Author: Nicky, Foresight News

Original Title: Is U the Stablecoin Binance Needs?

On January 13, Binance announced the listing of United Stables (U) and opened spot trading pairs for U/USDT and U/USDC, simultaneously launching zero-fee activities for these spot and leverage trading pairs. Within 30 minutes of the listing, the trading volume exceeded $4.5 million.

Against the backdrop of a highly mature stablecoin landscape and a continuously tightening regulatory environment, Binance's decision to list a new dollar-denominated stablecoin at this time carries significant implications. Since the gradual phase-out of BUSD, the compliance costs and regulatory pressures faced by centralized exchanges directly issuing stablecoins have significantly increased, while the demand for stable assets in trading, DeFi, and on-chain settlement scenarios has not diminished. How to introduce a stablecoin that is highly synergistic with its ecosystem without directly assuming issuance responsibilities has become a practical issue that exchanges must address.

The emergence of United Stables (U) may precisely meet this need. U is issued by the independent legal entity United Stables Limited, with Binance not being its legal issuer. However, the stablecoin has been rapidly integrated into BNB Chain, Binance Wallet, Binance Exchange, and multiple ecosystem protocols, making it highly tied to the Binance ecosystem in terms of usage.

Binance not only provides spot and leverage trading pairs for U but also simultaneously launches zero-fee activities to create conditions for its rapid establishment of liquidity and usage depth in the early stages.

On December 18, 2025, Binance founder CZ mentioned the latest progress of U during the "2025 Year-End Q&A AMA" hosted by BNB Chain, stating that it "has certain potential." However, the project has not disclosed any financing progress, and YZi Labs has also not disclosed relevant investment information.

