Original|Odaily Planet Daily(@OdailyChina)

Author|Wenser(@wenser 2010)

In September of last year, the battle over the Hyperliquid native stablecoin USDH once became a focal point in the industry; now, this once highly anticipated stablecoin has suddenly welcomed its own "exit moment."

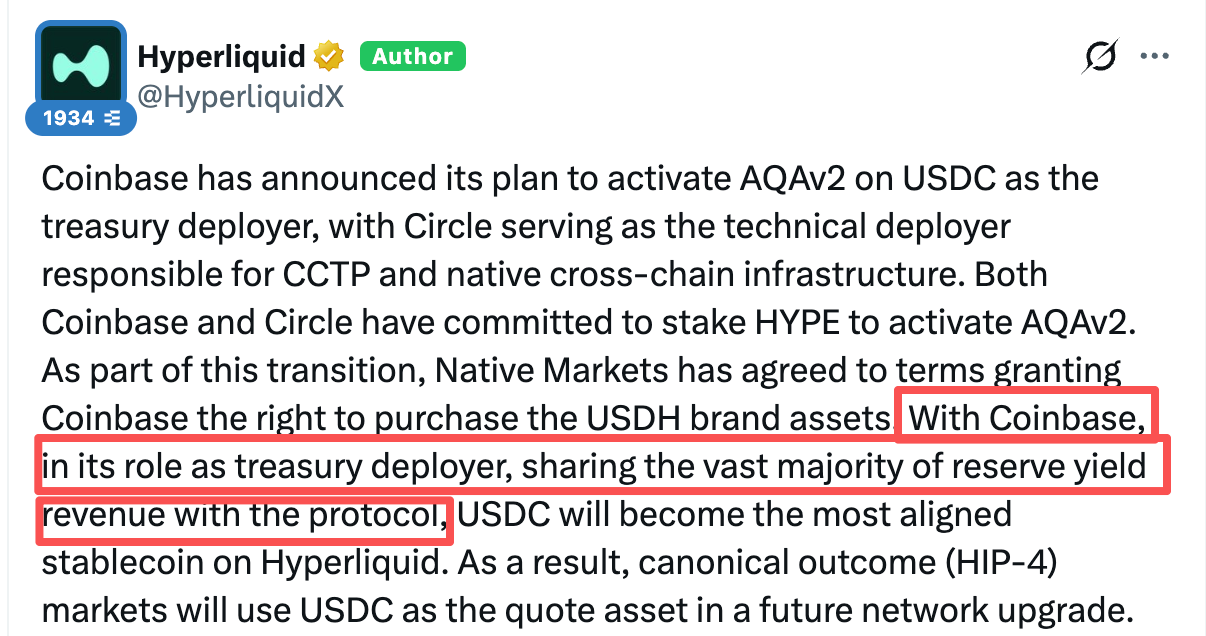

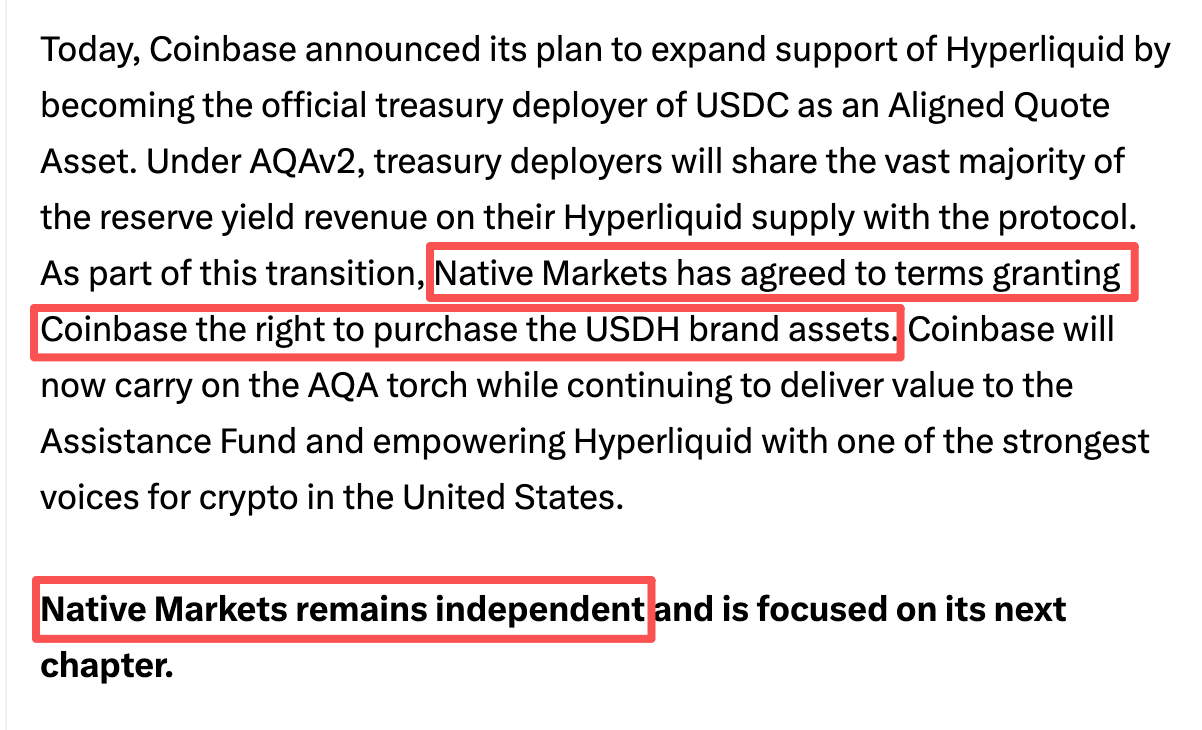

Last night, Coinbase announced it would become the official treasury deployer for USDC on Hyperliquid, while Native Markets, the issuer of the Hyperliquid native stablecoin USDH, granted Coinbase the right to purchase USDH brand assets. Subsequently, the USDH market will be gradually phased out, during which users can still convert USDH to USDC or fiat currency without transaction fees.

From this point on, the once-famous USDH has become an asset absorbed by Coinbase, while USDC is officially established as the official stablecoin and quote asset of Hyperliquid. Odaily Planet Daily will briefly analyze the details and subsequent impacts of this event in this article.

USDH Exits, USDC Rises: The Economic Calculations Behind $50 Billion

This grand play of the "Hyperliquid Ecosystem Stablecoin Battle" ultimately concluded with a win-win-win outcome for the three parties: Coinbase & Circle, Hyperliquid, and Native Markets, the USDH issuer.

Coinbase further deepened its integration with the Hyperliquid ecosystem through this move; Hyperliquid secured the majority of the revenue from USDC stablecoin reserves within its ecosystem; Native Markets, as the ultimate beneficiary of USDH, received its reward in the form of "selling the USDH brand assets."

Coinbase & Circle: Binding to Hyperliquid's On-Chain Economy, Continuously Increasing Investment in HYPE

Currently, the scale of USDC on Hyperliquid is approximately $5.164 billion, a year-on-year increase of 2 times.

As the official partner and revenue-sharing party for USDC, Coinbase's action undoubtedly aims to deeply integrate with the Hyperliquid ecosystem.

Additionally, according to official Hyperliquid announcement information, both Coinbase (funds deployer) and Circle (responsible for CCTP and native cross-chain infrastructure technical deployment) have committed to staking HYPE to activate AQAv2 (Aligned Quote Asset v2).

