Author:Memento Research

Compiled by: Deep Tide TechFlow

Deep Tide TechFlow Introduction: Crypto funding data for the first four months of 2026 reveals a harsh reality: the Game and DePIN sectors are nearly starved of capital, while Kalshi and Polymarket, two prediction market companies, have taken more money than all DeFi projects combined for the entire year. More alarmingly, the number of M&A deals has already matched seed rounds, indicating a shift in capital from betting on new ideas to acquiring existing leaders.

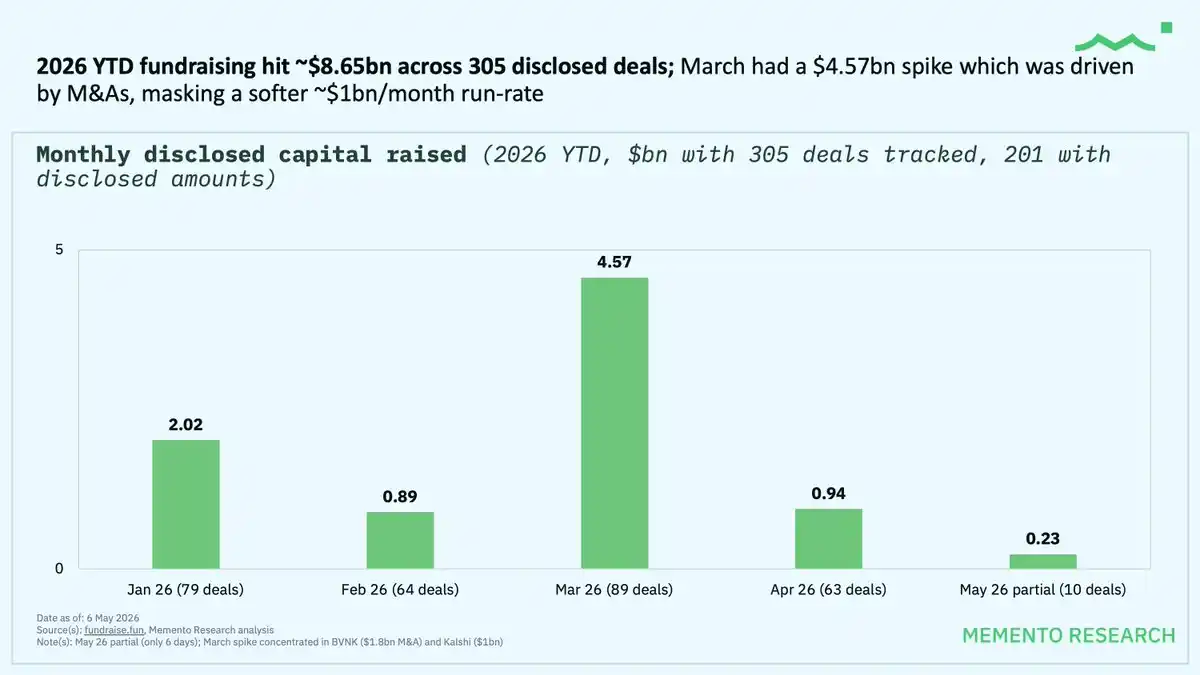

Funding Overview: March's Surge Was an Illusion

From January 1st to May 6th, 2026, the crypto industry completed 305 funding rounds, totaling $8.65 billion. However, the "surge" to $4.57 billion in March was actually just two massive M&A deals: BVNK's $1.8 billion and Kalshi's $1.0 billion.

Excluding these two deals, the real funding pace is about $1 billion per month, even weaker than at the end of 2025.

