Cryptocurrency exchange Crypto.com is building an internal market-making team as part of its expansion into prediction markets, a move the company says is fully aligned with federal regulations and intended to improve liquidity, even as market-making in outcome-based trading continues to draw scrutiny.

Bloomberg reported Tuesday that the exchange is recruiting for a new role on its market-making desk, citing a job posting for a “quant trader” who would help buy and sell contracts tied to the outcomes of sporting events on Crypto.com’s prediction platform.

The report has drawn attention to the practice of exchanges facilitating trading against customer orders, a structure that can raise questions about conflicts of interest as prediction markets gain traction across both crypto and traditional finance.

In a statement to Cointelegraph, a Crypto.com spokesperson said the company’s internal trading team is fully disclosed to the US Commodity Futures Trading Commission and makes markets across its North American derivatives business.

“The bottom line for customers is [that] more competition and liquidity on the platform creates a better overall experience,” the spokesperson said, adding that internal and external market makers operate under the same rules to ensure market fairness and integrity.

“No market maker at Crypto.com gets a ‘first look’, and our internal market maker does not have access to proprietary data or customer order flow before other market makers or market participants,” the spokesperson said.

They added that Crypto.com does not rely on proprietary trading as a revenue source. “We have a simple business model providing our retail customers access to digital assets for a fee, while staying risk neutral," they said.

Related: Phantom taps Kalshi to offer regulated prediction markets in wallet

Market-making isn’t unique to Crypto.com

Crypto.com is not the only prediction-market operator to rely on market makers to support liquidity.

The Bloomberg report noted that competitors such as Kalshi and Polymarket also use professional trading companies or dedicated liquidity providers to facilitate trading on their platforms.

Kalshi, which operates a federally regulated event-contract exchange, relies on designated market makers rather than a purely peer-to-peer order book, and those arrangements have largely been public. It has been reported that quantitative trading company Susquehanna International Group has provided market-making services to Kalshi since 2024, helping supply liquidity as trading volumes surged.

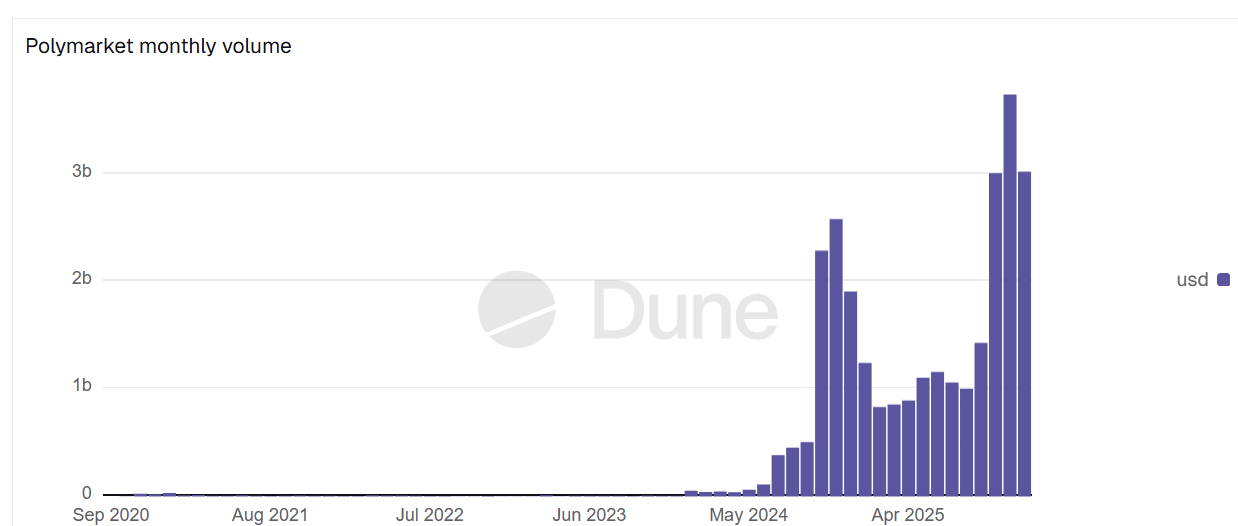

Polymarket, a decentralized prediction market that drew widespread attention during the US presidential election for accurately predicting the outcome, is also building an internal market-making unit, according to Bloomberg.

Related: DraftKings eyes crypto offerings as it expands into prediction markets