Written by: Brad Stone, Bloomberg

Compiled by: Saoirse, Foresight News

Two months before the stock market crash that triggered the Great Depression's "Black Monday," an economist from Massachusetts named Roger Babson was deeply concerned about the frenzy of retail investors borrowing money to speculate in stocks. In a speech, he declared, "Sooner or later, a crash is coming, and it may be terrific." The market immediately fell by 3%, a drop that became known as the "Babson Break." But as Andrew Ross Sorkin writes in his fascinating new book, "1929: The Inside Story of Wall Street's Worst Crash and How It Destroyed a Nation," in the following weeks, "the market shook off Babson's ominous prediction," partly due to optimism about new mass consumer goods like radios and cars. "The 'imaginative' investors once again took the upper hand."

Today, there are many such "doomsayers" like Babson warning of risks in the artificial intelligence (AI) sector, particularly the valuations of public and private tech companies and their blind pursuit of the elusive goal of Artificial General Intelligence (AGI)—systems that can perform nearly all human tasks, even surpassing human capabilities. Data analytics firm Omdia's data shows that by 2030, tech companies will spend nearly $1.6 trillion annually on data centers. The hype around AI is immense, but its prospects as a profit-generating tool remain entirely hypothetical, leaving many sober investors perplexed. Yet, much like a century ago, the fear of missing out on the next big opportunity drives many companies to ignore these "apocalyptic prophecies." Adwait Arun, an analyst for climate finance and energy infrastructure at the Center for Public Enterprise, stated, "These companies are like they're playing a game of 'Mad Libs,' thinking these bold technologies will solve all existing problems." He recently released a report in the style of Babson's views, titled "It's a Bubble or It's Nothing," questioning the financing schemes behind data center projects and noting, "We are undoubtedly still in a phase of irrational exuberance."

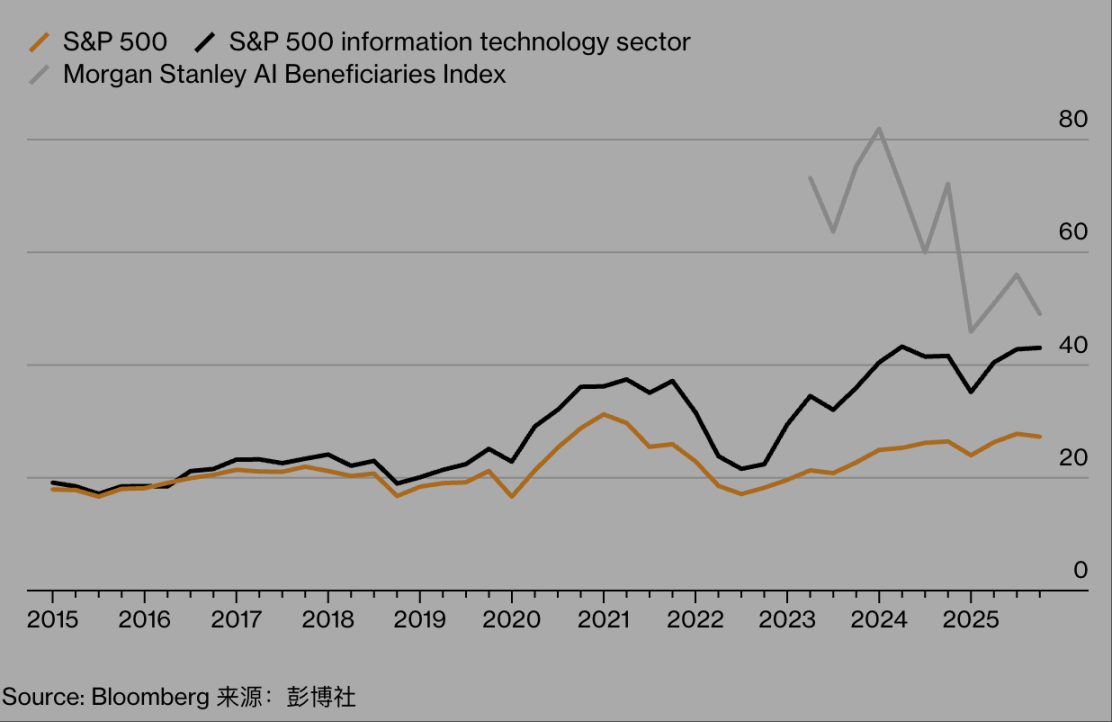

Tech stocks have been soaring:

Source: Bloomberg

(This chart uses three index lines—S&P 500, S&P 500 Information Technology Sector, and Morgan Stanley AI Beneficiaries Index—to show the process from 2015 to 2025 in U.S. stocks where AI-related concept stocks first surged significantly due to speculation, then fell back as the bubble receded, diverging from the trends of the broader market and traditional tech sectors, reflecting the speculative frenzy and retreat risks in the AI field.)

Journalists should generally avoid arguing whether a particular resource or technology is overvalued. I don't have a strong stance on whether we are in an "AI bubble," but I suspect the question itself might be too narrow. If we define a "speculative bubble" as "an unsustainable rise in the value of an asset detached from its determinable fundamentals," then looking around, bubbles seem to be almost everywhere, and they appear to be inflating and contracting simultaneously.

