatGPT's operational losses exceeded $5 billion in 2024, with subscription revenue far from covering costs. Even with stronger cost control capabilities, ByteDance would find it hard to completely escape this industry-wide death spiral.

Finally, the price war will inevitably return.

The competitive logic in the domestic market is simple: once a product proves it 'can make money,' other players quickly follow, then use pricing to undercut.

Once competitors start a new round of price cuts, subsidies, or free membership involution, Doubao will face a dilemma: follow the price cuts and fall into the 'low-price trap' it deliberately avoided, disrupting its original pricing system and cost model; or don't follow and face mass exodus of price-sensitive users.

ByteDance has won in many sectors through low prices and subsidies, but this time, it's the one with higher pricing. Whether it can withstand the involution and insist on value-based pricing is a huge test.

A Good Start is Easy, the Long Run is Hard

Returning to the core question: can Doubao's paid subscription succeed?

The answer is quite clear. Achieving scaled paid users and completing preliminary commercialization in the short term is highly probable. But whether it can establish a healthy, profitable closed-loop in the long run and become a benchmark for domestic C-end AI subscriptions is filled with uncertainty.

Short-term, the base of 345 million monthly active users is there. Even achieving just a 1% paid conversion rate could quickly form a paying user base of 3.45 million.

Long-term, whether this endeavor truly succeeds does not depend on its user scale, nor the strength of its model capabilities, nor even the obviousness of ByteDance's ecosystem advantages. It depends on whether it can solve two fundamental problems: First, can it truly translate ByteDance's ecosystem advantages into an irreplaceable payment imperative for users, rather than a dispensable marketing gimmick? Second, can it escape the industry death cycle of domestic C-end subscriptions—'low-price involution, low renewal rates, cost inversion'—and find a truly healthy and sustainable business model?

For the entire domestic AI industry, Doubao's commercialization effort holds benchmark significance far beyond the product itself. If Doubao succeeds, then the domestic large model industry has found a viable path for C-end commercialization that doesn't rely on low-price involution. If it ultimately stumbles on the industry's structural challenges, then domestic large model players need to rethink: how can the path of C-end subscriptions truly be made viable?