It is worth mentioning that in September last year, Circle had already purchased HYPE tokens, and its current HYPE token staking scale has increased to around 500,000.

Hyperliquid: Secures the Lion's Share of USDC Reserve Revenue, Enjoys the Convenience of Being a Coinbase Ally

As for the biggest winner of this cooperation, it is undoubtedly Hyperliquid as the foundational ecosystem.

According to the official announcement, Coinbase will subsequently share the majority (vast majority) of reserve revenue income with the Hyperliquid protocol. Although the specific split ratio has not been disclosed, if based on the previous USDH revenue-sharing mechanism, Hyperliquid will actually receive approximately 90% of the reserve revenue.

According to calculations by Hyperliquid community members, based on a scale of $4.7 billion and a 3.8% interest income rate, this revenue corresponds to approximately $160 million; in other words, it corresponds to a daily HYPE token buyback of about $440,000.

Furthermore, with the CLARITY Act passing the vote in the U.S. Senate Banking Committee, the deep integration between Hyperliquid and Coinbase also means that HYPE and Hyperliquid have gained a certain level of support in terms of U.S. regulation.

Native Markets: USDH's Historical Mission Accomplished

As the issuer of the Hyperliquid native stablecoin USDH, Native Markets might seem like the biggest loser in this "absorption event," but judging from its official statement, its ending can also be considered a "successful retirement."

On one hand, USDH provided a model and template for the revenue sharing of USDC between Coinbase and the Hyperliquid protocol; on the other hand, Coinbase likely directly acquired the USDH-related brand assets. The USDH stablecoin issued by the Native Markets team was essentially "acquired by Coinbase," thus providing the team with a certain economic return.

Subsequently, Native Markets also stated it would remain independent and seek developments in other areas.

