Charles Hoskinson, the founder of Cardano and CEO of Input Output, abruptly told followers on X that he is “taking a break,” following a tense livestream on June 2 in which he questioned what power he actually has to stop project failures and funding disputes inside Cardano’s decentralized governance system.

The post was brief: “I’m taking a break. TTYL.” Hoskinson gave no explicit explanation. But the timing points to a broader frustration that has been building around Cardano’s ecosystem funding, the shutdown of TapTools, and the practical consequences of Voltaire-era governance moving authority away from founding entities and toward on-chain decision-making.

TapTools Shutdown Puts Cardano Governance Under Pressure

TapTools, one of the most visible analytics and data platforms in the Cardano ecosystem, said it would wind down operations after nearly four years, citing a series of senior departures and rising operating costs. According to the platform, both co-founders, its chief operating officer and chief technology officer had already left earlier this year. A backend developer who stepped into the CTO role later also departed, leaving the company without technical capacity it said could not be replaced quickly enough to keep the platform running responsibly.

The shutdown clearly hit a nerve. In his livestream, Hoskinson warned that the second half of the year could bring further stress across Cardano DeFi.

“So this year is going to be very hard. The second half of the year for Cardano, we’re probably going to see more dApps in DeFi die and a consolidation happen. I’m not exactly sure what my role or place is to resolve this.”

His core argument was not that Cardano lacked resources, but that the network’s governance and funding architecture no longer gives him unilateral control over those resources. Hoskinson said he is often blamed for ADA’s market performance and ecosystem setbacks, while having no direct command over the treasury, protocol upgrades or brand infrastructure.

“You know, I keep getting criticized relentlessly online. People every single day post on my Twitter feed the price of ADA and blame me for it collapsing. And I’d really like to know, I just like to understand what my agency is here.”

Hoskinson Says He Lacks Control

The comments reflect a deeper tension in Cardano’s current phase. Cardano’s governance system was designed to shift control from founding entities to ADA holders, delegated representatives and other governance bodies. That structure gives the community more formal authority over treasury withdrawals and protocol decisions, but it also makes emergency coordination more difficult when key ecosystem companies are under pressure.

The same governance dynamic was visible days earlier when the Cardano Foundation canceled Cardano Summit 2026 in Singapore after its treasury funding proposal failed to reach the required two-thirds approval threshold. A revised request for roughly 7.8 million ADA received majority support but still fell short, while a smaller EMURGO proposal for a Cardano presence at TOKEN2049 Singapore was approved.

For Hoskinson, TapTools appears to have become a case study in the limits of founder influence after decentralization. He said the resources intended to grow and govern the ecosystem were assigned to separate entities, not to him personally.

“I don’t have any special powers with Cardano. I don’t have any governance keys. I don’t have any ability to even initiate a hard fork, much less a protocol parameter change. I don’t have access to the treasury. I don’t even own the trademark for the name Cardano.”

He continued: “All of the funding that was given for growing the ecosystem and governing the ecosystem was given to separate entities. And at the all-time high, it was billions of dollars. It was not given to me.”

The episode leaves Cardano facing an uncomfortable test. Its governance system is now powerful enough to reject major spending requests, including those from core ecosystem institutions. The harder question is whether it can also move quickly enough to preserve critical infrastructure during a market downturn without recreating the centralized dependency it was designed to remove.

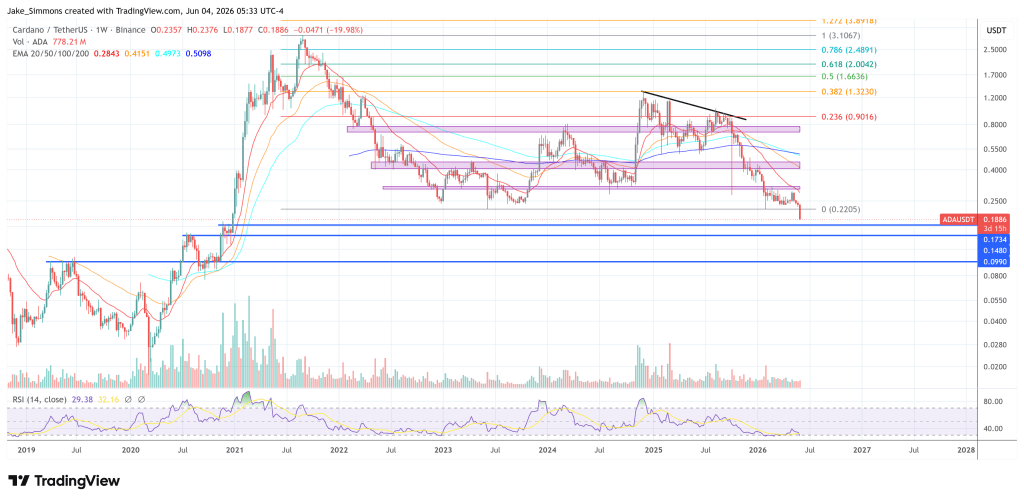

At press time, ADA traded at $0.1886.