While Bitcoin has been holding steady these past few days, the altcoin season has seen a long-absent surge of intense volatility.

Tokens with a circulating market cap of less than $20 million have doubled, tripled, or even increased fivefold within a few days, with some approaching tenfold gains. There were no major developments, no ecosystem breakthroughs, no new institutional entries—the price was simply pushed up.

There's a ready explanation for this phenomenon: altcoins are high-Beta assets; when Bitcoin rises, alts run even faster. This holds true statistically but doesn't tell the whole story. High Beta can explain why alts outperform Bitcoin, but it can't explain the dozens-of-times difference in gains. That multiple comes from something else.

The Altcoin Season Index currently sits at 34, and the BTC Dominance rate is 58.5%. Both numbers tell you that this market is still quite a distance from a true altcoin season. Yet, in this market devoid of an alt season, certain tokens are moving with the intensity of one.

From December 2024 to April 2026, the total market capitalization of altcoins (excluding Bitcoin and Ethereum) shrank from a peak of approximately $1.16 trillion to around $700 billion, evaporating nearly 40%. When the market cap shrinks sufficiently, the rules of the game change. Price is no longer determined by market consensus but by who holds enough chips.

This is a vulnerability created by oversold conditions, not a signal from a bull market.

Altcoins Have Simply Fallen Too Much

The blockchain space has the concept of a 51% attack—controlling more than half of a network's hash rate allows one to alter records, double-spend tokens, and rewrite history. The capital version of this is logically simpler; it requires no technology, no computing power, just money. And in this cycle, the altcoin market, with its nearly 40% evaporation in market cap, has proportionally lowered the entry barrier by 40%.

As of early April 2026, the total altcoin market cap is approximately $700 billion, down about 40% from its peak of ~$1.16 trillion in December 2024. Using end-2025 as a cutoff point, the decline is about 44%. The two measurements use different time nodes, but the direction is consistent: the overall size of this market has nearly halved.

What does a halved market cap mean? $10 million represents 2% of the circulating supply in a market with a $500 million market cap, but 20% in a market with a $50 million market cap. The threshold has been lowered tenfold, but the amount of money hasn't changed. After being oversold, the cost of controlling the market becomes calculable. And if it's calculable, it's executable.

