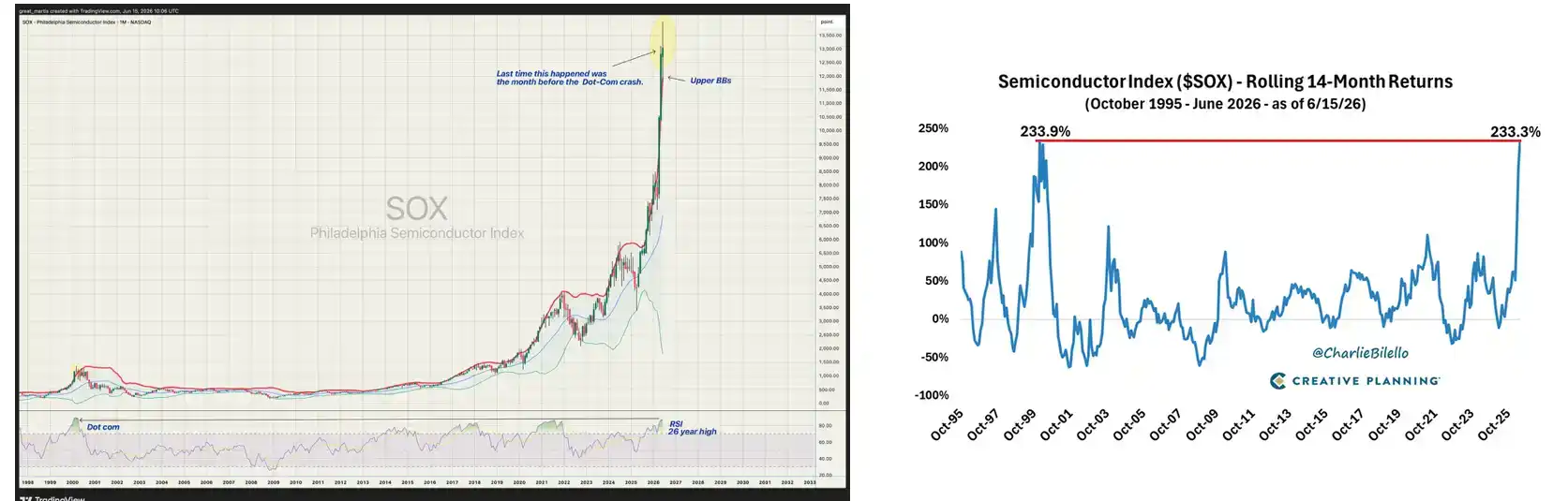

U.S. stocks closed overnight, with the Philadelphia Semiconductor Index (SOX) breaking through the 14,000-point mark for the first time, hitting a new all-time high.

Historically, there have only been two periods when the SOX rose over 230% within 14 months: from December 1998 to February 2000, and from April 2025 to the present.

The returns in this semiconductor bull market have been highly concentrated and significant. The year-to-date gains for the memory trio—Micron, SK Hynix, and Samsung—are approximately 141%, 186%, and 114%, respectively. TSMC's U.S. ADR has gained over 50% year-to-date.

Nvidia hit a new all-time high of $235.47 on May 14. Broadcom, Marvell, and ASML have either set new records or are approaching them in their respective market segments. The 52-week low for the entire SOXX ETF is $148, with the high near $369, representing a price swing of nearly 150%.

In April, Goldman Sachs revised its 2026 DRAM supply-demand deficit forecast from 3.3% to 4.9%, calling it the most severe memory shortage in 15 years. HBM prices are even more staggering: a single HBM3E stack costs about $300, and the upcoming HBM4 is estimated at $500 per stack. SK Hynix's 2026 HBM capacity has already been fully booked by Microsoft, Google, and Nvidia, with some customers even paying deposits in full upfront to secure capacity.

Clearly, the speed of AI data center construction is far outpacing the expansion of chip production capacity.

The 'Bottleneck' Bull Market

Scarcity is the most profitable product.

Understanding this phrase essentially captures the core logic of this semiconductor bull market. Whoever controls the bottleneck in AI infrastructure holds the most powerful pricing authority. Conversely, for segments that can be substituted or face price pressure, even with high demand, stock prices won't rise.

Optical modules are a typical example of the latter. A Photon Capital report in April pointed out that while Chinese optical module companies hold seven of the top ten global spots, they aren't making much profit; the profits are still with the chip companies. Zhongji Innolight and Sunsea are at a global first-tier level in terms of shipment volume and cost control for 800G and 1.6T optical modules, directly squeezing the margins of U.S. optical module companies like Coherent and Lumentum. Demand has doubled, yet profit margins have thinned. The reason is singular: the assembly stage of optical modules is not scarce enough.

