Original|Odaily Planet Daily(@OdailyChina)

Author|Wenser(@wenser2010 )

Have you ever wondered how much of the profit generated from selling an iPhone is distributed to various component suppliers?

Recently, overseas tech blogger @BluthCapital jokingly commented on the "business acumen" behind the iPhone from the perspective of Micron's CEO: "For over a decade, Apple has been buying chips from us (MU) for $5, putting them in a metal box, and selling them to consumers for $99; when we tried to raise the price to $7, they laughed. But now, when we try to charge them $50, they increase the product price by $250." The remarks clearly express disdain for Apple's recent price hike and its attempt to blame memory manufacturers.

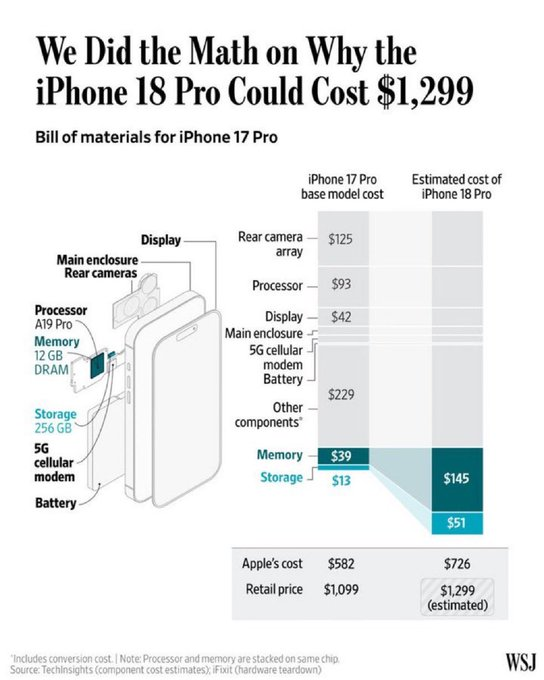

The post quickly sparked discussions on social media. This morning, @BluthCapital continued the topic by posting a cost structure chart for the iPhone 18 with specific numbers to support their point:

Previously, Micron's Chief Commercial Officer, Sumit Sadana, also mentioned in an interview with The Wall Street Journal, "During the downturn in the memory industry, certain customers took advantage to push prices down, leading to negative profits for our company." Now, due to strong demand from the AI and tech sectors, the memory industry has become the side holding the bargaining power. This has turned the entire supply chain dynamic on its head.

The Profit Structure of an iPhone: Apple Takes Nearly 25%, Memory Giants Like Micron Get Less Than 3%

Estimates suggest that in the profit from a single iPhone, Apple takes about a quarter, memory giants get only about one-thirtieth, TSMC takes about 4%-5% of the profit due to its monopoly position; the remaining portion is covered by other hardware suppliers, channels, R&D, taxes, and other factors.

Looking Back at Apple's Financial Reports: Net Profit Margin Consistently Above 24%, Grabbing 75% of Industry Total Profits

According to data from institutions like Counterpoint, Apple has long occupied nearly 50% of the global smartphone market's operating profits. 2025 IDC data shows it takes about 75% of the industry's total profits with an 18% market share.

Based on Apple's latest Q2 2026 data, iPhone revenue was $57 billion, net profit was $34 billion, and estimated shipments were around 61 million units. From this, it can be inferred that Apple's net profit per iPhone is approximately $320-$340, with a net profit margin of 33%-36%.

From a comparison of financial data over the past 5 years, we can also clearly see that iPhone revenue has been relatively stable overall; the scale of net profit gradually grew from around $94 billion in 2021 to around $112 billion in 2025; the net profit margin remained relatively stable, typically around 25%.

Looking at different models like the iPhone X in 2017, the iPhone 14 Pro in 2023, and the iPhone 17 series in 2026, their profit structures have undergone a series of changes due to differing memory costs.

From iPhone X to iPhone 17: Memory Costs Double

The role of memory cost in iPhones has gone through 3 historical phases: from the initial "scrap material," to later becoming an "important component," and now a "critical component."

2017 iPhone X Era: The "Scrap Material" Period for Memory

According to Counterpoint's teardown report data from that year, during the iPhone X era, benefiting from its longstanding brand advantage and position in the upstream ecosystem, Apple's net profit margin once approached 50%; while memory manufacturers like Samsung and Hynix from South Korea only accounted for about 135–195 yuan in profit; about 1.6%–2.3% of the total selling price of 8388 yuan.

This was the weight of "memory" in the iPhone X era: about 2% of the cost, almost the component Apple cared about the least.

2023 iPhone 14 Pro Era: Memory as an "Important Component"

In 2023, the iPhone 14 series launched. Apple's material costs saw a slight increase. Taking the Pro version as an example, its BOM (Bill of Materials) cost reached around $464 (approximately 3,170 RMB), accounting for nearly 40% of the selling price, but Apple's net profit margin remained around 40%.

According to feedback from tech media at the time, the above data was only for the 128GB version. The cost increase for more expensive memory versions wasn't high, but their selling prices were significantly higher. This was during the "camera and processor price hike period," so ultimately, the overall profit for the iPhone 14 Pro was 3.7% lower than that of the iPhone 13 Pro.

2026 iPhone 17 Era: Memory as a "Critical Component"

Fast forward to 2025-2026, the iPhone 17 series became Apple's main model, and memory costs have doubled compared to a few years ago. It is now estimated that memory cost accounts for 12%-15% of the BOM cost, approximately $60-$80.

In summary, the following is relevant data on iPhone costs and memory cost proportions across different periods.

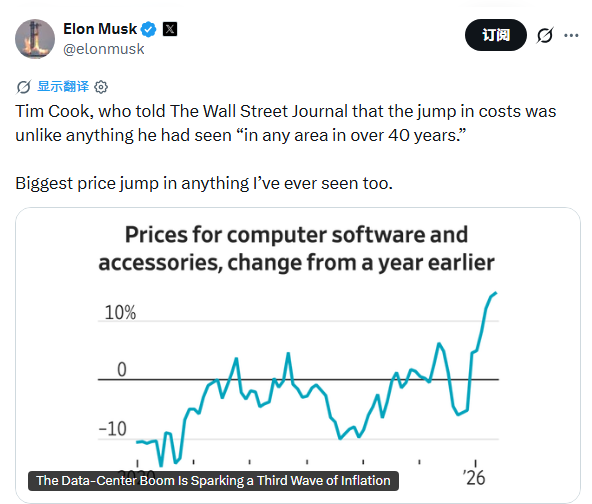

It's worth noting that TrendForce data shows general-purpose DRAM contract prices surged by 93% to 98% quarter-over-quarter in Q1 2026. Citi expects the average DRAM price increase for full-year 2026 to reach 88%. This aligns with the trend of rising memory costs. This phenomenon also drew affirmation from Apple CEO Tim Cook and Elon Musk.

Cook: Memory Price Hike, a Once-in-40-Years Event

On June 17, Apple CEO Tim Cook (Odaily Planet Daily Note: He will step down as CEO in September this year, succeeded by former Senior Vice President of Hardware Engineering, John Ternu) mentioned the cost pressure from memory price hikes in an interview with The Wall Street Journal. He said, "When consumers need devices, supply has decreased, and memory manufacturers are passing on significant price pressure. We absolutely need memory pricing and supply to return to reasonable levels for consumer products. That's the bottom line."

But less than a week later, he quickly changed his tune.

On June 25, Cook was interviewed again by The Wall Street Journal, referring to the cost impact as a "hundred-year flood," saying, "In over 40 years, I've never seen anything like it in any field." Subsequently, Apple announced price increases across its entire product line, including Mac, iPad, HomePod, Apple TV, and Vision Pro.

Upon the news, Apple's stock price fell 6%, wiping out $263 billion in market value; marking its largest decline since April 2025.

Musk: I Haven't Seen This Either

Cook's words also garnered strong agreement from Elon Musk. Recently, he also posted, "Cook tells WSJ this cost surge is something he's 'never seen in any field in over 40 years.' Same for me, this is the sharpest price jump I've ever seen."

Thanks to AI Data Centers and HBM, Memory Has a Stronger Backbone Now

A closer look at the "memory bull market" starting last year reveals the key driving factor is still the strong demand from the AI industry.

Industry estimates generally suggest that compared to a regular server, each AI server requires 8 times and 3 times the amount of DRAM and NAND, respectively.

Given this market demand, the three major memory giants—Samsung, SK Hynix, and Micron—naturally shift more advanced process capacity towards high-margin HBM (High Bandwidth Memory) and high-end DDR5 products, proactively cutting production lines for consumer-grade products like DDR4, leading to shortages in general-purpose DRAM.

Public information shows that a single AI server's DRAM capacity is 8 to 10 times that of a traditional server. Combined with demand for general server inventory replenishment and the proliferation of AI PCs, the supply-demand gap for memory chips continues to widen.

The astonishing gross margin of 84.6% in Micron's recent Q3 financial report and revenue growth of 346% year-over-year to $41.46 billion also showed many people the money-making power of monopolistic memory manufacturers. On the other side, SK Hynix recently announced plans for a US listing, seeking to raise about $29 billion to further capitalize on memory demand.

It's no exaggeration to say that memory demand from the AI industry is squeezing, even devouring, the memory supply for consumer electronics. Statistics show that the memory used in one Nvidia Vera Rubin AI server is equivalent to about 14,500 MacBook Neos. A 1:14,500 ratio highlights the current imbalance between memory supply and demand.

For memory manufacturers who have long suffered from price suppression by giants like Apple, this is their era. No wonder there were previous reports that Apple is actively lobbying the Trump administration, hoping to get approval to purchase memory chips from Chinese chipmaker ChangXin Memory Technologies (CXMT).

As for whether CXMT can replicate the wealth-creating miracles of star companies like SK Hynix and Micron in the capital market, perhaps the answer will be revealed next month.

Related Reading

Super Unbelievably Spiraling Explosion, Micron's Earnings Report Rekindles the Semiconductor Long Bull