Original Author: Shirley Li, Researcher at Web3Caff Research

How to easily grasp the market hotspots, technological trends, ecosystem progress, and governance developments happening in the Web3 industry...? The "Market Pulse Analysis" column launched by Web3Caff Research delves into the front lines to explore and filter current hot events, providing value interpretation, commentary, and principle analysis. See through the phenomenon to grasp the essence, and follow us now to quickly capture the frontline market trends in Web3.

Compliance Notice: Stablecoins are virtual currencies (Tokens), and please be aware that issuing and participating in Token investment have varying degrees of regulatory requirements and restrictions in different countries and regions, especially in Mainland China where issuing Tokens may constitute "illegal securities issuance," and providing Token trading services or other cryptocurrency-related activities may also be considered "illegal financial activities" (Readers in Mainland China are strongly advised to read "Summary of Mainland China Laws and Regulations Related to Blockchain and Virtual Currency and Key Points"). The following content is only an objective analysis of the progress and market feasibility strategies of Arc Network, and aims to explore and analyze how application scenarios based on blockchain technology are developing responsibly within the global regulatory environment. Therefore, please do not use this information for related decision-making, and please strictly comply with the laws and regulations of your country and region, and refrain from participating in any illegal financial activities.

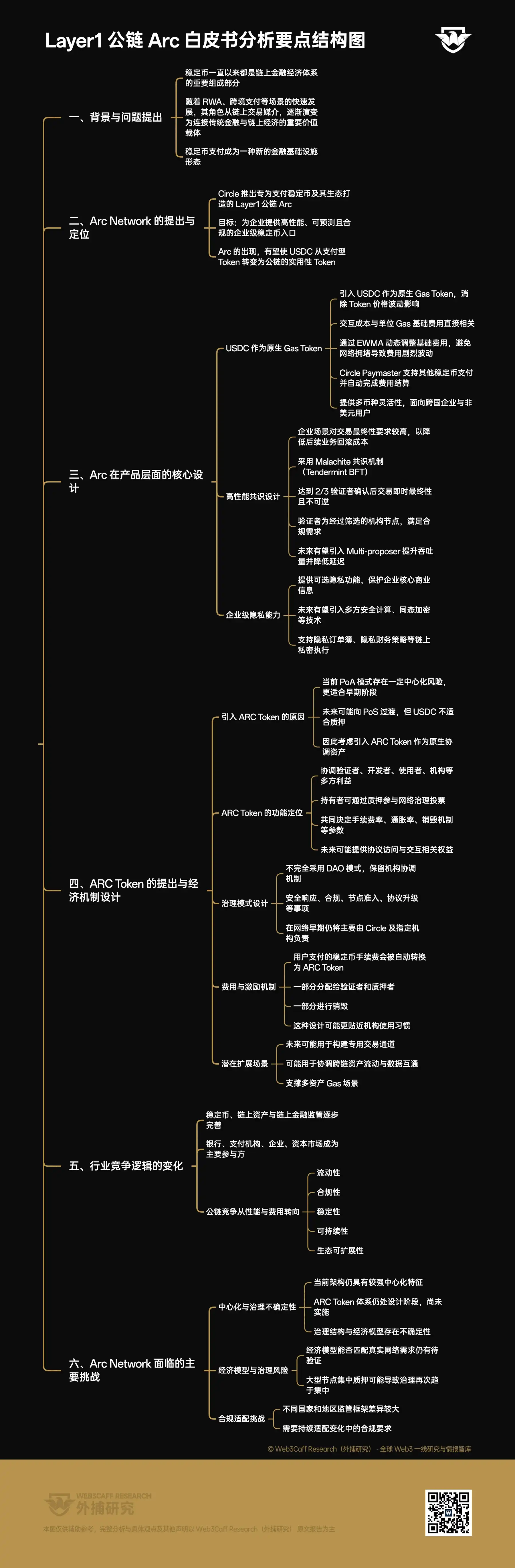

Stablecoins have long been a crucial component of the on-chain financial and economic system. Recently, with the rapid development of scenarios such as RWA and cross-border payments, their role is gradually evolving from a simple medium of exchange on-chain to an important value carrier connecting traditional finance and the on-chain economy within the scope of some countries and regions worldwide. Stablecoin payment has also become a new form of financial infrastructure.

Last May, Circle announced the launch of Arc, a Layer 1 public blockchain specifically designed for stablecoin payments and its supporting ecosystem, aiming to provide enterprises with a high-performance, predictable, and compliant entry point for enterprise-grade stablecoins. The emergence of Arc also has the potential to transform Circle's native stablecoin, USDC, from a single-function payment Token into a utility Token for a public chain. Previously, Circle had released the Arc Litepaper, introducing the operational logic of the blockchain at the product level, which Web3Caff Research also analyzed in detail:

As an L1 public chain, Arc has introduced the following innovations primarily around enterprise users:

- USDC as the Native Gas Token: Arc first introduces USDC as the native Gas Token of the public chain to eliminate the impact of Token price volatility, making the prediction of interaction costs directly related to the base fee per unit of Gas. To further reduce volatility, Arc dynamically adjusts the current base fee using an Exponentially Weighted Moving Average (EWMA) of historical block utilization, avoiding sudden, sharp increases in fees due to sudden network congestion. Furthermore, when users use other payment stablecoins, Arc's Circle Paymaster will automatically use its native stablecoin to advance the interaction fees and deduct an equivalent value of other stablecoins from the user's account. This provides flexibility for multinational corporations and users in non-dollar regions, positioning Arc to potentially become a global, multi-currency financial settlement public chain.