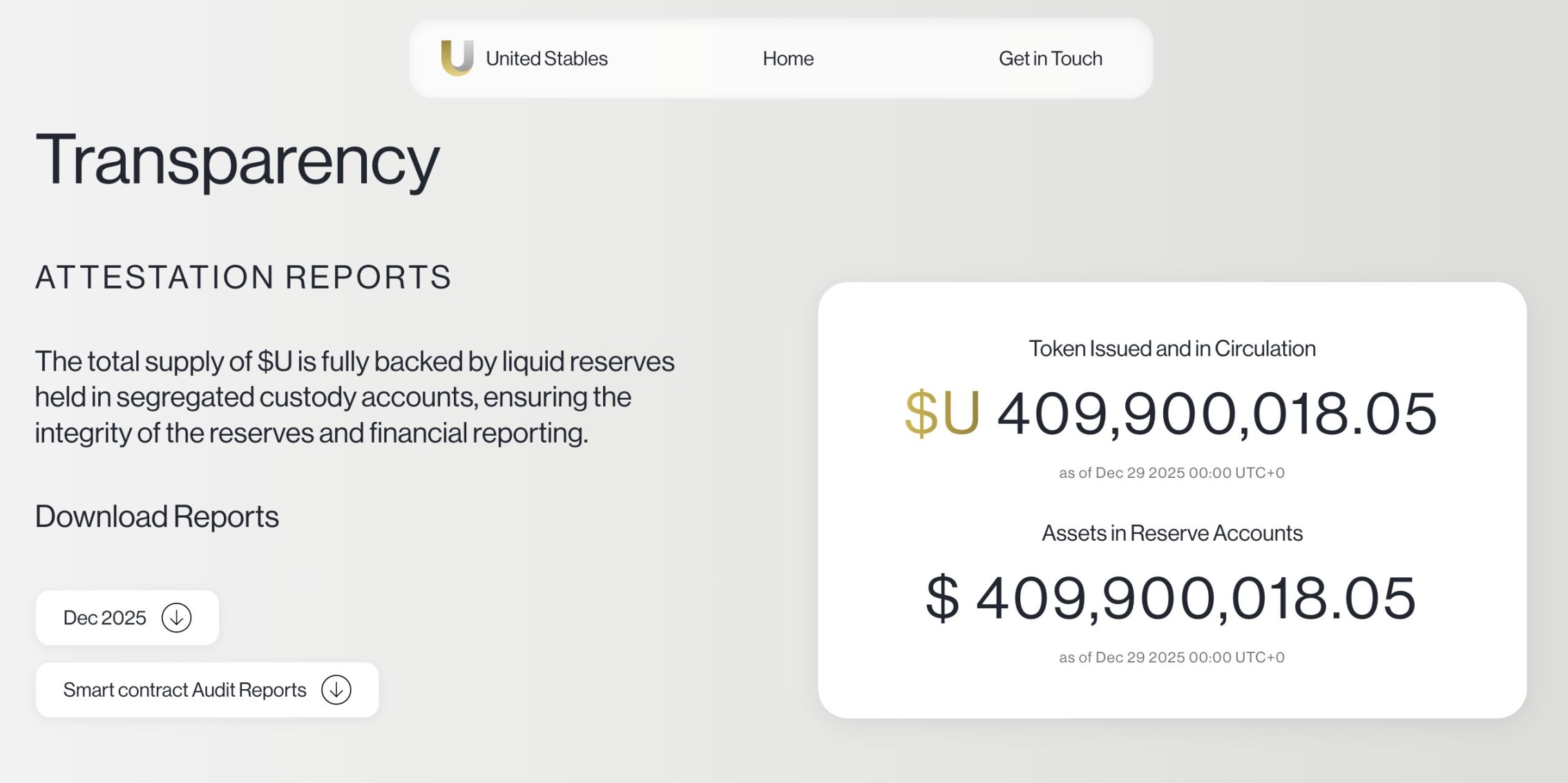

United Stables (U) is issued by United Stables Limited, a company registered in the British Virgin Islands (BVI). According to the project's official website, U is pegged to the US dollar and adopts a 1:1 reserve backing mechanism. Reserve assets are custodied through an independent trust structure to achieve legal isolation from the issuer's assets. Fiat reserves are held in compliant banking institutions, while digital asset reserves are custodied by licensed custodians.

Previously, the digital asset custody platform Ceffu issued the latest custody balance proof for the project on December 29, 2025, while PeckShield has issued a smart contract audit report.

For comparison, the reserve management models of current mainstream stablecoins vary. Tether (USDT) is issued by Tether Limited, with its reserve assets primarily consisting of US Treasury bonds, money market instruments, reverse repurchase agreements, and cash. These assets are held by multiple financial institutions and custodians, and reserve proof reports issued by third-party accounting firms are regularly published. Circle (USDC), on the other hand, manages its reserves through regulated bank accounts and US-registered government money market funds, continuously disclosing reviewed or audited reserve reports.

It is important to note that United Stables Limited explicitly states on its official website that U has not been registered or licensed under the EU's MiCA, Hong Kong's "Stablecoin Ordinance," the US GENIUS Act, or any relevant US or EU securities or stablecoin regulatory frameworks. This means the stablecoin is currently not included in the regulatory systems for stablecoins in major jurisdictions.

