Following the semiconductor crash on June 5th, the market's focus quickly shifted from 'why it fell' to another question: after the drop, who will recover first.

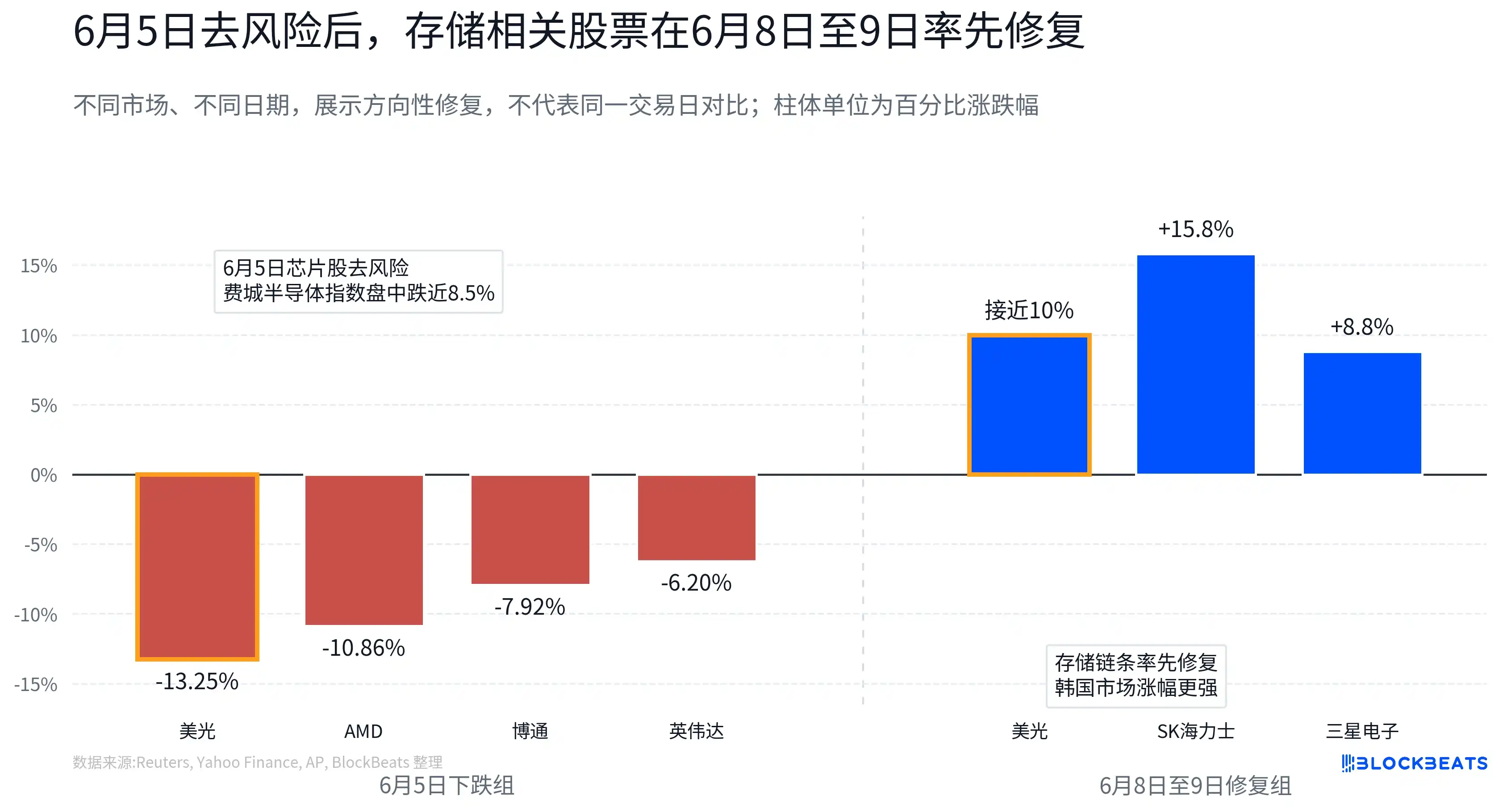

The answer is not uniform. According to Reuters, the market value of US-listed chip stocks once evaporated over $1 trillion, with the Philadelphia Semiconductor Index falling nearly 8.5% intraday. At the individual stock level, Micron fell about 13.25%, NVIDIA fell about 6.2%, AMD fell about 10.86%, and Broadcom fell about 7.92%. However, by June 8th, Micron rebounded nearly 10%; on June 9th, SK Hynix and Samsung Electronics in the Korean market also strengthened simultaneously.

Funds did not leave AI semiconductors but are re-screening within the sector. As valuations begin to be tested, the market's focus has also shifted from 'who has the AI story' to 'who can convert AI demand into profits the fastest'. Compared to some AI hardware segments that are still trading on expectations of future product cycles, customer adoption, and capital expenditure expansion, the demand growth for memory is already more directly reflected in orders, prices, and financial reports.

This is also why memory is the first to receive fund inflows. What the market is buying back is not just memory itself, but the EPS growth logic behind it that is easier to verify.

A Plunge Means High-Expectation Trades Are Being Re-evaluated

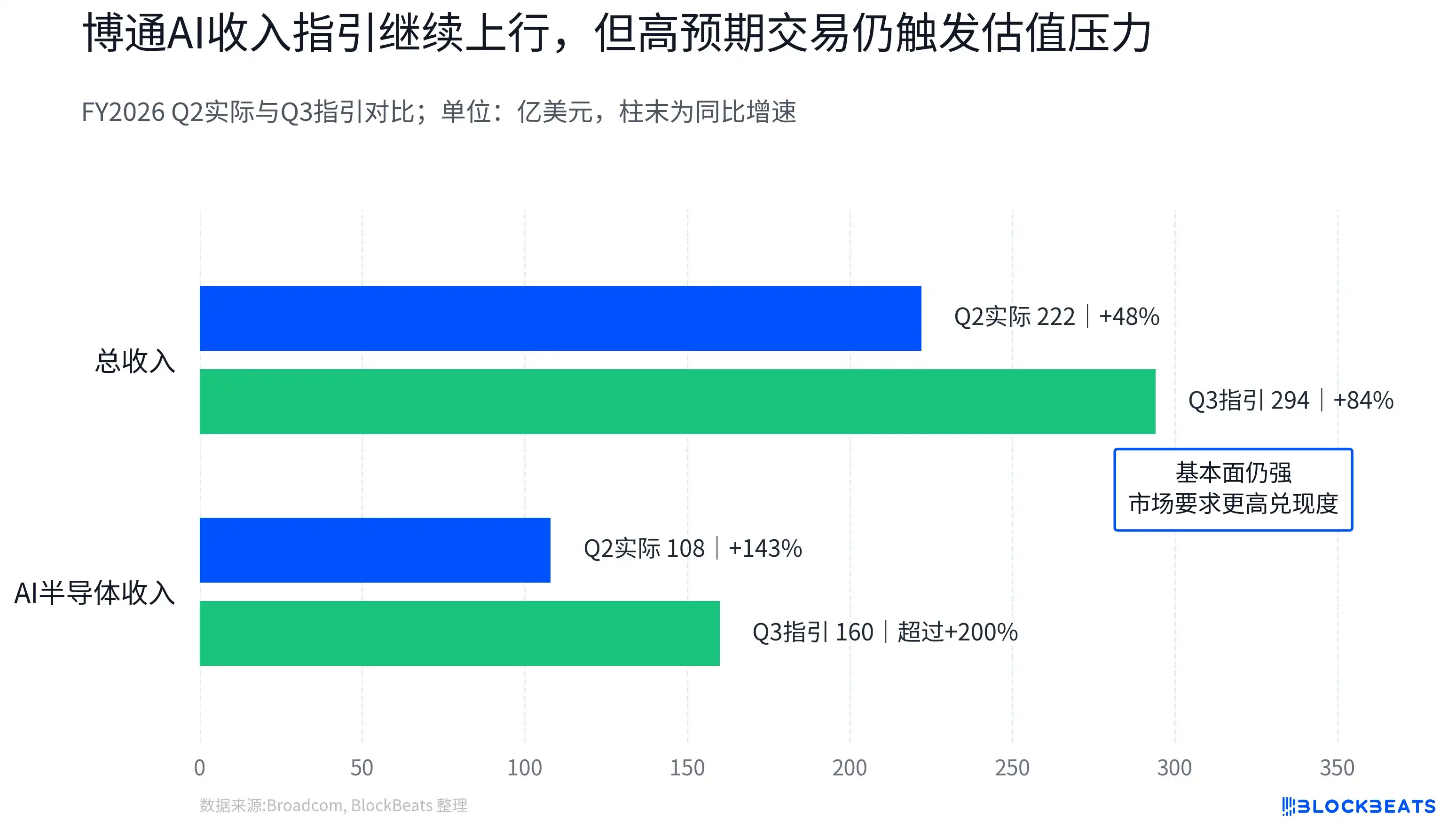

One of the triggers for this de-risking was the expectations gap after Broadcom's earnings report.

Looking at absolute numbers, Broadcom's fundamentals are not weak. According to the company's announcement, FY2026 Q2 revenue was $22.2 billion, a year-on-year increase of 48%. The company expects FY2026 Q3 total revenue to be approximately $29.4 billion, with AI semiconductor revenue expected to reach $16 billion, a year-on-year increase of over 200%.

Yet the market chose to sell. The reason is not that AI demand suddenly disappeared, but that AI semiconductor assets have accumulated very high expectations over the past year. When a company with strong fundamentals can also trigger selling pressure because its AI revenue guidance falls short of some expectations, it indicates the market's pricing threshold has changed. Simply being part of the AI chain is no longer enough; the growth trajectory, profit realization, and next-quarter guidance must all justify the valuation.

This is the meaning of the June 5th plunge. It was not a test of demand collapse, but a stress test for high-expectation trades.

The main narrative for AI semiconductors in the past was more like 'who is closer to AI CAPEX (capital expenditure)'. GPU, ASIC (custom chips), high-speed optical modules, copper interconnects, equipment materials—as long as they could be placed in the AI cluster expansion chain, their valuations could receive a premium. But when the market begins to worry about crowded trades, excessive valuations, and the pace of guidance fulfillment, the question shifts from 'who has the AI story' to 'who can turn AI demand into financial reports the fastest'.

For the stock market, what ultimately determines valuation is not the orders themselves, but whether orders can translate into earnings per share (EPS). Because stock prices, in the long run, are essentially a pricing of corporate profitability. When the market starts focusing on next-quarter profits rather than a story three years from now, changes in EPS often become more important than the narrative itself.

Broadcom's role is thus also of signaling significance. It is one of the core assets in the AI ASIC and networking chip chain. Precisely because it is strong, the stock price reaction after its earnings report shows that the AI semiconductor chain is being subjected to higher verification standards.

