Original | Odaily Planet Daily (@OdailyChina)

Author | Ding Dang (@XiaMiPP)

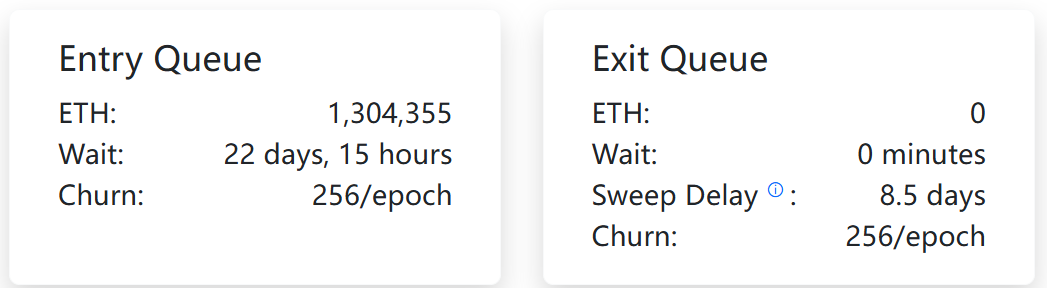

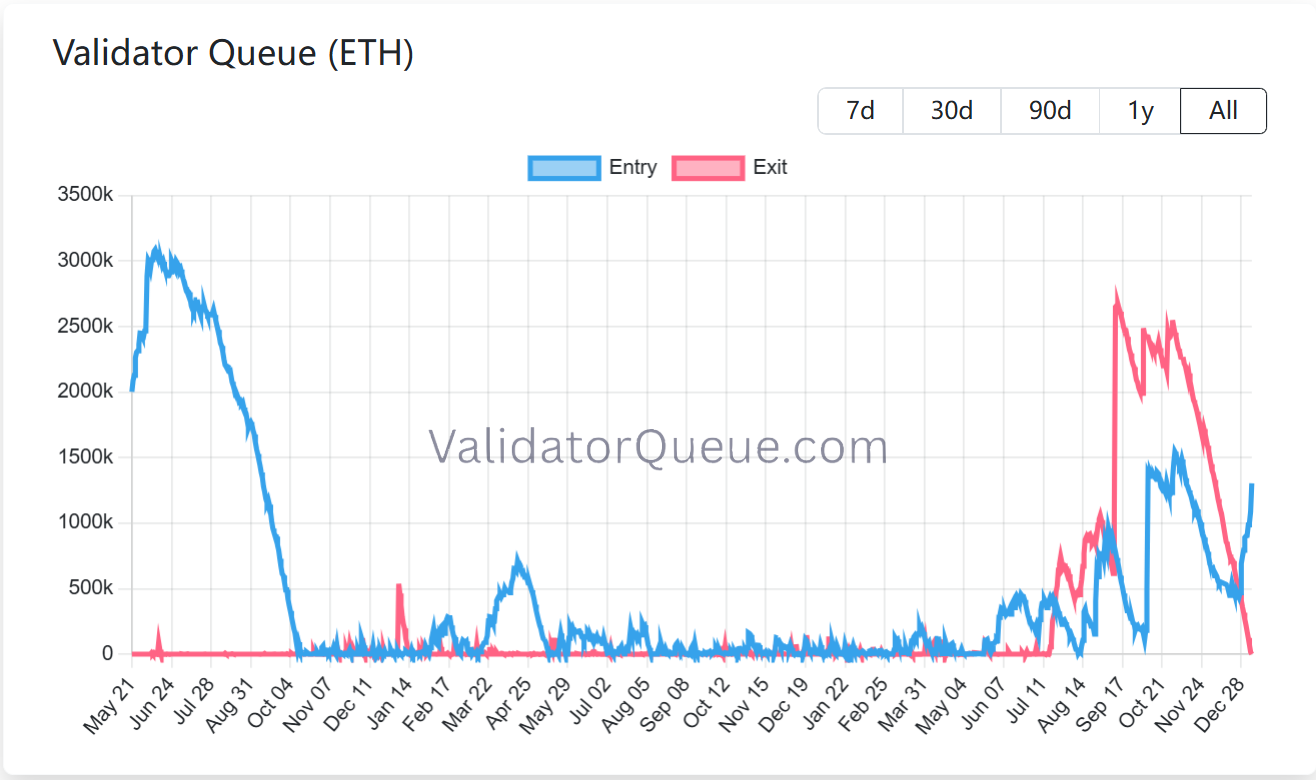

On January 7, the exit queue for Ethereum's Proof-of-Stake (PoS) mechanism officially cleared. At least from on-chain data, the sustained exit pressure over the past months has finally been fully digested, with no new large-scale redemption requests currently observed.

At the same time, the size of the staking entry queue has significantly increased, now reaching approximately 1.3044 million ETH, with a waiting time of about 22 days and 15 hours. This situation is a complete reversal compared to mid-September last year.

At that time, ETH's price was at a阶段性高点 of around $4,700, and market sentiment was high, but the staking side showed a different attitude: 2.66 million ETH chose to exit staking, with exit queue wait times一度 exceeding 40 days. In the following three and a half months, ETH's price fell by about 34%, dropping from $4,700 to $3,100.

Now, after a deep price correction, the exit queue has finally been fully digested.

Staking Queue as a "Sentiment Indicator," But Not a Price Signal?

Typically, changes in the validator queue are seen as an important barometer for gauging market sentiment. The logic behind this is that Ethereum's PoS, to ensure consensus stability, does not allow nodes to enter or exit arbitrarily. Instead, it uses a flow control mechanism to regulate the pace of staking and exit behaviors.

Therefore, when ETH's price is at a high stage, exit demand tends to accumulate. Some stakers may choose to cash out profits, but the potential selling pressure is not released instantly; instead, it is "stretched out" on-chain through the exit queue. When exit demand gradually dries up and is fully digested, it may indicate that a structural selling pressure is coming to an end.

From this perspective, the clearing of the current exit queue, coupled with the simultaneous rise in the entry queue, does constitute a noteworthy change. However, I believe that while this change appears to form a positive resonance on the surface, its impact on market prices—note, "impact"—is not equivalent to the "high exits, low entries" phase in September. This is because ETH entering the staking queue does not equate to "new funds actively buying ETH at the moment." A significant portion of the筹码 entering staking likely completed accumulation at an earlier stage and is only choosing to reallocate at the current time. Therefore, the rise in the staking queue reflects more a change in preference for long-term returns, network security, and the stability of staking rewards, rather than a significant strengthening of immediate price demand. This also means that the current improvement in queue structure is more about expectation repair than an equally strong boost to short-term prices.

Nevertheless, the significant growth in the current staking entry queue is still worth attention. The main driving force behind this comes from BitMine, the largest DAT treasury company for Ethereum. CryptoQuant data shows that BitMine has staked approximately 771,000 ETH in the past two weeks, accounting for 18.6% of its holdings of about 4.14 million ETH.

This means that this shift in staking trends is driven by a single large institution's asset allocation behavior, rather than a synchronized回暖 in overall market risk appetite. Therefore, it cannot be simply interpreted as a "return of全面看多 sentiment." However, in an emerging market like crypto, where liquidity distribution is uneven, the actions of large institutions are often more likely to, and can more easily, provide a certain degree of emotional support and expectation repair in the short term.

Whether this trend can continue or spread to a broader range of participants remains to be seen over time. But from on-chain fundamental data, several core metrics of Ethereum are simultaneously showing signs of marginal improvement.

From "Staking Changes" to "Coordinated Fundamental Improvement"

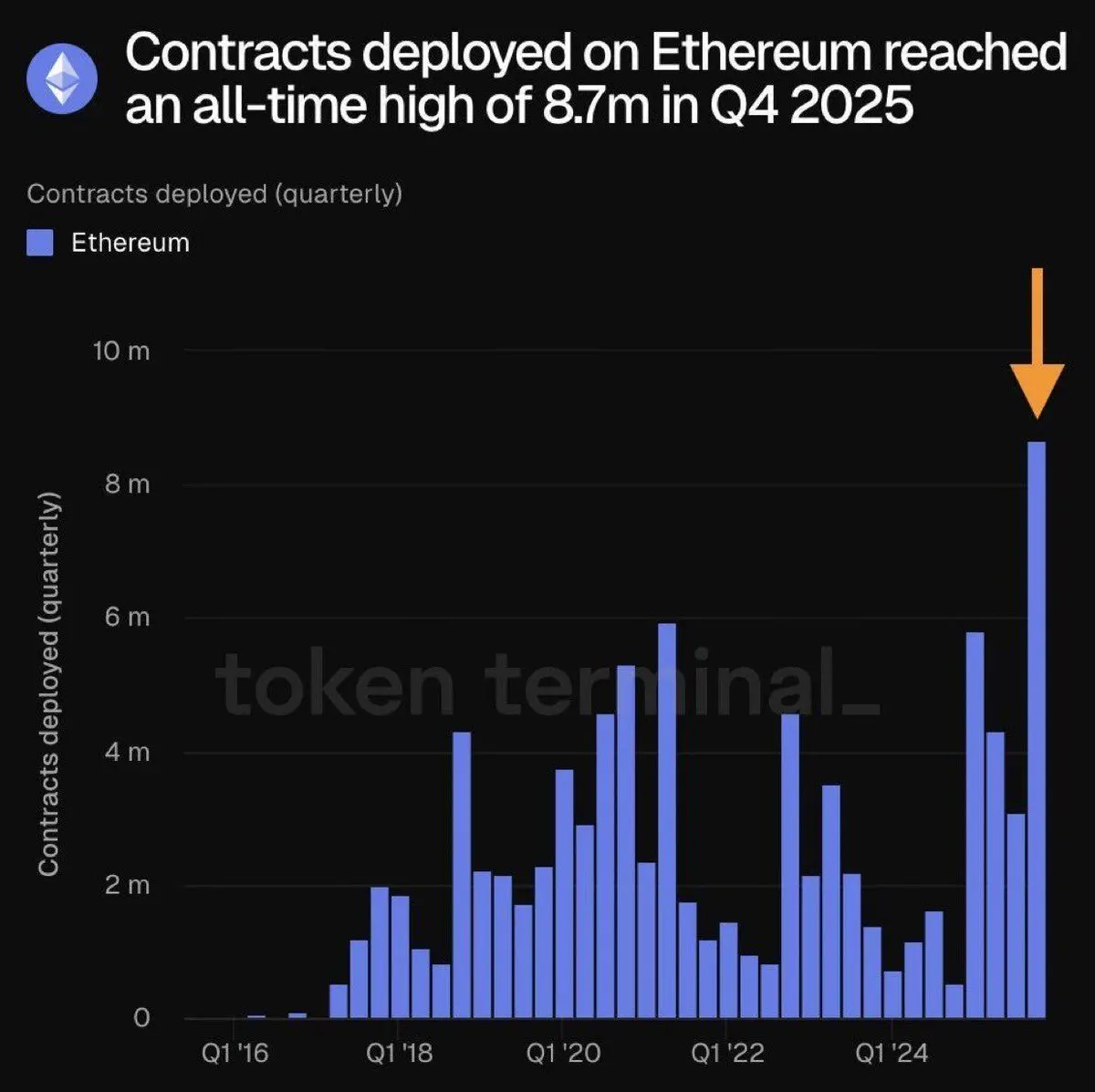

First, in terms of developers, Ethereum's development activity is hitting all-time highs. Data shows that in Q4 2025, Ethereum deployed approximately 8.7 million smart contracts, setting a new historical record for a single quarter. This change is closer to sustained product and infrastructure development rather than short-term speculative behavior. More contract deployments mean more DApps, RWA, stablecoins, and infrastructure are being launched, continuously strengthening Ethereum's role as a core execution and settlement layer.

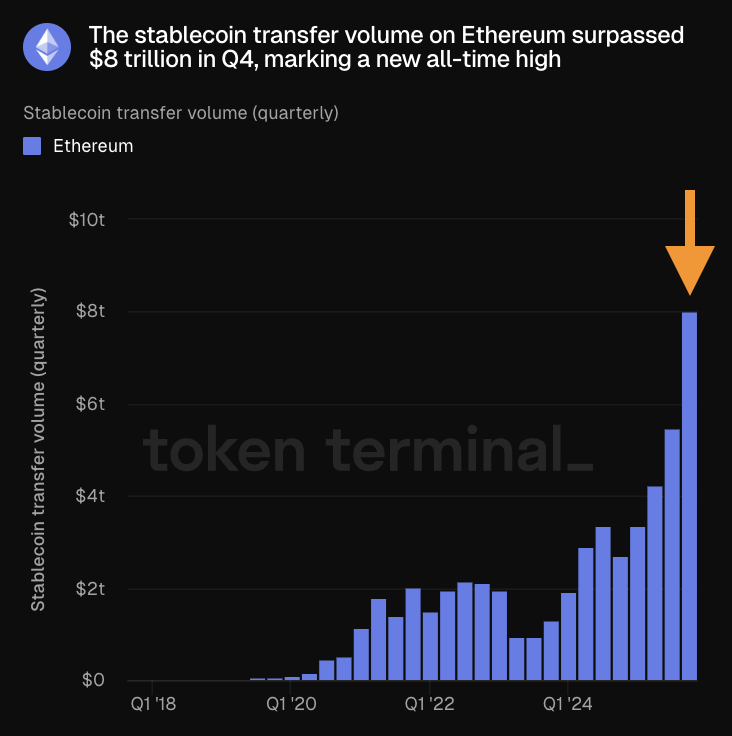

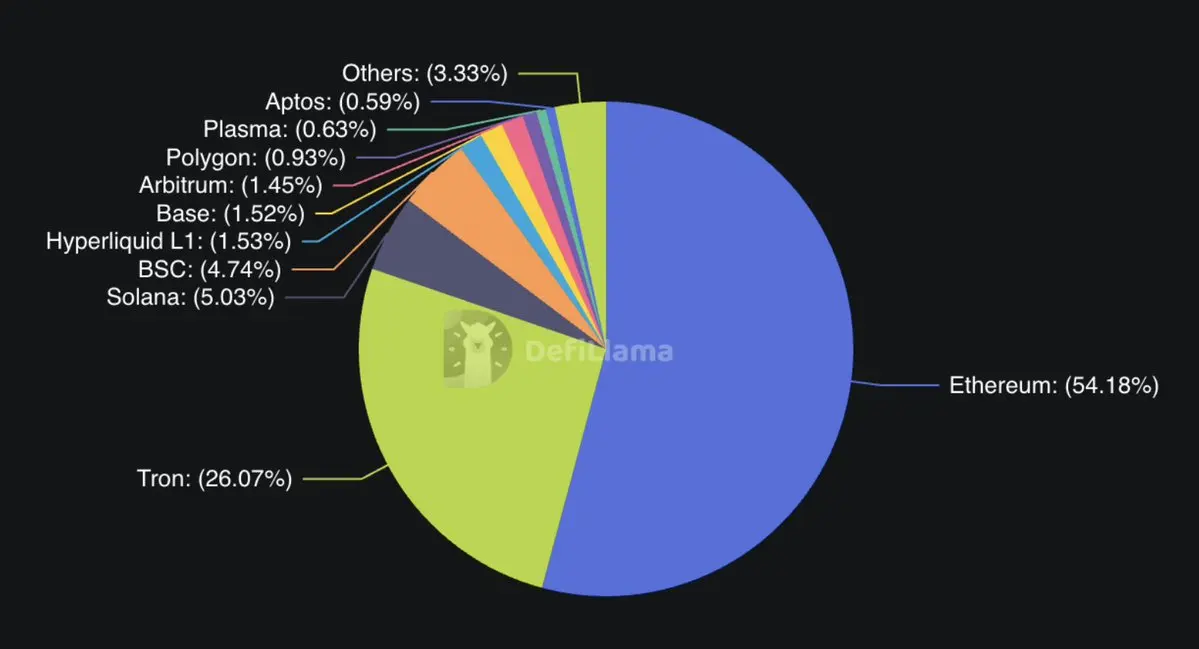

In the stablecoin sector, the on-chain transfer volume of stablecoins on Ethereum in Q4 exceeded $8 trillion, also setting a new historical record. In terms of issuance structure, Ethereum's advantage in the stablecoin ecosystem remains significant. Data shows that the share of stablecoin issuance on Ethereum is as high as 54.18%, far exceeding other mainstream blockchain networks like TRON (26.07%), Solana (5.03%), and BSC (4.74%).

At the same time, Ethereum Gas fees have hit the lowest records since the mainnet launch and are continuously breaking records. In some periods, Gas fees were even below 0.03 Gwei. Considering that Ethereum will continue to推进 block扩容 