Original | Odaily Planet Daily (@OdailyChina)

Author | Ethan (@ethanzhang_web3)

December 12, 2025, Washington D.C. - The Office of the Comptroller of the Currency (OCC) announced that it has conditionally approved five digital asset institutions - Ripple, Circle, Paxos, BitGo, and Fidelity Digital Assets - to convert into federally chartered national trust banks.

This decision was not accompanied by dramatic market fluctuations but is widely regarded as a watershed moment by regulators and financial circles. Crypto businesses, long operating on the fringes of the traditional financial system and frequently facing banking service disruptions, have for the first time been formally incorporated into the US federal banking regulatory framework with a "bank" identity.

The change did not come suddenly, but it is thorough. Ripple plans to establish "Ripple National Trust Bank," and Circle will operate "First National Digital Currency Bank." These names themselves clearly convey the signal released by regulators: digital asset-related businesses are no longer just "high-risk exceptions" passively undergoing scrutiny but are allowed to enter the core layer of the federal financial system under clear rules.

This shift stands in stark contrast to the regulatory environment of a few years ago. Especially during the banking turmoil of 2023, the crypto industry was once deeply mired in the so-called "de-banking" dilemma, systematically cut off from the US dollar settlement system. With President Trump signing the GENIUS Act in July 2025, stablecoins and related institutions obtained a clear legal definition at the federal level for the first time, also providing the institutional premise for the OCC's concentrated licensing.

This article will analyze the institutional logic and practical impact behind this approval from four perspectives: "What is a Federal Trust Bank," "Why is this license so important," "The Regulatory Shift in the Trump Era," and "Traditional Finance's Response and Challenges." The core judgment is: The crypto industry is transitioning from being an "external user" dependent on the banking system to becoming part of the financial infrastructure. This not only changes the cost structure of payments and clearing but is also reshaping the definition of a "bank" in the digital economy.

What is a "Federal Trust Bank"?

