Author: Tao Zhu, Jinse Finance

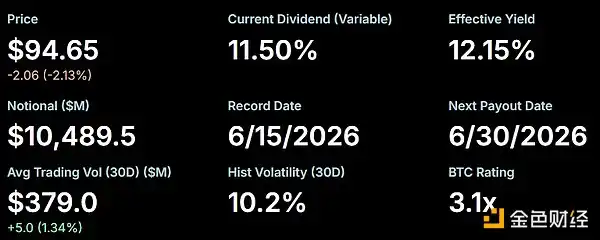

Summary: On May 29, STRC fell to $97.11 before recovering and closing at $98.57. Since then, STRC has mainly trended downward, trading at $94.65 at the time of writing. For a preferred stock designed to trade long-term around its $100 par value, such a decline has indeed drawn market attention.

1. What is STRC?

According to the Strategy website, Stretch (STRC) is the perpetual preferred stock of Strategy company. It currently has an annual dividend yield of 11.50%, paid monthly in cash. STRC's dividend rate adjusts monthly, aiming to encourage its stock price to trade around its $100 par value and reduce price volatility. STRC is listed on NASDAQ and can be traded on most mainstream brokerage platforms.

"Preferred" means having higher priority over common stock in terms of dividends and liquidation. As preferred stock issued by Strategy, STRC ranks below bonds but above common stock. Specifically, the "preference" of preferred stock manifests in two main aspects. First, priority in receiving dividend payments; preferred shareholders receive dividends before common shareholders and are the first to receive profits when earnings are insufficient. Second, priority in receiving compensation in case of company bankruptcy; compared to common shareholders who may lose their entire principal, preferred shareholders might recover part of theirs.

STRC is essentially more like a "high-yield cash flow product" rather than a growth stock seeking capital appreciation. The core purpose for many investors buying STRC is to obtain a yield above 11%, rather than focusing on whether the stock price will rise.

2. Why Has STRC Depegged Recently?

1. BTC Price Decline

Strategy's largest asset is Bitcoin, making it highly correlated with BTC's price. In late May, the overall crypto market experienced a significant pullback: BTC's price has dropped from a monthly high of around $82,000 to around $64,300 at the time of writing, a decline of 21.59%.

The rapid decline in BTC from its highs has led to a sell-off in risk assets, putting pressure on Strategy's related products.

2. Pressure from Competitors

Another Bitcoin asset management company, Strive Asset Management (ASST), has adopted a different strategy. The company recently announced that its perpetual preferred security, SATA, will distribute dividends daily. Over the past two weeks, SATA's price has remained stable around its $100 par value, maintaining a dividend yield of approximately 13% even during Bitcoin's price decline.

Over the past three months, Strive's stock price has risen about 110%, while MSTR has only risen 12%, and Bitcoin is up only 8%. This divergence suggests investors may prefer Strive's more robust balance sheet and higher-yielding preferred stock structure.

Note: Strive was originally an asset management company, founded in 2022 and headquartered in Dallas, Texas, USA. It initially focused on issuing ETF funds and was known for its "shareholder value maximization" philosophy. Starting in 2025, Strive underwent a significant transformation. It began emulating Strategy's model—becoming a Bitcoin reserve company and issuing preferred stock.

Perhaps inspired by Strive's daily dividend, according to an announcement, Strategy has proposed changing STRC's dividend payment frequency from monthly to bi-monthly. If the proposal is approved and adopted, it is expected to shorten the reinvestment lag, enhance liquidity and market efficiency, and improve price stability.

This proposal requires a joint vote by both MSTR and STRC shareholders and can only pass if both classes vote in favor. According to the proposal timeline, voting began on April 28 and will conclude on the meeting day of June 8. If approved, the first record date under the new schedule will be June 30, with the first payment date on July 15. Shareholders eligible to vote must have held shares by April 17.

3. Technical Selling

Strategy intends for STRC to maintain a price around $100 long-term. When STRC falls below $100, many quantitative funds may perceive the market as questioning the product's pricing mechanism. This could lead to issues such as passive de-risking, technical stop-losses, and arbitrage capital exiting, potentially causing the decline to widen further.

3. Does STRC Carry Default Risk?

There is no apparent default risk at present.

First, investors previously questioned whether Strategy would ultimately sell Bitcoin to repay debt or pay dividends, or continue using funds raised from securities issuance to expand its Bitcoin holdings. Saylor responded on X: "Work is proceeding nicely."

On June 1, Strategy founder Michael Saylor confirmed that the dividend yield for its perpetual preferred stock STRC would remain at 11.50% for June 2026. STRC dividends have not been cut, suspended, or defaulted; everything is proceeding normally.

Second, Strategy still possesses a massive Bitcoin reserve. With 843,706 BTC, Strategy firmly holds the top spot among corporate BTC treasuries, owning 4.01% of the total 21 million BTC. As long as BTC does not experience a long-term crash and the company's financing channels remain open, STRC's cash flow pressure remains manageable.

4. How Do Industry Insiders View This?

-

Forbes pointed out: STRC was listed in July 2025, marking the largest IPO in the US that year, raising $2.521 billion. Monthly dividend payments are approximately $80-90 million. By publicly and intentionally selling small amounts of Bitcoin to fulfill these obligations, Strategy signals to rating agencies that the company treats preferred stockholders as priority creditors. This credibility makes STRC more attractive. Increased demand for STRC means more funds raised, leading to more Bitcoin purchases.

-

Benchmark analyst Mark Palmer noted: "Investors should now view Strategy's Bitcoin holdings as a reliable backup for financing preferred stock dividends."

-

Prominent gold advocate and cryptocurrency critic Peter Schiff stated on X: "Most STRC investors are likely to lose a large portion of their money because once Michael Saylor is forced to cancel the dividend, STRC's price will ultimately crash. At that point, a wave of lawsuits is likely to further exacerbate the problems facing Strategy (MSTR). Investors who suffer losses due to misleading promotions are expected to seek compensation through legal channels to recover their investments."

-

The Motley Fool believes: First, focus on STRC's inflation problem. Inflation delivers a double blow: it erodes the real value of your $100 stock and diminishes the value of the dividends you receive. Therefore, the longer you hold this stock, the more severe the inflation problem becomes. Second, Strategy can easily cut or delay dividends without triggering a traditional debt default. Therefore, if the price falls below par, new stock issuance will stop, and you will be left holding an asset yielding less than initially advertised, with the principal potentially unrecoverable in the short term or even forever.

Summary

STRC's recent decline from around $100 to $94.65 is primarily influenced by factors including the Bitcoin price drop, competitor impact, and technical selling. Currently, STRC shows no apparent default risk; the company continues to pay dividends at the 11.5% level and consistently uses it as a core financing tool.