Memory, meanwhile, has become the hardest theme in this U.S. semiconductor bull market. Essentially, it's because it controls a bottleneck, and that grip is tightening.

HBM is not ordinary DRAM. 3D stacking, TSV (Through-Silicon Via), specialized packaging processes—each layer of technological barrier is the result of over a decade of heavy capital investment. Globally, only three companies can mass-produce HBM, with SK Hynix taking roughly half the market share.

Interestingly, this logic holds true even when magnified to a macro, national level.

The true winners in AI data center infrastructure are not "all semiconductor countries," but those countries and regions that, over the past few years or even decades, have built scarce industrial clusters in some irreplaceable link of the chain. Scarcity is the key.

Every Region Has Its Own Main Track

It's quite interesting to see this perspective raised in U.S. stock forums.

The United States remains at the top of the value chain.

Nvidia, AMD, Broadcom's ASIC design; Synopsys and Cadence's EDA tools; Arista's AI networking; the three major cloud providers packaging computing power as services sold worldwide. Google, Amazon, and Microsoft are all accelerating in-house ASIC development. Broadcom and Marvell collectively hold about 95% of the custom ASIC design market. Google alone spends roughly $8 billion annually on TPU development with Broadcom.

The core nodes in manufacturing are in Taiwan and South Korea, but they are eating from completely different plates.

Taiwan's story revolves around TSMC and advanced packaging. 3nm and 2nm processes can only be mass-produced by TSMC globally. TSMC's three CoWoS backend factories are fully loaded, with lead times of 52 to 78 weeks. Nvidia alone has locked up 60% to 70% of CoWoS capacity. TSMC is expanding its monthly capacity from 35,000 wafers at the end of 2024 to 130,000 wafers by the end of 2026, nearly a fourfold increase. Even with this expansion, capacity remains tight. Taiwan's server OEM system, including Foxconn, Quanta, and Wistron, is also benefiting from the surge in AI server shipments.

South Korea's story is entirely centered on memory. SK Hynix captures about 50% to 55% of the global HBM market share, Samsung holds 19% to 35%, and Micron around 5% to 20%. HBM is not the same as ordinary memory; 3D stacking, TSV, specialized packaging—each layer of technological barrier is the result of decades of continuous heavy investment by South Korean companies.

Japan and the Netherlands also play crucial roles. Tokyo Electron makes semiconductor equipment; Shin-Etsu Chemical and SUMCO produce silicon wafers; Ajinomoto makes ABF substrate materials. Japan has long been out of the competition in finished chip products, but its position in materials and precision processing remains irreplaceable today.

The Netherlands is even more direct: ASML monopolizes EUV lithography machines. In January, Morgan Stanley significantly raised its target price for ASML to 1400 euros, predicting that 2027 will be the company's year of highest profit growth, with EPS growing 57% year-over-year. They base this judgment on three drivers: better-than-expected expansion of advanced logic foundry capacity, large-scale expansion in the DRAM memory sector, and overall demand performing better than expected. Dutch packaging equipment companies like BESI are also securing large orders amid the explosion in AI chip packaging demand.

China and Europe have different entry points, but the logic is similar: they have established cost advantages or delivery capabilities in specific links of AI infrastructure.

Zhongji Innolight and Sunsea are at a global first-tier level in shipment volume and price control for 800G and 1.6T optical modules. However, Photon Capital's analysis also warns of an important time window: the current high profit margins of optical module companies come from temporary pricing power due to the short-term shortage of 800G capacity. Once 1.6T ramps up in the second half of 2026 into 2027 and second- and third-tier manufacturers also fill their capacity, price pressure on the module end will arrive quickly.

In Europe, companies like Schneider Electric, ABB, and Vertiv, which focus on power distribution and thermal management, are receiving orders far exceeding expectations against the backdrop of soaring data center power consumption. Wedbush estimates that hyperscalers' AI infrastructure spending in 2026 will be about $725 billion, a 77% year-over-year increase, with power infrastructure being one of the fastest-growing subcategories.

