Author: Claude, Shenchao TechFlow

Shenchao Insight: Long-term bonds in developed countries are collectively faltering. The market is no longer repricing the fiscal surprise of a single country, but rather the reality of high debt, high deficits, and even higher interest rates coexisting in the long term. As debt growth persistently outpaces economic growth, energy shocks rekindle inflation, and central banks' room for rate cuts is compressed, the "low-interest rollover model" that has supported developed countries' financing for over a decade is developing cracks.

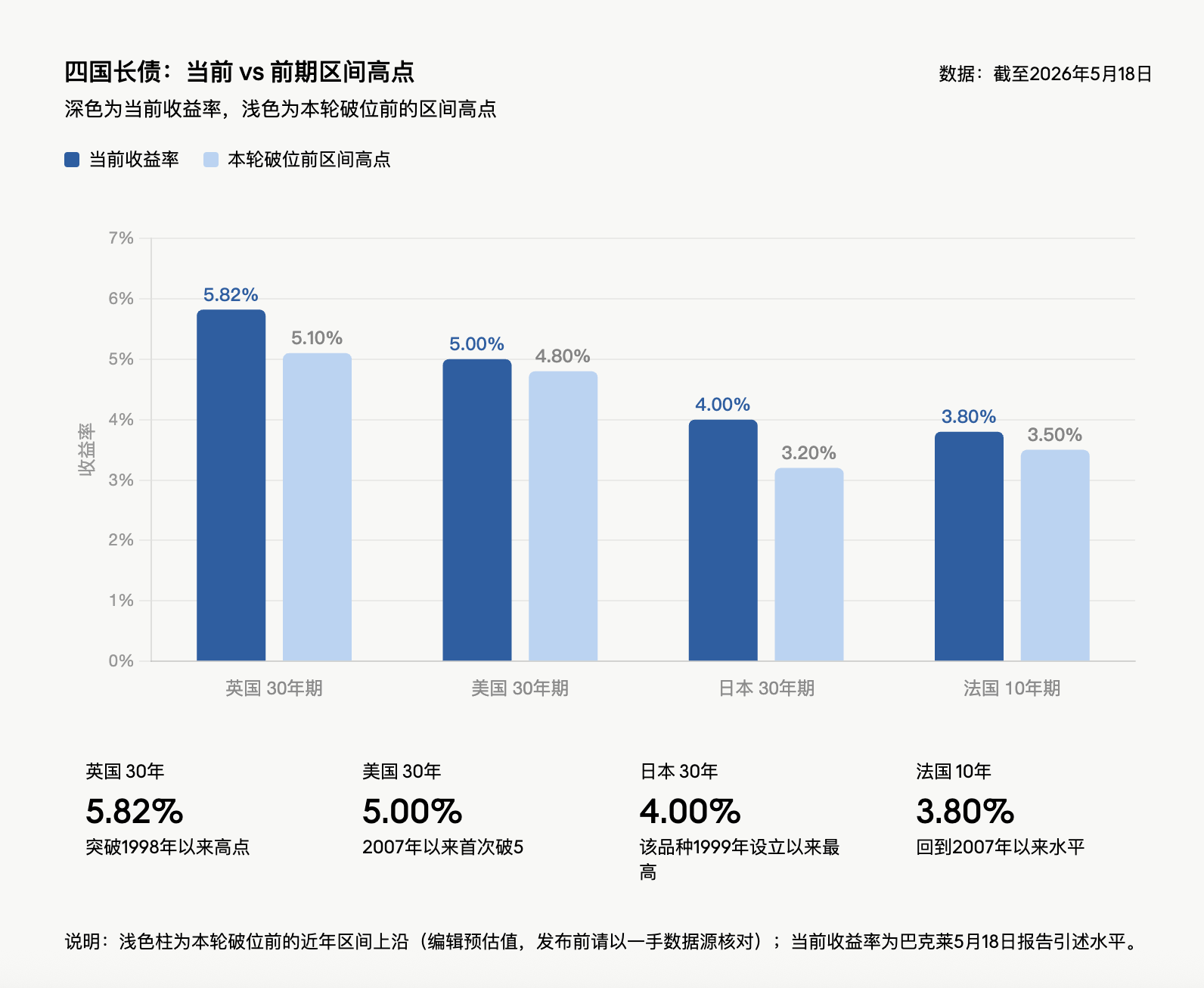

Over the past week, the yield on the UK 30-year government bond rose to 5.82%, the highest since 1998; Japan's 30-year government bond yield hit 4%, a record high since its inception in 1999; the US 30-year Treasury yield surpassed 5% for the first time since 2007; France's 10-year bond yield climbed above 3.8%, also returning to levels last seen in 2007. This sell-off has already weighed on global stock markets, prompting G7 finance ministers to specifically discuss this bond rout at their meeting this week.

