Original Author: Joe Zhou, Foresight News

Original Title: Save 18% on Hotel Bookings with USDT, Trip.com's Overseas Version Strongly Promotes Stablecoin Payments

Trip.com, the overseas version of Ctrip, is quietly entering the stablecoin payment track.

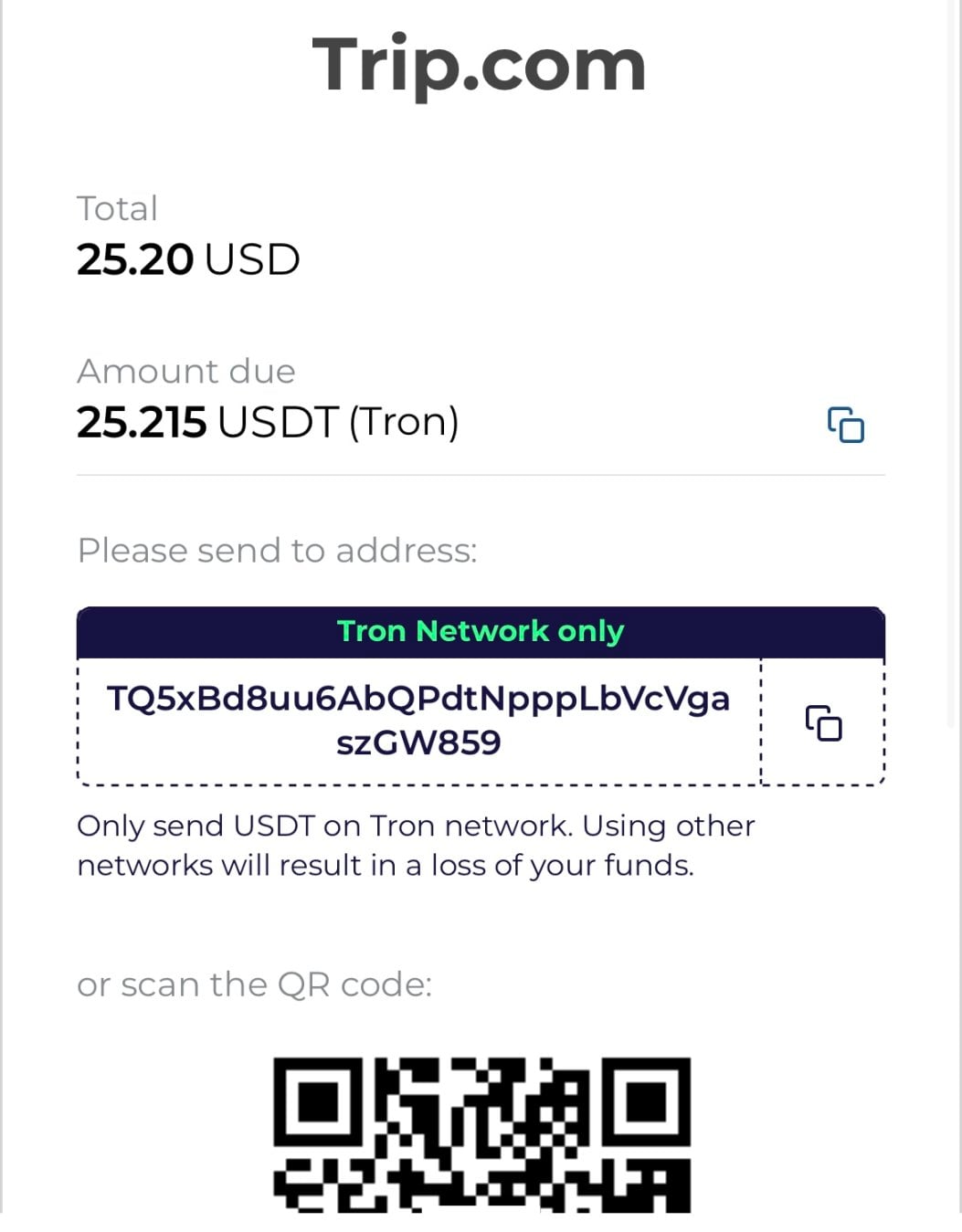

On December 25, 2025, Foresight News learned that Trip.com, the overseas version of Ctrip, has launched a stablecoin payment function for global users, currently supporting two USD stablecoins: USDT and USDC. Two sources close to Trip confirmed this information to Foresight News.

After downloading and logging into Trip.com in Vietnam, the author successfully completed a hotel reservation in Nha Trang, Vietnam, using USDT payment in less than 10 minutes.

More notably, after checking the prices of several local hotels, it was found that the price of some hotels on the Trip.com App when paying with USDT was even lower than using the Ctrip official website or traditional payment methods.

Trip.com Overseas Version Already Supports USDT/USDC

On December 24, 2025, the author booked a hotel in Nha Trang, Vietnam, using USDT on the Trip.com overseas version APP, and on December 25, purchased a plane ticket from Nha Trang to Ho Chi Minh City with USDT, both showing successful payment. The author has now successfully checked into the hotel.

The author found that the flight ticket purchased with USDT on Trip.com saved approximately 18% of the cost compared to the ticket purchased on Ctrip. The hotel booked with USDT saved 2.35% of the cost.

Trip has enabled USDT and USDC payments

Currently, Trip.com's crypto payments support multiple public chains including Ethereum, Tron, Polygon, Solana, Arbitrum One, and TON.

During the actual payment process, the author noticed the presence of another payment company, Triple-A. This company provides crypto payment-related services to Trip.com. Public information shows that Triple-A is a licensed crypto payment institution headquartered in Singapore, mainly providing payment gateway and settlement services for cryptocurrencies and stablecoins.