- High-Performance Consensus Design: In the on-chain context, because finality confirmation of interactions requires time, enterprises cannot immediately start processing an order, as there is a certain possibility that subsequent automated processing by a series of financial/business systems may need to be rolled back. Therefore, each transaction an enterprise makes carries a potential extra processing cost, which is unacceptable in actual enterprise operations. To address this, Arc employs the Malachite consensus mechanism (a variant of Tendermint Byzantine Fault Tolerance). Under this mechanism, once a payment is voted on and committed by two-thirds of the validators, it is instantly finalized and cannot be reversed. At the same time, Arc's validators are not anonymous staking nodes but a selected group of institutions with good reputations, capable of meeting compliance requirements across different global regulatory systems. In the future, Arc will also introduce multi-proposers, allowing multiple validators to generate block proposals in parallel within the same time window, which are then aggregated into a single block during the consensus phase. This will further enhance the payment system's throughput and reduce latency in financial processing.

- Enterprise-Grade Privacy: To ensure that core enterprise business information is not leaked, Arc provides enterprises with optional privacy capabilities, to be implemented in phases. In the future, as secure technologies like Multi-Party Computation and Homomorphic Encryption mature, Arc will introduce more complex privacy settings on-chain, such as private order books, privatized financial strategies that automatically run as confidential on-chain contracts.

If you want to learn more about the operational logic of the Arc blockchain, we recommend reading: "Market Pulse Analysis: Circle Advances into the Public Chain Arena, Can Its L1 Network Arc Become the First Compliant Chain for Payment Stablecoins?".

Fast forward to May of this year, half a year after the Arc testnet went live, Circle has released the Arc blockchain whitepaper, further elaborating on the design logic of the ARC Token as the native coordination asset of the Arc network, and revealed that the Arc mainnet is expected to launch this summer.

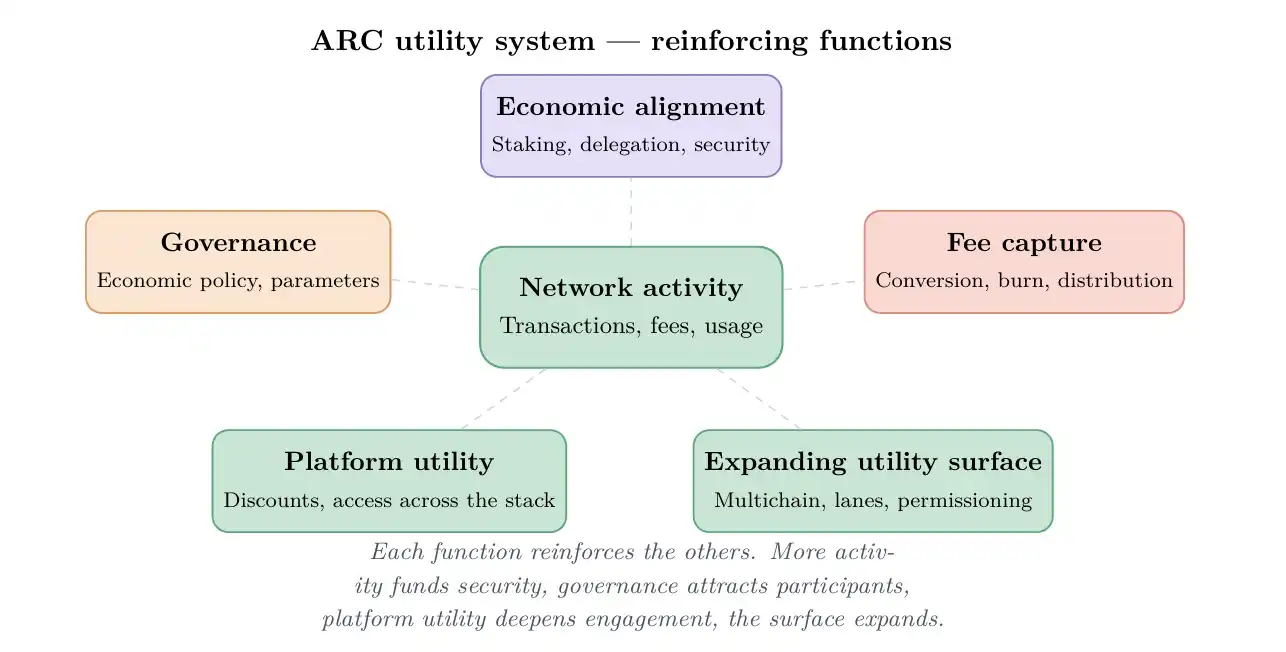

As mentioned earlier, currently, the Arc network employs a Proof of Authority (PoA) mechanism, meaning a selected group of reputable institutional nodes are responsible for network validation and block production. However, this model carries certain centralization risks and is more suitable for the early launch phase of a project. As network adoption scales, the Arc network is likely to transition to a Proof of Stake (PoS) mechanism in the future, but USDC, being a stablecoin, is not suitable for staking. Therefore, Circle is considering introducing a new Token system—the ARC Token—to serve as the native coordination asset of the Arc network, responsible for coordinating the interests and actions of various participants (validators, developers, users, institutions, etc.) in the network.