After USDH's Exit, In a Win-Win-Win Situation, Only USDH Users Get Hurt

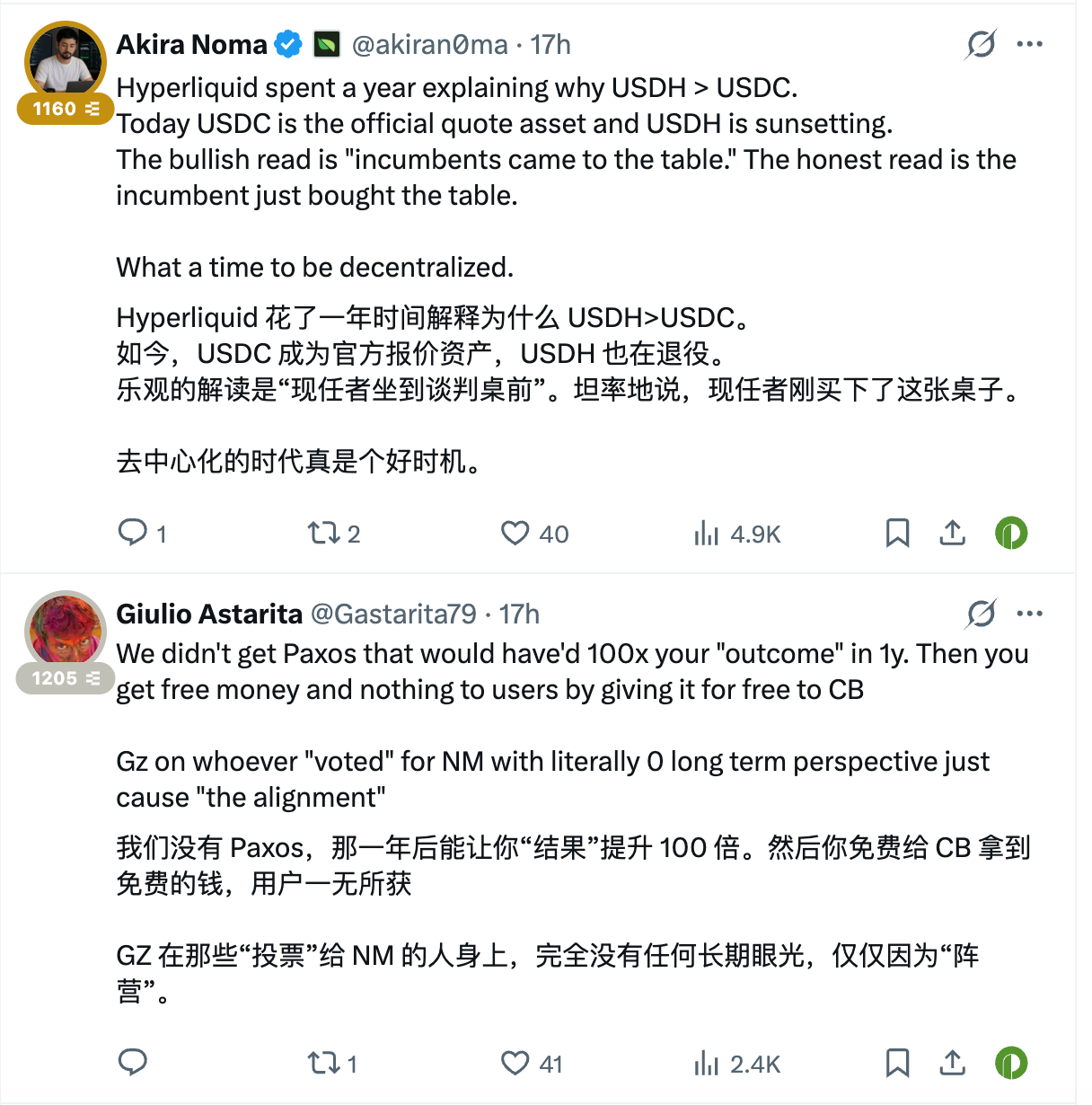

Of course, Native Markets' exit has not been met with universal "praise." Hyperliquid community users have also expressed disapproval of its so-called "sitting at the negotiation table" narrative.

Some believe that the exit of USDH signifies a complete regression of the decentralization era;

Others point out that during the original USDH stablecoin issuer vote, Paxos should have been chosen, as they at least considered users and stablecoin growth. Those who voted for Native Markets were merely aligning with factions and internal interests. Ultimately, users gained nothing. These remarks have garnered considerable agreement and support.

Thus, the drama from a year ago, filled with "dominant pursuit," "resistance against giants," has finally come to an end.

However, looking back now at the scene of Hyperliquid "shaking hands and making peace" with Coinbase and Circle is somewhat poignant and slightly ironic.

In the end, everything was merely about the distribution of interests, not the once-loudly proclaimed slogans of "for the community" or "for Hyperliquid."

Recommended Reading

Hyperliquid Stablecoin USDH Becomes the "Industry's Favorite," Giants Trigger Chaotic Battle for Distribution Rights

USDH Vote in Progress: "Prearranged Script," "Dominant Pursuit," "Stepping Down Bravely" Take Turns on Stage