Today, the Crypto Fear & Greed Index has plummeted to a shocking value of 10, officially marking market sentiment as entering the "Extreme Fear" zone.

This is the lowest level since the global market crash triggered by the COVID-19 pandemic in March 2020, even surpassing the panic levels of the Terra/Luna collapse in 2022.

In this morning's sharp decline, Bitcoin briefly touched a low of $85,100, while Ethereum also fell to a low of $2,880.

Market participant sentiment has nearly frozen solid; this panic is not only reflected in prices but is deeply etched into every byte of on-chain data.

The Harsh Truth of On-Chain Fees: The "Survival Stress Test" for Blockchains

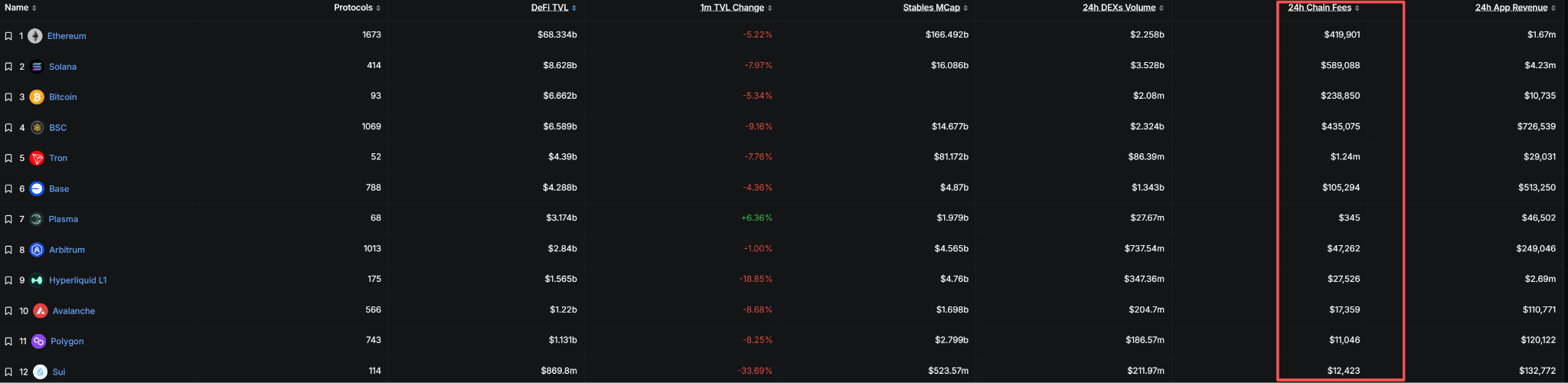

The ranking of fees generated across all blockchains in the past 24 hours presents an extremely polarized picture:

Tron leads with $1.24 million, SOL follows closely with $589,088, the BNB Chain ranks third with $435,075, while Ethereum trails in fourth place with only $418,425.

This data far exceeds general expectations, with several so-called star blockchains like SUI and Plasma generating less than 1/10th of Tron's fees.

