Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

The pre-IPO (Pre-IPO) stock token market has just experienced a severe shock. The epicenter of this earthquake stems from two statements issued by two major AI companies, Anthropic and OpenAI.

Anthropic and OpenAI Successively Declare They 'Do Not Acknowledge' Unauthorized Sales

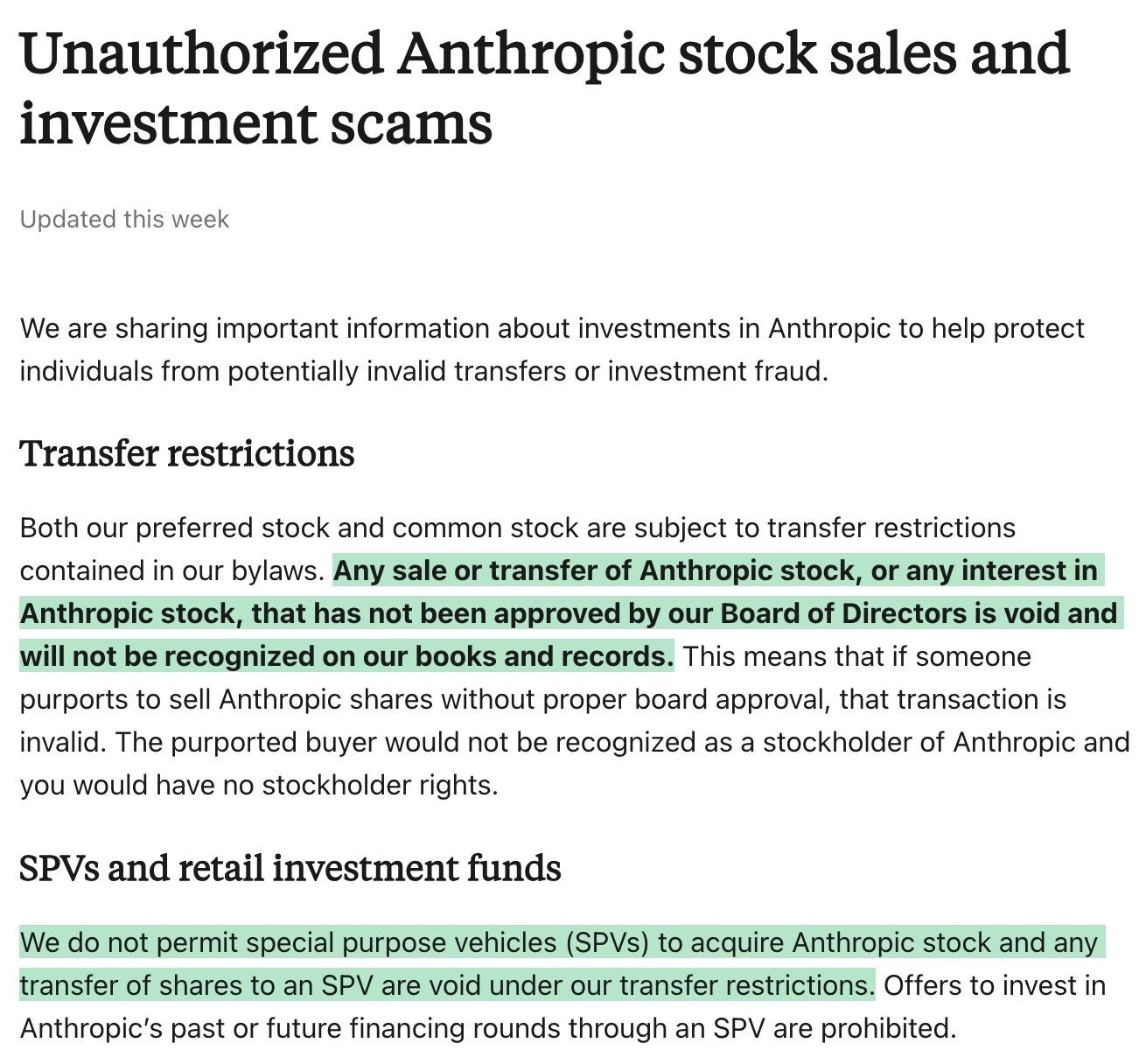

Today, Anthropic updated an official statement it released in February titled "On Unauthorized Sales of Anthropic Stock and Investment Scams".