Furthermore, the author learned that Triple-A is also cooperating with Singapore's internet giant Grab as a technical partner for the crypto payment channel, enabling GrabPay users to directly use crypto assets to top up their wallet balance within the Grab app.

Additionally, the author noticed a detail:

When booking a hotel on Trip.com using USDT, there is no need to fill in detailed personal information; only a name and email are required to complete the order. This means that when using USDT for payment in hotel scenarios, the platform can hardly obtain the user's complete privacy information. Of course, if purchasing a flight ticket, information such as nationality, passport number, and phone number are still required—this is a compliance requirement of the aviation industry itself.

Privacy and data security have become major social issues.

Just this month, the Ctrip Group encountered a relatively significant "public trust incident." In December, Ctrip Group and the Cambodia National Tourism Administration signed a marketing cooperation agreement in Shanghai. After the news was announced, it sparked concerns among some users about local security, telecom fraud risks, and personal information security. A large number of screenshots of uninstalling the Ctrip App appeared on social media.

In many overseas regions, users are far more sensitive to privacy and information security than in the domestic market. This may also be an important practical background for Trip.com's promotion of stablecoin payments.

For travelers around the world without international credit cards, stablecoin payment is a new path. According to public information, the number of people globally who own credit cards is approximately 125 million to 130 million, and the number of people with international credit cards is even lower, which also means that over 80% of the global population cannot smoothly use the international credit card system.

Credit cards are not merely "payment tools" but an entry point to the credit system; however, most people globally are not within this system. In many countries and regions, such as Southeast Asia, Latin America, Africa, and India, many people cannot be incorporated into the credit system. This also prevents them from having credit cards.

Stablecoin payments are providing these people with a global payment path that bypasses the credit system.

Of course, the practical problems of stablecoins still exist: transaction fees remain relatively high and unstable.

During the actual payment process, the author found significant differences in fees between different wallets. When paying to Trip.com's USDT收款码 (receiving QR code) via Binance, a fee of 1 USDT was required, with a minimum transfer threshold of 10 USDT; whereas when using Bitget Wallet, the first transaction showed a fee of 0, the second showed a fee of 2.39 USDT, and no minimum transfer amount was set. The differences may be related to the public chain used (Tron) and its fee mechanism.

Why Are Giants Entering the Stablecoin Space One After Another?

Ctrip Group is not the first company to enter the stablecoin track.

Previously, several global internet and payment giants have clearly布局 (laid out plans for) stablecoins, including Ant Group, JD.com, Paypal, Stripe, Meta (Facebook), Grab, and TADA.

Several banking giants have also publicly stated their entry into the stablecoin field, for example, Bank of America and Morgan Stanley.

Some实体制造业企业 (physical manufacturing companies) are also接入 (integrating) stablecoin payments. Public reports show that some dealers of BYD (Build Your Dreams) in Bolivia already support USDT payments; manufacturing companies like Toyota and Yamaha also accept stablecoin settlements in overseas markets. Tether CEO Paolo Ardoino has publicly confirmed this.

Advertisement for cooperation between BYD dealers and USDT

Internet giants,实体制造业巨头 (physical manufacturing giants), banking giants are all布局 (laying out plans for) stablecoins... Their use cases for stablecoins vary.

An obvious trend is that payment giants like PayPal and Ant Group are no longer satisfied with仅仅作为 (merely being) the payment entry for stablecoins but hope to directly become the issuers of stablecoins. PayPal has already launched PYUSD; Ant Group is also promoting the application for a Hong Kong dollar stablecoin license. The boundary between payment institutions and currency issuance is being reshaped.

For实体制造业企业 (physical manufacturing enterprises) like BYD and Toyota, there is no ideological judgment about stablecoins or crypto payments, only one practical question: which method are users more willing to pay with.

Fiat Currency Continues to Depreciate, Stablecoins Become the "Practical Solution"

In Bolivia, the official fiat currency, the Boliviano (BOB), depreciated against the US dollar by 65%–137% from the end of 2024 to mid-2025. It can be said that Bolivia's fiat currency depreciates every day.

In this environment, any company expanding overseas cannot long bear the exchange losses brought by settlement in the local currency. USDT has gradually become the de facto payment tool locally.

And Bolivia is not an isolated case but a phenomenon simultaneously上演 (playing out) in multiple countries around the world.

The author visited Iran, Turkey, Egypt, and other countries this year and found that the cumulative depreciation of these economies' national currencies against the US dollar over the past three years generally exceeded 80%; stretched over a five-year周期 (cycle), the currencies of Iran, Turkey, and Egypt have all depreciated by more than 200% against the US dollar.

Currency depreciation is evolving from a "local risk" in a few countries to a broader, more structural global phenomenon.

At the black market in Tehran, Iran's capital, the author is witnessing a currency transaction

More残酷的是 (cruelly), in the aforementioned countries (the countries mentioned above), the speed of local currency depreciation has long far exceeded the income growth rate of ordinary people. In real transactions, monetary disorder is directly changing people's payment methods.

This is precisely why consumer internet platforms like Trip.com Overseas Version and Grab; payment giants like PayPal and Ant Group; and physical manufacturing companies like BYD and Toyota have begun to尝试引入 (try to introduce) USDT and other stablecoins in different markets.

The world is partially collapsing, with some regions率先失衡 (becoming unbalanced first).

When the existing financial system can no longer perform the functions of stability, settlement, and trust, a new economic system is pushed to the forefront by reality.

The new economic system is not designed but is "forced" out by reality where the old system fails. The spread of stablecoins is not because they are ideal enough, but because in some places, they are already the least bad choice available.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush