Author:Nancy,PANews

The South Korean stock market, which had been on a continuous upward trajectory and was approaching the 9,000-point mark, recently took a sharp turn downward. The successive corrections have left the heavily leveraged and debt-fueled "Ant Army" treading on thin ice.

Following a "Black Friday" last week, the South Korean stock market experienced another severe plunge this week. The KOSPI index opened with a steep dive, triggering a circuit breaker, and the two major market bellwethers, Samsung Electronics and SK Hynix, both hit their daily down limits. As the selling wave swept the market, panic quickly spread, prompting even Lee Jae-myung and Jensen Huang to step in for "emergency market rescue."

From Nationwide Euphoria to Collective Stampede, the 'Ant Army' Panics Collectively

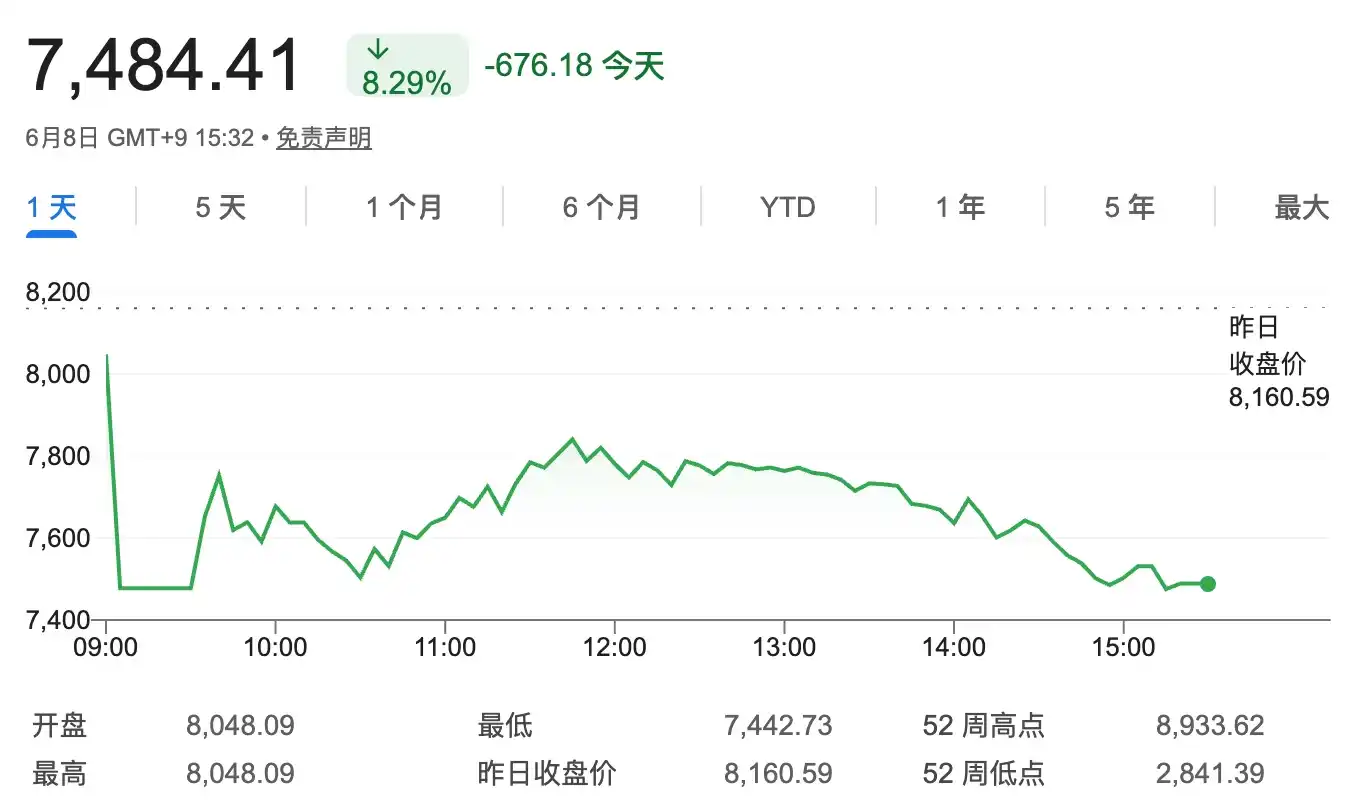

On June 8, the South Korean stock market continued the sharp decline from last Friday.

Shortly after the opening, the KOSPI index fell by over 8%, triggering the circuit breaker mechanism. The Korea Exchange (KRX) urgently suspended trading for 20 minutes. Facing the severe market volatility, the KRX held an emergency meeting that morning to assess market risks and study countermeasures to stabilize market operations.

Yet, just a week earlier, the South Korean stock market was one of the hottest in the world. Driven by the AI semiconductor boom, the KOSPI index had been repeatedly刷新历史 highs and was once challenging the 9,000-point mark. Massive funds flooded into the tech sector, with South Korea's "Ant Army" adding leverage and borrowing money to enter the market, hoping to ride this AI wealth train.

However, within just a few days, the market sentiment shifted drastically. The "Ant Army" that entered at high levels collectively panicked, openly stating they were afraid to open their accounts. In South Korea, retail investors are commonly called "ants," similar to American retail investors calling themselves "apes." Although individual power is limited, their sheer numbers allow them to "swarm" the market like an ant colony, influencing stock price movements. This group is mainly divided into two categories: "Donghak Ants" who buy domestic stocks and "Seohak Ants" who swarm into overseas markets like the US stock market.

The trigger for this round of暴跌 came from a collective correction in US tech stocks. As the South Korean stock market heavily relies on the semiconductor industry, the two chip giants Samsung Electronics and SK Hynix have almost become the core force supporting the entire bull market. In the KOSPI index, the combined weight of these two companies is as high as 54%, and their average daily trading volume accounted for about half of the index's total turnover in May. Nearly three-quarters of the KOSPI index's gains this year came from these two companies. On the day the KOSPI hit its all-time high last Tuesday, only 2.6% of the index's components reached new 52-week highs, while 31% of stocks fell to 52-week lows.

To some extent, the South Korean stock market experienced a bull run dominated by Samsung Electronics and SK Hynix, with SK Hynix employee uniforms even becoming "shedding singles battle robes." Therefore, when the correction in US tech stocks triggered a revaluation of the AI industry chain's valuation, Samsung Electronics and SK Hynix quickly became targets of selling, with their single-day跌幅 both approaching 10%, directly dragging down the entire South Korean stock market into a significant decline.

Simultaneously, foreign capital withdrawal and the depreciation of the Korean Won further intensified market pressure. The stronger-than-expected latest US non-farm payrolls data reinforced market expectations for interest rate hikes and boosted the short-term strength of the US dollar, leading international funds to begin withdrawing from emerging markets like South Korea. In just last week, foreign investors net sold over $10 billion worth of Korean stocks. The massive capital exodus not only hit the stock market but also impacted the foreign exchange market. The Korean Won rapidly weakened against the US dollar, falling to its lowest level since the 2009 global financial crisis. The asset depreciation risk brought by the currency depreciation further prompted overseas funds to leave, creating a dual attack on both stocks and the currency.

More importantly, after a prolonged period of rapid gains, the South Korean stock market itself had accumulated a large number of profit-taking positions. Coupled with the concentrated bets on the AI and semiconductor sectors by a large amount of margin financing and leveraged ETFs, when leading stocks fell, margin pressure and passive selling jointly triggered a stampede effect, further amplifying market volatility.

Facing the剧烈 market震荡, South Korean President Lee Jae-myung urgently stepped forward to voice support, emphasizing that the South Korean stock market is still undervalued, and stated that South Korea will advance the integration of AI across all industries and prepare large-scale investment projects related to the chip industry.

Adding a dramatic touch, the sharp correction in the South Korean stock market coincided with NVIDIA CEO Jensen Huang's visit to South Korea. During his visit, he announced a collaboration between NVIDIA and SK Hynix and revealed plans to meet with Samsung's leader. This move was specifically seen as a vote of confidence in South Korea's semiconductor industry.

Leveraged Stock Trading, 'Herd Effect' Raises Regulatory Concerns

Just as the cryptocurrency trading frenzy once swept South Korea, South Koreans are now bringing the same疯狂 to the stock market.

Public data shows that active stock trading accounts in South Korea have exceeded 102 million, while the total population is approximately 51.6 million. This means the average person has nearly two stock accounts. The investment enthusiasm has even appeared among minors. In Q1 this year, the number of new accounts opened by minors surged nearly 10 times year-over-year. Many parents open accounts for their children immediately after birth, buying ETFs as their life's first investment.

This investment狂热 has permeated the daily lives of South Koreans. Every day around 3:30 PM, close to the market close, restroom stalls in many office buildings and shopping malls in Seoul become "impossible to find." Many office workers hide in restrooms to check行情 and operate their accounts; some simply take leave to monitor the盘 full-time at home; tech-savvy individuals have even developed a看盘 website called "Excel Kospi," disguising the stock interface as office software, allowing employees to trade stocks "openly" under their boss's watchful eye.