Anthropic explicitly stated in the article: "Any sale or transfer of Anthropic stock that is not approved by our Board of Directors, or any disposition of economic interests in Anthropic stock, is invalid (note the term 'invalid') and will not be recognized on the company's books and records. This means that if someone sells Anthropic stock without board approval, the transaction will be deemed invalid. The purported buyer will not be recognized as a shareholder of Anthropic and will not enjoy any shareholder rights."

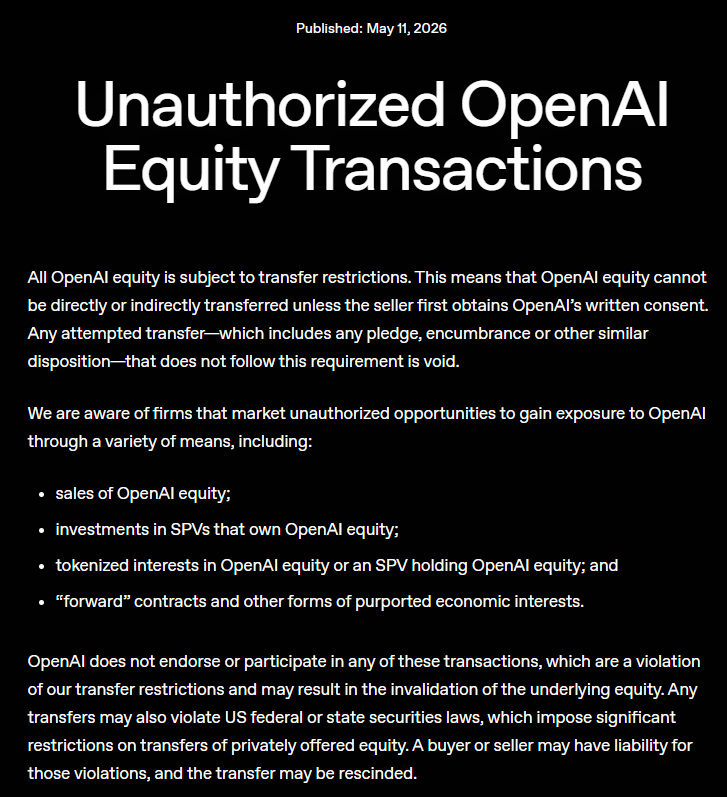

Shortly after Anthropic updated its statement, OpenAI also followed up with an announcement stating: "All equity is subject to transfer restrictions. No shares may be transferred, directly or indirectly, without the Company's written consent. Any sale without consent is not only unauthorized but also invalid."

In their announcements, both Anthropic and OpenAI explained that the companies' preferred and common shares are subject to transfer restrictions stipulated in their charters, meaning all stock transfers require board consent.