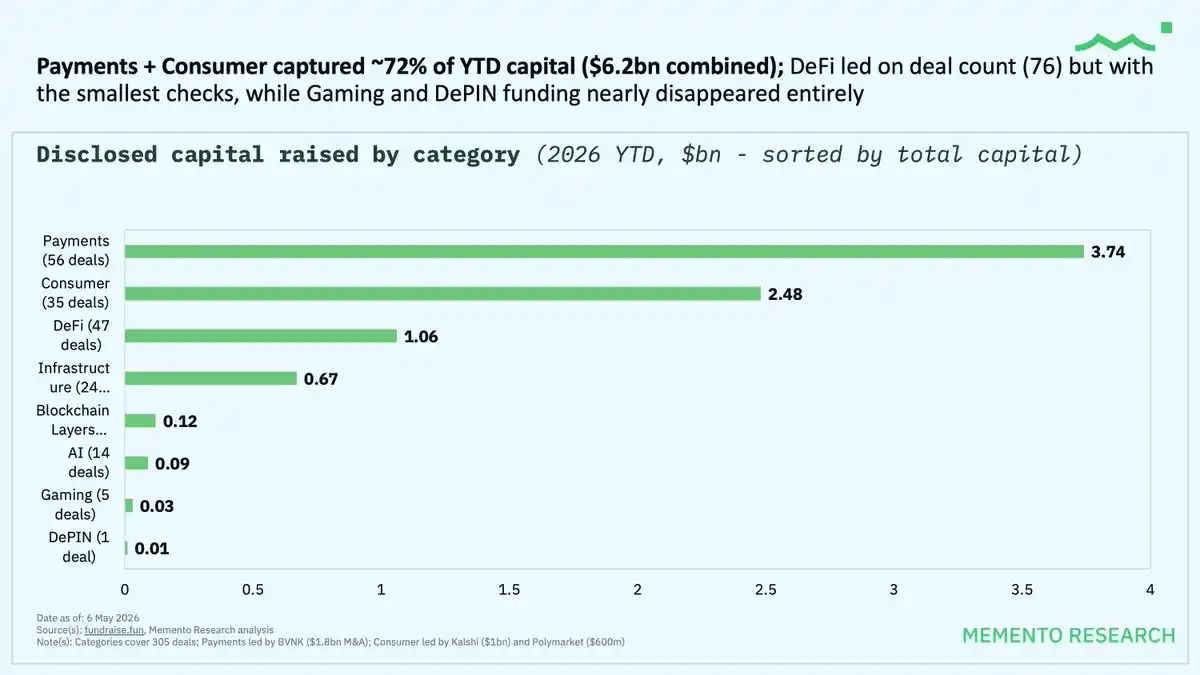

Capital Flow: Payments and Consumer Absorb 72%

By sector breakdown:

Payments: $3.74 billion (56 deals)

Consumer: $2.48 billion (35 deals)

DeFi: $1.06 billion (47 deals, the highest number of transactions)

The Payments and Consumer sectors combined account for 72% of the year's total funding. Funding for Game and DePIN has nearly vanished.