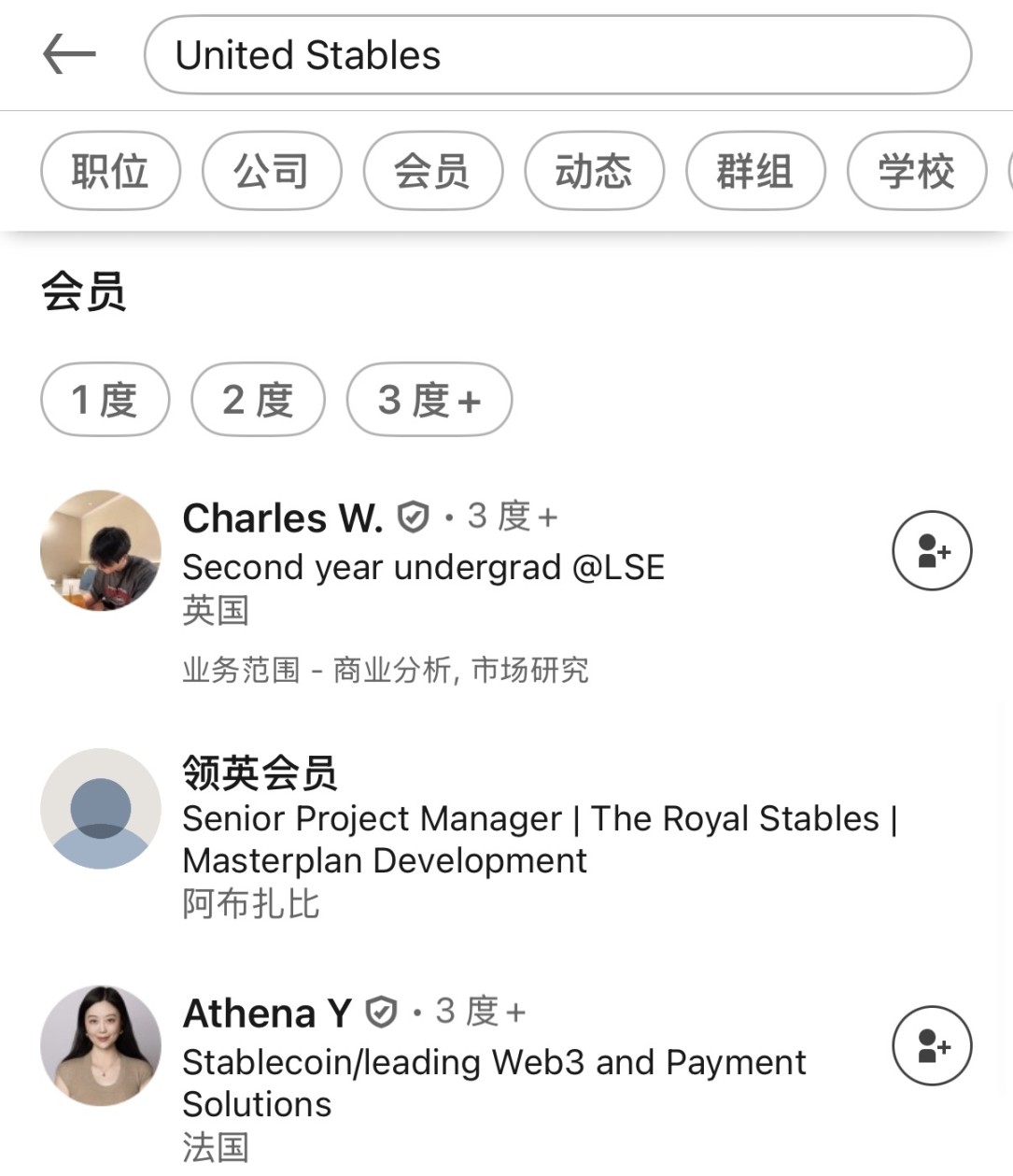

Public information shows that its core members include Athena Y and Charles W., among others. Athena Y is currently the CEO of United Stables, previously the co-founder of the payment platform Wello, and has served as the head of Binance's NFT business and as the CEO of the institutional digital asset custody platform Ceffu. Charles W. is currently studying at the London School of Economics (LSE) and participates in the project's community communication and external collaboration as an intern at United Stables. His past experiences include internships at institutions such as Goldman Sachs and Citadel.

Further background checks on the project reveal that, apart from the public information about the CEO, United Stables has not systematically disclosed a complete management team structure, including key positions such as compliance, risk control, finance, or reserve management.

In terms of product positioning, U does not describe itself as a direct replacement for mainstream stablecoins like USDT or USDC but rather attempts to serve as a "unified liquidity layer." Its core idea is to use fiat or mainstream stablecoins for minting, providing a unified settlement and circulation vehicle for different stablecoins when used on-chain, thereby reducing the operational friction costs across protocols and scenarios. The official documentation also mentions that U's target use cases include exchanges, DeFi, payment networks, and AI automation agents, among others.

According to on-chain data, as of the time of writing on January 13, the total supply of U is approximately 410 million tokens, with nearly 14,000 holder addresses and over 1.8 million cumulative transfers.

In terms of ecosystem progress, U has been rapidly integrated into multiple applications and protocols centered around BNB Chain after its launch. On December 18, 2025, HTX listed U and opened deposit and withdrawal services, while Aster simultaneously opened the U/USDT trading pair. Binance Wallet also supported trading on BNB Chain and Ethereum networks on the same day.

On the same day, Four.Meme announced that U would be one of the stablecoins used for fundraising and trading on its platform. However, current on-chain data shows that the overall scale of Meme tokens using U as their liquidity remains limited, with UDOG leading with a market capitalization of approximately $900,000, though it was not launched on the Four.Meme platform.

In DeFi, Lista DAO has launched U vaults and multiple lending markets. As of the time of writing on January 13, the deposit scale of the U Vault is approximately 3.51 million tokens, with an annualized yield of about 3.3%. In the payment sector, AEON announced a collaboration with United Stables. Its AEON Pay already supports offline扫码 payments using U and has adopted U as a settlement asset for x402 AI-native payment and automated trading scenarios on BNB Chain.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush