Author: Jae, PANews

When Aave faced a massive withdrawal of hundreds of billions of dollars, Spark caught the overflowing liquidity.

The on-chain disaster triggered by cross-chain vulnerabilities in Kelp DAO and LayzerZero split the DeFi lending market into two distinct worlds.

The influx of "toxic" asset rsETH into Aave resulted in approximately $200 million in bad debt, causing a complete liquidity drain and a panicked exodus of hundreds of billions in funds.

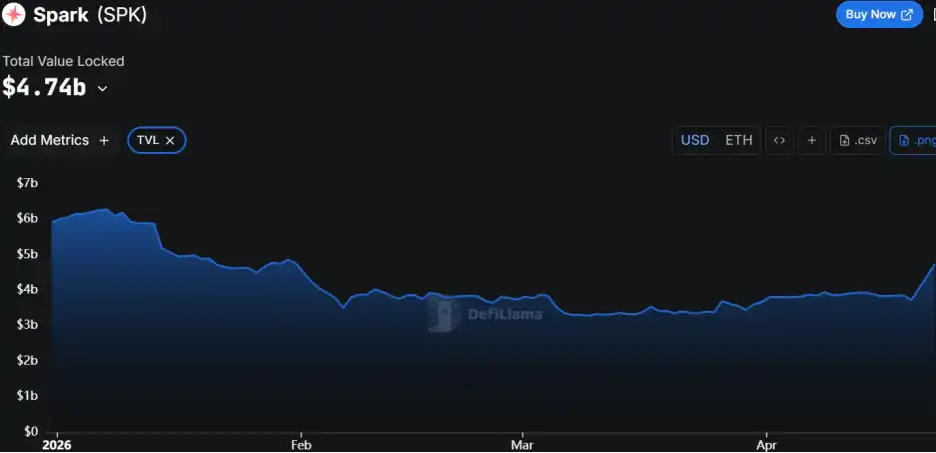

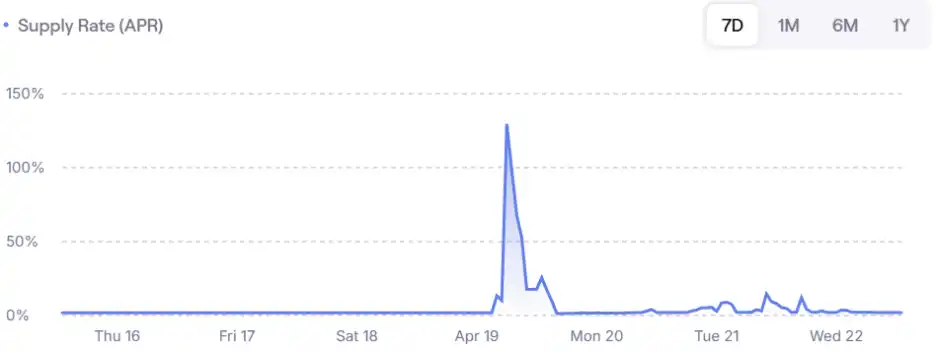

However, amid the widespread fear, another lending protocol giant, Spark, had its moment of glory. Its TVL (Total Value Locked) rapidly increased by $1.3 billion, and the ETH deposit rate once surged to 130%, making it the safe harbor of choice for whales transferring assets.

A black swan event has revalidated the true ruler of the DeFi iron throne.

Aave's Bloodbath of a Bank Run, Spark Seizes the Opportunity to Attract $1.3 Billion

The breach of rsETH's cross-chain bridge effectively pressed the pause button on Aave's entire lending market.

Hackers used fraudulently minted rsETH as collateral on Aave to borrow large amounts of WETH, draining the pool of clean assets and leaving behind a pool of bad debt.

Related reading: KelpDAO Cross-Chain Explosion, AAVE Becomes the "Patsy," Industry Calls for Risk Repricing

Panic spread like a virus: Over the past three and a half days, $151 billion has fled Aave, with total deposits dropping from $485 billion to $307 billion—about one-third of the funds have exited; WETH utilization rates on multiple chains hit 100% directly; depositors couldn't withdraw, and liquidators had no funds to borrow.

The most notable move came from Justin Sun, who quickly withdrew 65,584 ETH from Aave, worth approximately $154 million.

This "withdraw first" behavior created a herd effect in the market. For investors, no annualized yield could offset the panic of being unable to withdraw their principal.

Just as Aave became the hackers' liquidity exit, Spark became the users' escape route.

Spark's TVL反而 increased by $1.3 billion, with its total scale reaching $4.74 billion. This money is a vote of confidence cast by the market with real capital.

Due to the massive influx of borrowing demand into Spark, coupled with highly scarce liquidity, Spark's ETH deposit rate experienced a spectacular surge, once reaching an annualized level of 130%. This directly reflects the extremely high premium for safe assets.

Spark's ability to meet this demand is thanks to its unique ecosystem structure. Unlike Aave, it is the lending engine of the Sky ecosystem, backed by the vast USDS reserves. As Sky's liquidity outpost, Spark not only relies on external deposits but can also directly obtain stablecoin supplies through Sky's credit lines.

This "central bank-level" liquidity backing allows it to keep withdrawal channels open even during market turmoil.

Abandoning TVL Vanity, Spark Defies Trend to Delist rsETH

Spark avoided the rsETH pitfall due to a counter-trend decision made three months ago.

Same day, different fate. On January 29th, the two major lending platforms took opposite approaches in handling Liquid Restaking Tokens (LRTs).

Aave went full throttle. The protocol officially launched rsETH E-Mode, allowing users to conduct leveraged borrowing with a high collateral ratio (LTV) of 93%. Aave's goal was to attract an anticipated $1 billion inflow of rsETH, restore WETH utilization, and boost TVL and revenue.

Spark prudently retreated. The protocol passed a governance Spell to completely halt new supply of rsETH and gradually remove it from the asset list.

This move by Spark caused strong dissatisfaction among ETH循环杠杆 users, who often use repeated抵押 of stETH or rsETH and similar staking assets to arbitrage interest rate differentials. Spark's delisting forced them to migrate their positions, with most flowing to Aave, which had more lenient policies and lower interest rates.

At the time, the community questioned Spark's team for being "too conservative" or "abandoning growth." No one expected that this step might have saved the entire protocol later.

After the fact, Spark's Strategy Lead, monetsupply.eth, pointed out in a review that the decision to delist rsETH was based on a security-oriented tightening mechanism.

- Marginal Cost vs. Marginal Benefit: If the cost of maintaining a certain asset exceeds its risk-adjusted return to the protocol, such assets will be purged;

- Risk Exposure: rsETH had extremely low utilization on Spark, almost monopolized by the same wallet address, making risk difficult to disperse;

- User Preference Research: The sole whale user of rsETH expressed a willingness to actively migrate to more mature collateral like wstETH or weETH, providing an opportunity for the protocol to smoothly clean up the asset.

It was this decision-making discipline and transparency, which "does not blindly pursue TVL," that allowed Spark to avoid all potential losses that could have been caused by hackers exploiting rsETH.

Multi-Layered Risk Control System: Rate Limits + Interest Rate Buffer + Isolated Architecture

PANews believes that even if rsETH had not been delisted, Spark's architecture would have been sufficient to withstand such risks. Compared to Aave's pursuit of capital efficiency at the expense of safety redundancy, Spark has established a multi-tiered, in-depth defense system.

Spark implements strict deposit and borrowing rate limits (Rate-Limited Caps), meaning the amount of funds that can be deposited and borrowed within a fixed time increases gradually. Even if rsETH were still listed, an attacker could not deposit $290 million in collateral all at once as they did on Aave. This design forcibly limits the maximum risk exposure scale of a single event, hard-capping losses within an acceptable range.

Spark has long maintained relatively high interest rate ceilings. Under stable market conditions, higher borrowing rates, while deterring over-borrowing (if it's expensive to borrow, people borrow less), on the other hand attract more people to deposit (depositors earn more). The result is that the pool always retains liquidity, avoiding a situation where funds are "all borrowed out," preventing people from being unable to withdraw their money. Especially during market crashes, it avoids bank runs due to liquidity枯竭.

When pool utilization rises, Spark's interest rate curve slope becomes steeper than Aave's, which has two significant consequences:

-

Forced Deleveraging: High interest costs force borrowers to actively seek liquidity to repay loans.

-

Attracting Supplementary Liquidity: High deposit APY quickly attracts external arbitrage capital, thus resolving the deadlock of 100% utilization.

Spark's modular isolated architecture offers strong controllability in risk management. When handling high-risk synthetic assets like USDe, Spark has also adopted a prudent approach, isolating them in specific primary risk pools. This ensures that even if a specific asset encounters problems, it will not affect the main lending pools on the platform.

The great liquidity migration from Aave to Spark signifies a shift in risk preference from yield chasing to safety and stability.

Aave's hundred-billion-dollar outflow is a wake-up call for all protocols pursuing high capital efficiency. When safety margins are sacrificed, any minor external关联 risk can evolve into a global crisis for the protocol.

Spark's rise proves that in an uncertain market environment, prudent risk governance decisions and the implementation of a "risk-first" strategy are the moats with greater long-term value.