Author: Attorney Liu Honglin

For a startup looking to integrate stablecoins into its product, the current challenge isn't a lack of stablecoins to use, but rather: with so many stablecoins available in the market, which one should I choose?

Coinbase's answer is, you don't have to choose any of them; I'll tailor-make one for you.

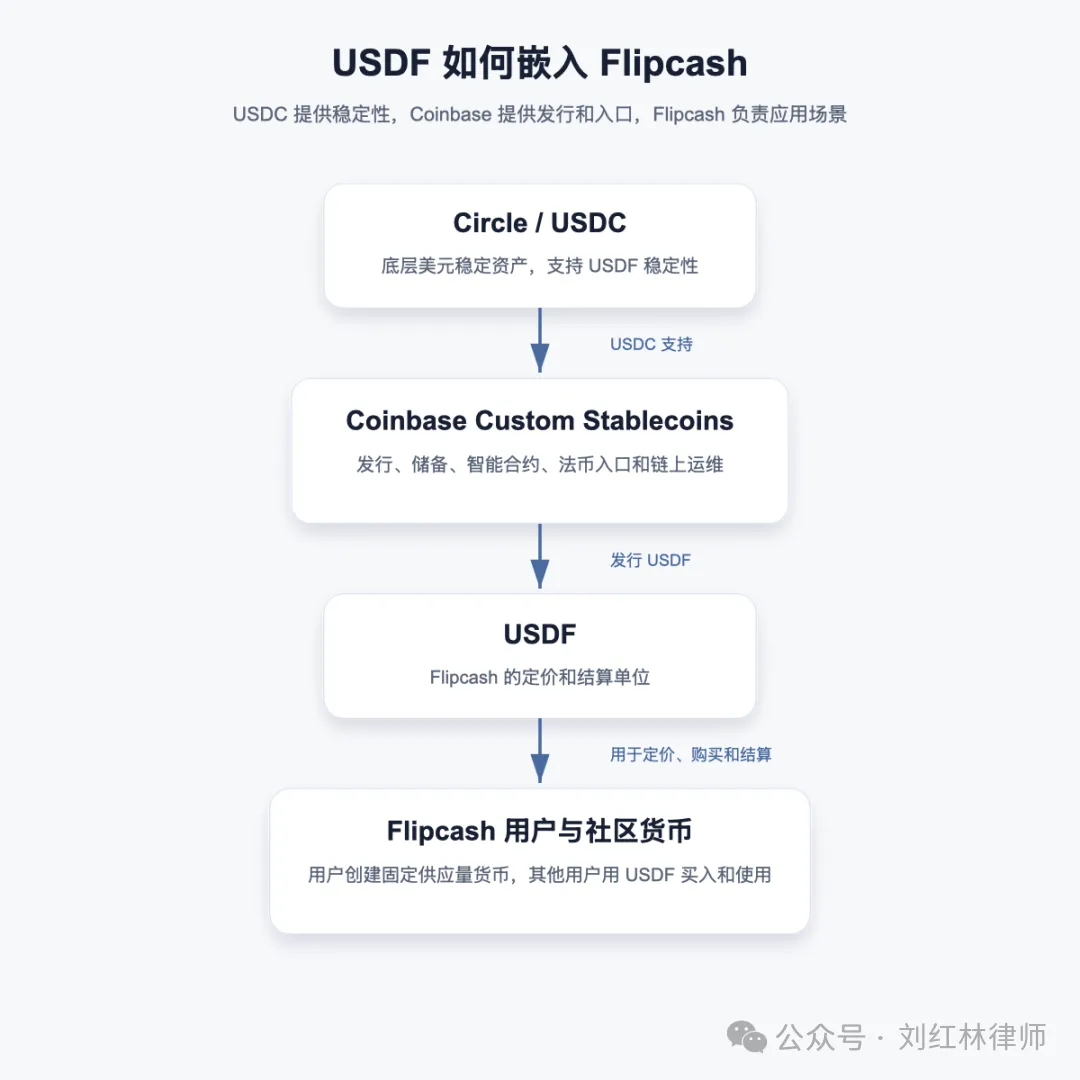

On May 20th, Coinbase announced the launch of USDF for Flipcash via its Custom Stablecoins platform. Flipcash is an application focused on community currencies and social payments, where users can create digital currencies with a fixed supply and use them like digital cash. The role of USDF is to provide these community currencies with a relatively stable pricing and settlement unit.

According to Coinbase's introduction, USDF is issued on Solana and is backed 1:1 by USDC. Flipcash doesn't need to build the underlying capabilities for issuance, reserves, on-chain contracts, and user deposits from scratch; instead, it hands these foundational tasks to Coinbase.

The value of this news lies precisely in this change.

A few days ago, US discussions around the CLARITY Act were still focusing on the boundaries of stablecoin yields: Can stablecoin-related platforms pay users yields similar to bank deposit interest? The regulatory line regulators want to draw is clear: stablecoins cannot easily become high-interest accounts without a license. The direction Coinbase is providing now is to turn stablecoins into a payment and settlement capability that applications can plug into.

The industry significance of this move is that it further pushes stablecoins from being an 'asset used by platforms to retain users' towards being a 'payment component that applications can call upon.'

For entrepreneurs, stablecoins don't necessarily have to exist only as an independent financial product; they can also hide behind specific products like social media, gaming, creator economies, and cross-border e-commerce, becoming an underlying tool for pricing, purchasing, and settlement.

This is much more interesting than simply launching a new coin.

Stablecoins Becoming a Service

Many people's understanding of stablecoins may still be stuck on the logic of the issuer profiting from interest spreads: who issues it, how big is its scale, what's the trading volume, and does it generate yield? But the USDF case reminds us that the commercial value of stablecoins isn't necessarily just in 'issuing an asset'; it can also be in 'helping others leverage stablecoin capabilities.'

To understand USDF, you first need to understand the problem Flipcash is actually trying to solve.

It's not just a simple wallet, nor an ordinary trading platform. It aims to let users create fixed-supply community currencies. For example, a creator, a community, or a small group can all create their own digital currency on it and let other users buy and use it like digital cash.

Looking at specific usage scenarios makes the role of USDF clearer. A user creates a fixed-supply community currency on Flipcash, and this currency needs to be priced in USDF; other users who want to buy or use this type of community currency also complete settlement via USDF. Coinbase also mentions that Flipcash chose it because it needed transparent 1:1 USDC backing, USDC incentives that scale with USDF circulation, convenient fiat on-ramps for users, and the crypto infrastructure Coinbase has built over many years.

So why doesn't Flipcash just use USDC directly?

USDC can certainly serve as the underlying stable asset, but Flipcash clearly wants a settlement unit closer to its own product. The name USDF itself is tied to Flipcash; users see the platform's own stablecoin within the product, not an external, general-purpose asset. More importantly, Coinbase bundles USDF with fiat on-ramps, USDC backing, circulation-based incentives, and on-chain operations. What Flipcash gets is a complete suite of stablecoin capabilities, not just putting USDC into its product.

The focus here isn't 'Flipcash launched another coin,' but rather that community currencies at the application layer need a stable payment and settlement base. USDF serves as that base.

You can view the structure of this as follows:

Coinbase's Custom Stablecoins platform is designed precisely to solve such problems. According to Coinbase's product description, businesses can create their own branded stablecoins, supported by 1:1 exchange with USDC, with Coinbase handling issuance, reserves, smart contracts, and on-chain operations. These can also be integrated with scenarios like payments, rewards, and developer tools.

Stablecoins are no longer just assets displayed upfront for users; they can also hide behind products, becoming part of the payment, pricing, and settlement process.

For businesses, they may not actually want to become stablecoin issuers. What they care more about is whether their product can have a stable settlement unit, whether users can pay and exchange smoothly, whether cash flows can be reconciled, whether risks can be controlled, and whether the underlying system can operate stably.

These issues are more practical and closer to the work that must be faced when stablecoins enter real business scenarios than 'launching another coin.'

Coinbase's New Role

If you only think of Coinbase as an exchange, it might be harder to understand the USDF initiative.