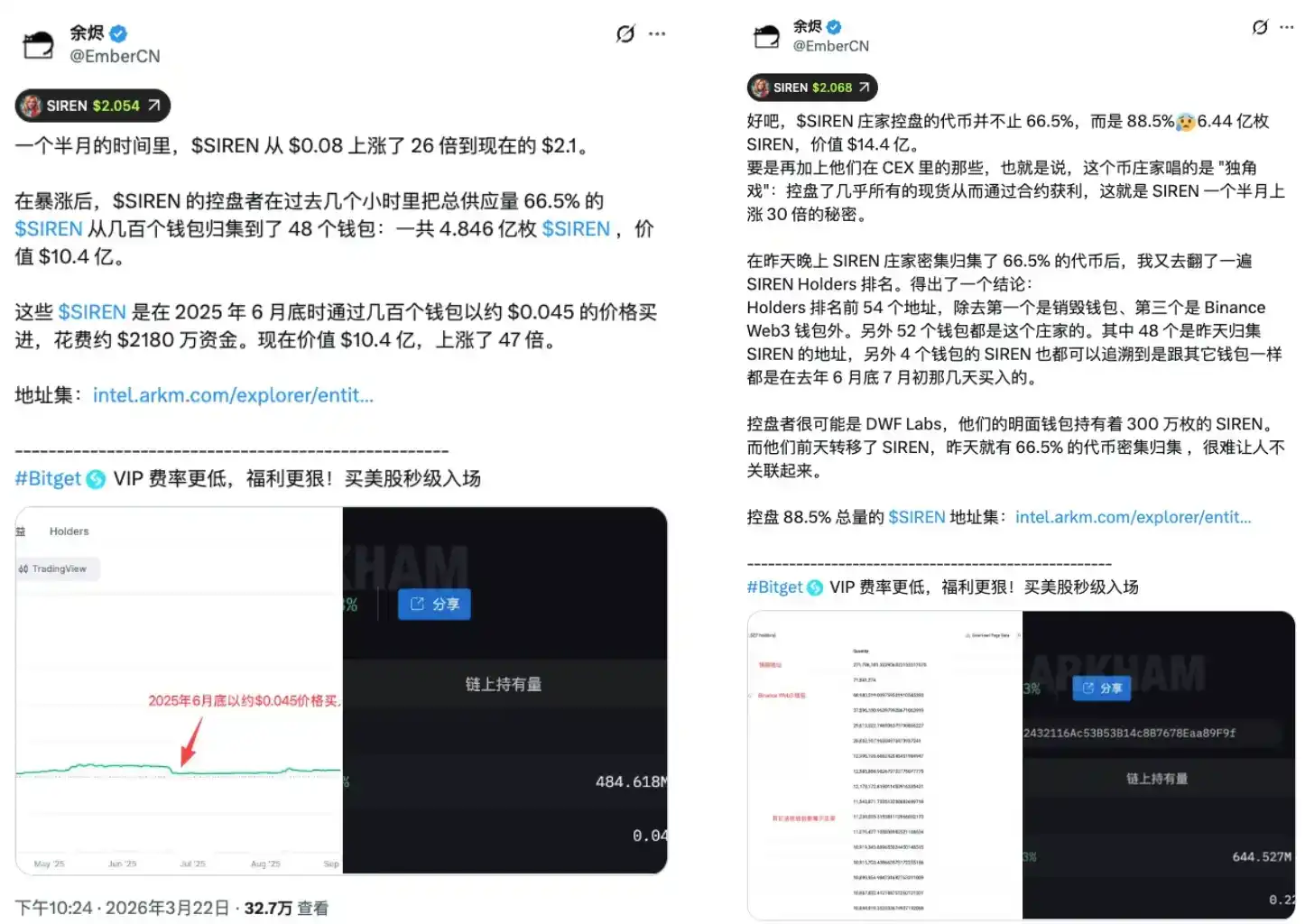

The recent sharp rise of the SIREN token provides a case study. SIREN experienced a rapid pump in late March, drawing significant attention. On March 24th, on-chain analyst EmberCN issued a warning: a single entity potentially controlled up to 88% of SIREN's circulating supply, worth approximately $1.8 billion at the time. As the news spread, SIREN plummeted from $2.56 to $0.79 that day, a drop of over 70%. During the rapid price exodus, almost no one could exit at a reasonable price because that price was never formed by the market in the first place.

A conservative estimate suggests 48 wallets hold about 66.5% of the circulating chips. Even by this most conservative measure, an extremely limited set of addresses already possesses the structural conditions to control the price direction. From the moment the price was formed, the symmetry of this game was broken. Retail traders, bringing money they thought was participating in a free market, entered a container with a pre-set exit path.

SIREN is not an isolated case, nor a black swan; it is the structural norm for oversold altcoins. The deeper the fall, the less money is needed, and the easier it is to be hijacked. Being oversold isn't a discount; it's fragility. And this cycle's overall 40% market decline means this fragility has systematically expanded across the entire market.

Shorts Are the Fuel

If the story ended there, the logic would be one-directional: whales lock up supply, pump the price, dump on retail, and the price crashes. But the行情 of ultra-low market cap alts usually has another layer of structure superimposed on it: shorts become the kindling for the fire.