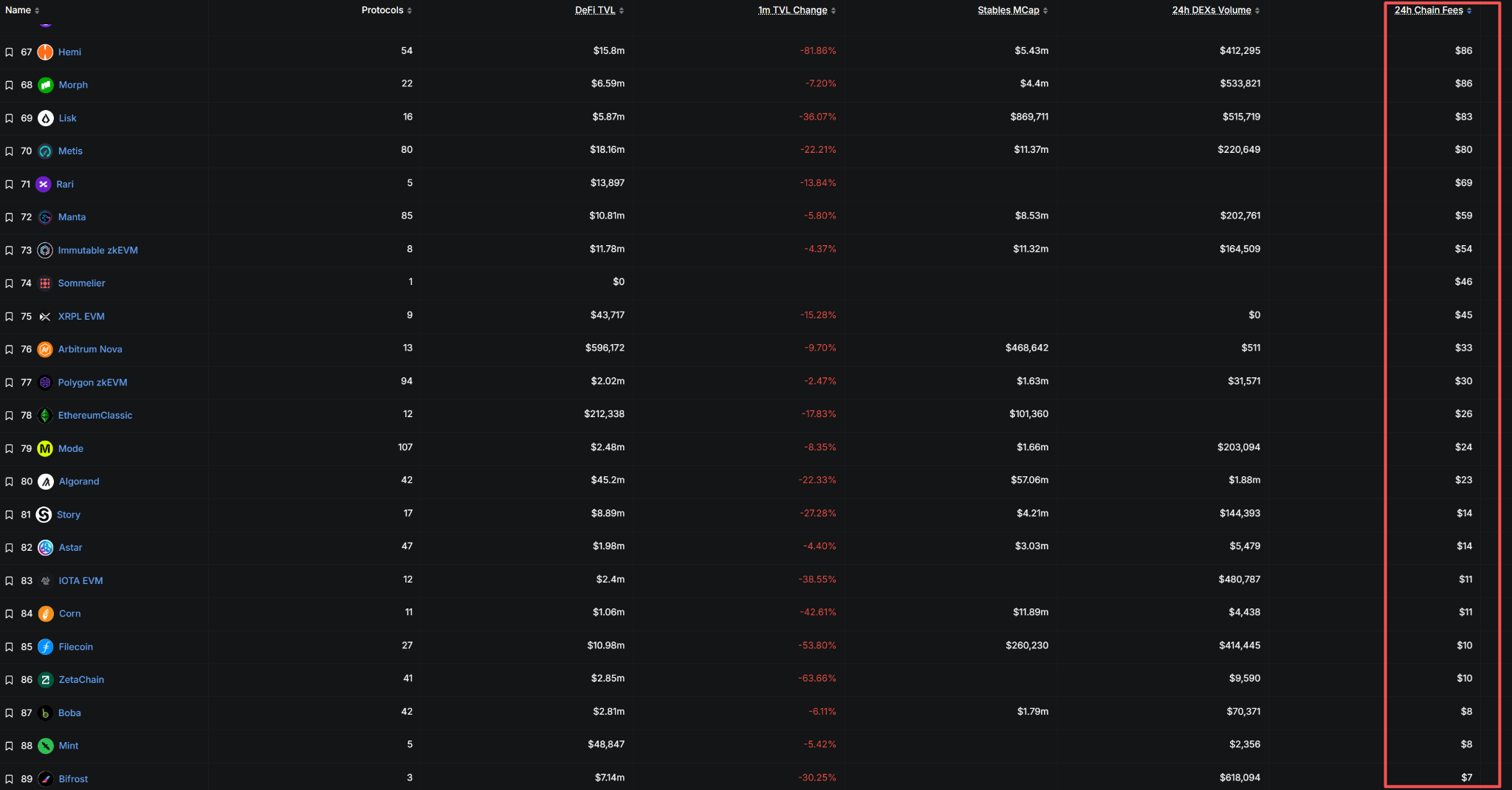

However, the truly alarming situation is the survival state of the long-tail blockchains.

Blockchains that were once popular, such as Celestia, Hemi, Morph, Manta, Immutable zkEVM, EthereumClassic, Algorand, Story, and Filecoin, generated less than $50 in fees in the past 24 hours—less than a roadside stall.

This data undoubtedly indicates that the actual usage of these blockchains is nearing zero.

Fees are the direct "tax" of a blockchain's economy and a core metric for measuring network value.

When a blockchain's daily fees are less than $50, its network security, degree of decentralization, and long-term sustainability are all called into serious question.

The Macro Backdrop of Market Panic: Liquidity Crisis and Narrative Breakdown

This market panic is not due to a single factor but is the result of a combination of tightening global liquidity and the breakdown of internal crypto narratives.