Why Memory: Prices and Profits Are Already in the Model

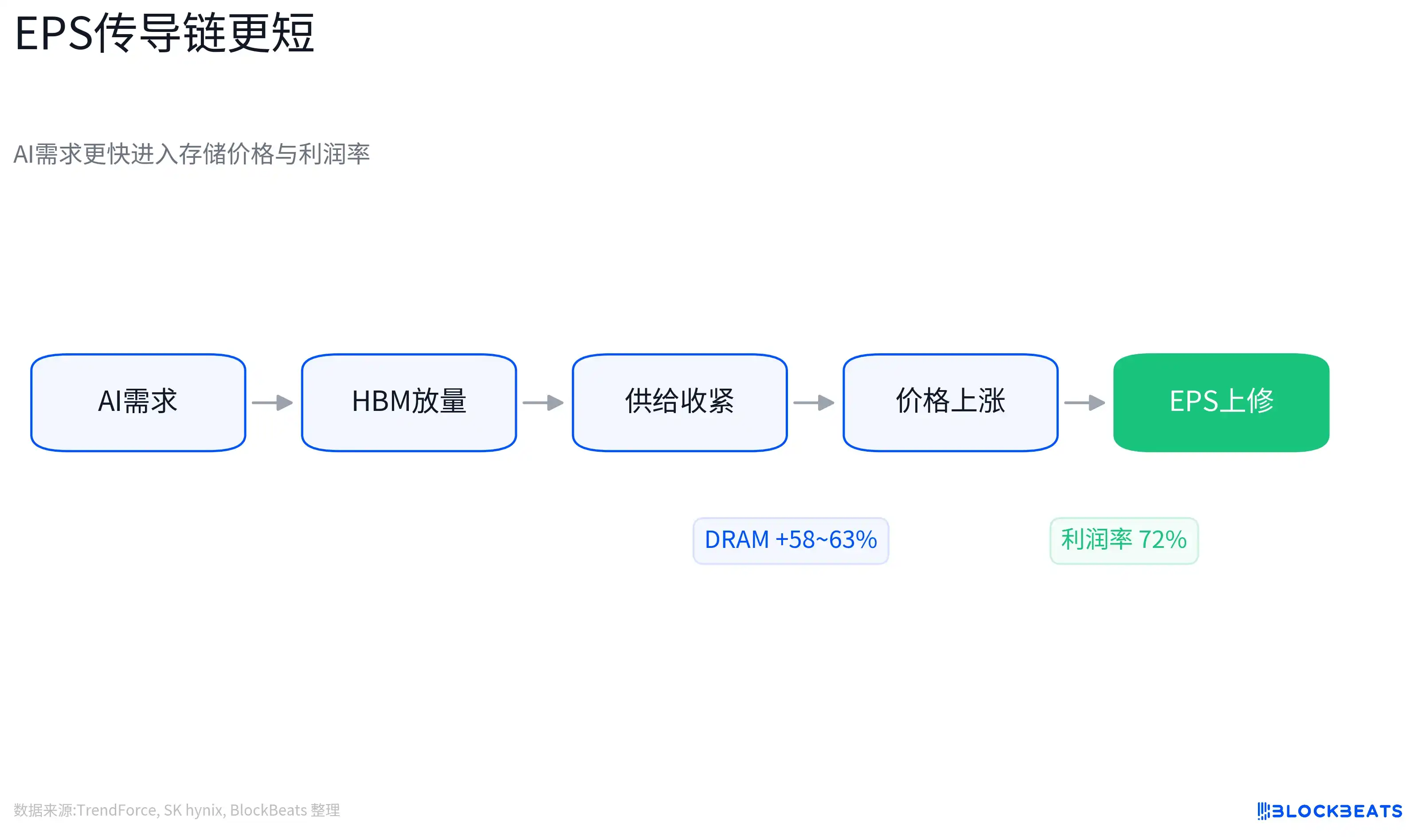

The advantage of memory is that its EPS transmission chain is shorter.

AI server demand first alters the supply-demand relationship for high-value-added products like HBM (High Bandwidth Memory), server DRAM, and eSSD (enterprise Solid State Drives). As cloud providers and AI system vendors need more computing power, they also require more GPU-compatible memory, higher-capacity server memory, and larger-scale data center storage.

When memory manufacturers shift capacity towards HBM and high-end server products, the supply of conventional DRAM and NAND will be further squeezed, leading to increases in contract prices. This chain of events does not rely entirely on distant imagination but will enter revenue, gross margins, and EPS relatively quickly.

Micron's earnings report already reflects this change. According to the company's announcement, FY2026 Q2 set records across multiple metrics including revenue, gross margin, EPS, and free cash flow, with data center-related revenue surging year-on-year. The company also guided for FY2026 Q3 to continue to set significant new highs. For Micron, AI memory is no longer a distant vision but a source of revenue entering the current quarter's statement.

SK Hynix's report is more direct. According to the company's announcement, 1Q26 revenue was 52.5763 trillion won, operating profit was 37.6103 trillion won, and the operating profit margin reached 72%. The company attributed the growth to high-value-added products such as HBM, high-capacity server DRAM modules, and eSSD. For investors, this kind of profit margin reflects the combined entry into the financial statements of product mix, supply-demand gap, and pricing power.