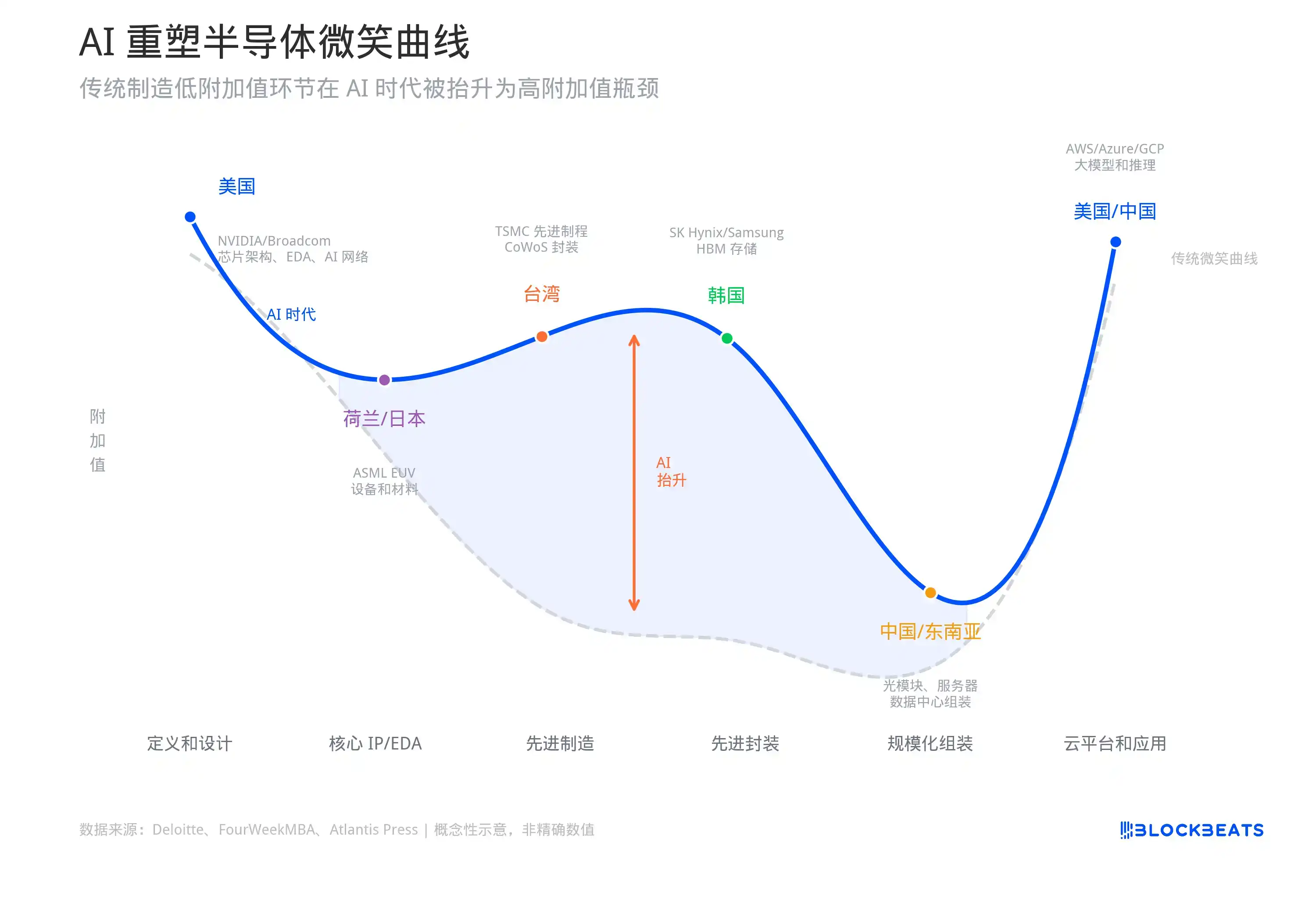

AI Reshapes the Semiconductor "Smile Curve"

Using the smile curve to summarize this landscape: The left end, led by the U.S., is responsible for "definition and design." The mid-to-high segment, involving Taiwan (China), South Korea, the Netherlands, and Japan, is responsible for "manufacturing advanced chips." The mid-to-low segment, involving Taiwan (China), China, and Southeast Asia, handles "large-scale assembly." The right end, with the U.S. and China, handles "cloud platforms, models, and customer access."

The original creator of this curve was Stan Shih, founder of Acer, who in 1992 used this model to explain why PC assembly had the thinnest profit margins.

But thirty years later, AI data centers are rewriting the shape of this curve.

Value chain analyses by FourWeekMBA and a paper published this year by Atlantis Press both point to the same conclusion: AI is re-elevating the middle segment of the traditional smile curve. TSMC's advanced CoWoS packaging, SK Hynix's HBM stacking, and ASML's EUV lithography machines—these segments, which in the traditional manufacturing smile curve belonged to the low-margin "middle manufacturing segment"—have become the most scarce resources in the AI era, with profit margins and pricing power not lower than those of the design or application ends.

Data from the paper shows that Nvidia's gross margin for 2023-2024 was 72.72%, with a net margin of 48.85%. However, TSMC's gross margin for Q1 2026 also reached 66.2%, with a net margin of 50.5%. The gap between design and manufacturing margins is narrowing, which is unprecedented in the history of the semiconductor industry.

