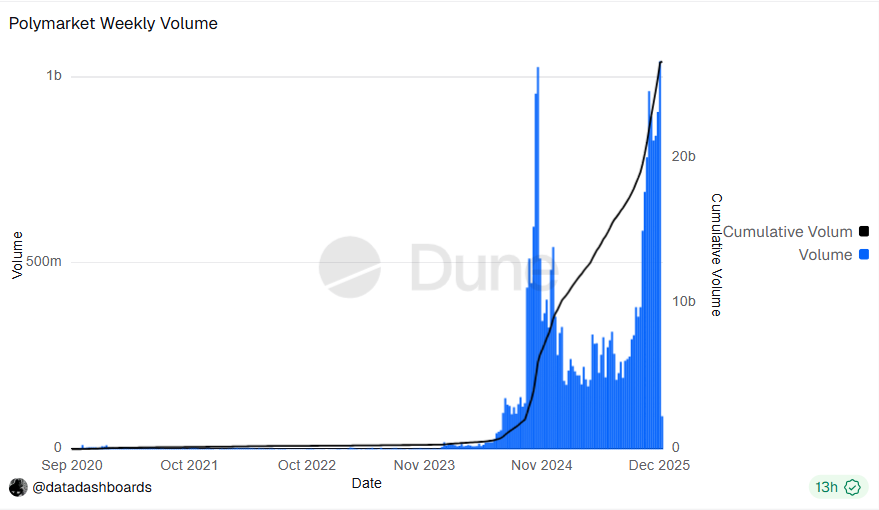

Prediction markets like Kalshi and Polymarket are growing, generating billions of dollars in volume. But some observers are concerned about the ethical problems and potential credit risks posed by major prediction betting platforms.

Last week, Polymarket saw a notional volume of over $1.2 billion, according to Dune Analytics. Media giant CNBC has entered into a partnership with prediction market Kalshi to integrate prediction data in its TV, digital and subscription platforms.

On the back of this success, Kalshi co-founder Tarek Mansour has mentioned creating “a tradable asset out of any difference in opinion,” stating that prediction markets could soon surpass the stock market in size.

Regulators in some jurisdictions are taking efforts to curb their activities. Concerns over wash and insider trading have surfaced in recent weeks, and some analysts believe it’s making credit risks worse.

Russo-Ukrainian War map altered, prediction market bet resolved

Prediction markets have opened up a range of possibilities for setting wagers on events. These can range from a specific element of a sports match to the outcome of a war. In some instances, this has led to insider manipulation to resolve a market in a certain way.