According to a report dated May 18 by Ajay Rajadhyaksha, head of Fixed Income, FX, and Commodities Research at Barclays, "Long bonds didn't just sell off last week, they broke out of ranges everywhere." The core judgment is that with debt growing faster than the economy, inflation paths worsening, and no political will for fiscal reform, there is insufficient reason to extend duration even as long bonds have already sold off.

Priya Misra, Portfolio Manager at J.P. Morgan Asset Management, issued a similar warning: "Rates are rising in unison across the long end of the globe, and they tend to reinforce each other, and expectations of Fed rate hikes are now entering the market narrative."

Multi-Country Bond Markets Break Down Simultaneously, Collective "Fiscal Ponzi Scheme" Comes to Light

A decline in a single country's bond market can often be attributed to local inflation, fiscal policies, politics, or central bank communication. However, the near-simultaneous breakdowns in the UK, Japan, the US, and France indicate the market is now trading more than just local risks.

The commonality is clear: major developed economies generally have debt-to-GDP ratios above 100%, and fiscal deficits are not covered by nominal growth. The US deficit is approximately $2 trillion, about 6.5% of GDP, with nominal growth around 4.5% to 5%; France's nominal GDP grew 2.2% year-on-year for the quarter ending March 2026, with a deficit around 5%; the UK's deficit exceeds 4%.

This is the core contradiction pointed to by the "fiscal Ponzi scheme": governments continuously rely on new debt and rollover financing to sustain spending, but the pace of debt expansion exceeds economic growth, while interest costs are becoming more expensive again. As long as this combination persists, long-term bonds require higher yields to attract buyers.

New spending is adding further pressure. NATO agreed in The Hague last year to raise its defense spending target to 5% of GDP by 2035; European defense spending already grew by double-digit percentages last year and may continue for a decade; the US government is requesting a $1.5 trillion defense budget for the next fiscal year. These expenditures lack corresponding offsetting cuts.

Strait of Hormuz Blockade, Oil Price Shock Reignites Inflation

Debt and deficits were already fragile; an energy price shock is further tightening the policy space. The blockade of the Strait of Hormuz is the direct trigger for this bond market turmoil. The disruption of the world's most crucial oil shipping chokepoint has continuously pushed oil prices higher, reigniting inflation expectations.

Barclays' base case assumes Brent crude will average $100 in 2026, a 50% increase from the 2025 average. This would directly worsen the inflation outlook, compress central banks' room for rate cuts, and could even force them to hike rates. Higher rates mean existing debt interest payments will continue to rise, which in turn makes reducing deficits even more difficult. This resembles a fiscal ratchet mechanism—with each forward turn, the government's maneuvering room shrinks, and bond investors demand greater compensation.

J.P. Morgan Managing Director Priya Misra stated bluntly: "Unless the strait reopens, the rate range has shifted higher overall."

Looking at short-term data, the US 2-year yield briefly rose to 4.09%, the highest since February 2025; the 10-year yield stood at 4.58%, near a one-year high; US Treasuries overall have recorded negative returns year-to-date, whereas gains were nearly 2% as of late February.

Inflation Narrative Dominates the Market, Term Premium Being Repriced

The judgment from Karen Manna, Fixed Income Strategist and Portfolio Manager at Federated Hermes, is: "We are seeing a world that is truly dealing with a new inflation wave."

Kevin Flanagan, Head of Investment Strategy at WisdomTree, anticipates the next Consumer Price Index report may show annual inflation reaching 4%, the highest level since 2023. He directly points out the market logic: "The inflation narrative is dominating the market. The bond market is demanding a higher premium to hold newly issued Treasuries."

Last week's Treasury auctions confirmed this pricing: The 30-year auction rate hit 5%, the first since 2007, but demand was tepid; investor demand for the 3-year and 10-year auctions was also lukewarm. Even the rise in long-term bond yields to year-to-date highs is not, in itself, a sufficient reason to add duration.

Fed Path Completely Reverses, Bets Shift from Two Cuts to a March Hike

The inflation storm is reshaping expectations for the Federal Reserve's policy path. The environment facing incoming Fed Chairman Kevin Warsh is far from the "easing channel" envisioned by the market at the start of the year.

Traders now see a March hike next year as highly probable, with the odds of a hike by December around three-quarters; back at the end of February, the market was expecting two rate cuts in 2026. US Treasury yields are now about 50 basis points or more higher than their late-February levels.

Official commentary has further cemented hawkish pricing. Chicago Fed President Austan Goolsbee said last week that broad price pressures might even signal an overheating economy; Fed Governor Michael Barr called inflation the "overwhelming" risk facing the economy. The Fed's April meeting minutes will be released this Wednesday, and the market will closely watch how much support dissenting members garnered among officials.

The latest J.P. Morgan US Treasury Client Survey shows net short positions on Treasuries have risen to their highest level in 13 weeks, indicating a clear increase in market bets for further bond market declines.