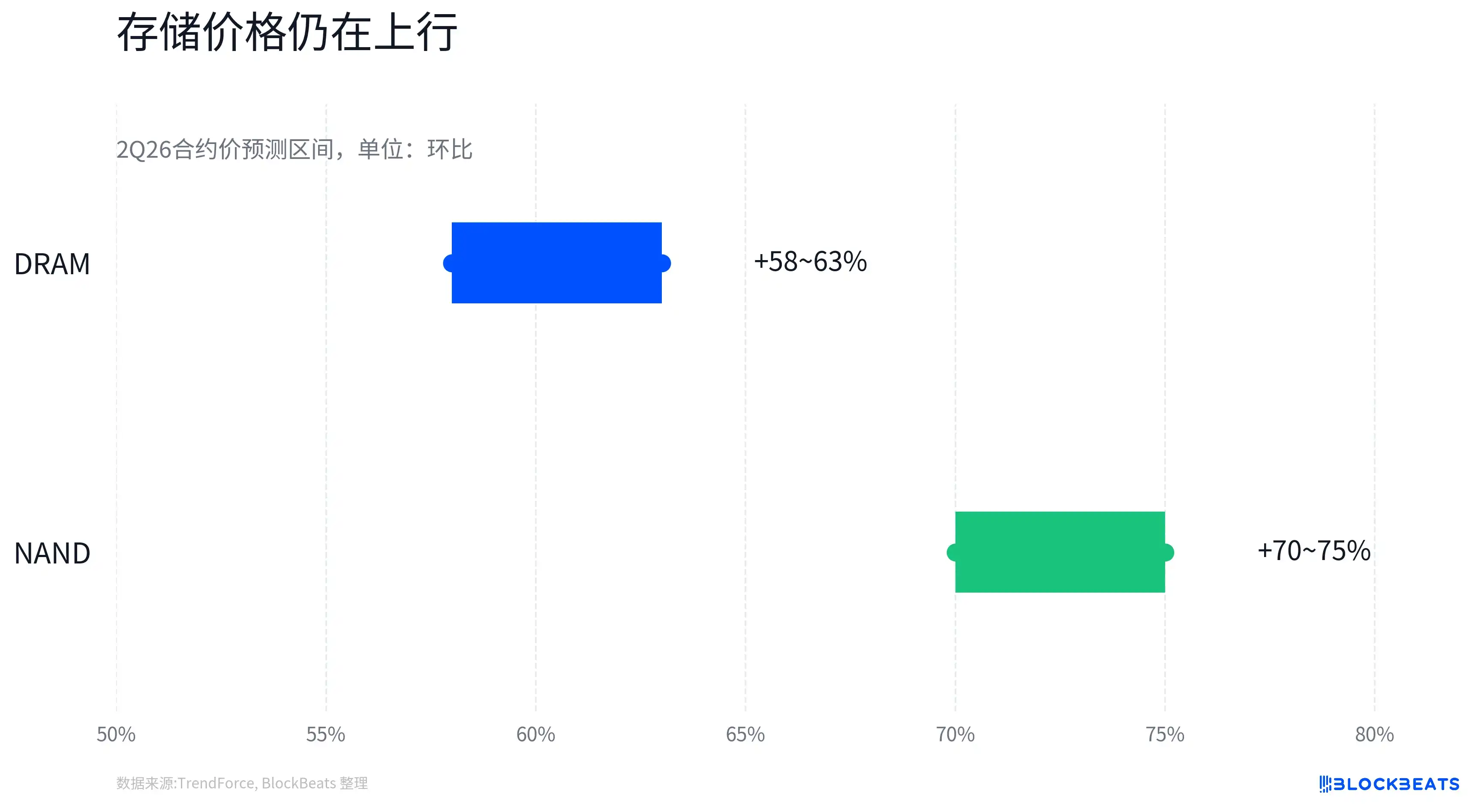

Industry price data also supports the same logic. TrendForce expects 2Q26 conventional DRAM contract prices to increase 58% to 63% quarter-on-quarter, and NAND Flash contract prices to increase 70% to 75% quarter-on-quarter. Its report also shows that 1Q26 DRAM industry revenue grew 81% quarter-on-quarter.