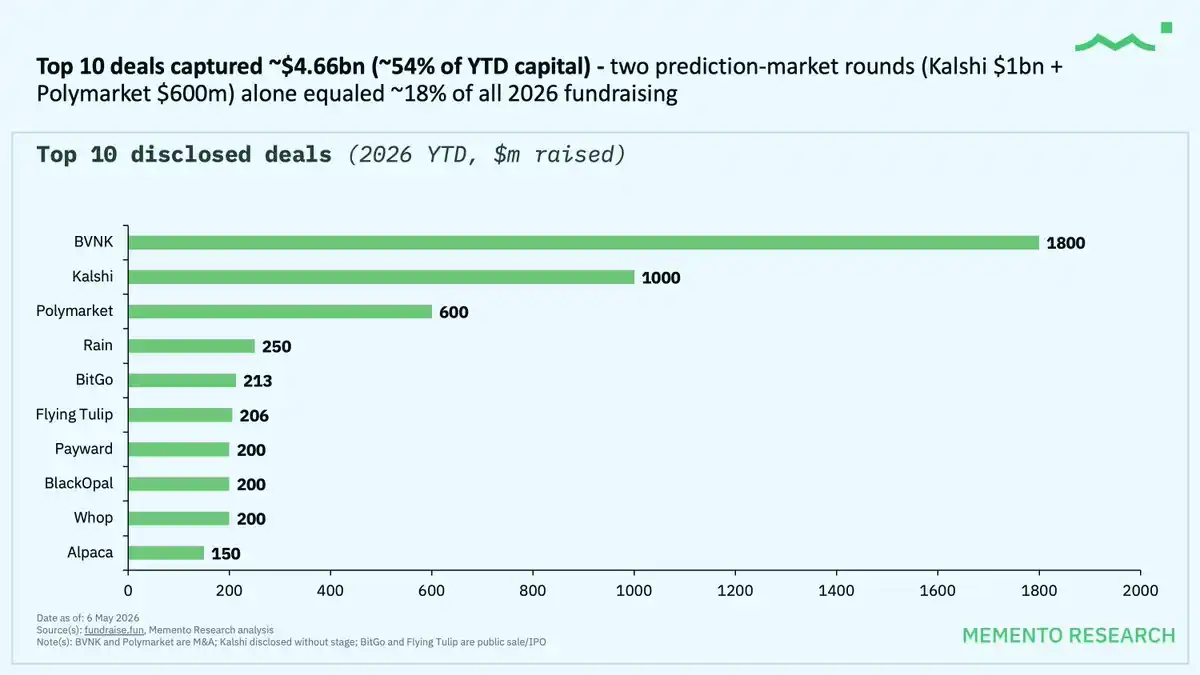

Prediction Markets Dominate the Consumer Sector

Two prediction market companies accounted for 18% of the year's total funding:

Kalshi: $1.0 billion

Polymarket: $600 million

These two deals totaling $1.6 billion exceed the sum of all 47 DeFi funding rounds.

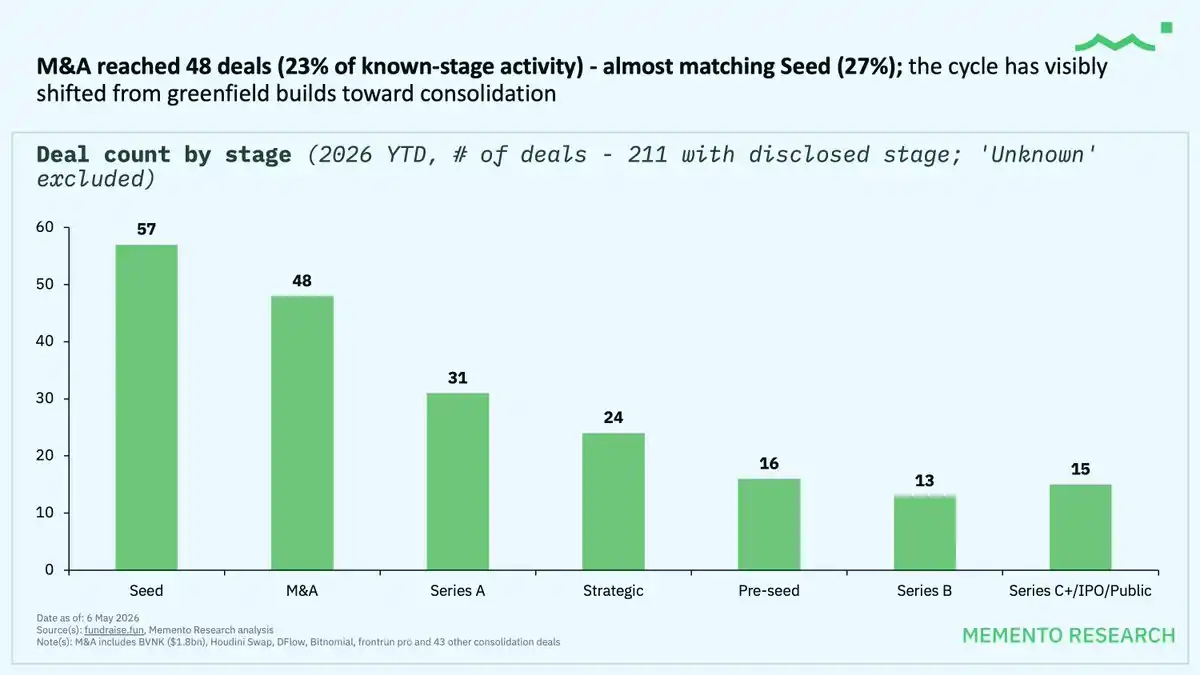

M&A Becomes Mainstream

M&A deals reached 48 (accounting for 23% of known-stage transactions), nearly matching the 57 seed rounds (27%). This cycle has shifted from investing in new ideas in early stages to acquiring industry leaders.

Investor Rankings Reshuffled

Most active funds in 2026:

Coinbase Ventures: 18 deals (ranked second during 2021-26 period)

Tether: 13 deals (new top lead investor)

Animoca Brands: 11 deals (ranked first during 2021-26 period)

GSR: 11 deals

a16z: 7 deals (a significant drop compared to ~200 deals during 2021-26 period)