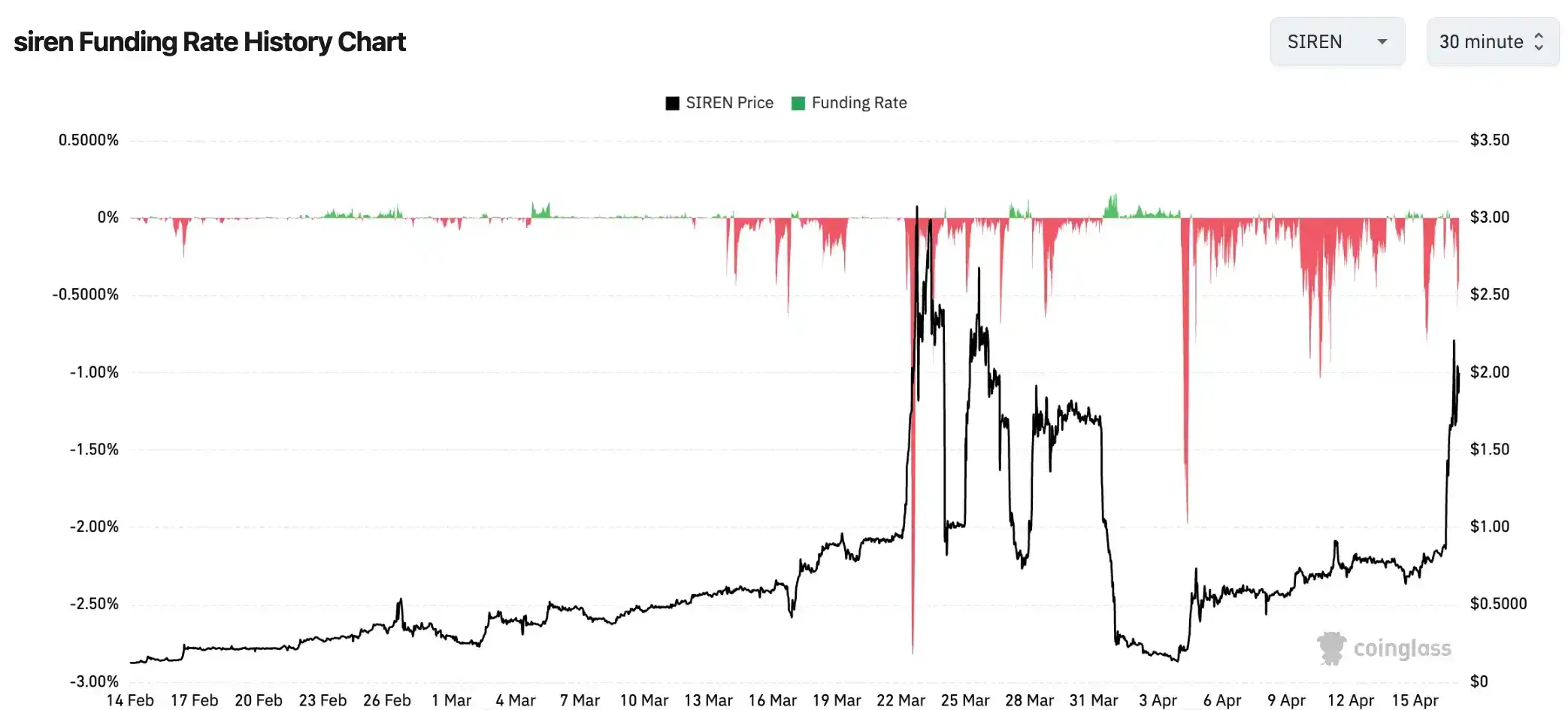

During SIREN's rapid price increase, the funding rate touched -0.2989% per 8 hours, annualized at approximately -328%. Translated, this means that shorting SIREN and holding the position requires paying the long side about 0.3% of the principal every 8 hours as a funding fee. Holding for a month, this fee alone could devour over 25% of the principal, not even counting the paper losses from the rising price.

This number is not uncommon in small-cap alt markets. Some tokens have seen funding rates as low as -0.4579% per 8 hours during extreme moves, annualized at roughly -501%. At this level, short sellers face not the risk of being wrong on direction, but the certainty of being slowly ground down by a machine. Even if the eventual direction is correct, they are depleted before the right day arrives.

You see an altcoin pump 80% and decide to short it, waiting for a pullback. Every short position you open pays an interest payment to the opposing long side. Meanwhile, if the price continues to rise and hits your liquidation price, the system automatically buys back at market price to close your position. This forced buying further pushes the price higher.

The传导链 of a short squeeze operates like this: Price rises -> Shorts show paper losses -> Paper losses hit forced liquidation levels -> System automatically buys to close positions at market price -> This buying pushes price higher -> More shorts are triggered -> A new wave of buying arrives. In thin, low-liquidity, small-cap markets, each order can cause a much larger price move, making the chain reaction far more efficient than in large-cap assets.