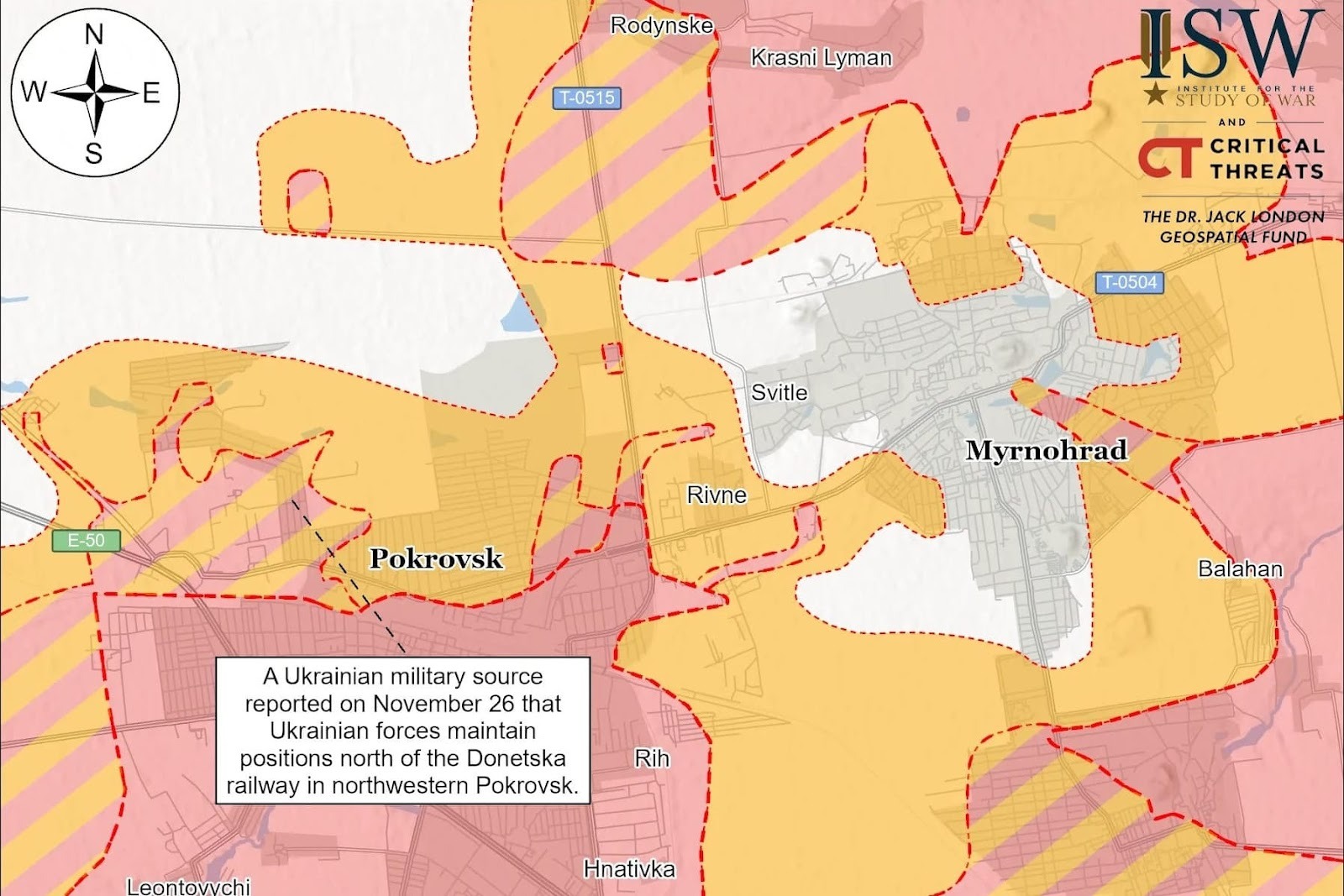

This is what may have happened in November, when the Institute for the Study of War (ISW) announced an unauthorized edit to its map of the Russo-Ukrainian War. The map is used by media organizations worldwide to track changes to frontline positions.

The edit concerned the ISW’s map of Myrnohrad, where Ukrainian troops have been defending the city against the Russian Pokrovsk offensive since July 2024. The unauthorized change to the map of the city coincided with the resolution of a bet on Polymarket, “Will Russia capture Myrnohrad by...” and then a series of dates.

The market resolution was triggered if Russia held an intersection between two streets, Vatutina Vulytsya and Puhachova Vulytsya. According to 404 Media, on Nov. 15, someone edited the map to show Russian troops had taken the intersection. Just minutes after the market resolved, the edit disappeared.

The updated Nov. 17 ISW map did not show that Russian forces controlled the intersection. Source: ISW, 404

The ISW announced the unapproved edit on Nov. 17. It noted that, “The map does not represent battlefield changes in real-time, and all adjustments made during our workday are subject to review and change over the course of the day.”

In this instance, not only was insider knowledge allegedly used to manipulate data, but that manipulation could have affected the public perception of an ongoing violent conflict.

