Author: Momir @IOSG

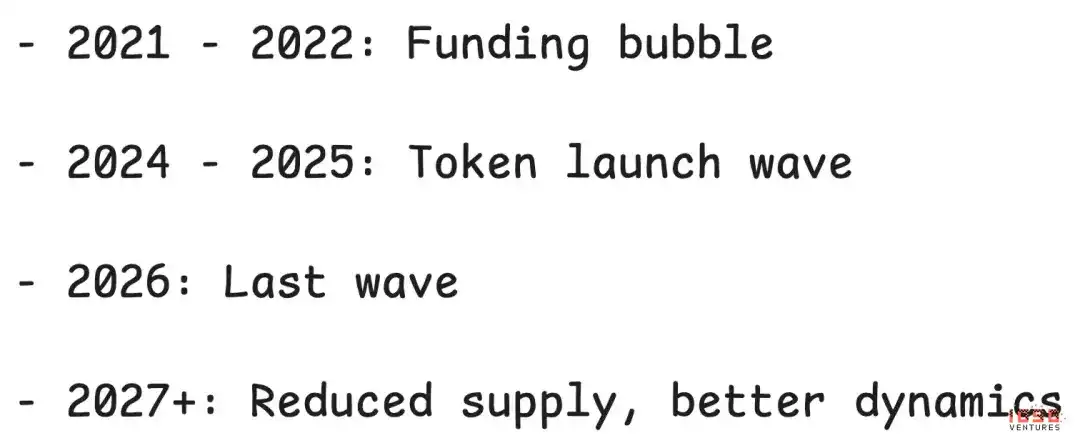

The altcoin market has experienced its toughest period this year. To understand why, we must go back to decisions made years ago. The financing bubble of 2021-2022 spawned a batch of projects that raised substantial funds. These projects are now issuing tokens, leading to a fundamental problem: a massive supply is hitting the market, while demand is scarce.

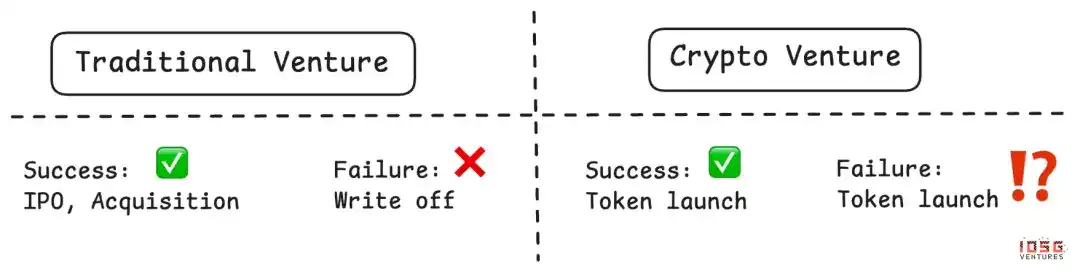

The issue is not just oversupply; worse still, the mechanisms that created this problem have remained largely unchanged. Projects continue to issue tokens regardless of product-market fit, treating token issuance as an inevitable step rather than a strategic choice. As venture capital dries up and primary market investments shrink, many teams see token issuance as the only financing channel or a way to create exit opportunities for insiders.

This article will analyze the "lose-lose-lose-lose dilemma" that is unraveling the altcoin market, examine why past repair mechanisms have failed, and propose potential rebalancing ideas.

1. The Low Float Dilemma: A Four-Way Losing Game

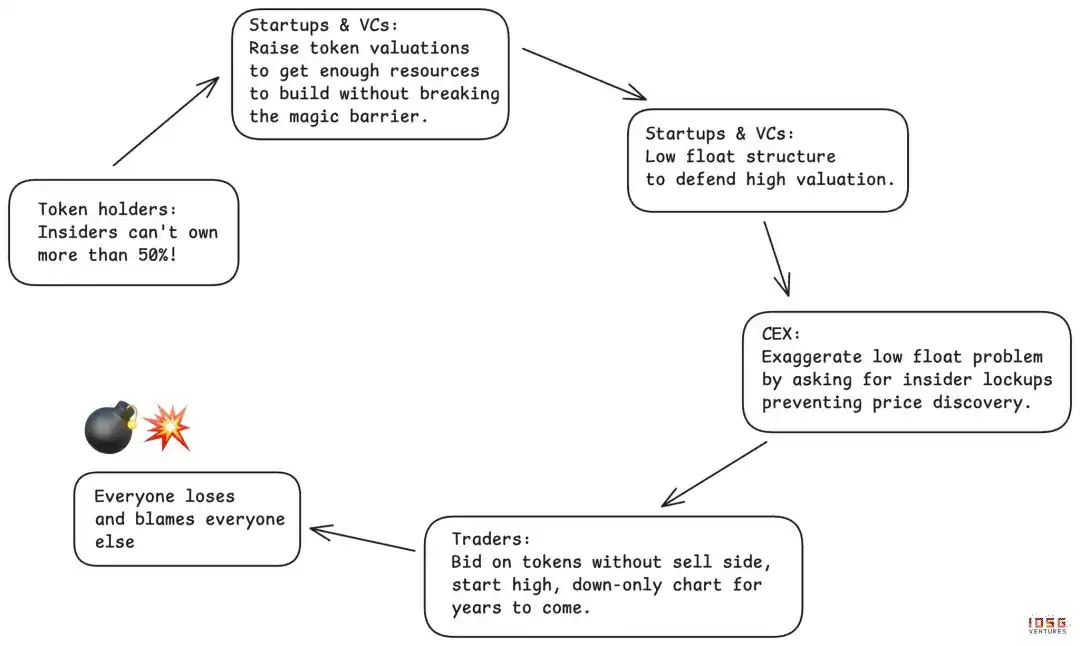

Over the past three years, the entire industry has relied on a severely flawed mechanism: low float token launches. Projects issue tokens with extremely low circulating supplies, often only a single-digit percentage, artificially maintaining a high FDV (Fully Diluted Valuation). The logic seems reasonable: low supply should stabilize the price.

But a low float doesn't stay low forever. As supply is gradually released, the price inevitably crashes. Early supporters become the victims instead. The data shows that most tokens have performed poorly since listing.

The most cunning aspect is that the low float creates a situation where everyone thinks they are benefiting, but in reality, everyone is losing:

- Centralized exchanges (CEXs) thought they were protecting retail investors by demanding low floats and strengthening control, but instead incurred community resentment and poor token performance.

- Token holders originally believed "low float" would prevent insider dumping, but ended up with neither effective price discovery nor protection, instead seeing their early support backfire. When the market demanded that insider holdings not exceed 50%, primary market valuations were pushed to distorted levels, forcing insiders to rely on low float strategies to maintain superficial stability.

- Project teams thought they could sustain high valuations and reduce dilution through low float manipulation, but once this practice became a trend, it destroyed the entire industry's financing capacity.

- Venture capitalists (VCs) thought they could mark their holdings based on the low float token's market cap and continue fundraising, but as the drawbacks of the strategy were exposed, their mid-to-long-term financing channels were ultimately cut off.

A perfect lose-lose-lose-lose matrix. Everyone thinks they are playing a masterful game, but the game itself is inherently disadvantageous to all participants.

2. Market Reactions: Meme Coins and MetaDAOs

The market has attempted to break the deadlock twice, and both attempts exposed the complexity of token design.

First Wave: The Meme Coin Experiment

Meme coins were a backlash against VC low-float launches. The slogan was simple and appealing: 100% circulating supply on day one, no VCs, completely fair. Finally, retail wouldn't be screwed by the game.

Reality was much darker. Without a filtering mechanism, the market was flooded with unscreened tokens. Rogue, anonymous operators replaced VC teams. This didn't bring fairness; instead, it created an environment where over 98% of participants lost money. Tokens became vehicles for rug pulls, with holders being cleaned out minutes or hours after launch.

Centralized exchanges were caught in a dilemma. Not listing meme coins meant users would trade directly on-chain; listing them meant taking the blame when the price crashed. Token holders suffered the worst losses. The real winners were only the issuing teams and platforms like Pump.fun.

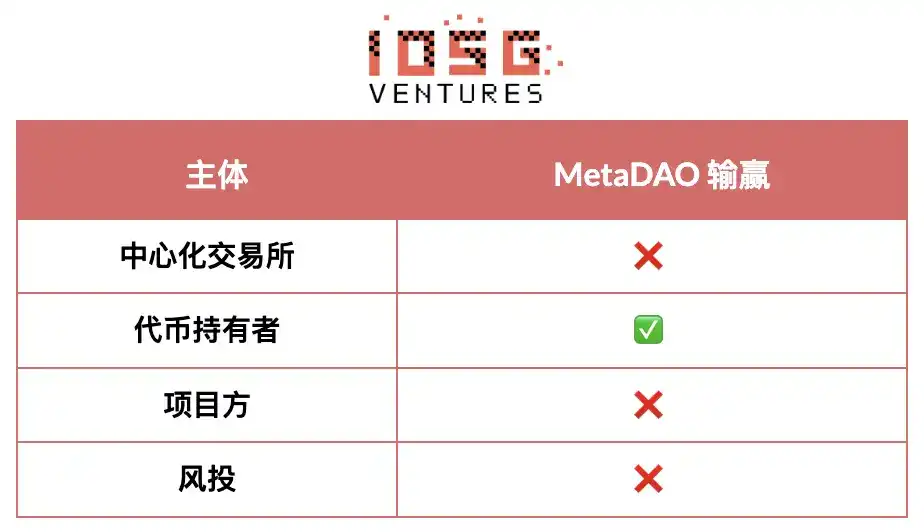

Second Wave: The MetaDAO Model

MetaDAOs were the market's second major attempt, swinging the pendulum to the other extreme—heavily favoring token holder protection.

There were indeed benefits:

- Token holders gained control, making capital deployment more attractive

- Insiders could only cash out upon achieving specific KPIs

- Opened new financing avenues in a capital-tight environment

- Relatively lower initial valuation, fairer access

But MetaDAOs overcorrected, bringing new problems:

Founders lost too much control too early. This created a "founder lemon market"—talented teams with options avoided this model, leaving only desperate teams to accept it.

Tokens still launched at a very early stage, experiencing extreme volatility, but with even fewer screening mechanisms than the VC cycle.

Infinite minting mechanisms made listings on tier-1 exchanges nearly impossible. MetaDAOs and CEXs, which control the vast majority of liquidity, are fundamentally misaligned. Without CEX listings, tokens are trapped in illiquid markets.

Each iteration attempted to solve problems for one party and proved the market's ability to self-correct. But we are still searching for a balanced solution that serves the key participants: exchanges, holders, projects, and capital providers.

The evolution continues. Until balance is found, there will be no sustainable model. This balance isn't about pleasing everyone but drawing a clear line between harmful practices and reasonable rights.

3. What Should the Balanced Solution Look Like?

Centralized Exchanges

Should stop: Requiring extended lockups that hinder proper price discovery. These extended locks appear protective but actually prevent the market from finding a fair price.

Are entitled to demand: Predictability in token release schedules and effective accountability mechanisms. The focus should shift from arbitrary time locks to KPI-based unlocks, with shorter, more frequent release cycles tied to actual progress.

Token Holders

Should stop: Overcorrecting due to historical lack of rights, exerting excessive control that scares away the best talent, exchanges, and VCs. Not all insiders are the same; demanding uniform long-term lockups ignores role variations and hinders price discovery. Obsessing over magical ownership thresholds ("insiders can't exceed 50%") precisely creates the soil for low-float manipulation.

Are entitled to demand: Strong information rights and operational transparency. Holders should understand the business behind the token, receive regular updates on progress and challenges, and know the true state of treasury reserves and resource allocation. They have the right to ensure value isn't siphoned through opaque dealings or alternative structures. The token should be the primary IP holder, ensuring created value accrues to token holders. Finally, holders should have reasonable control over budget allocation, especially for significant expenses, but should not micromanage daily operations.

Project Teams

Should stop: Issuing tokens without clear signals of product-market fit or actual token utility. Too many teams treat tokens as inferior, glorified equity—worse than venture equity but without legal protection. Token issuance shouldn't happen just because "that's what crypto projects do" or because money is running out.

Are entitled to demand: The ability to make strategic decisions, place bold bets, and handle daily operations without needing DAO approval for everything. If held accountable for results, they must have the power to execute.

Venture Capitalists

- Should stop: Forcing every portfolio company to issue a token, reasonable or not. Not every crypto company needs a token. Forcing token issuance to mark holdings or create exit opportunities has flooded the market with low-quality projects. VCs should be stricter and realistically assess which companies are truly suited for a token model.

- Are entitled to demand: Returns commensurate with the extreme risk of investing in early-stage crypto projects. High-risk capital deserves high returns when bets pay off. This means reasonable ownership stakes, fair vesting schedules reflecting contribution and risk, and the right not to be demonized upon successful investment exits.

Even if a balanced path is found, timing is crucial. The short-term outlook remains grim.

4. The Next 12 Months: The Final Wave of Supply Shock

The next 12 months will likely be the last wave of oversupply from the previous VC hype cycle.

After weathering this digestion period, the situation should improve:

- By the end of 2026, projects from the last cycle will have either finished token issuance or shut down.

- Financing costs remain high, limiting the formation of new projects. The pipeline of VC projects waiting to launch tokens has noticeably shrunk.

- Primary market valuations return to rationality, reducing the pressure to use low floats to prop up high valuations.

Decisions made three years ago shaped today's market. Decisions made today will determine the market's state two to three years from now.

But beyond the supply cycle, the entire token model faces a deeper threat.

5. Existential Crisis: The Lemon Market

The greatest long-term threat is altcoins becoming a "lemon market"—where quality participants are driven away, leaving only those with no other options.

Possible evolution path:

Failed projects continue issuing tokens to gain liquidity or extend their lifespan, even with zero product-market fit. As long as all projects are expected to issue tokens, regardless of success, failed projects will keep flooding the market.

Successful projects, seeing the惨状 (miserable state), opt out. When strong teams see persistently poor overall token performance, they may pivot to traditional equity structures. Why endure the torment of the token market if you can be a successful equity company? Many projects lack a compelling reason to issue a token. For most application-layer projects, tokens are shifting from a necessity to an option.

If this trend continues, the token market will be dominated by failed projects with no other choice—the unwanted "lemons."

Despite the risks, I remain optimistic.

6. Why Tokens Can Still Win

Despite the challenges, I still believe the worst-case lemon market scenario will not materialize. Tokens offer unique game-theoretic mechanisms that equity structures simply cannot replicate.

Accelerating growth through ownership distribution. Tokens enable precise allocation strategies and growth flywheels impossible with traditional equity. Ethena's use of token-driven mechanisms to rapidly bootstrap user growth and build a sustainable protocol economic model is a prime example.

Creating a moated community of passionate loyalty. Done right, tokens can build a community with real skin in the game—participants become highly engaged, loyal ecosystem advocates. Hyperliquid is an example: their trader community became deeply involved, creating network effects and loyalty that would be impossible to replicate without a token.

Tokens can enable growth much faster than equity models while opening vast space for game-theoretic design, unlocking huge opportunities when executed correctly. These mechanisms are truly transformative when they work.

7. Signs of Self-Correction

Despite the difficulties, the market is showing signs of adjustment:

Tier-1 exchanges have become extremely selective. Token issuance and listing requirements have tightened significantly. Exchanges are strengthening quality control, conducting stricter evaluations before listing new tokens.

Investor protection mechanisms are evolving. Innovations from MetaDAOs, DAO-owned IP (referencing Uniswap and Aave governance disputes), and other governance experiments show communities are actively trying better structures.

The market is learning, albeit slowly and painfully.

Recognizing the Cycle's Position

Crypto markets are highly cyclical, and we are currently in a trough. We are digesting the negative consequences of the 2021-2022 VC bull market, hype cycle, overinvestment, and misaligned structures.

But cycles always turn. Two years from now, after the 2021-2022 cohort is fully digested, after new token supply diminishes due to funding constraints, and after better standards are trial-and-errored—market dynamics should improve significantly.

The key question is whether successful projects will return to the token model or permanently shift to equity structures. The answer depends on the industry's ability to solve the issues of interest alignment and project screening.

8. The Path to Breaking the Deadlock

The altcoin market stands at a crossroads. The four-way lose-lose dilemma—exchanges, holders, projects, and capital all losing—has created an unsustainable market condition, but it is not a dead end.

The next 12 months will be painful, with the final wave of 2021-2022 supply arriving. But after the digestion period, three things could drive a recovery: better standards formed from painful trial and error, a realignment mechanism acceptable to all four parties, and selective token issuance—only when it truly adds value.

The answer depends on choices made today. Three years from now, looking back at 2026, we will view it just as we view 2021-2022 today: What are we building?