Traditionally, exchanges handle matching trades, asset listings, user buying/selling, and transaction fees. But in the USDF scenario, the role Coinbase plays is no longer just a trading gateway. It acts more like a stablecoin infrastructure provider: helping applications issue stablecoins, providing USDC backing, connecting fiat on-ramps, maintaining on-chain contracts, and offering enterprise-level technical and compliance capabilities.

It's also important to see the positions of Circle and USDC here. Circle isn't the protagonist in this news, but USDC is the asset backing USDF. That means, on the surface, USDF is Flipcash's branded stablecoin, but its US dollar stability is still provided by USDC underneath.

This is significant for USDC. In the past, typical USDC scenarios were exchange balances, on-chain transfers, DeFi, and institutional settlements. Now, through Coinbase's custom stablecoin platform, USDC can be embedded into more specific applications, becoming the underlying asset behind community currencies, social payments, and platform settlements. What users see might be USDF, but what underpins its stability is still USDC.

From this perspective, the division of labor between Coinbase and Circle becomes clearer. Circle provides the underlying stablecoin asset, Coinbase packages this capability into a product businesses can integrate, and application builders then incorporate it into their own user scenarios. Competition in the stablecoin industry is no longer just about who issues a larger scale, but also about who can enter more real-world applications.

This aligns with Coinbase's direction over the past few years. It no longer just wants to be at the end where users buy and sell crypto assets; it wants to enter more foundational positions like developers, enterprise payments, wallets, and on-chain settlement. USDF is just one concrete example.

Of course, this path is also heavier.

Once stablecoins enter specific application scenarios, the issues aren't just about fast on-chain transfers. They include user identity, fund sources, deposits/withdrawals, anti-money laundering (AML), sanctions screening, reserve transparency, redemption mechanisms, accounting processes, and user complaints. When stablecoins enter real business, relying solely on the technical narrative of the crypto world isn't enough.

What Crypto Payment Entrepreneurs Should Look At

For crypto payment entrepreneurs, the most valuable aspect of USDF isn't necessarily 'can I also issue my own stablecoin?' A more valuable question is: why does Flipcash need Coinbase to help it do this?

The answer is actually quite practical. Flipcash's core business is community currencies and social payments, not stablecoin issuance. It needs stablecoin capabilities so that the community currencies users create can be priced, bought, settled, and used. If it handled issuance, reserves, on-chain contracts, user deposits, and compliance interfaces itself, the entire product's focus would be dragged down by the underlying infrastructure.

This offers a very direct insight for crypto payment entrepreneurs: many applications don't need to become issuers themselves; they need to integrate stablecoin capabilities into their operations. Whoever can make this integration process smoother may become the infrastructure supplier for the next wave of applications.

In the USDF case, the specific problems and business needs are: How does the platform reconcile the cash flow from users buying community currencies with on-chain settlement? How do users enter via fiat on-ramps? How is the exchange relationship between the branded stablecoin and the underlying USDC ensured to be clear? How do you explain to users who exactly issues this stablecoin, who backs it, and who to contact if there are problems?

These issues go beyond 'coin launch marketing' and enter the phase where product, payment, and compliance must be implemented together.

What real customers need isn't a stablecoin concept that sounds novel. They need a system that allows users to pay smoothly, the platform to complete settlements, and the backend to clearly account for fund flows.

However, the USDF matter also cannot be taken to the other extreme, suggesting that any company in the future can issue its own branded stablecoin.

After all, once a product involves real fund exchange, user balances, redemption arrangements, and transferable assets, it naturally approaches financial regulation. Even if it's packaged as a community currency, branded coin, or in-app dollar account, regulators still look at where the funds come from, why users buy it, what the platform promises, whether the asset can circulate, and who bears the risk.

Coinbase can do this because it already has a foundation within the US crypto infrastructure and compliance system, and can integrate USDC, fiat on-ramps, on-chain operations, and enterprise services.

If an ordinary startup team only sees 'every app can have its own stablecoin,' it's easy to imitate superficially and go down the wrong path.