The traditional smile curve posits that manufacturing has the thinnest margins. AI is turning the most difficult manufacturing links into the most scarce resources.

Morgan Stanley's March report on Asian semiconductors reached a similar conclusion: the 2023-2024 AI cycle was primarily focused on GPUs. From 2025 to 2026, demand is starting to diffuse across a broader industry chain, with memory, advanced packaging, custom ASICs, and data center networking taking the baton.

Every rotation of the bottleneck brings a new group of previously overlooked companies to the forefront, while those that gained the most in the previous phase enter a consolidation period.

How Much Further Can the Bull Run? Bull vs. Bear Views

Let's first hear from the bulls. Wedbush's Dan Ives said on CNBC in May that he expects the Nasdaq to reach 30,000 points in the next year, citing that AI chip demand still far exceeds supply. Goldman Sachs provided more concrete numbers: global AI capital expenditure in 2026 is about $765 billion, climbing to $1.6 trillion by 2031.

Morgan Stanley's March report on Asian semiconductors explicitly stated: AI computing investment is still in an expansion phase, and the semiconductor industry is entering a new structural demand cycle.

Bullish calls on memory are even more aggressive. Goldman Sachs recently revised down its DRAM supply-demand deficit forecasts for 2026-2028 into deeper shortage territory, adjusting the 2027 deficit from -2.5% to -5.9%, almost double. Their judgment is that this memory cycle is different from past ones: AI server demand has higher visibility, supply growth is locked down by long-term contracts, and price increases will last longer than the market expects.

Goldman Sachs even significantly raised its operating profit forecasts for Kioxia for 2027-2029 by 16% to 48%, citing that this period of high profitability could last two to three years. For a company in the highly cyclical memory business, a "high profitability lasting three years" call is very rare on Wall Street.

Morgan Stanley's change in stance is even more interesting. In 2024, they were still calling for a "DRAM winter," predicting price declines for years starting in Q4 2024. By 2025, they completely flipped to a super-cycle thesis, forecasting a 62% DRAM price increase in 2026 and predicting that SK Hynix and Samsung's profits would exceed consensus expectations by 30% to 50%.

But the bearish voices are also loud and come from significant players.

Michael Burry publicly warned in May that this semiconductor rally closely resembles the final months of the 1999-2000 internet bubble. The SOX is up 65% year-to-date, gained 10% in a single week, and the SOXX ETF is 60% above its 200-day moving average—this level of technical stretch has rarely been sustainable historically. SEC filings show he purchased a large number of put options on SOXX, QQQ, Nvidia, Palantir, and Oracle, expiring in January 2027, with strike prices well below current levels.

Man Group (one of the world's largest listed hedge funds) published a lengthy article in June specifically dissecting AI bubble risks. Their core view is that the financial architecture built around AI has become too large, over-leveraged, and overly reliant on a few interconnected players.

They specifically mentioned that a significant portion of AI data center construction is financed through private credit, with these loans collateralized by "hardware that depreciates as quickly as mobile phones, not long-term assets like buildings." The first wave of defaults could emerge in 2027-2028, when initial leases expire and the gap between financing assumptions and reality becomes impossible to ignore.

Looking ahead, several time nodes are worth watching.

Micron's earnings report on June 24th will be crucial; forward guidance on HBM demand and capacity allocation will determine the direction of the entire memory sector for the summer. Nvidia's next earnings report is equally critical; if there is even a slight signal of deceleration in AI chip demand, the sentiment across the sector will be repriced once again.

Looking further out, the timeline for capacity ramp-up is the real watershed. SK Hynix's M15X fab is expected to ramp in mid-2027, with its Yongin new fab moved up to February 2027. Samsung's P5 fab will come online in 2028. Micron's Idaho Fab 1 is expected to contribute output in mid-2027.

Combined, industry capacity will increase by 20% to 30% in the second half of 2027 to the first half of 2028. The question is whether HBM demand, with a compound annual growth rate of over 40%, will be met. Whether supply can catch up with demand depends on whether AI capital expenditure slows down before then.

The final variable is geopolitics. The higher the concentration of the semiconductor supply chain, the greater the impact of a black swan event. TSMC alone accounts for over 90% of global advanced process foundry capacity—this number represents efficiency during a bull market but systemic risk in a conflict scenario. Factors like the Taiwan Strait situation, potential escalation of U.S. export controls on China, and the degree of cooperation from Japan and the Netherlands on equipment restrictions are topics no one wants to discuss when the market is good. But if something happens, repricing will happen faster than any fundamental change.