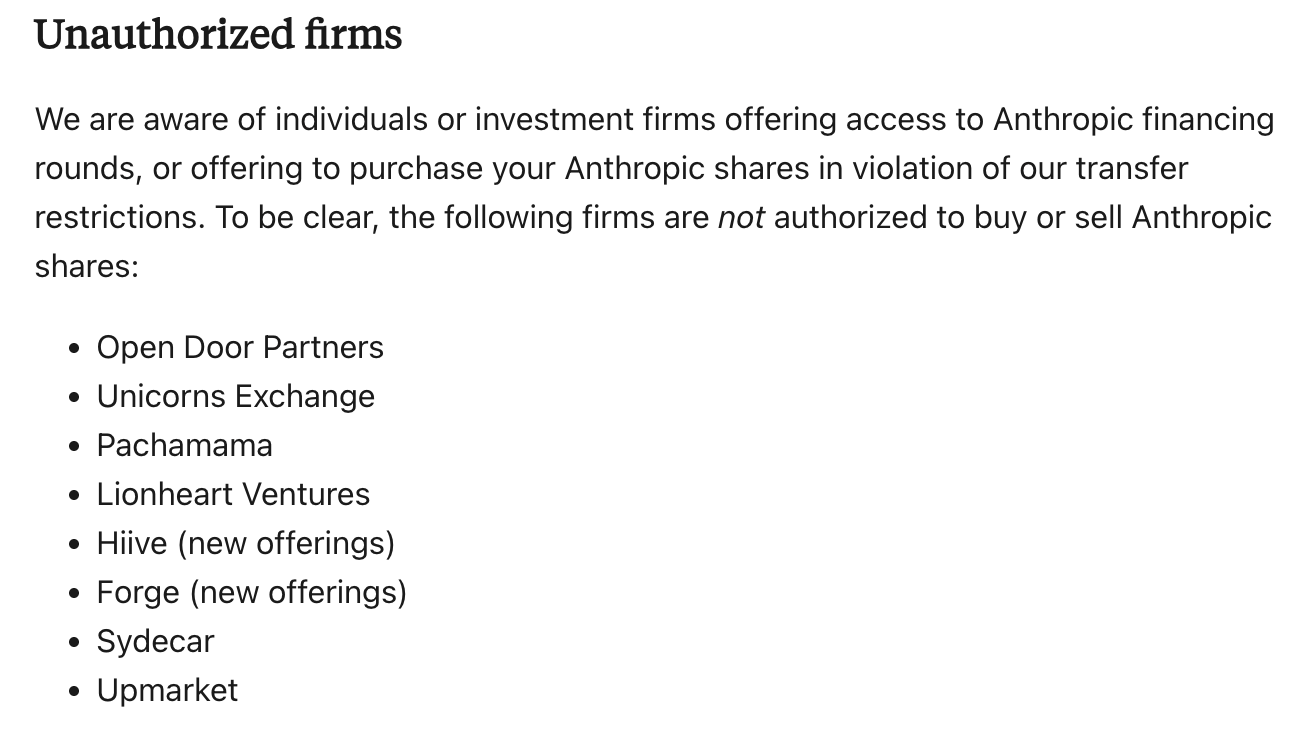

Anthropic particularly emphasized that the company also does not permit "Special Purpose Vehicles" (SPVs) to acquire its shares, and any transfer of shares to an SPV violates the company's transfer restrictions...... Certain investment funds may claim to provide indirect access to Anthropic stock, but these funds are likely attempting to circumvent transfer restrictions. Therefore, any third party claiming to sell Anthropic stock to the public — whether through direct sales, forward contracts, stock tokens, or other mechanisms — may be engaged in fraud or offering worthless investments due to Anthropic's transfer restrictions.

- Odaily Note: The image shows platforms named by Anthropic for unauthorized equity transfers.

What is an SPV?

To understand why this update has such a massive impact on the pre-IPO stock token market, one must first understand what an SPV is.

In traditional pre-IPO stock trading, directly transferring original shares is extremely difficult, restricted not only by company charters but also involving complex legal procedures. In this context, SPVs emerged.

An SPV is a legal entity established separately for a specific transaction or investment purpose, which can be understood as a 'shell company specifically used to hold a certain asset' — multiple investors can indirectly hold shares in a company or a type of asset by contributing capital to the same SPV, thereby achieving centralized ownership, lowering entry barriers, and optimizing legal and tax structures. SPVs are especially common in popular pre-IPO stock trades. As many star companies are often unwilling to directly introduce a large number of small shareholders, institutions typically first establish an SPV, which then uniformly invests in the target company.

For example, the so-called "early participation in Anthropic or OpenAI share subscriptions" in the market essentially involves investors first contributing capital to an SPV, which then uniformly acquires the unlisted equity of Anthropic.

Currently, most pre-IPO stock token platforms in the market (such as Prestock) adopt the SPV structure.

- The platform or its partners will register an SPV in a certain jurisdiction. The sole task of this SPV is to buy original shares of Anthropic in the secondary market (usually from employees or early investors);

- The platform then issues derivative tokens on-chain (such as ANTHROPIC or OPENAI), which are legally defined in agreements as "claims to the economic benefits of that SPV";

- In theory, these tokens are 1:1 pegged to the original shares; for every token issued, the offline SPV should hold a corresponding share of stock.

