Organisations around Cardano, Avalanche, Sui and IOTA have filed a joint response to the UK Financial Conduct Authority’s CP25/40 consultation, arguing that the rulebook should draw hard lines around “custody and control” and avoid sweeping non-custodial crypto activity into regimes designed for intermediaries.

The submission, led by the IOTA Foundation alongside the Sui Foundation, Cardano Foundation and the Avalanche Policy Coalition, is a targeted push on two areas the group says are most exposed to “scope, proportionality and technical interpretation” problems: staking and decentralized finance.

In a post on X, IOTA framed the core message as a scoping exercise as much as a policy one: “focus on custody & control, keep it proportionate, and support non-custodial, decentralized innovation for UK.”

Cardano, Avalanche, Sui And IOTA Warn Against Overregulation

The open letter expands that into a broader architecture: “A consistent theme across our feedback on both staking and decentralized finance is the importance of clearly distinguishing between infrastructure functions and intermediary functions. We recommend that regulatory obligations remain focused on entities that exercise custody, discretion, or commercial intermediation, while preserving the neutrality of public blockchain infrastructure.”

The letter adds that developers and infrastructure providers should be exempted: “[They] deliver software development, validation, communications, or other protocol-level services without controlling client assets or exercising unilateral decision-making are performing infrastructure roles rather than financial intermediation, and warrant a proportionate and differentiated regulatory treatment.”

That distinction matters, the group argues, because staking and DeFi aren’t single business models. They sit on a spectrum from fully custodial services where a firm safeguards assets and intermediates execution to protocol-native activity where users retain control of keys and assets.

On staking, IOTA’s X thread distilled the policy ask into a binary: “regulation must clearly distinguish custodial vs non-custodial/models.” It adds that custodial staking “where firms safeguard assets” warrants “appropriate retail disclosures, consent + record-keeping,” while “non-custodial/protocol-level staking (no control of user assets/keys) should not be swept into the same regime.”

The letter mirrors that framing and narrows it to where the risk sits: “Where staking is provided through a custodial arrangement, and the firm safeguards client assets and intermediates the staking process, we recommend applying the proposed requirements on information provision, key contractual terms, express prior consent for retail clients, and record-keeping.”

It then draws the line the signatories want the FCA to adopt: “For non-custodial and delegated staking arrangements, where firms do not control client assets or private keys, we recommend that such activities remain outside the scope of regulated staking activity, as this maintains proportionality and aligns regulatory obligations with the actual sources of risk.”

The second pressure point is the FCA’s concept of a “clear controlling person” in DeFi. IOTA’s post argues the term needs a “technical, objective definition,” warning that obligations should scale with “custody, discretion, and unilateral control; not with writing code, participating in governance, or providing neutral infrastructure.”

The open letter keeps the same structure: it accepts the FCA’s intent to capture cases where an identifiable party is “effectively carrying on regulated cryptoasset activities,” but pushes back on triggering regulatory status based on development and infrastructure. Instead, it urges the FCA to anchor expectations to “demonstrable, unilateral control over protocol operation, governance or economic outcomes,” particularly because DeFi “rel[ies] on self-custody, automated execution and open participation.”

IOTA positioned the argument as pro-scope, not anti-rules: “smarter scoping = better consumer protection where risk is real, plus legal certainty that keeps non-custodial innovation from being regulated out of existence.”

The letter closes on the same trade-off: obligations tied to “custody, discretion and unilateral control” would, the group says, “strengthen legal certainty, enhance consumer protection where it is most needed, and reinforce the UK’s position as a jurisdiction that understands the architectural realities of decentralized technologies.”

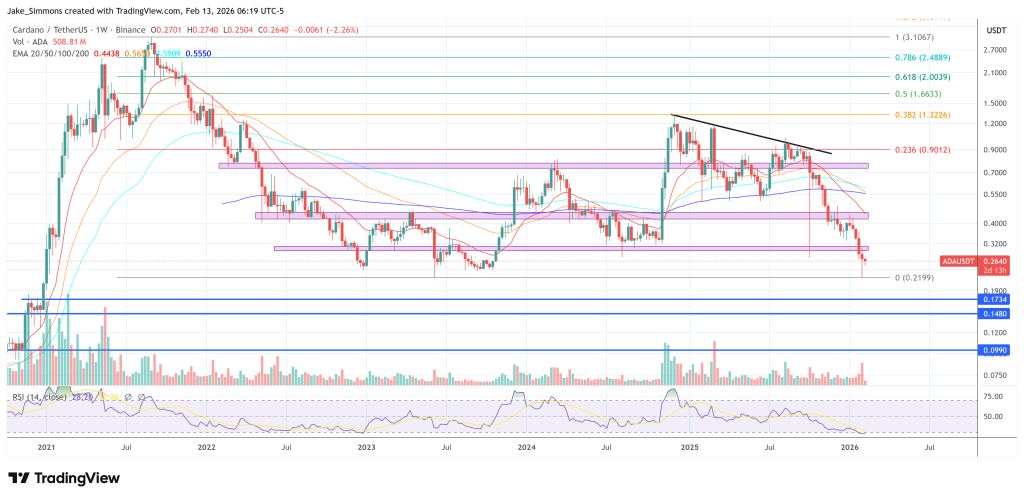

At press time, Cardano traded at $0.264.