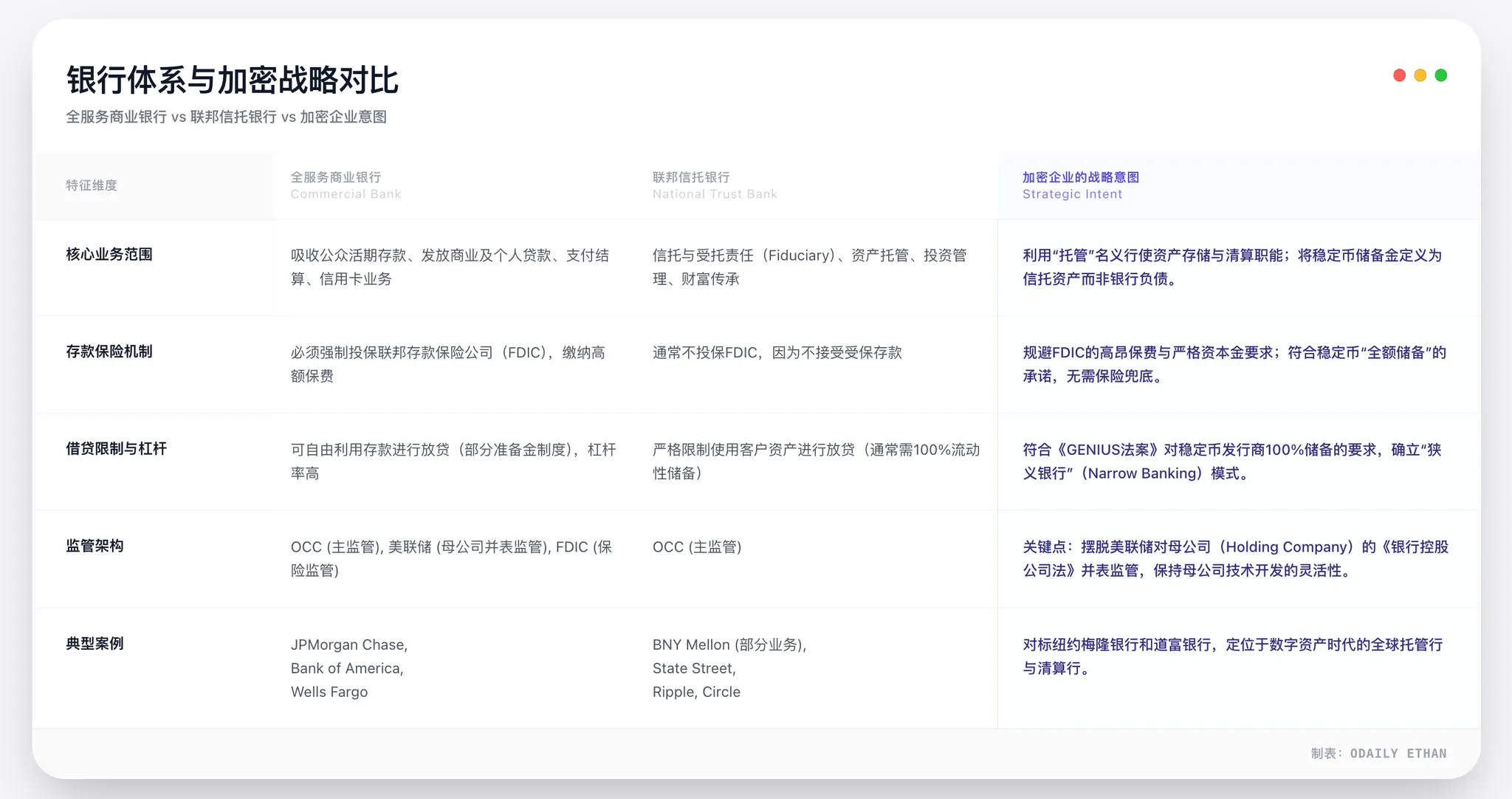

To understand the true weight of this OCC approval, one must first clarify a easily misunderstood point: This is not these five crypto firms obtaining a traditional "commercial bank charter."

The OCC approved "National Trust Bank" status. This is a type of bank charter that has long existed in the US banking system but was primarily used for businesses like estate management and institutional custody. Its core value lies not in "how much business it can do" but in its regulatory level and infrastructure status.

What does Federal Chartering mean?

Under the US dual banking system, financial institutions can choose to be regulated by state governments or the federal government. The two are not simply parallel in terms of compliance intensity but have a clear hierarchy of authority. A federal charter bank license issued by the OCC means the institution is directly regulated by the Treasury system and enjoys "federal preemption," no longer needing to adapt to the regulatory rules of each individual state for compliance and operations.

The legal basis for this can be traced back to the National Bank Act of 1864. Over the following century and a half, this system has been a key institutional tool for forming a unified financial market in the US. This is particularly critical for crypto companies.

Prior to this approval, whether it was Circle, Ripple, or Paxos, to operate compliantly nationwide in the US, they had to apply for Money Transmitter Licenses (MTLs) in all 50 states, facing a "patchwork" system with different regulatory stances, compliance requirements, and enforcement standards. This was not only costly but also severely limited business expansion efficiency.

After converting to a federal trust bank, the regulatory body shifts from various state financial regulators to the unified oversight of the OCC. For the companies, this means a unified compliance path, a nationwide business passport, and a structural elevation of regulatory credibility.

Trust Bank, not a "Mini Commercial Bank"

It is crucial to emphasize that a federal trust bank is not equivalent to a "full-service commercial bank." The five approved institutions are not permitted to accept FDIC-insured public deposits, nor can they make commercial loans. This is also a core reason for criticism from traditional banking organizations (like the Bank Policy Institute), which argue this is an admission with "unequal rights and obligations."

However, from the perspective of the crypto firms' own business structures, this restriction is highly compatible. Taking stablecoin issuers as an example, whether it's USDC or Ripple's RLUSD, their business logic is inherently built on 100% reserve asset backing. Stablecoins do not engage in credit expansion nor rely on a fractional reserve lending model, thus they do not carry the systemic risk associated with the "maturity mismatch" of traditional banks. Under this premise, introducing FDIC deposit insurance is unnecessary and would significantly increase the compliance burden.

More importantly, the core of a trust bank charter lies in fiduciary duty. This means licensed institutions are legally required to strictly segregate client assets from their own funds and prioritize client interests. This has strong practical significance for the entire crypto industry post the FTX client asset misappropriation scandal. Asset segregation is no longer a company promise but a mandatory obligation under federal law.

From "Custodian" to "Payment Node"

Another profound implication of this change is a key shift in the regulatory interpretation of the "trust bank" business scope. OCC head Jonathan Gould explicitly stated that the new federal bank access "provides consumers with new products, services, and sources of credit, and ensures the banking system is vibrant, competitive, and diverse." This laid the policy foundation for accepting crypto institutions.

Under this framework, the strategic value of Paxos and BitGo's "conversion" from state trust to federal trust bank status far exceeds a mere change in title. The core lies in the fact that the OCC system grants federal trust banks a key right: the eligibility to apply for access to the Federal Reserve's payment systems. Therefore, their real target is not the "bank" title, but competing for direct access to the central bank's core settlement system.

Taking Paxos as an example, although it had already become a compliance benchmark under the strict supervision of the New York State Department of Financial Services (NYDFS), state charters have inherent limitations: they cannot directly connect to the federal payment network. The OCC's approval document clearly states that the converted new entities can continue to engage in businesses like stablecoins, asset tokenization, and digital asset custody. This is equivalent to officially acknowledging at the institutional level: stablecoin and asset tokenization issuance have become legitimate "banking activities." This is not a breakthrough for individual companies but a substantive expansion of the "banking" function.

Once fully implemented, these institutions are expected to directly connect to central bank payment systems like Fedwire or CHIPS, no longer necessarily relying on traditional commercial banks as intermediaries. The leap from "custodied asset manager" to "direct node in the payment network" is the most structurally significant breakthrough in this regulatory shift.

Why This License is Priceless

The true value of the federal trust bank license lies not in the "bank" identity itself, but in the fact that it potentially opens a door to direct access to the Federal Reserve's clearing system.

This is also why Ripple CEO Brad Garlinghouse called this approval a "huge step forward," while traditional banking lobby groups (BPI) appeared very uneasy. For the former, it means efficiency and certainty; for the latter, it means the long-monopolized financial infrastructure is being redistributed.

What does Direct Fed Connection mean?

Prior to this, crypto companies were always in the "peripheral layer" of the dollar system. Whether Circle issuing USDC or Ripple providing cross-border payments, any final settlement involving US dollars had to be completed through commercial banks as intermediaries. This model is known in financial terms as the "correspondent banking system." Superficially, it's just a longer process, but in essence, it has caused three long-term problems plaguing the industry.

First is the uncertainty of the right to exist. In recent years, the crypto industry has repeatedly faced situations where banks unilaterally terminated services. Once a correspondent bank withdraws, the fiat channels of crypto companies can be cut off in a very short time, bringing business to a halt. This is the so-called "de-banking" risk.

Second is the cost and efficiency issue. The correspondent model means every fund flow must go through multiple layers of bank clearing, each layer accompanied by fees and time delays. This structure is inherently unfriendly to high-frequency payments and stablecoin settlements.

Third is settlement risk. The traditional banking system generally adopts T+1 or T+2 settlement cycles. Funds in transit not only tie up liquidity but are also exposed to bank credit risk. When Silicon Valley Bank collapsed in 2023, Circle had approximately $3.3 billion in USDC reserves temporarily stranded in the banking system, an event still seen as a cautionary tale for the industry.

The federal trust bank status changes this very structure. At the institutional level, licensed institutions are eligible to apply for a Federal Reserve "master account." Once approved, they can directly access federal-level clearing networks like Fedwire, achieving real-time, irrevocable final settlement within the dollar system, no longer relying on any commercial bank intermediary.

This means that in the critical环节 of fund clearing, institutions like Circle and Ripple, for the first time, stand at the same "system level" as JPMorgan Chase and Citibank.

Ultimate Cost Advantage, Not Marginal Optimization

The reduction in payment costs from obtaining a master account is structural, not marginal. The core principle is that a direct connection to the Federal Reserve's payment system (like Fedwire) completely bypasses the multiple intermediaries of the traditional correspondent banking system, thereby removing the corresponding middleman fees and markups.

Based on industry practices and the Fed's public fee structure for 2026, projections indicate that in high-frequency, large-volume scenarios like stablecoin issuance and institutional payments, this direct connection model could reduce overall settlement costs by approximately 30%-50%. Cost reduction primarily comes from two levels:

- Direct Fee Advantage: The Fed's per-transaction fee for large-value Fedwire payments is significantly lower than commercial banks' wire transfer quotes.

- Structural Simplification: Eliminates various handling fees, account maintenance fees, and liquidity management costs associated with the correspondent bank环节.

Taking Circle as an example, its nearly $80 billion USDC reserves face huge daily fund flows. If direct connection is achieved, the savings on payment channel fees alone could amount to hundreds of millions of dollars annually. This is not a minor optimization but a fundamental cost restructuring at the business model level.

Therefore, the cost advantage brought by master account eligibility is certain and substantial, directly translating into a core moat for stablecoin issuers in terms of fee competition and operational efficiency.

The Legal and Financial Attributes of Stablecoins are Changing

When stablecoin issuers operate as federal trust banks, the attributes of their products also change. In the old model, USDC or RLUSD were closer to "digital vouchers issued by tech companies," their security highly dependent on the issuer's governance and the soundness of partner banks. In the new structure, stablecoin reserves will be placed within a federally regulated OCC fiduciary system and achieve legal mandatory segregation from the issuer's own assets.

This is not equivalent to a central bank digital currency (CBDC), nor does it involve FDIC insurance, but under the combination of "100% full reserve + federal-level regulation + fiduciary duty," its credit rating is significantly higher than most offshore stablecoin products.

A more practical impact lies in payments. Taking Ripple as an example, its ODL (On-Demand Liquidity) product has long been constrained by bank operating hours and fiat channel availability. Once integrated into the federal clearing system, the切换 between fiat and on-chain assets will no longer be limited by time windows, significantly enhancing the continuity and certainty of cross-border settlements.

Market Reaction is More Rational

Although this development is seen as a milestone within the industry, the market reaction did not show剧烈波动. Whether XRP or USDC-related assets, price changes were relatively limited. But this does not mean the license value is underestimated; it更可能表明: the market already views it as a long-term institutional change, not a short-term trading theme.

Ripple CEO Brad Garlinghouse defined this progress as "the highest standard on the stablecoin compliance path." He not only emphasized that RLUSD is now under dual regulation (OCC federal and NYDFS state) but also directly targeted traditional banking lobbies: "Your anti-competitive tactics have been seen through. You complain that the crypto industry doesn't follow the rules, but now we are under the OCC's direct regulatory standards. What are you really afraid of?"

Meanwhile, Circle also stated in related announcements that the national trust bank charter will fundamentally reshape institutional trust, enabling issuers to provide digital asset custody services with greater fiduciary responsibility to institutional clients.

The statements from both converge: From "being served by banks" to "becoming part of the bank," crypto finance is entering a全新的 stage. And the federal trust bank license is not just a permit; it paves a safe通道 for institutional capital, which has been观望 due to compliance uncertainty, to enter the crypto market.

The Trump Era's "Golden Period" and the GENIUS Act

Rolling back the clock three or four years, it was hard to imagine crypto companies gaining federal recognition as "banks" by the end of 2025. What facilitated this转变 was not technological breakthrough but a fundamental shift in the political and regulatory environment.

The return of the Trump administration and the enactment of the GENIUS Act together paved the way for crypto finance to access the federal system.