this year, this trend has room to continue in the medium term. Lower transaction costs directly reduce the barrier to on-chain activity and provide a practical foundation for the continued expansion of the application layer.

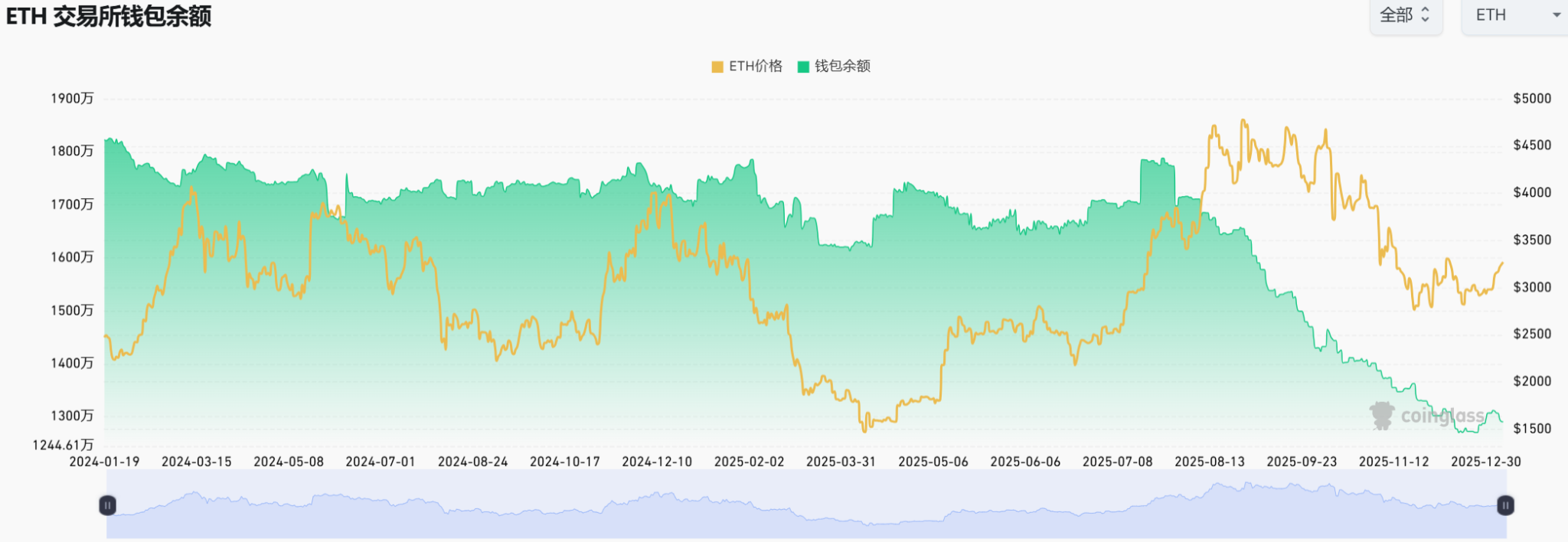

Looking at the exchange balance metric, Ethereum's potential selling pressure is also at a low level. In mid-December, Ethereum's exchange supply dropped to 12.7 million, the lowest level since 2016. Especially since August 2025, this metric has shown a significant decline of over 25%. Although exchange balances have slightly increased recently, the increment is only about 200,000 ETH, and the overall level remains in a historically low range, indicating weak selling意愿 among traders.

