MicroStrategy, now operating as Strategy, has become synonymous with corporate Bitcoin accumulation. However, the company’s returns on BTC are currently negative, and there are concerns about how it would fare in a more severe downturn and when its Bitcoin position would be finally wiped out.

Michael Saylor has now responded directly, reposting a statement from Strategy claiming the company can withstand a drop in BTC to $8,000 and still fully cover its debt.

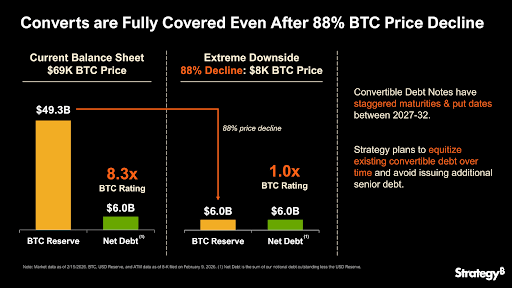

Strategy Says It Can Survive An 88% Bitcoin Crash

Michael Saylor is still bullish on Bitcoin, and according to him, Strategy could continue meeting its obligations even if BTC’s price dropped to $8,000, with the plan being to equitize convertible debt over the next 3 to 6 years.

At the time of writing, Strategy is holding 714,644 BTC in its Bitcoin reserve. Based on the current Bitcoin price of around $69,000, those holdings are valued just under $49 billion. According to recent details shared by Strategy, the firm reports around $6.0 billion in net debt, giving it an 8.3x BTC asset coverage ratio under present conditions.

The interesting part of the disclosure is the downside scenario. The company modeled an 88% price decline in Bitcoin, which would push BTC down to around $8,000. Under that assumption, its Bitcoin reserve would fall to roughly $6.0 billion. That figure still matches or slightly exceeds its net debt position, resulting in a 1.0x coverage ratio.

This means that even if BTC’s price were to suffer an 88% collapse from current levels, Strategy’s Bitcoin holdings would theoretically still be sufficient to cover its outstanding debt obligations on paper.

No Immediate Liquidation Risks For Strategy

Strategy’s borrowings are primarily low-interest convertible notes with staggered maturities and put dates stretching between 2027 and 2032. These are not margin loans secured by BTC that trigger automatic liquidations if BTC falls.

Since there are no margin calls associated directly with BTC price fluctuations, Strategy would not be forced to sell its BTC holdings in a sudden downturn. Instead, the company noted that it plans to equitize existing convertible debt over time. That means converting debt into company shares and avoiding issuing new senior secured debt.

Strategy is still in the business of purchasing huge amounts of Bitcoin, despite the recent price crash below $70,000. The most recent purchase was an additional 1,142 BTC for approximately $90 million in early February. Saylor even recently reiterated that Strategy plans to continue buying Bitcoin on a regular basis.

A BTC collapse to $10,000 would represent an extreme crash of 85% to 90% from recent levels. Although Strategy’s model suggests it could technically cover its net debt at $8,000 per BTC, such a scenario would dramatically shrink the value of its equity from $48.5 billion to less than $6 billion.