On one hand, global USD liquidity is facing severe challenges. The Fed's maintained hawkish stance, delaying rate cut expectations, has led to a heavy blow to global risk assets.

The Bank of Japan's rate hike has further intensified global liquidity contraction. Historical data shows that BoJ hiking cycles often coincide with global liquidity tightening; the two rounds of hikes in March 2024 and January 2025 both caused Bitcoin to retreat by over 30%.

On the other hand, two core internal narratives of the crypto market are being severely tested.

Bitcoin spot ETFs have turned from an "engine" into a "pump," with net outflows exceeding $2.3 billion since November alone.

More worryingly, long-term holders have been selling Bitcoin on a large scale, a rare occurrence, selling approximately 815,000 BTC just in early November. When the two major narratives of "institutional adoption" and "long-term holding" show cracks simultaneously, market confidence collapses like an avalanche.

On-chain data shows the market just experienced "the largest realized loss day in the past six months," meaning a massive amount of assets were sold below their purchase price, and investors are纷纷 "cutting losses" and exiting.

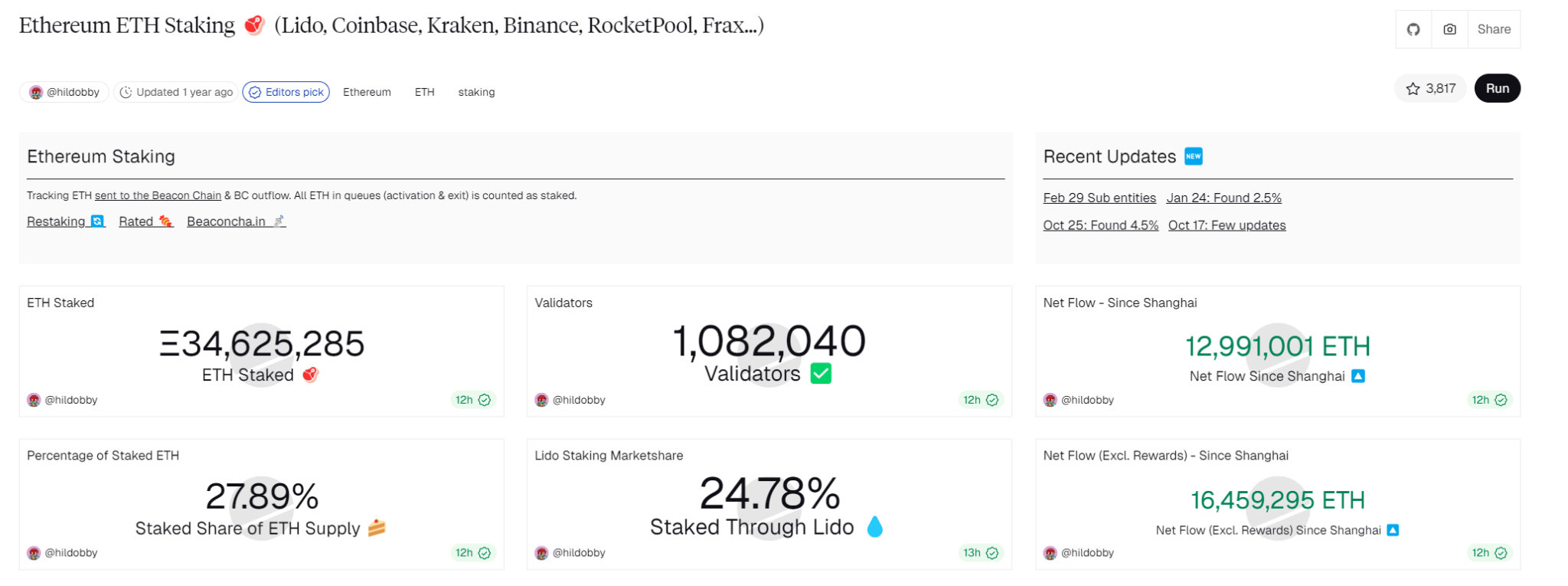

The Economic Paradox of Ethereum Staking: Who is Paying for the Whales' Profits?

