In a recent YouTube stream, data aggregator CoinGecko noted that altcoins have remained in a slump for a sustained period of time.

The platform also analyzed previous cycles, highlighting a recurring pattern—capital always rotates from Bitcoin into Ethereum and then into other altcoins once Bitcoin hits a new all-time high (ATH).

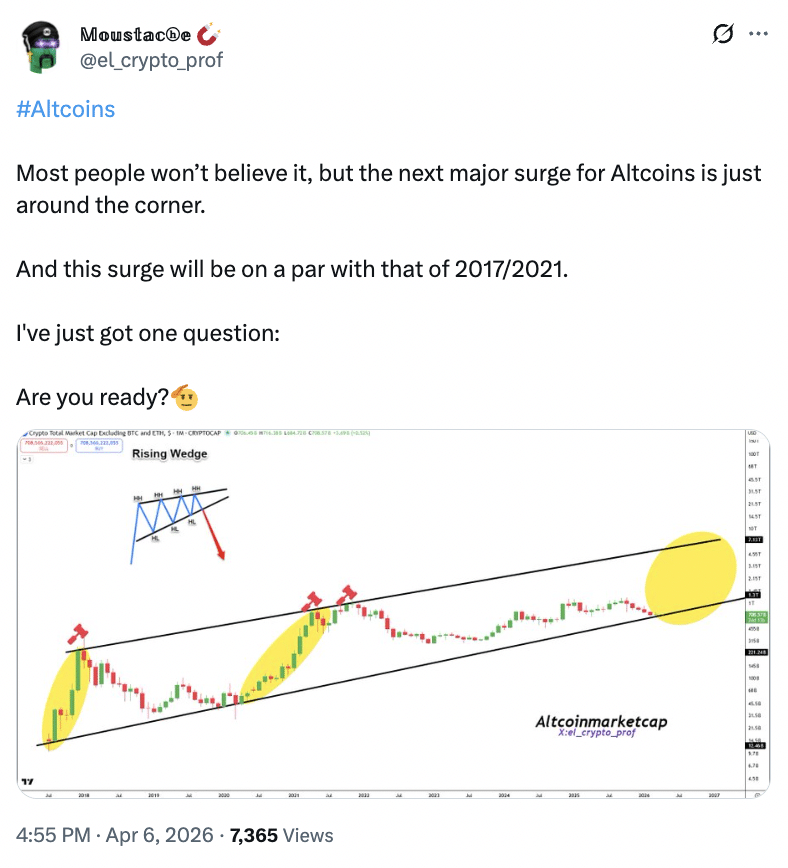

Bitcoin’s all-time high of $126,000 has come and gone, but altcoins are still in the gutter.

However, the current market isn’t following past patterns. Bitcoin reached its ATH of $126,000 back in October 2025, yet altcoins have still failed to outperform.

This change in pattern is notably because of the approval of exchange-traded funds (ETFs) and other related products approved in 2024. For perspective, in the new cycle, money is coming in, but mostly from institutions via ETFs, and “tends to stay concentrated in Bitcoin.”

So, with the biggest concentration lying in the hands of Spot Bitcoin ETFs, the altseason does appear like a far-fetched dream.

CoinGecko brought up this discrepancy, noting,

It doesn’t trickle down into smaller tokens the way retail flows used to.

The weight of the situation

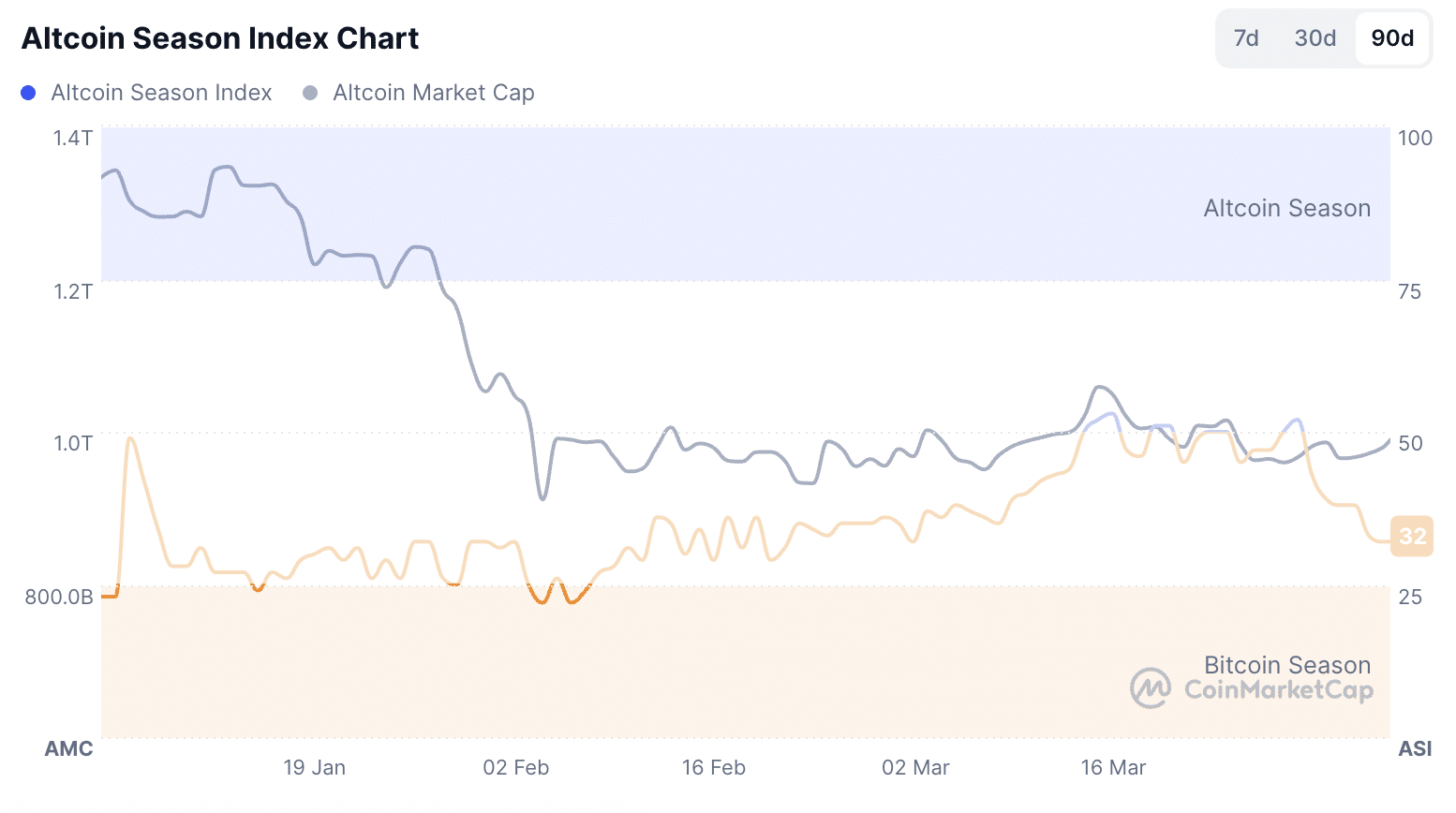

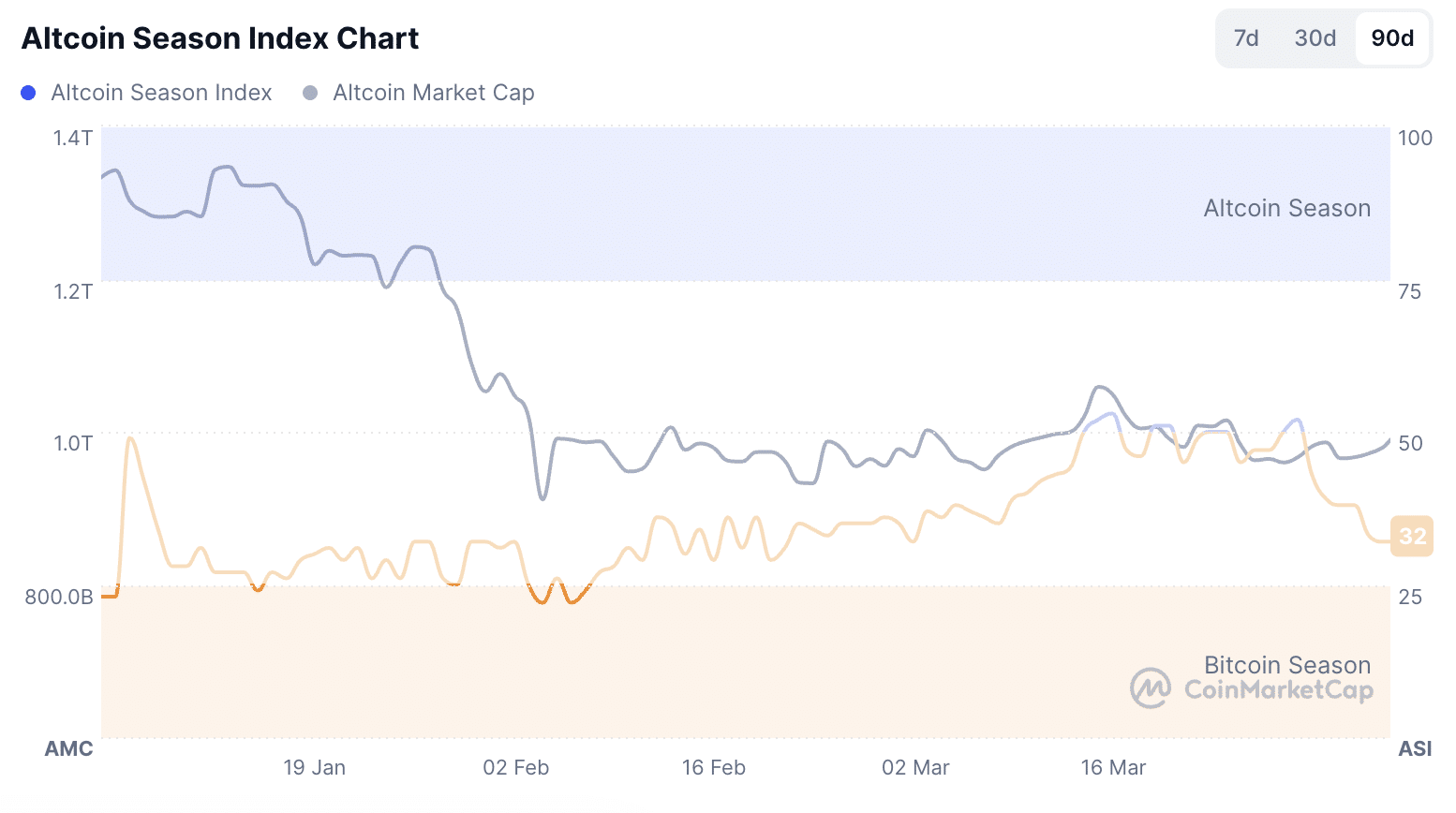

The CoinMarketCap Altcoin Index, sitting at 32 at the time of reporting, further suggests that the Bitcoin season is still in action.

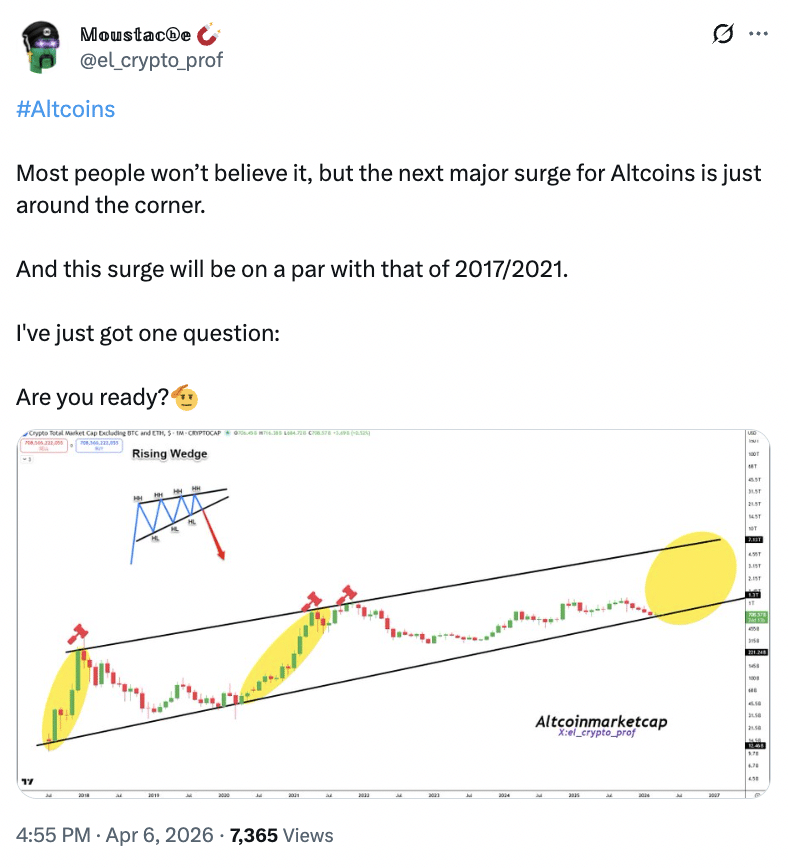

However, others in the crypto community still believe that the altcoin season is “just around the corner.”

If the altcoin season is actually about to happen, then Bitcoin dominance needs to weaken. Moreover, the top 10 altcoins trending in 90 days should include big names like Dogecoin, Solana, and Cardano.

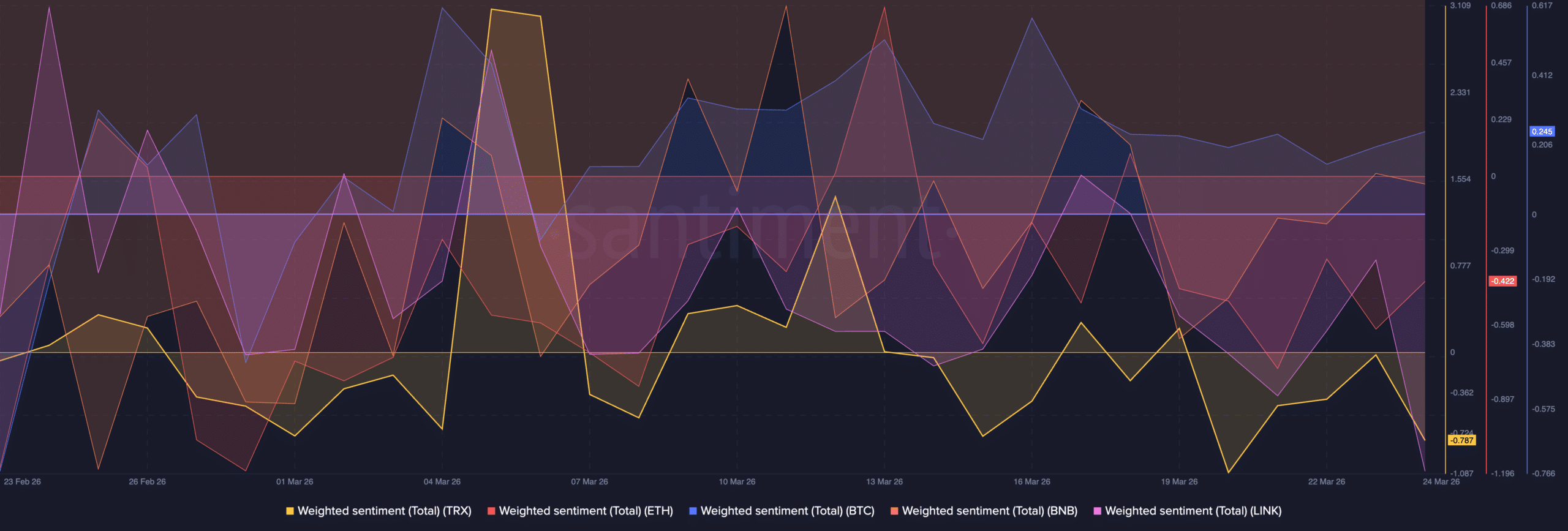

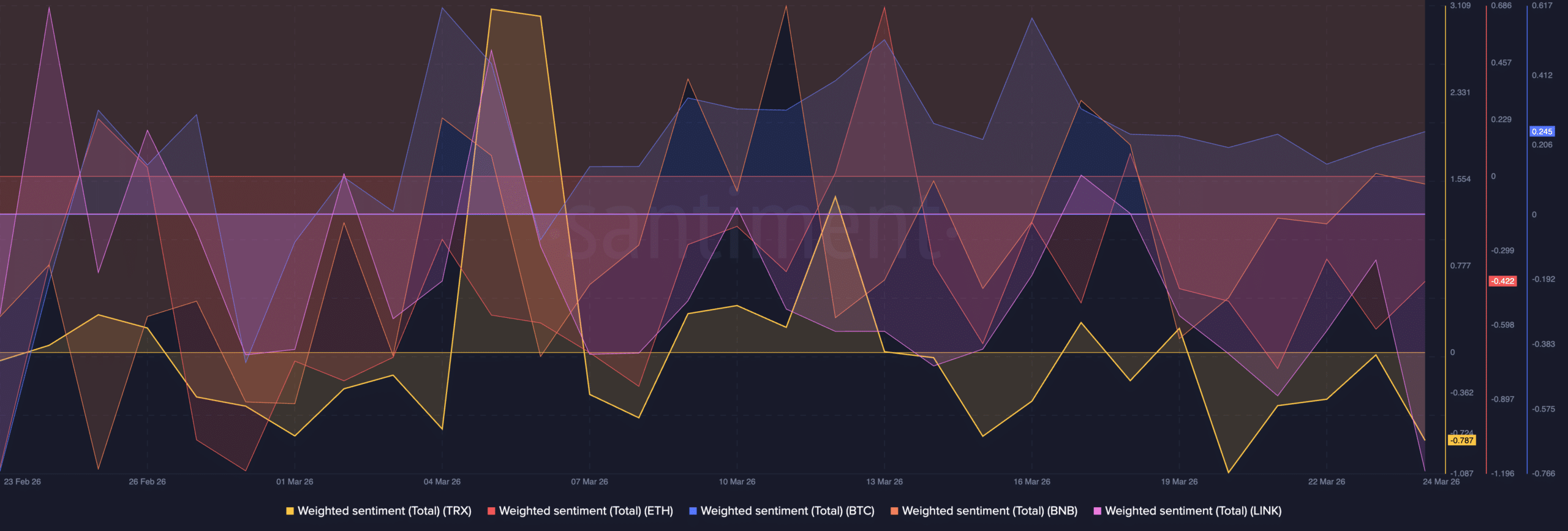

This was further confirmed by Santiment’s Weighted Sentiment analysis. The chart clearly shows that Bitcoin is the only token with positive Weighted Sentiment, whereas other altcoins are below the 50-level mark in the negative zone.

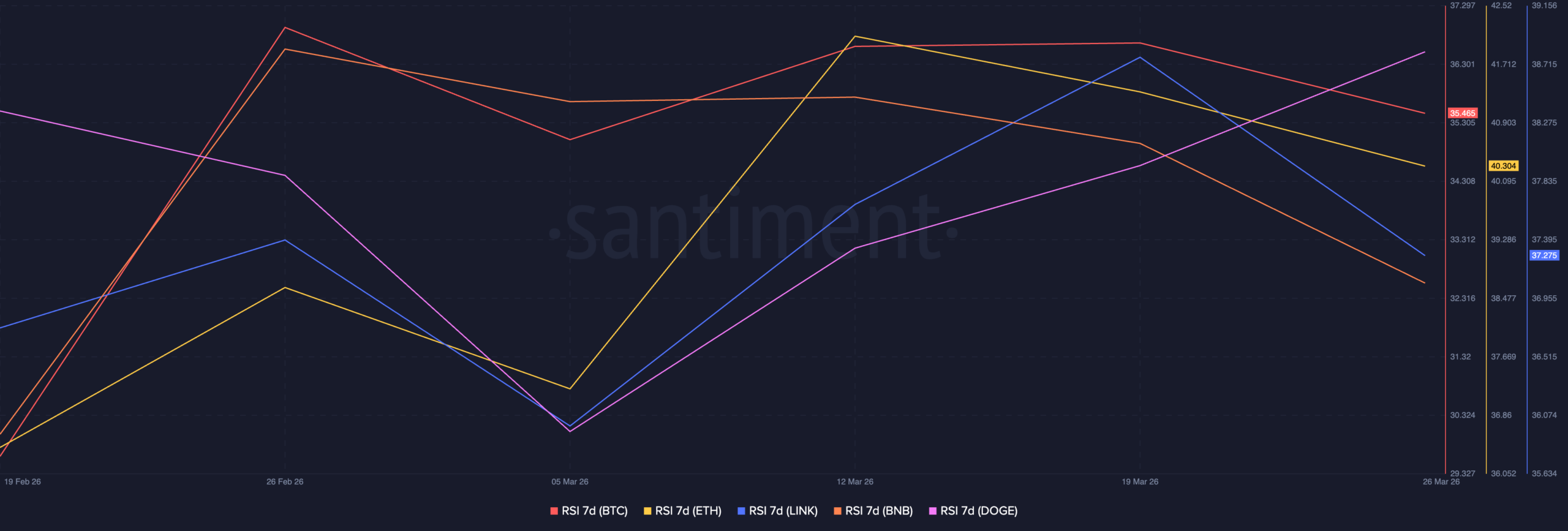

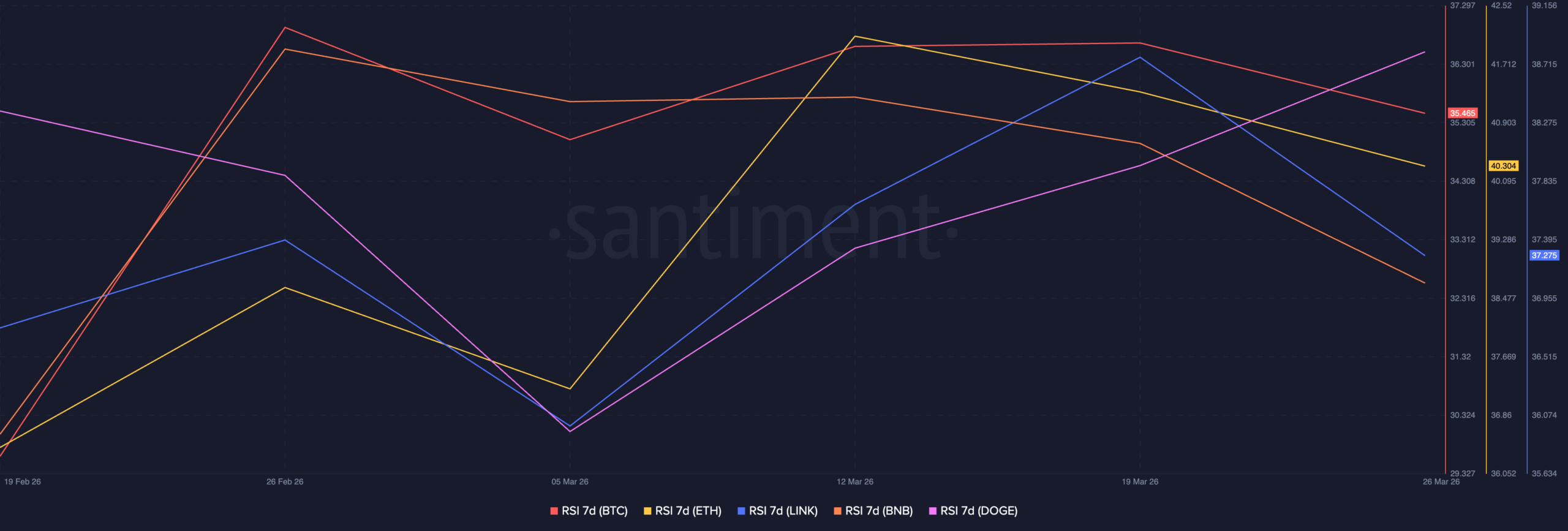

But the RSI of all the tokens, including Bitcoin, lying below the 50-level mark, aka the neutral level, suggests that the overall market sentiment is in the sellers’ hands.

This was further confirmed by AMBCrypto’s recent analysis, which also suggests that analysts are in favor of an altseason, but the on-chain data looks pessimistic.

Final Summary

- CoinGecko believes that altcoins are in the “gutter” after Bitcoin hit an ATH back in October 2025.

- However, hope for an upcoming altseason remains strong among investors.