Original Author: KarenZ, Foresight News

On November 3, 2025, a security incident resulting in losses exceeding $120 million largely shattered the growth illusion of the veteran DeFi protocol, Balancer.

This was the largest security incident in Balancer's history. But the deeper wound lies not in that astronomical figure.

Looking at the financial data attached to Balancer's latest proposal, its fundamentals are already grim: the protocol's annualized fees are approximately $1.65 million, while the DAO's estimated annualized revenue is only $290,000, accounting for 17.5%.

The remaining funds flow to veBAL holders, core pools, the Balancer Alliance plan, and other parties. The entire system appears to be a continuously running "money printer," but it's actually "leaking" on both sides: on one hand, fees are split and lost through multiple layers; on the other hand, the BAL token has an annual inflationary release of approximately 3.78 million tokens, creating continuous selling pressure of about $580,000 at current prices — note that BAL's current fully diluted valuation (FDV) is only $11 million.

The annual operating budget is as high as $2.87 million, while the annualized revenue is only $290,000, resulting in a deficit of $2.58 million.

The DAO treasury (excluding BAL) holds only $10.3 million. At this rate, the treasury has less than 4 years left.

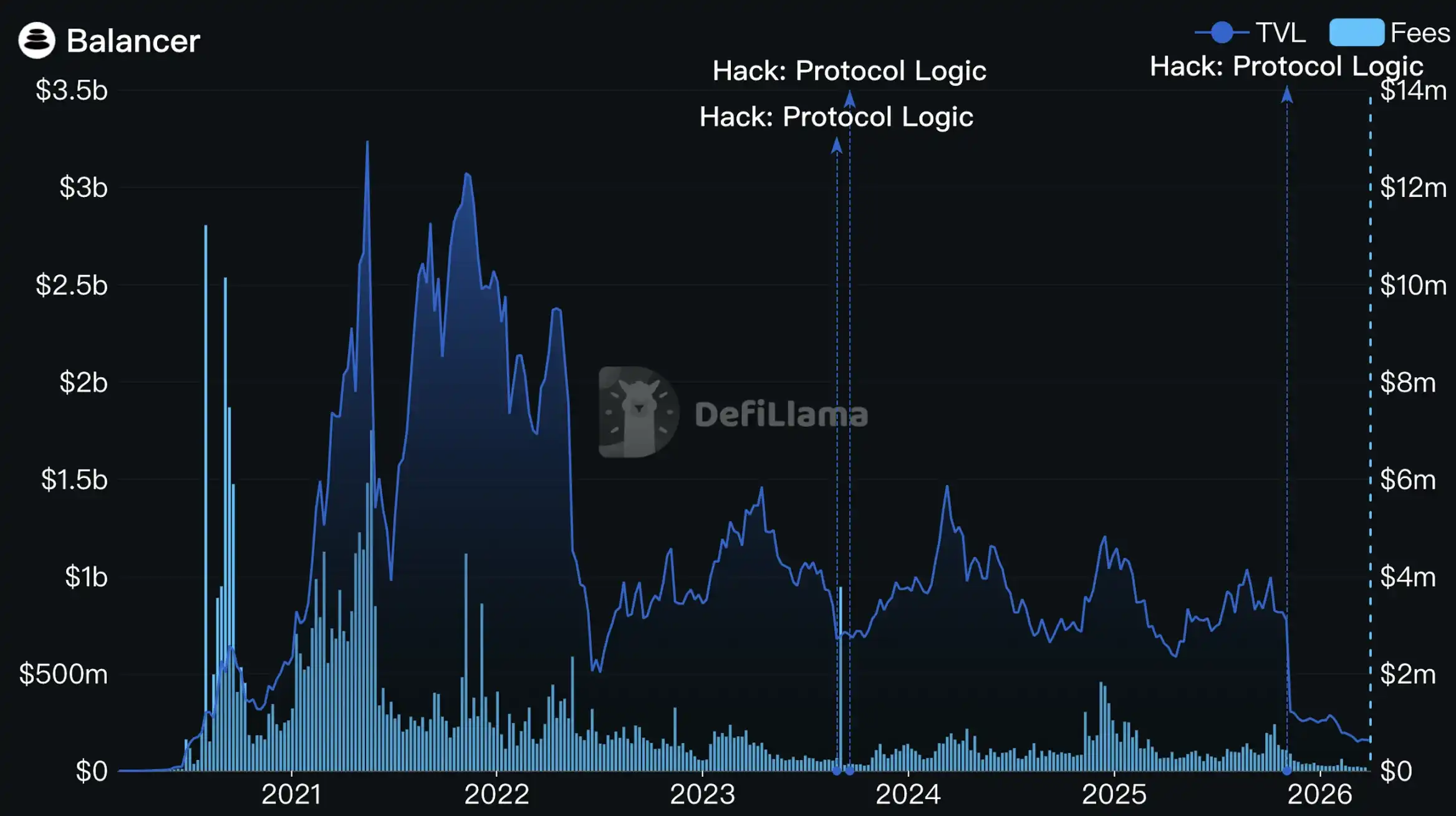

After the security incident, Balancer's TVL took a further hit. It dropped from $800 million to approximately $300 million, and then continued to decrease. The current TVL is less than $160 million. Recall that at its peak in 2021, Balancer's TVL had reached over $3 billion.

Source: DefiLlama