Against the bear market backdrop, Ethereum's economic model deserves particular scrutiny.

Ethereum's problem gets to the core: Big players staking Ethereum are taking so much money from the protocol every day; who is paying for that?

In reality, the Ethereum Beacon Chain staking annual yield is approximately 3.5%. These returns primarily come from two parts: block rewards (paid by the protocol issuing new tokens, effectively diluting the value for all token holders) and transaction fees (paid by users engaged in on-chain activity).

During a bull market, high Gas fees can be absorbed by active users through DeFi, NFT, and other applications;

but in a bear market, on-chain activity plummets, and staking rewards rely more on token issuance—this essentially means later participants are "transfusing" early stakers through inflation.

The current total amount staked on the Ethereum Beacon Chain accounts for 27.89% of the circulating supply. These stakers earn stable returns from the protocol daily. However, with fee revenue at only $418,000 (less than a third of Tron's), whether the Ethereum network can sustainably support such massive staking rewards is indeed worth pondering.

More seriously, when the Ethereum price falls, stakers may face a situation where "rewards are insufficient to cover the currency's depreciation," potentially triggering a negative feedback loop of unstaking and selling.

This does share similarities with Ponzi structures in traditional finance: any system reliant on new funds to maintain old returns exposes its fragility during liquidity contractions.

A Philosophical Question: After the Crypto "Red Pill" Takes Effect

"When people say Bitcoin is a Ponzi scheme, it's also the first time they realize the essence of any form of property rights in the real world is a Ponzi." This view touches the essence of the problem.

All value systems are built on consensus, whether fiat currency, gold, or cryptocurrency.

When people say the crypto space is a casino, it might be the first time they truly recognize the nature of the global financial system.

In traditional financial markets, central banks can print money indefinitely, governments can change rules arbitrarily, and insider trading and market manipulation are commonplace. Compared to these traditional financial markets hidden behind opaque rules, the crypto space at least presents the brutality of finance in an extremely transparent, real-time manner to all participants.

In today's market, the Bitcoin Fear & Greed Index is only 11, and on-chain data shows most blockchains are nearly "brain dead." Investors are not disappointed with crypto itself but are unable to accept the real world seen after swallowing the "red pill."

The cryptocurrency market is like a mirror, reflecting the nature of the global financial system: all asset prices are ultimately driven by liquidity, not intrinsic value. When the Fed "turns off the tap," everything from stocks and crypto to gold faces selling pressure.

Historical Perspective: Value Return After Extreme Fear

Looking back at cryptocurrency history, every period of extreme market fear has ultimately proven to be an excellent opportunity for long-term investment.

During the COVID-19 crash in March 2020, the Fear & Greed Index plummeted to 10-15, but Bitcoin subsequently embarked on a bull market that lasted over a year.

In June 2022, following the Terra/Luna collapse and macro-economic tightening, the index remained in "Extreme Fear" territory (8-15) for weeks. Although prices fell across the board, sustained panic actually marked the market bottom. Currently, although market sentiment is extremely pessimistic, on-chain data reveals another picture: behind the panic "surrender," a great "asset transfer" is quietly taking place. Medium-sized whales and panicked retail investors are selling, while large strategic entities and steadfast retail investors are actively accumulating.

Data shows that the largest strategic entities (holding >10,000 BTC) continued to accumulate throughout November, with a net increase of 10,700 BTC. Even Bitcoin's most famous evangelist, Michael Saylor's company, announced buying another $50 million worth of Bitcoin amidst the market panic.

Periods of extreme fear are the perfect time to "be greedy when others are fearful." Historically, choosing to sell when the Fear Index drops to single digits has often been the wrong move.