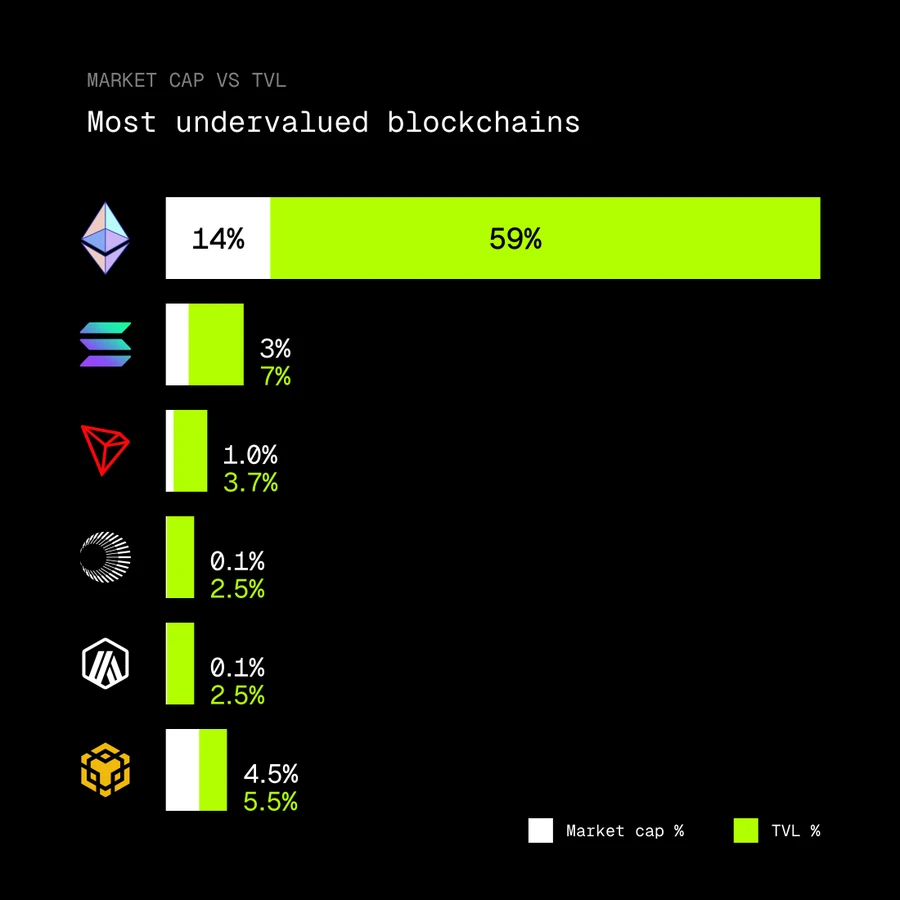

Additionally, crypto KOL rip.eth recently posted on X platform, pointing out that judging from the gap between Total Value Locked (TVL) and market capitalization, Ethereum might be the most undervalued blockchain network currently. Data shows that Ethereum carries 59% of the crypto market's TVL, but its token ETH's market share is only about 14%. In comparison, Solana's token market cap / TVL ratio is 3% / 7%, Tron's is 1% / 3.7%, and BNB Chain's is 4.5% / 5.5%. This, to some extent, reflects that there is still a significant misalignment between ETH's valuation and the scale of economic activity it supports.

Conclusion

Overall, changes in the staking queue may not be the "single variable" determining price trends. But when it improves simultaneously with metrics like developer activity, stablecoin usage volume, transaction costs, and exchange balances, it no longer presents an isolated signal but a more comprehensive fundamental picture.

For Ethereum, this might not be a sentiment-driven rapid reversal, but rather a process where the system is gradually restoring structural stability after undergoing a deep adjustment.