But now the problem is, Anthropic and OpenAI have explicitly stated they 'do not acknowledge unauthorized stock transfers'. This means if an SPV transfers stock without board approval (which is basically impossible to obtain), the stock held by that SPV may be considered invalid in the eyes of Anthropic and OpenAI — if the SPV's stock is invalid, then the "economic benefits" referenced by the on-chain tokens become worthless.

The Risk of SPV "Nesting"

A significant reason why Anthropic and OpenAI are so resistant to SPVs is that with the ongoing speculative frenzy around their pre-IPO stock tokens (Anthropic's pre-IPO valuation once soared to $1.4 trillion, far higher than its last funding round valuation), the risk of SPVs becoming over-financialized has begun to surface.

Among these risks, the "nesting" problem of SPVs is most noteworthy — many investors buying pre-IPO stock tokens believe they are purchasing company shares, but in reality, they only hold claims to the economic benefits of some SPV. Even more exaggeratedly, many SPVs do not directly hold Anthropic's original shares but are themselves nested two or three SPV layers down.

This "nesting" structure is, in fact, very dangerous.

- Legal Transparency Issues: With each additional layer, the authenticity of the underlying asset becomes more ambiguous. Investors find it difficult to confirm whether the SPV at the very bottom has actually received board approval for the transfer.

- Management Fee Exploitation: Each SPV layer charges management fees, performance fees, and dividends. After layers of skimming, investors' actual returns are severely diluted.

- Risk of Wipeout: If the equity transfer at any layer is deemed "invalid" by Anthropic, the entire value chain can collapse instantly.

Whether for reputation or investor protection considerations, Anthropic and OpenAI clearly do not want to see this situation.

Pre-IPO Stock Tokens Plunge, Contracts Remain Relatively Stable

Once the announcements from Anthropic and OpenAI spread, the market reacted immediately.

ANTHROPIC on PreStocks plunged sharply, once falling below $1,000, temporarily reported at $1,082 as of 12:00, down 20.62% for the day; OPENAI temporarily reported at $1,440, down 26.82% for the day.

Investors' panic is easily understood. Since Anthropic and OpenAI explicitly stated they do not acknowledge unauthorized holdings, the "rights" behind these tokens face the probability of becoming "worthless paper," and holders may face significant risks in confirming ownership and legal litigation costs.

Interestingly, while pre-IPO stock tokens were under pressure, another type of pre-IPO trading product performed relatively stably — pre-IPO contracts that rely entirely on market bilateral speculation. This is because such products do not inherently hold any real stock; the restrictions by Anthropic and OpenAI have no direct impact on them. They are essentially "bilateral bets" on the future IPO price, relying on price competition between buyers and sellers.

Future Trend Predictions

Facing Anthropic and OpenAI's "non-acknowledgment" stance, two contrasting voices have emerged within the industry.

Some believe the logic of pre-IPO crypto-stock trading is dead. If headliners like Anthropic and OpenAI take the lead in banning SPVs, other giants may follow suit. With the backing of equity rights being shaken, whether pre-IPO stock tokens still hold value is questionable.

However, others, including Rivet founder Nick Abouzeid, believe this is not a big deal. Trading pre-IPO stock tokens through unofficial channels is inherently a gamble; buyers should have been prepared for the possibility that the "company would not acknowledge" them from day one — what you lack is direct investment opportunities; obtaining such opportunities through other means always carries certain risks.

In summary, with the continuous expansion of pre-IPO stock token premiums and increasingly fervent market sentiment, the stance of Anthropic and OpenAI undoubtedly pours a bucket of cold water on the entire sector.

Over the past few months, more and more investors have begun to view pre-IPO stock tokens as a "low-barrier channel to participate in the growth of top AI companies." The valuations of some AI-concept pre-IPO stock tokens have clearly detached from reality, even experiencing frenzied speculation far exceeding the valuations of their last funding rounds. Against this backdrop, the public "debunking" by Anthropic and OpenAI is, in a way, redrawing boundaries for this wildly growing new market.

For speculators, this is a risk education; but for the industry's long-term development, the market may also need such a "de-bubbling" moment.