There is an often-overlooked asymmetry here. Someone who sees a token surge 90% and decides to short it typically believes they are making a probabilistically correct judgment: "It has to pull back after rising so much." But in a market highly concentrated and locked up by holdings, this judgment must contend not only with the price direction but also with a funding fee bleeding 0.3% of principal every 8 hours, plus the chain reaction triggered by forced buying once liquidation levels are hit. This game is asymmetric from the start.

Extreme negative funding rates are the dashboard reading of this machine. Shorts have accumulated, ammunition is loaded, and accelerating the pump now means the people on the other side have only two choices: get liquidated or FOMO in and buy high. Both choices add fuel to the price. This isn't a rise formed by market consensus; it's a one-sided consumption event with a pre-designed structure.

A Bustling Market Without New Money

BSC chain's weekly DEX volume is up 97% year-over-year; the Altcoin Season Index is 34/100; BTC Dominance is 58.5%. These three numbers can be true simultaneously, and are simultaneously contradictory.

The on-chain heat is indeed scorching, but the latter two numbers tell you this market is still in "Bitcoin Season"—fewer than half of the major altcoins are outperforming Bitcoin, dominant capital is highly concentrated in Bitcoin, far from the point of diffusion. But the three numbers also point to the same reality: this is存量资金 accelerating their circulation, not new money entering. The hustle and bustle is real, but hustle and bustle does not equal expansion.