According to the whitepaper design, ARC holders can participate in network governance voting based on their staked weight, collectively deciding on network fee rates, inflation rates, and burn logic. Additionally, they may gain certain rights related to protocol access and interaction in the future. However, the whitepaper also clearly states that Arc network's governance model will not fully adopt a DAO model and will retain institutional coordination mechanisms. High-sensitivity matters involving security response, compliance, validator node admission, and protocol upgrades will still be primarily managed by Circle and designated institutions in the network's early stages.

Simultaneously, the fees users pay using stablecoins on the Arc network will be automatically converted into ARC Tokens. A portion will be distributed as rewards to validators and stakers, while another portion will be burned. Compared to traditional public chains requiring users to directly hold the native Gas Token, this design may better align with the usage habits of institutions and enterprises.

For the Arc network, the application scope of the ARC Token may be further expanded in the future, for example, to be used for building dedicated transaction channels; coordinating and managing asset flows and data interoperability between different blockchains; supporting Circle Paymaster's multi-asset Gas scenarios, enabling users to pay network fees with different stablecoins, and so on.

Image Source: ARC: The Native Asset of the Economic OS

However, it's important to note that the ARC Token system is currently still in the discussion and design phase and may undergo significant changes in the future. Furthermore, Circle has repeatedly emphasized that ARC itself is neither a security nor an investment product and does not represent any equity or right to profits.

On specialized blockchains like Arc Network, which are centered on stablecoin payments, large-scale economic activities often originate from banks, payment institutions, corporate users, and capital markets. As laws and regulations related to stablecoins, on-chain assets, and on-chain financial activities are being established and refined globally, the pathways for these institutions to participate in building on-chain infrastructure are becoming increasingly clear. This trend is also driving a shift in the competitive logic of Web3 infrastructure. The battle of public chains solely competing on network performance and transaction fees is becoming a thing of the past. Instead, network liquidity, compliance, stability, sustainability, and ecosystem scalability are becoming the new focal points of competition.

Of course, this transformation will not happen overnight, and the future development of Arc Network will still face several potential challenges.

For example, the current overall architecture of the Arc network still carries a strong centralization characteristic. Although Circle attempts to establish a longer-term economic coordination and governance mechanism for the network by introducing the ARC Token and gradually promote the network's evolution towards PoS, this system is still in the discussion phase and has not been officially implemented. Its specific governance structure and economic model remain highly uncertain. Simultaneously, the ARC Token mechanism itself will introduce some additional governance and security risks to the Arc network, such as whether the economic model design can match the real network needs? Could governance power become centralized again due to concentrated staking by large nodes? These questions await further discussion and optimization by the official team.

Furthermore, although stablecoin regulatory mechanisms are gradually being perfected, specific regulatory frameworks can vary significantly between different countries and regions. This means that Arc Network will need to continuously adapt to evolving compliance requirements in the future.

Currently, traditional public chains like Ethereum, Base, and Solana are actively expanding towards on-chain financial infrastructure, stablecoin payments, and institutional-grade applications. This can be seen as a signal of the changes sought by leading Web3 institutions, including Circle. However, who will ultimately succeed in building the next generation of global on-chain financial infrastructure remains to be observed continuously.

Key Points Diagram:

References:

[1] Introducing the ARC Whitepaper: Exploring Arc’s Native Coordination Asset

Disclaimer: This report is prepared by Web3Caff Research. The information contained herein is for reference only and does not constitute any prediction, investment advice, proposal, or offer. Investors should not rely on such information to purchase, sell any securities, cryptocurrencies, or adopt any investment strategy. The terminology used and views expressed in the report are intended to aid understanding of industry trends and promote responsible development in the Web3 and blockchain industry, and should not be interpreted as definitive legal opinions or the views of Web3Caff Research. The opinions reflected in the report are solely those of the author(s) as of the stated date, are independent of the position of Web3Caff Research, and may change following subsequent developments. The information and opinions contained in this report are derived from proprietary and non-proprietary sources that Web3Caff Research considers reliable and do not necessarily cover all data, nor is their accuracy guaranteed. Therefore, Web3Caff Research does not provide any warranty regarding their accuracy and reliability and shall not be liable for errors and omissions arising in any other manner (including liability to anyone for negligence). This report may contain "forward-looking" information, which may include forecasts and projections, and this article does not constitute a guarantee of any prediction. The decision to rely on the information contained in this report is entirely at the reader's discretion. This report is for informational purposes only and does not constitute investment advice, a proposal, or an offer to buy or sell any securities, cryptocurrencies, or adopt any investment strategy. Please strictly comply with the relevant laws and regulations of your country or region.