World Economic Forum CEO Børge Brende pointed out that there may be bubbles in gold and government bonds. He recently stated that since World War II, the overall debt situation of countries has never been so severe; as of December 12, gold prices had surged nearly 64% in a year. Many financial practitioners believe there is also a bubble in the private credit sector. This market, worth $3 trillion, involves large investment institutions providing loans (many for building AI data centers) and operates outside the strictly regulated commercial banking system. Jeffrey Gundlach, founder and CEO of asset management firm DoubleLine Capital, recently called this opaque, unregulated, chaotic lending phenomenon "junk loans" on Bloomberg's "Odd Lots" podcast; JPMorgan Chase CEO Jamie Dimon referred to it as a "fuse for a financial crisis."

The most absurd phenomena occur in areas where "intrinsic value is difficult to judge." For example, from the beginning of the year to October 6, the total market capitalization of BTC increased by $636 billion, but as of December 12, not only were all gains erased, but there was an even larger decline. According to data from cryptocurrency media company Blockworks, the trading volume of "meme coins"—virtual currencies commemorating internet hotspots—peaked at $170 billion in January but plummeted to $19 billion by September. Leading the decline were TRUMP and MELANIA—coins launched by the U.S. first family two days before the presidential inauguration, which have fallen 88% and 99% respectively since January 19.

Many investors evaluate these cryptocurrencies not based on their potential to create intrinsic value for shareholders and society (as one would when assessing a traditional company's stock that reports profits) but simply for the opportunity to "make quick, big money." Their attitude toward cryptocurrencies is akin to approaching a craps table during a trip to Las Vegas—full of speculation.

There may be demographic reasons behind investors (especially those attracted to cryptocurrencies, sports betting, and online prediction markets) trying to "manipulate" financial markets like a casino. A recent survey by Harris Poll showed that 60% of Americans today desire to accumulate vast wealth; among Gen Z and millennial respondents, 70% said they want to become billionaires, compared to only 51% among Gen X and baby boomers. A study last year by financial firm Empower found that Gen Z believes "financial success" requires an annual salary of nearly $600,000 and a net worth of $10 million.

Thanks to TikTok videos, group chats, Reddit, and the "instant and unavoidable" nature of the internet, people around the world can simultaneously learn about money-making opportunities. In principle, this seems fine, but in practice, it triggers imitation frenzies, fierce competition, and "groupthink"—a phenomenon that makes the new Apple TV series "Pluribus" particularly timely. The traditional economy, with its complex and diverse dimensions, has been replaced by the "attention economy": what is collectively obsessed with at any given moment globally.

In the business world, this "collective obsession" is focused on AI; in pop culture, following the "Pedro Pascal fever," there is "Sydney Sweeney fever," and also "6-7 fever" (if you don't have teenagers at home, you might want to search Google). Over the past year, thanks to celebrities like BLACKPINK member Lisa, the "cute but practically worthless animal-shaped plush toys" launched by Chinese toy manufacturer Pop Mart International Group have taken the world by storm—let's call it the "Labubble" (referring to Labubu fever).

There is also a clear "protein bubble" in the food sector: from popcorn makers to breakfast cereal producers, everyone is promoting their products' "protein content" to attract health-conscious consumers and GLP-1 (a blood sugar-lowering drug often used for weight loss) users. In the media sector, there might be bubbles in Substack newsletters, podcasts hosted by celebrities (like Amy Poehler's "Say More" and Meghan Markle's "Confessions of a Female Founder"), and almost weekly "authorized celebrity documentary biopics" (Netflix's latest include: "Becoming Eddie" about Eddie Murphy and a biopic about Victoria Beckham). W. David Marx, author of "Status and Culture: How Our Desire for Social Rank Creates Taste, Identity, Art, Fashion, and Constant Change," said, "Today, everyone's 'reference group' is global, far beyond what is visible around them and beyond their actual class and status. In these markets, 'globally synchronized movements' that were absolutely impossible in the past may occur."

Of course, the risks in the AI field are far higher than those related to "Labubu fever" products. No company wants to fall behind, so all industry giants are pushing forward, building computing infrastructure through "complex financing arrangements." In some cases, this involves "special purpose vehicles" (remember those from the 2008 financial crisis?)—entities that take on debt to purchase graphics processing units (i.e., AI chips) from Nvidia, and some observers believe these chips may depreciate faster than expected.

Tech giants have the capacity to withstand any consequences of this "FOMO-driven frenzy": they primarily rely on strong balance sheets to pay for data centers, and even if white-collar workers generally believe "the current version of ChatGPT is sufficient for writing annual self-evaluations," these giants can handle it calmly. But other companies are taking riskier moves. Oracle—a conservative database provider unlikely to be a challenger in the AI boom—is raising $38 billion in debt to build data centers in Texas and Wisconsin.

Other so-called "new cloud vendors" (like CoreWeave, Fluidstack, and other relatively young companies) are building specialized data centers for AI, Bitcoin mining, and other uses, and these companies are also borrowing heavily. At this point, the "cumulative impact" of the AI bubble begins to appear increasingly severe. Gil Luria, managing director at investment firm D.A. Davidson & Co., echoed Roger Babson from a century ago, stating, "When some institutions borrow money to build billions of dollars worth of data centers without even having real customers, I start to get worried. Lending for speculative investments has never been wise."

Carlota Perez, a British-Venezuelan researcher who has studied economic boom and bust cycles for decades, is also concerned. She points out that technological innovation is being transformed into high-risk speculation in an "over-leveraged, fragile, casino-like economy where bubbles burst once doubts spread." She wrote in an email, "If the AI and cryptocurrency sectors crash, it could trigger a global crisis of unimaginable scale. Historically, truly productive golden ages only arrive when the financial sector pays for its actions (rather than being bailed out continuously) and society restrains it through reasonable regulation." Until then, hold tight to your Labubu plush toy.