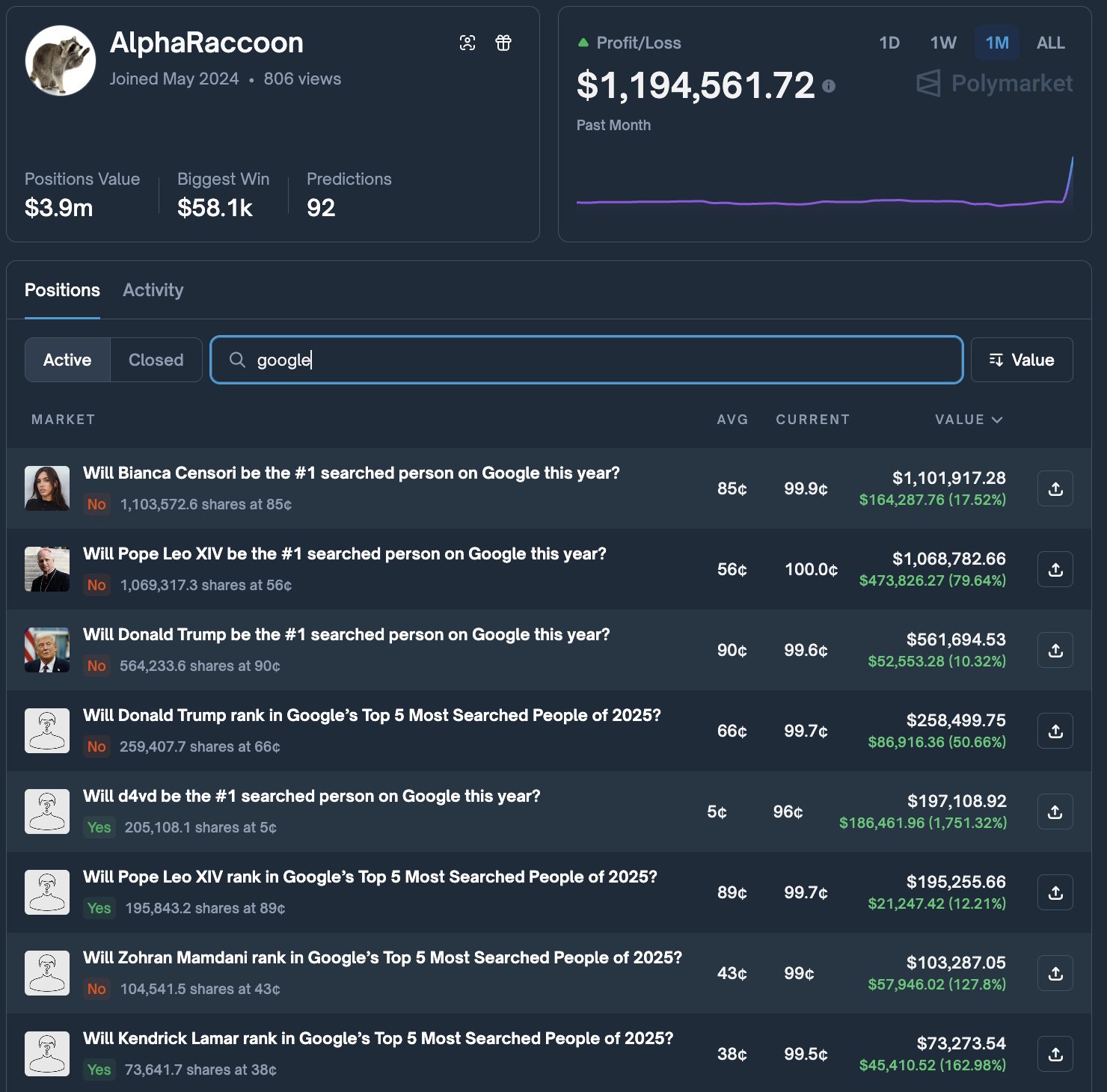

Other examples have also surfaced. Pseudonymous trader AlphaRaccoo netted over $1 million in bets relating to Google search result rankings. He also reportedly made $150,000 by predicting the exact day Google would launch a new version of its Gemini AI model.

Jeong Haeju, a senior software engineer at Meta, said, “He’s a Google insider milking Polymarket for quick money. It’s one of the wildest things I’ve seen on the platform.”

Allegations of manipulation aren’t limited to insider trading. A November report from researchers at the Columbia Business School found that wash trading — i.e., “buying and selling securities without taking a net position, for the purpose of artificially inflating recorded volume” — accounted for 60% of volume on Polymarket in December 2024.

Related: Polymarket rife with ‘artificial trading,’ Columbia University researchers find

This fell substantially but rose to nearly 20% of total volume by October 2025 and has comprised an average of 25% of all trading on Polymarket.

Wash trading “doesn’t add liquidity or information to the market,” said Yash Kanoria, a professor at Columbia University’s business school. This is especially important, given claims that prediction markets provide more accurate and dynamic analyses of a situation.

Jason Wingard, a distinguished visiting professor at Harvard University and executive chairman of the Education Board, wrote that prediction markets create a “‘truth signal’ that moves faster than polls, pundits, or official reports. When thousands of people are willing to lose money on what they think will happen, the result is a dynamic forecast of political outcomes, corporate decisions, economic trends, and cultural shifts.”

Regulation battles as prediction markets ponder new assets

Prediction platforms have won important regulatory approvals this year. In November, Polymarket secured regulatory approval from the US Commodity Futures Trading Commission (CFTC) to operate an intermediated trading platform.

Polymarket founder and CEO Shayne Coplan said, “This approval allows us to operate in a way that reflects the maturity and transparency that the US regulatory framework demands.”

Kalshi is also regulated by the CFTC, meaning that, on paper, it should be allowed to operate in all 50 states.

However, state regulators have taken issue with these platforms. Kalshi is currently facing legal battles with gaming regulators in Nevada, New Jersey, New York, Massachusetts, Maryland and Ohio over whether its platform constitutes a gambling enterprise.

Others see the potential for risks to the financial and credit systems. Bank of America analysts wrote, “Easy access and gamified interfaces encourage frequent and impulsive wagers, which can lead to overextension of credit and rising loan defaults.”

“For investors this convergence of entertainment and speculative finance signals heightened behavioral risk that could pressure credit quality, increase delinquencies, and impact earnings for issuers and subprime lenders.”

They said these risks could pressure credit quality and that online betting markets “introduce a new risk for lenders, one that they have not had to deal with historically and underwriting models may need to be adapted.”

The Connecticut Department of Consumer Protection has served cease-and-desist orders to Robinhood, Kalshi and Crypto.com. It stated that, in addition to lacking proper gambling licenses, the platforms pose “a serious risk to consumers who may not realize that wagers placed on these illegal platforms offer no protections for their money or information.”

Mansour’s plan to turn “any difference in opinion” into a tradable asset may sound novel, but betting platforms will first have to face regulatory scrutiny and a host of ethical issues.

Magazine: 6 reasons Jack Dorsey is definitely Satoshi... and 5 reasons he’s not