On-chain data shows the Cardano sharks and whales have quietly accumulated amid the market decline as their holdings have hit a new record.

Cardano Sharks & Whales Have Pushed Supply To A New All-Time High

In a new post on X, on-chain analytics firm Santiment has talked about the latest trend in the supply of millionaire Cardano wallets. A “millionaire wallet” in the context of ADA refers to an address with 1 million tokens, worth roughly $262,400 at the current exchange rate. The cohorts that are part of this range are popularly known as the sharks and whales.

Since investors with larger holdings have a greater potential influence on the market, holders that fall in this class are considered key for the network. As such, the behavior of the sharks and whales can be worth keeping an eye on.

Now, here is the chart shared by Santiment that shows the trend in the combined amount of supply held by the millionaire Cardano wallets over the last few years:

The value of the metric seems to have been climbing in recent years | Source: Santiment on X

As displayed in the above graph, the Cardano sharks and whales have seen their supply follow a pretty consistent uptrend since December 2023. During 2024 and 2025, the wider cryptocurrency sector followed a bullish trend, so it’s not surprising to see that large holders were accumulating.

Interestingly, however, the uptrend in the supply of the millionaire ADA wallets has maintained even through the bearish market shift that has followed since the last quarter of 2025. The analytics firm noted:

Although the asset has lost -71% of its market cap over the past 9 months, the “millionaire” tier of sharks and whales appear to be content with adding more while prices are at a discount.

Following the latest continuation of the metric’s upward trajectory, its value has reached the 25.09 billion ADA mark, which is a new all-time high (ATH). Though while this is a record in terms of the pure number of tokens, it’s not quite an ATH in terms of the supply share. Cardano has seen its supply go up over the years, so sharks and whales today control about 67.47% of the cryptocurrency’s supply, which is below the highs from 2020.

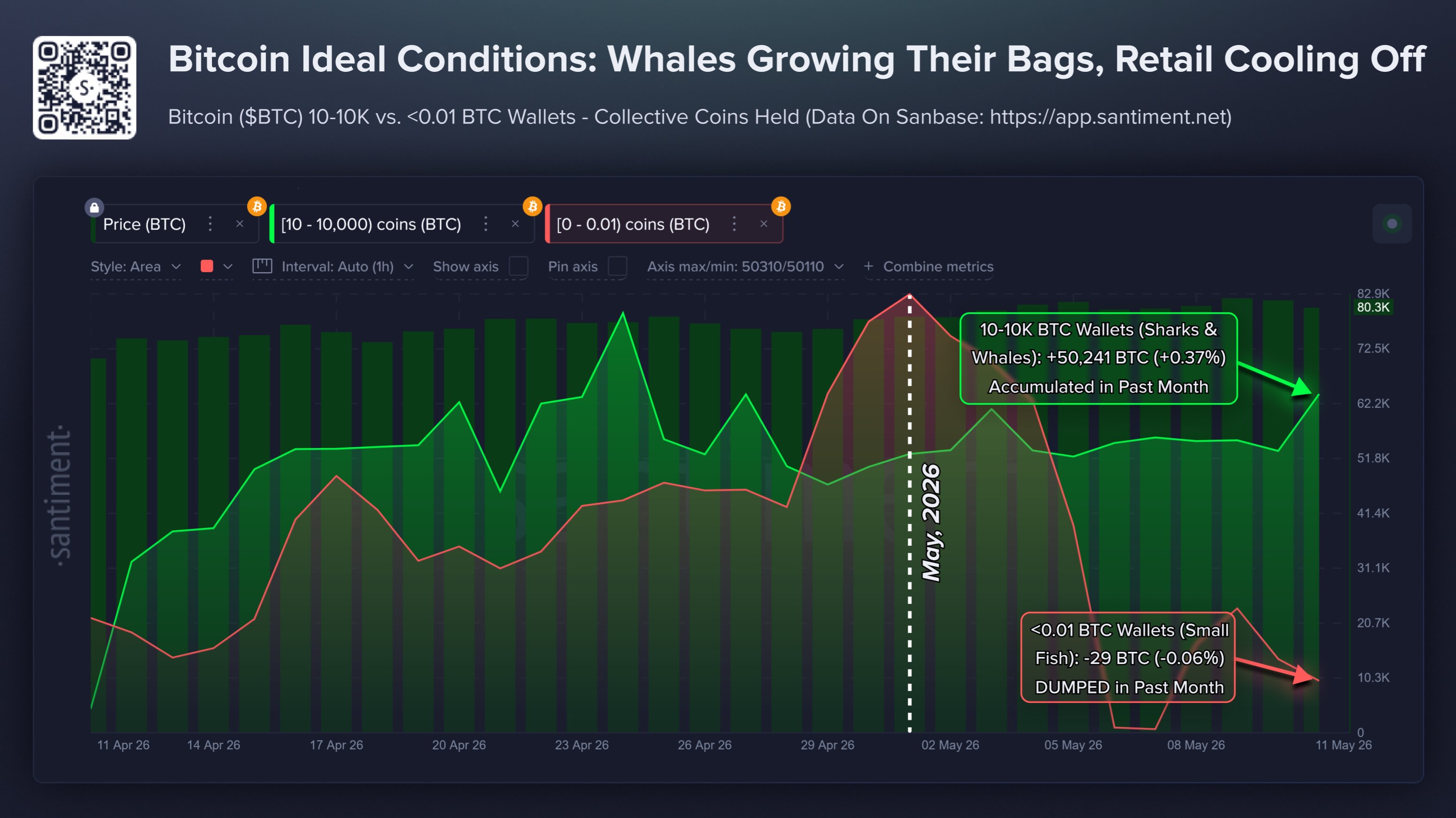

In related news, the Bitcoin sharks and whales have also participated in accumulation recently, as Santiment has highlighted in another X post. For BTC, these investors correspond to the 10 to 10,000 coins range.

As the chart below shows, these large investors have added 50,241 BTC to their holdings over the past month, representing an increase of 0.37%.

How the supply of the BTC sharks and whales has changed recently | Source: Santiment on X

While the large holders have been accumulating, the small entities carrying less than 0.01 BTC have collectively sold 29 BTC in this window instead. “Ideal conditions for any coin consist of large stakeholders continuing to add more to their bags, as retail shows FUD,” explained the analytics firm.

ADA Price

At the time of writing, Cardano is trading around $0.264, down 1.9% over the last 24 hours.

The trend in the price of the coin over the last five days | Source: ADAUSDT on TradingView