Author: Thejaswini M A

Compilation: Chopper, Foresight News

Thousands of years ago, the ancient Greek Agorá was the public marketplace in Athens, a place where anyone could come and trade freely, with no entry barriers, not bound by any local jurisdiction. The concept of "permissionlessness" lies at the very heart of this word.

The Bank for International Settlements (BIS) named its project Agorá, a choice laden with meaning. However, the actual design of the Agorá project, spearheaded by the BIS and implemented jointly by seven central banks and over forty private institutions, stands in stark contrast to the word's original association with a "free market."

In this system, funds are tagged with their country of origin before they are transferred; smart contracts perform anti-money laundering screening and sanctions list verification at the token layer; each central bank retains full control over its own reserves, and cross-border fund flows must pass through a compliance validation layer embedded within the token.

In short, this is a programmable fiat currency system where permission must be granted beforehand for everything.

The seven central banks participating in the Agorá project are: the Federal Reserve Bank of New York, the Bank of England, the Bank of Japan, the Bank of Korea, the Bank of Mexico, the Swiss National Bank, and the Banque de France representing the Eurozone; the Bank of Canada joined the ranks just four days ago. Financial giants such as JPMorgan Chase, HSBC, Deutsche Bank, UBS, Mastercard, Visa, and the Society for Worldwide Interbank Financial Telecommunication (SWIFT), along with more than forty other institutions, are jointly involved in the development.

A project mobilizing such a massive institutional force prompted me to delve deeper into dissecting this system.

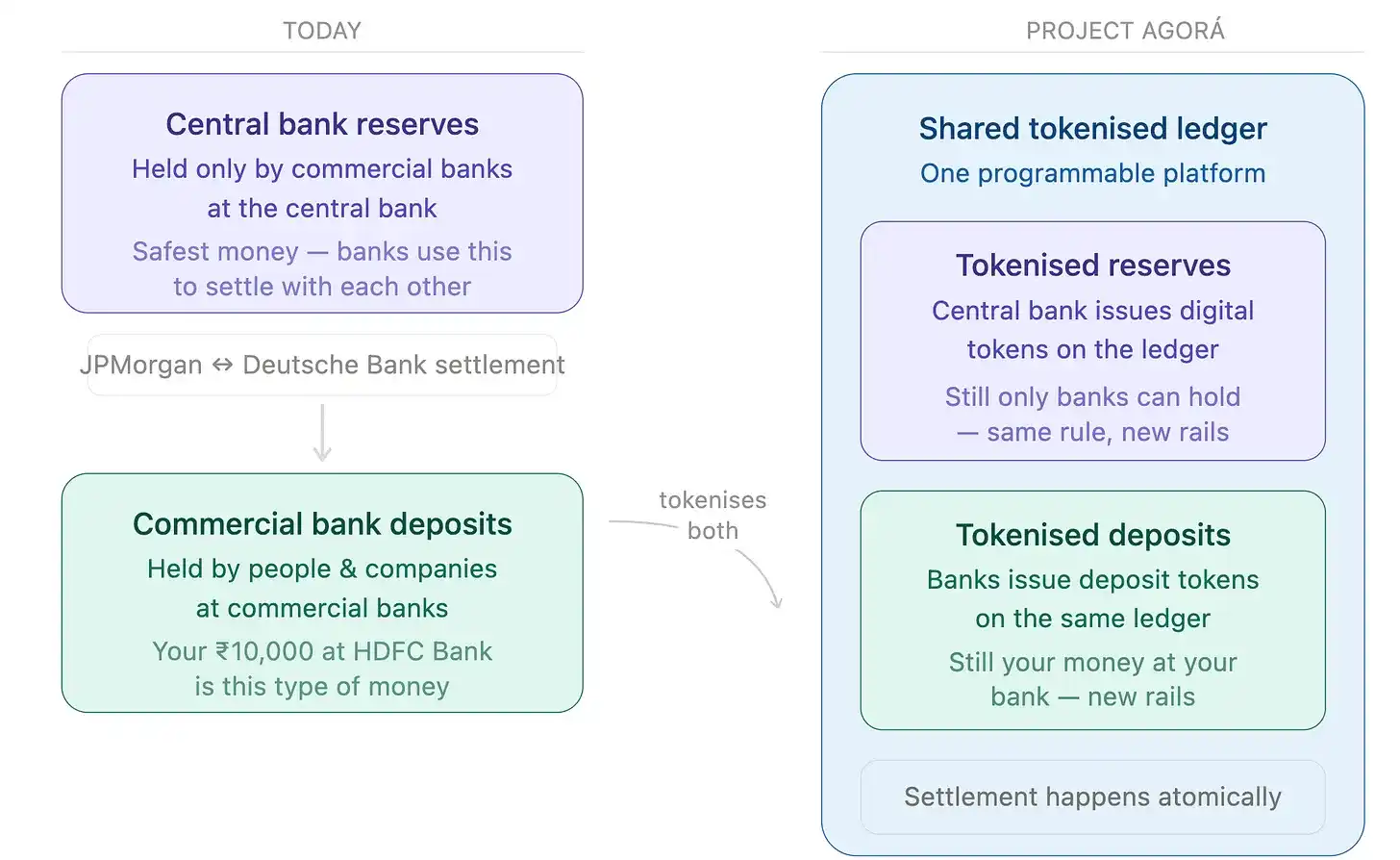

The project employs a two-tier separated architecture: one tier is fully controlled by the respective central banks, managing the underlying base currency reserves; the other tier is operated by commercial banks, handling daily transactions for end-users. Tokenized commercial bank deposits are consolidated onto a shared platform, processed collaboratively by multiple private institutions for multi-currency clearing; meanwhile, each central bank's reserves are stored independently on its own sovereign ledger, with sovereignty firmly retained by each respective central bank.

The BIS aims to build a state-controlled, closed-loop payment system by integrating commercial bank ledgers and anchoring sovereign reserves. Institutions are accelerating the implementation of a compliant framework, intending to establish it before decentralized stablecoins like Tether completely sever global commerce from the traditional banking system.