Balancer has officially reached a crossroads. On March 23, 2026, the Balancer core team simultaneously released two important governance proposals: a comprehensive overhaul of BAL tokenomics and an operational restructuring.

The core logic of these two documents combined can be summarized in one sentence: Abandon the growth model driven by token releases and shift towards sustainable operation driven by revenue.

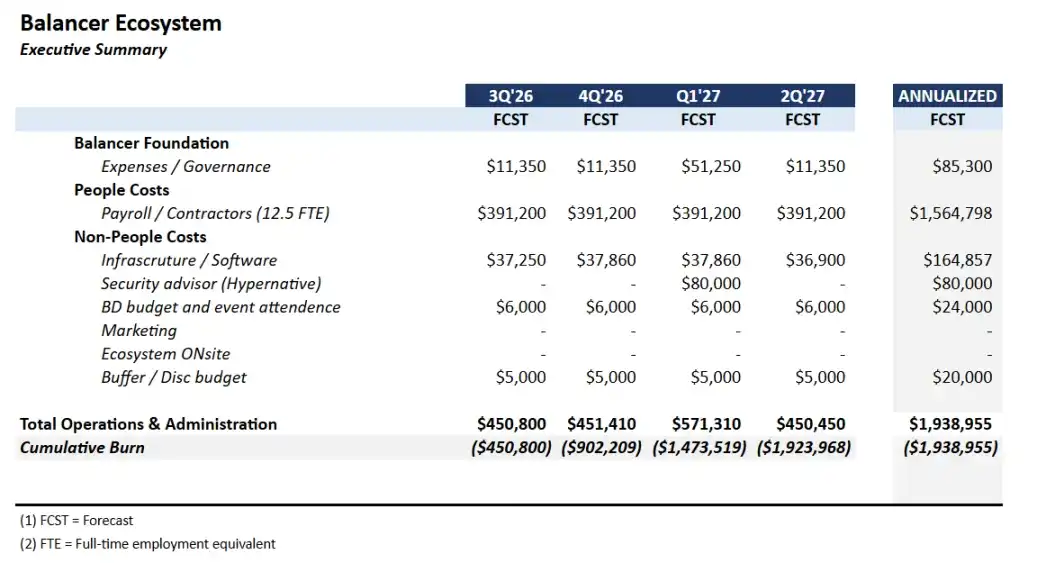

Operational Restructuring: Team "Slimming Down," Annual Budget Reduced by 34%

The proposal suggests formally dissolving Balancer Labs, with its core technical personnel transitioning to contractor roles and merging into Balancer OpCo Limited, which will continue to operate as the DAO's legal proxy entity.

The team size will be compressed from about 25 people to 12.5 full-time equivalents (including dedicated service providers like Beets, MAXYZ, etc.), and the annual operating budget will be reduced from $2.87 million to $1.9 million, a 34% cut.

The product lines are also being drastically narrowed. The team will focus resources on three products with validated commercial viability: Boosted Pools (flagship product), reCLAMM (to be relaunched after fixing vulnerabilities, possibly renamed), and LBP (token launch pools, operated opportunistically).

Other exploratory directions, such as ETF structured products, yield optimizers, and AI-driven liquidity tools, will only proceed subject to meeting "core KPIs".

On-chain deployments are also being scaled back. The current model of maintaining V2 and V3 on over 9 chains is unsustainable. The team explicitly retains four core chains: Ethereum, Gnosis, Arbitrum, and Base. Other deployments will be reviewed individually based on fee revenue and operational costs, and terminated if they do not meet standards.

