Mastercard announced on June 3 that it will expand its global settlement infrastructure to support on-chain settlement using crypto via regulated stablecoins — enabling card transactions to settle 24 hours a day, seven days a week, across weekends and holidays for the first time in the network’s history, per the company’s official press release.

Six regulated crypto and stable coins are supported in the initial rollout: Circle’s USDC, PayPal’s PYUSD, Paxos-issued USDG and USDP, Ripple’s RLUSD, and SoFi’s SoFiUSD. Settlement will operate across eight blockchain networks — Ethereum, Solana, Polygon, Base, Arbitrum, the XRP Ledger, Canton, and Tempo — per the official announcement.

ARQ (formerly DolarApp), CBW Bank, Cross River, Lead Bank, and Nuvei are among the first partners to support stablecoin settlement optionality, with the initial rollout targeting the United States and Latin America before broader expansion through 2026.

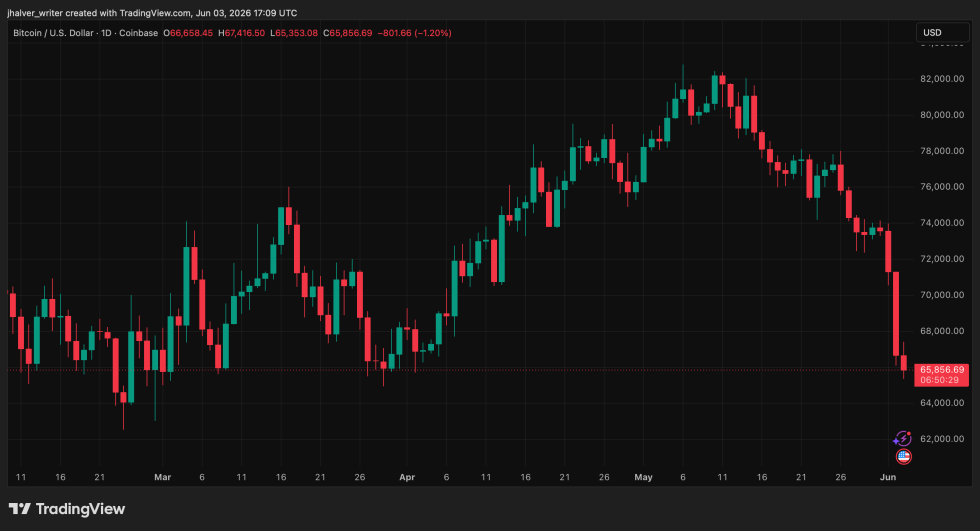

BTC's price trends to the downside on the daily chart. Source: BTCUSD on Tradingview

What Changes For Crypto — And What Doesn’t

The announcement is a settlement-layer development, not a consumer-facing product shift. Issuers and acquirers on Mastercard’s network can now choose to settle card-based transactions using regulated stablecoins on-chain rather than through traditional banking rails — or continue using existing fiat processes. Both options run in parallel. No cardholder needs to change how they pay.

What changes is the back-end infrastructure that clears and finalizes transactions between merchants, banks, and payment processors. That infrastructure can now operate on blockchain networks around the clock — removing the dead zones created by banking hours, weekend closures, and public holidays that have been a structural friction point in global payments for decades, per Mastercard’s press release.

Raj Dhamodharan, Mastercard’s Executive Vice President for Blockchain and Digital Assets, described the enhancement as expanding how partners manage liquidity while operating in an always-on digital economy, per the announcement. Ripple SVP Jack McDonald called it a landmark validation that blockchain technology is ready for the world’s most critical payment infrastructure, per Benzinga’s reporting of his statement.

This development marks a pivotal and historic moment for the nascent sector. The world’s second-largest card network opening its global settlement rails to six regulated stablecoins across eight blockchains — not as a pilot, not as a proof of concept, but as a live network-level enhancement — is the clearest institutional validation the stablecoin economy has received to date.

Cover image from Grok, BTCUSD chart from Tradingview