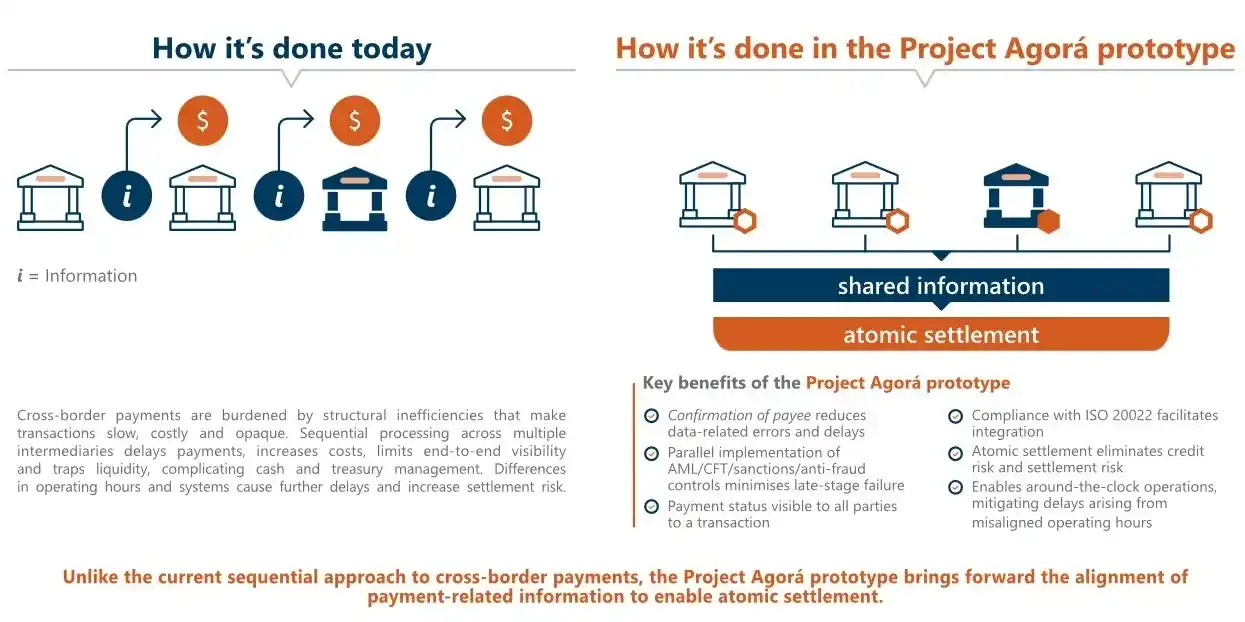

Current cross-border payments are akin to a relay race: message transmission, manual compliance checks, and ledger clearing belong to different institutional systems, often taking days. The Agorá project compresses this lengthy multi-step collaboration into a single on-chain, real-time operation. This prototype concluded on May 27, 2026, with the Bank of Canada promptly announcing its participation.

Organizers emphasize that the current phase remains infrastructure testing, with no formal timeline for commercial deployment, but the next stage will involve pilot tests with real funds.

Unlike previous central bank initiatives that only released research papers, seven major currency authorities spent two years developing and testing this real-time cross-border clearing system. The underlying code is functional. The existing challenge is no longer technical but rather how multiple governments will implement regulation and delineate responsibilities for the shared network, facing immense administrative coordination hurdles.

Meanwhile, the established cross-border messaging giant SWIFT is concurrently advancing its own underlying transformation, positioning its layout precisely within the commercial banking layer. On March 30, 2026, SWIFT finalized the design for its blockchain-based shared ledger, entering Minimum Viable Product (MVP) development, with plans to launch real-time transactions within the year. The ledger is built on Hyperledger Besu, which is compatible with the Ethereum Virtual Machine (EVM), with final fund clearing still performed off-chain using traditional Real-Time Gross Settlement systems.

However, SWIFT and Agorá are not in competition: the SWIFT ledger focuses on reconciling tokenized deposits between commercial banks, while Agorá handles the final large-value clearing of central bank reserves. The BIS ensured interoperability standards between the two systems from the outset, methodically transforming the traditional cross-border clearing system into a programmable digital network in two steps.

A closer look at the participant list reveals significant overlap: Deutsche Bank, a core Agorá member, also formed an alliance with Goldman Sachs, Bank of America, Barclays, Santander, and nine other banks to explore issuing 1:1 reserve-backed tokens on public blockchains; UBS and Citigroup are similarly involved in both; JPMorgan Chase participates in Agorá, operates its own JPM Coin, and recently piloted cross-border clearing on the Ripple ledger.

Such parallel investments are highly unusual in finance: the standard practice for institutions is to concentrate technical resources on one technological path. Top teams simultaneously developing two potentially competing frameworks on separate tracks reflects internal division within bank management. Giants holding vast data and enormous capital cannot predict which framework will ultimately prevail. The technological paths are clear, but policy directions remain uncertain.

Ripple, after a decade of effort, has consistently argued that "atomic settlement" (where a transaction either completes in full or fails entirely) is the optimal solution for cross-border payments. Now, the BIS's Agorá project has implemented this settlement logic, albeit replacing XRP as the bridging asset with central bank reserve tokens, directly undermining XRP's necessity as a cross-border bridge asset.

Nevertheless, the Ripple ledger continues to permeate traditional finance. On May 6, JPMorgan's Kinetyx, Mastercard, Ripple, and Ondo Finance completed the first cross-border redemption of tokenized U.S. Treasury bonds on Ripple, with the entire clearing process taking less than five seconds. The Ripple USD stablecoin RLUSD's market capitalization surpassed $1.4 billion; in January 2026, the total value of tokenized assets on Ripple exceeded $2 billion; Société Générale issued a Euro stablecoin on Ripple in February; and in December 2025, Ripple obtained a limited-purpose trust bank charter from the U.S. Office of the Comptroller of the Currency (OCC).

While Ripple's architectural logic is validated, the assertion that "XRP is indispensable" has not materialized. Even so, Ripple's ongoing integration into institutional clearing systems holds far greater significance for long-term value than debates over whether Ripple or central bank reserve tokens are superior.

Setting aside commercial rhetoric, on the Ripple network, transaction fees are extremely low and permanently waived, not flowing to node operators. Increased institutional transaction volume does not generate revenue for validators or token holders like Ethereum's Gas fees; it only results in a slight burn of the existing XRP supply. When institutions like JPMorgan transfer tokenized assets on-chain, they utilize their own liquidity pools and do not rely on XRP circulating in the market for liquidity support; the network merely provides high-speed transfer and cryptographic security.

The core value of this model lies in ecosystem lock-in. Once financial institutions trust the network to custody fiat and stablecoin assets, the technology becomes embedded in global financial infrastructure, compelling the deployment of bank-grade node facilities, and the ledger becomes a permanent component of the global financial system. In the long run, deep technological integration with global banking is far more important than the price fluctuations of a single token.

All these variables ultimately converge on the stablecoin arena. Tether's daily trading volume consistently ranges between $40-50 billion, with the total stablecoin market exceeding $320 billion. While Agorá is still in the pilot stage with deployment seemingly distant, SpaceX already uses stablecoins to manage cross-border corporate funds, and Western Union has launched remittance services on the Solana public blockchain; market competition has already taken the lead.

Agorá targets large-scale, wholesale cross-border clearing for institutions. If successfully deployed, it could divert corporate cross-border funding needs currently served by stablecoins. However, this is just one segment of stablecoin applications: Brazil's Central Bank issued Resolution 561, prohibiting local financial institutions from using stablecoins for cross-border payments, yet it cannot stop Brazilian citizens from holding dollar stablecoins as a store of value; Turkish retail investors buy USDT to hedge against lira inflation—these fragmented needs fall outside Agorá's intended scope.

In the short term, stablecoins and Agorá are more complementary than competitive, with almost non-overlapping use cases: Agorá is a closed institutional network, accessible only to central banks or licensed banks authorized by them; ordinary people hoarding dollars for safety or small payment companies using public blockchains for remittances cannot access this system. The official closed-loop system cannot achieve the inclusive access speed of public blockchains, nor can public chain stablecoins achieve the final settlement authority required by central banks.

The medium-term landscape is more complex. Currently, corporate treasury teams choose USDC or USDT for cross-border settlements primarily due to the lengthy cycles and high fees of traditional correspondent banking. If Agorá is successfully deployed in the future with sufficient liquidity, some corporate funds may shift. Given comparable clearing efficiency, corporate treasurers would likely prioritize official channels that are sovereign-regulated and free from third-party counterparty risk.

However, unifying governance rules among seven sovereign central banks is a monumental global challenge, and many past cross-border projects have failed at this hurdle. Simultaneously, major corporations have already integrated USDC systems and established mature risk control processes; they will not overhaul existing operations simply because of a theoretically superior new system.

The market will likely evolve towards stratification: Agorá monopolizes large-value institutional cross-border channels, while public chain stablecoins retain the retail and fragmented business segments. This appears to be a market split, but in reality, the sovereign system completes the boundary-setting for public chains, confining decentralized networks to areas that cannot challenge the foundations of traditional intermediaries—remittances, individual savings, and small-value payments in emerging markets. These markets are sizable but not the core concentration points of global financial leverage.

This market stratification theory is about to face real-world testing: the EU's Pontes framework is set to connect various distributed ledgers with Europe's core clearing system, TARGET, by September 2026—just three months away. Once successfully integrated, European institutional tokenized payments will gain direct access to central banks, marking the formal beginning of direct competition between the official system and open public blockchains.

The ancient Athenian Agorá marketplace ultimately perished because people stopped going there to trade. That, ultimately, is the final metric by which all financial networks are judged.