Japan's Low-Rate System Being Repriced

Japan's 30-year government bond yield touching 4% may not be extreme in the US or UK, but it holds different significance for the Japanese market. For the past 20 years, Japan's long-term interest rates have hovered near zero, and the balance sheet structures of pension funds, insurance companies, and regional banks were built around this environment.

The Bank of Japan's policy rate is currently 0.75%. At the April policy meeting, three out of nine board members opposed the current stance; market pricing shows a 77% probability of a June rate hike. Even if the BOJ raises rates to 1%, real rates would remain significantly negative.

The rise in Japan's long-term yields can be interpreted as monetary policy normalization: the end of deflation, real wage growth, and the economy returning to a more normal state. However, the issue is that normalization may not be gentle for an economy with debt exceeding twice its GDP. A 4% yield on a 30-year Japanese bond is not just a change in a yield figure; it signifies the repricing of the entire low-interest-rate financial system.

UK, France: Political Structures Make Deficit Reduction Almost Impossible

The UK Labour government has a working majority of over 150 seats in the 650-seat parliament, theoretically possessing the capacity for fiscal adjustment. However, last summer, proposed savings of just £1.4 billion related to winter fuel subsidies sparked a backlash within the Labour parliamentary party.

Political pressure is mounting. Ninety-seven Labour MPs have demanded the Prime Minister resign or provide a departure timeline; main challenger Andy Burnham once argued fiscal policy should not submit to the bond market, later clarifying he would not completely ignore investors. The UK has had four prime ministers and five chancellors of the exchequer in the past four years. Bond market pricing indicates over 60 basis points of further rate hike potential for the Bank of England by year-end, although Governor Bailey may prefer to wait and see.

France's problem is less eye-catching than UK gilts, but its fiscal structure is equally tricky. France has had five prime ministers in less than three years. The current government has survived two no-confidence votes to push through a budget targeting a 5% of GDP deficit. The 2023 reform raising the retirement age to 64 is under attack, even though 64 is still below most Western economies. France's deficit is already significantly higher than its nominal GDP growth, voters will harshly punish austerity attempts, and constitutional arrangements make it easier for parliament to block spending cuts. Everyone knows the deficit must fall, but no one is willing to bear the political cost of reducing it.

US Buyer Structure Has Changed: Foreign Central Banks Turn to Gold, Private Investors Demand Higher Prices

The US 30-year Treasury yield surpassing 5% is the first time since 2007. The direct causes are rising inflation, fiscal expansion, and high deficits, but this is not new. The deeper change lies in the shifting marginal buyers.

The US federal deficit is approximately $2 trillion. The Congressional Budget Office projects that federal debt held by the public will rise from its current level of over 100% of GDP to 120% by 2036. However, this forecast may still be optimistic. A key variable is tariff revenue: The US effective tariff rate has fallen from a peak of 12% to between 7% and 8%, below the CBO's assumption of 15%. Even if it eventually rises to 10%, tariff revenue over the next decade would only be about 60% of the roughly $3 trillion deficit reduction assumed in its projections. Assumptions for defense spending and interest costs may also be too low.

The dollar's reserve currency status remains a structural advantage for the US, allowing it to finance at rates that peer debtors struggle to obtain. However, this does not mean a 6.5% deficit ratio is sustainable. Foreign central banks were once stable buyers of duration assets, but since the West froze Russia's foreign reserves, central bank allocations have shifted towards gold. Last year, gold's share in central bank reserves surpassed that of US Treasuries. Japan, the largest holder of US Treasuries, finds its domestic market rates more attractive. The Fed is still in quantitative tightening mode. Those stepping in to buy long-term bonds are price-sensitive private investors demanding higher term premiums.

The Fed is Not a "Fuse" for Long Bonds

Debt management offices have relatively reduced long-term bond issuance in recent years and may continue adjusting issuance structures, but this can only ease supply pressure, not change the fiscal and inflation direction.

Some in the market discuss whether the Fed might be forced to restart large-scale asset purchases to prevent long-end rates from rising further. However, Warsh's previous statement regarding the Fed's balance sheet was, "A bloated balance sheet could be meaningfully reduced," which is not language suggesting preparation for a US version of Yield Curve Control.

Faced with the ongoing sell-off, some investors choose to stay on the sidelines. WisdomTree analyst Kevin Flanagan said he currently maintains holdings in floating rate notes and keeps interest rate exposure low, "preferring to buy later rather than too early." He views the 4.5% level on the 10-year yield as "more of a psychological barrier," and if Middle East tensions escalate again and push oil prices higher, yields could retest last year's high of 4.62%. Hank Smith, Head of Investment Strategy at Haverford Trust, holds a more cautious view, stating that it remains an unresolved question whether the rise in consumer and producer prices is temporary "or will persist into 2027."

The forces driving the sell-off—fiscal deterioration, increased defense spending, sticky inflation, and constrained central banks—are not disappearing in a week or two. Unless economic data weakens significantly or credible changes emerge in fiscal paths, developed market long bonds are still trading on the same issue: the low-interest financing model of the high-debt era is being repriced by the market.