Tokenomics Reform: A Complete Overhaul, Not Minor Tweaks

Stop BAL Emissions, Abolish veBAL

If the proposal passes, Balancer will terminate BAL token incentive emissions, with no transition period.

Simultaneously, the veBAL governance mechanism will be formally abolished. Holders will stop receiving any economic rewards after the final bi-weekly fee distribution. Their locked veBAL will become purely governance credentials, waiting to expire at the end of the lock-up period.

This is a painful decision, but the logic behind it is clear: the veBAL mechanism had a structural flaw from the start, being prone to oligopolistic control. Currently, Aura Finance (a veBAL meta-governance protocol) and whales hold significant voting power, making genuine community voices increasingly faint in governance. This mechanism not only failed to promote the protocol's healthy development but became a vehicle for circular economic games — protocol money flows to middlemen via incentives, and the middlemen's votes direct more incentives towards themselves.

If veBAL was once an experiment by Balancer borrowing from Curve's design, the team now frankly admits: the experiment is over, and the results did not meet expectations.

Regarding the termination of veBAL economic rights, Balancer stated it will provide a $500,000 compensation activity, distributed directly to veBAL holders as pure cash compensation.

All Fees Go to DAO Treasury, Reduce V3 Protocol Take Rate

All protocol fees — V2 swap fees, V3 swap fees, Yield fees, LBP fees — will thereafter flow 100% to the DAO treasury, abandoning the previous multi-party split mechanism.

Simultaneously, the V3 protocol fee take rate will be reduced from 50% to 25%. This means for the same transaction, liquidity providers (LPs) previously received 50%, but will now receive 75%.

These two moves seem opposite in direction but share the same underlying logic: the former eliminates the circular economy, allowing the treasury to obtain real usable funds; the latter increases LP attractiveness, trading lower platform fees for more organic liquidity and real trading volume.

The proposal estimates that post-reform, the DAO's annualized revenue could reach approximately $1.22 million, more than 4 times the current $290,000.

Exit Option: Burn BAL for Stablecoins at $0.16 per Token

The treasury will also allocate 35% of its assets (currently about $3.6 million) to a dedicated pool. This is not for actively buying BAL on the secondary market, but to open a "burn for stablecoins" channel: BAL holders can voluntarily send their tokens to a contract to be burned, receiving stablecoins of equivalent value at the NAV price (Net Asset Value, approximately $0.16 per token).

The window will open 12 months after the proposal passes and last for 12 weeks. Any unused stablecoins after the window closes will return to the treasury. The 12-month waiting period is designed specifically to allow holders whose veBAL unlocks gradually to participate.

At the time of writing, the BAL price is $0.1548, below the NAV price. Offering an exit at the NAV price provides a more dignified option for those wanting to leave than a secondary market stampede.

If this channel is fully utilized, it would burn approximately 22.7 million BAL tokens, about 35% of the circulating supply, which is 6 times the current annual inflation emission.

9-Year "Runway": Is It Enough?

If both proposals pass, the team's projected financial model is as follows:

DAO annualized revenue ~$1.22 million (assuming TVL recovers somewhat after V3 fee reduction), annual operating expenses $1.9 million, buyback expenditure ~$3.6 million, plus the $500,000 veBAL compensation.

After completing the buyback and compensation, the treasury would still have approximately $6.2 million remaining. The annual funding gap would narrow from about $2.6 million to $700,000, giving a theoretical survival period of nearly 9 years.

For a DeFi protocol, 9 years is enough to span a full industry cycle.

But this model is built on optimistic assumptions: that reducing the V3 protocol take rate will indeed attract more organic TVL; that the slimmed-down team can truly support daily protocol operations, security maintenance, etc.; and that core products (especially reCLAMM) can successfully attract the market again after repairs.

If any link underperforms expectations, the 9-year survival period will shorten rapidly. The team itself explicitly states that if DAO monthly revenue falls below $60,000 for 3 consecutive months, a revised plan must be submitted to the community.

For Balancer, this is a nearly all-or-nothing reform. Abandoning the once-proud veBAL mechanism, abandoning the complex multi-party split structure, and returning to an extremely simplified origin: let real transaction fees drive protocol survival, not newly minted tokens maintaining false prosperity.

Whether this desperate reform will work ultimately depends on the market and time, awaiting long-term observation.