Prices are not equal to profits, but during periods of tight supply, shifting product mix upward, and strong demand, rising prices will improve market modeling of EPS for the coming quarters. Korean export data also provides an industry-level leading indicator. According to Reuters and Korean media reports, Korea's May 2026 exports hit a record, with semiconductor exports growing 169.4% year-on-year to approximately $37.16 billion. Chips accounted for over 40% of total exports for the first time.

This cannot be directly equated with SK Hynix or Samsung Electronics' earnings per share, but it shows that the memory boom is already reflected in the accelerating revenue at the national export level.

Memory Is Not a Stronger Narrative, But Faster Verification

In this round of revaluation, the difference between memory and other AI semiconductor directions is not whether there is growth, but how the growth is verified.

NVIDIA remains the main valve for AI demand. GPU platform iterations determine AI server architecture, HBM capacity requirements, and supply chain qualifications. However, the market is already highly familiar with NVIDIA's growth and profits, and valuations have long been concentrated on the strongest AI assets. In the short term, it is more susceptible to influences such as export controls, supply chain constraints, platform transition pace, and expectation gaps.

The ASIC direction also has genuine logic. Cloud vendors' in-house chip development, custom accelerators, and rising AI inference demand are driving the long-term potential of assets like Broadcom and Marvell. But ASIC is more like a project-based business, and factors such as customer concentration, the pace of single-project adoption, mass production windows, and next-generation platform transitions all affect the market's judgment of revenue visibility.

Optical modules and copper interconnects also have EPS realization paths. Companies like Coherent and Credo benefit from bandwidth upgrades within AI clusters; 1.6T, 3.2T optical modules, and changes in cluster interconnect architecture bring demand. However, pricing in these directions relies more on future architecture roadmaps, customer certification, shipment schedules, and capital expenditure cycles. When the market is willing to give a premium, their elasticity is strong. When the market starts demanding verification, they are also more likely to be questioned about when orders will enter revenue.

In contrast, the current pricing basis for memory is more direct. HBM demand pulls high-end products, capacity shifts squeeze conventional DRAM/NAND supply, rising contract prices improve revenue, a shifting product mix upward pushes gross margins higher, ultimately entering EPS.

This chain does not mean there are no risks, but it is easier to be verified by the next quarter's earnings report than 'future generations of architecture will bring massive orders'. This is the meaning of memory being easier to model. It's not saying memory is more important than GPU, ASIC, or optical modules, but rather that in this round of de-risking AI semiconductors, the market prefers assets that can be verified through a combination of price, orders, profit margins, and export data.

The EPS Logic Is Strengthening, But Not Yet a Consensus

A one-day or two-day rebound does not prove that AI semiconductor trading has completely shifted from PE expansion to EPS verification.

Micron's nearly 13% drop on June 5th and its nearly 10% rebound on June 8th may include technical recovery, short covering, and risk appetite recovery. SK Hynix's rise was also catalyzed by news related to data center cooperation with NVIDIA. News, positioning, and fundamentals are often superimposed in short-term market movements; not all gains can be attributed to EPS certainty.

Memory itself remains a cyclical industry. Rapidly rising DRAM and NAND prices may improve supplier profits, but may also stimulate supply expansion or suppress purchasing intentions of some end customers. HBM's annual contracts, yield ramp-ups, customer qualifications, and share allocations are still changing; one cannot simply assume all price increases will enter the profit statement without loss.

SK Hynix and Micron are already highly watched AI memory stocks, and stock price elasticity is not always synchronized with fundamental elasticity. If the future rate of DRAM/NAND price increases slows, HBM market share falls short of expectations, or customer duplicate ordering is disproven, the EPS upward revision logic will also face challenges.

Similarly, one cannot conversely negate ASIC, optical modules, copper interconnects, and equipment materials. If these directions deliver stronger orders, clearer customer adoption, or better-than-expected guidance, the market may still re-grant valuation premiums. AI semiconductors are not left with only memory as a direction; rather, at the current stage, memory can more easily explain through financial reports why it should be bought back.

A more prudent judgment of this round of market action is that the June 5th plunge raised the verification threshold for AI assets. The recovery from June 8th to 9th shows that funds, within the AI chain, currently prefer segments with shorter EPS realization paths. Memory happens to be in a position where orders, prices, capacity, and profit margins are all visible simultaneously.