From "De-banking" to Institutional Acceptance

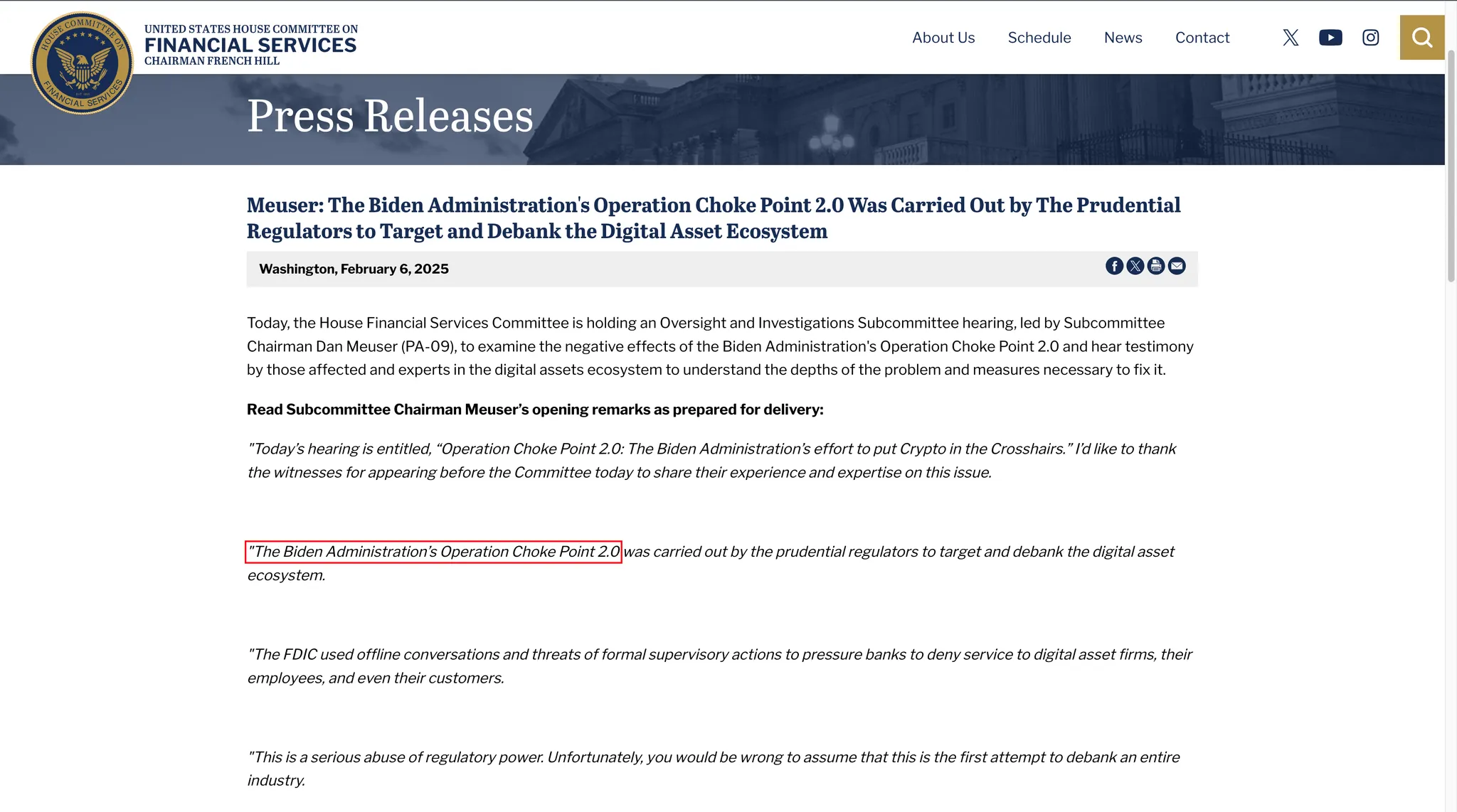

During the Biden administration, the crypto industry long remained in an environment of strong regulation and high uncertainty. Especially after the FTX collapse in 2022, the regulatory基调 shifted to "risk isolation," with the banking system being urged to stay away from crypto business.

This phase was called "de-banking" within the industry and described by some lawmakers as "Operation Choke Point 2.0." According to subsequent investigations by the House Financial Services Committee, multiple banks cut ties with crypto firms under informal regulatory pressure. The successive exits of Silvergate Bank and Signature Bank were a集中体现 of this trend.

The regulatory logic then was clear: Rather than painstakingly regulating crypto risks, isolate them outside the banking system.

This logic was fundamentally reversed in 2025.

Trump repeatedly expressed support for the crypto industry during his campaign, emphasizing making the US the "global center for crypto innovation." Upon returning to office, crypto assets were no longer单纯 viewed as a risk source but incorporated into broader financial and strategic considerations.

The key shift was that stablecoins began to be seen as an extension tool of the dollar system. On the day the GENIUS Act was signed, the White House explanation明确指出 that regulated dollar stablecoins help expand the demand for US Treasury bonds and consolidate the international status of the US dollar in the digital age. This实质上 redefined the role of stablecoin issuers in US finance.

The Institutional Role of the GENIUS Act

In July 2025, Trump signed the GENIUS Act. The significance of this act lies in首次 establishing a clear legal identity for stablecoins and related institutions at the federal level. The act explicitly allows non-bank institutions, upon meeting conditions, to be regulated federally as "qualified payment stablecoin issuers." This provided an institutional entry point into the federal framework for companies like Circle and Paxos, which were originally outside the banking system.

More importantly, the act imposes hard requirements on reserve assets: stablecoins must be 100% backed by highly liquid assets such as US dollar cash or short-term US Treasury bonds. This实质上 excludes algorithmic stablecoins and high-risk allocations, also高度契合 the trust bank model of "not taking deposits, not making loans."

Furthermore, the act establishes the priority claim right of stablecoin holders. Even if the issuing institution goes bankrupt, the relevant reserve assets must be prioritized to redeem the stablecoins. This clause significantly reduces regulatory concerns about "moral hazard" and enhances the credibility of stablecoins at the institutional level.

Under this framework, the OCC's issuance of federal trust bank licenses to crypto companies became a顺理成章的 institutional implementation according to regulations.

Traditional Finance's Defense and Future Challenges

For the crypto industry, this is a long-awaited institutional breakthrough; but for Wall Street incumbents, it更像是一次必须反击的 invasion of territory. The OCC's approval for five crypto institutions to convert into federal trust banks did not garner unanimous applause but quickly triggered a猛烈的防御 from traditional banking coalitions represented by the Bank Policy Institute (BPI). This war between "old and new banks" has just begun.

BPI's Fierce Counterattack: Three Core Accusations

BPI represents the interests of giants like JPMorgan Chase, Bank of America, and Citigroup. Immediately after the OCC announced its decision, its leadership issued sharp质疑, with core arguments targeting deep-seated conflicts in regulatory philosophy.

First, is the accusation of "regulatory arbitrage" - "calling a deer a horse" (挂羊头卖狗肉). BPI pointed out that these crypto institutions applying for "trust" charters is a form of self-deception, as their actual activities are core banking businesses like payments and clearing, with systemic importance even exceeding that of many medium-sized commercial banks.

However, through the trust charter, their parent companies (e.g., Circle Internet Financial) cleverly avoid the consolidated supervision by the Federal Reserve that is mandatory for "bank holding companies." This means regulators have no authority to review the parent company's software development or external investments—if code vulnerabilities in the parent company lead to bank asset losses, this would create a huge risk exposure in a regulatory blind spot.

Second, is the破坏 of the sacred principle of "separation of banking and commerce". BPI warned that allowing tech companies like Ripple and Circle to own banks实质上 breaks the firewall preventing industrial and commercial giants from using bank funds for输血 (funneling). What makes traditional banks even more dissatisfied is unfair competition: tech companies can use their monopolistic advantages in social networks and data flows to squeeze out banks, without having to fulfill the Community Reinvestment Act (CRA) obligations mandatory for traditional banks.

Finally, is the fear regarding systemic risk and the lack of a safety net. Since these new trust banks have no FDIC insurance backstop, once panic about stablecoin depegging occurs, traditional deposit insurance cannot act as a buffer. BPI argues that this kind of unprotected liquidity crunch would quickly spread, evolving into a systemic crisis similar to 2008.

The Fed's "Final Checkpoint"

The OCC issuing a license does not mean everything is settled. For these five newly minted "federal trust banks," the final and most critical checkpoint to the federal payment system—the right to open a master account—remains tightly held by the Federal Reserve.

Although the OCC认可 their bank status, under the US dual banking system, the Fed has independent discretion. Previously, the crypto bank Custodia Bank in Wyoming initiated lengthy litigation after being denied a master account by the Fed. This precedent shows that there is still a huge gap between obtaining a license and真正接入 Fedwire.

This is also the next main battlefield for traditional banking (BPI) lobbying. Since阻止 the OCC from issuing licenses is impossible, traditional banking forces will势必 pressure the Fed to set extremely high thresholds when approving master accounts—for example, requiring these institutions to prove their anti-money laundering (AML) capabilities are on par with universal banks like JPMorgan Chase, or requiring their parent companies to provide additional capital guarantees.

For Ripple and Circle, this game has just entered the second half: if they get the license but cannot open a Fed master account, they will still have to operate through the correspondent banking model, greatly diminishing the gold content of this "national-level bank"招牌.

Conclusion: The Future is More Than Just Regulatory Games

It can be expected that the future game surrounding crypto banks will显然 not stop at the licensing level.

On one hand, the attitude of state regulators remains uncertain. Powerful state regulators represented by the New York State Department of Financial Services (NYDFS) have long played a leading role in crypto regulation. As federal preemption expands, whether state regulatory power is weakened may trigger new legal disputes.

On the other hand, although the GENIUS Act has taken effect, numerous implementation details still need to be formulated by regulatory agencies. Specific rules including capital requirements, risk isolation, and cybersecurity standards will become the focus of policy in the coming period. Games between different interest groups will likely play out in these technical provisions.

Furthermore, changes at the market level are also worth noting. As crypto institutions obtain bank status, they could become either合作对象 for traditional financial institutions or potential acquisition targets. Whether traditional banks acquire crypto institutions to补齐技术能力, or crypto companies move反向 into banking, the financial landscape could undergo structural adjustments accordingly.

One thing is certain: this OCC approval is not the end of the controversy, but a new starting point. Crypto finance has entered the institutional interior, but how to find a balance between innovation, stability, and competition will remain a question that US financial regulation must answer in the coming years.