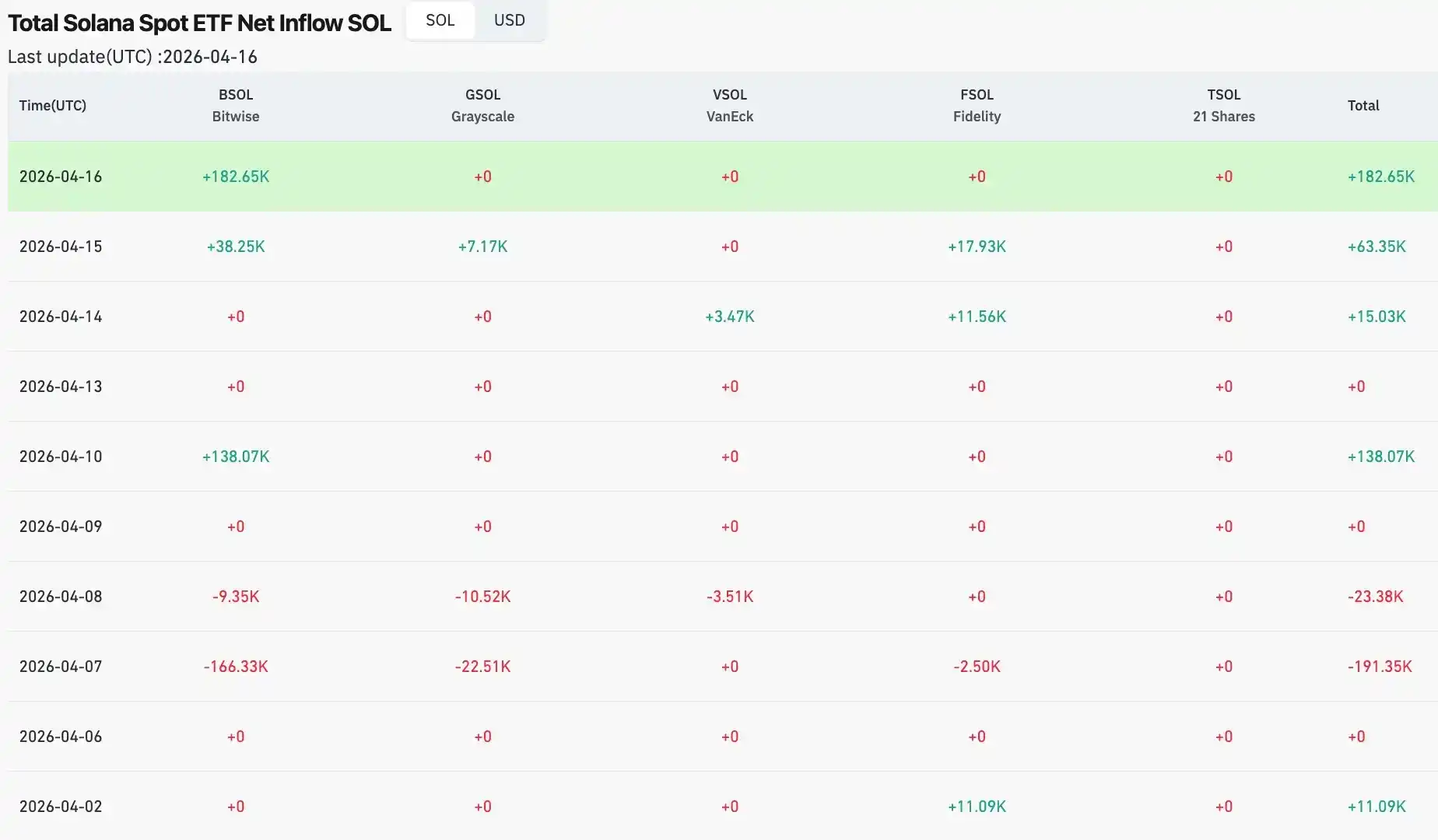

Institutional fund flows provide corroboration. In early April, net inflows for the Solana ETF fell to zero in a single day, after recording a net outflow of $6.2 million on March 30th. The XRP ETF saw continuous net outflows at the start of the month, with only a微量 inflow of about $64.6k on April 2nd. The Ethereum ETF, while seeing a single-day net inflow of $120 million on April 6th, had already experienced an outflow of $71 million the previous day. The overall pattern of institutional funds towards alts is观望, not rotation.

Comparing this to the true altcoin season of 2021 reveals a structural gap. That cycle, from the beginning of the year to May, BTC Dominance fell from over 70% to below 40%, touching a low of around 39%. The rotation of funds between Bitcoin and alts was clear, and the Altcoin Season Index once exceeded 90. That was a全面扩张 driven by泛滥的宏观流动性, with the afterglow of DeFi Summer still warm, retail FOMO entering en masse, stablecoin issuance rapidly expanding同期, and incremental funds continuously pouring into the entire ecosystem. Today's score of 34 and 58.5% dominance paint a different picture; the engine is just warming up, far from running at full speed.

There is also a variable unique to this cycle. Institutional money entering the market via ETFs follows an internal asset allocation logic, not the emotional logic of the crypto market. Institutions are doing "adjust Bitcoin allocation to X%", not "alt season is coming, load up on alts". Structurally, this capital will not spontaneously rotate into the alt market unless explicit instructions are given. This is the most fundamental structural difference between 2021 and 2026. The money that came in 2021 included a large amount of retail capital that went "wherever was hot". Today's institutional money is anchor-style, with a fixed path, not drifting with market sentiment.

The +97% on-chain volume hustle is real, but a market without new money is zero-sum. Every winner's gain corresponds to another player's loss; the total size of the pool hasn't grown.存量博弈 doesn't necessarily mean a crash, but it defines the structure of the game. The热闹 belongs only to those already in the field, those who already hold chips. Those who come in later are typically using their own money to complete the last mile of someone else's exit.

Epilogue

Returning to the data from the beginning: Bitcoin rose about 0.85% in four days, while a few small-cap tokens multiplied several times over the same period. Now you have a framework. Bitcoin's rise is one thing—the macro environment is catching its breath, institutional money is testing the waters, the market is waiting for the next clear signal. The altcoin暴拉 is another thing—low market caps post-overfall create structural vulnerabilities, small amounts of capital leverage price in thin liquidity containers, and extreme negative funding rates turn shorts into fuel for longs. These two things happening simultaneously does not mean they are telling the same story.

Altcoin Season Index 34, BTC Dominance 58.5%. By the historical standards of 2021, this machine hasn't even finished its warm-up procedure. BTC Dominance needs to fall from 58% towards the ~39% seen back then, institutional funds need to expand from "Bitcoin allocation" to "crypto asset portfolio allocation", incremental funds need to持续流入 instead of cashing out at highs. None of these are things a single price surge can solve.

There are two types of people in this machine: those who know for whom it is running, and those who are the fuel required for its operation.

BTC's rise is the signal; the altcoin暴拉 is the echo. Distinguishing between these two things is necessary to make choices in this market that aren't pre-designed by the machine.