Driving this全民炒股持续升温 is the惊人的赚钱效应.

According to Shinhan Investment Corp statistics, in Q1 2026, investors who sold Korean stocks and realized profits accounted for as high as 80%. These profitable investors earned an average of 8.48 million won (approximately $4,654). Among them, Samsung Electronics became the biggest cash machine, with average profits reaching 7.14 million won (approximately $4,654); SK Hynix followed closely, with average profits around 5.94 million won (approximately $3,871). In contrast, the remaining 20% of losing investors suffered average losses of about 4.96 million won (approximately $3,232).

The massive赚钱效应 further ignited market FOMO (Fear Of Missing Out) sentiment. More and more investors, fearing missing the bull market, rushed into the market, even willing to borrow money to trade stocks.

As of the end of May 2026, the margin loan balance at South Korean securities firms soared to a record 38 trillion won (approximately $247 billion), a significant increase from 27.3 trillion won at the end of 2025. Simultaneously, a large portion of new loan funds did not flow into real estate but was entering the stock market. As of the end of May, personal credit loan balances at South Korea's five major commercial banks reached 106.99 trillion won, of which overdraft account balances rose to 41.93 trillion won, the highest level since 2021. In contrast, housing mortgage loans showed almost no growth during the same period.

Moreover, South Korean散户 are increasingly using leveraged ETFs as everyday investment tools, massively employing leverage to bet on the market.

For many South Korean散户, leveraged ETFs are no longer high-risk investment instruments but essential weapons to amplify returns. Stimulated by the bull market atmosphere and赚钱效应, more and more investors believe that as long as they bet in the right direction, leverage means faster wealth growth.

According to data released by the Korea Exchange (KRX) in April this year, since the beginning of the year, the average daily trading volume of 1,093 ETF products in the South Korean market totaled 4.483 billion shares. However, the average daily trading volume of just 88 leveraged ETFs, inverse ETFs, and double inverse ETFs reached 4.046 billion shares, accounting for 90.49% of all ETF trading volume. In other words, the main trading force in the South Korean ETF market is almost entirely concentrated in high-risk leveraged products.

In South Korea, investors must complete a 1-hour online education course before trading leveraged ETFs; if trading single-stock leveraged ETFs, an additional 1-hour training is required. However, this risk firewall has not dampened investor enthusiasm. According to disclosures from the Korea Financial Investment Institute (KOFIA), the average monthly number of course completions was about 7,579 people three years ago, but has surged nearly 20 times to an average of 149,948 people per month this year. Among them, many investors simply open the course video and let it play in the background to meet the account opening requirements, without caring about the operational mechanisms of leveraged products and their potential risks.

In response to the暴涨 in market leverage demand and to attract funds back to the domestic market, South Korean regulators recently approved the listing of the first batch of single-stock leveraged ETFs. Eight asset management companies一口气 launched 16 ETFs linked to Samsung Electronics and SK Hynix with double leverage and inverse structures, hoping to lure the previously large flow of "Seohak Ants" (South Korean散户 investing in the US) back to the South Korean stock market, while boosting the performance of Korean stocks and stabilizing the Korean Won exchange rate. On the first day of product launch, due to excessively火爆 application numbers, the website of the Financial Investment Education Center of the Korea Financial Investment Association experienced temporary故障 due to a surge in访问量.

According to data from South Korean securities calculation company ETF Check, from June 1 to 5, the ETF with the largest net purchases by individual investors was the KODEX Samsung Electronics Leverage ETF, and the top four ETFs by individual net purchases were all single-stock leveraged products related to Samsung Electronics and SK Hynix. Meanwhile, data from the Korea Exchange shows that in the first five trading days after their launch on May 27, the trading volume of the four most actively traded single-stock leveraged ETFs accounted for 21% of the total trading volume of South Korean ETFs.

However, leverage can amplify returns but also magnify losses exponentially. Especially when more and more散户 use margin funds and leveraged ETFs to concentrate bets on a few popular tech stocks, it can easily trigger more剧烈 stampede effects. Precisely because of this, South Korea's Finance Minister, Choo Kyung-ho, recently stated he is concerned about the increase in leveraged stock investments and will take immediate measures when necessary to address the "herd effect" in financial markets.

Babies Open Accounts to Buy ETFs, Seniors Cash Out Insurance to Borrow Money for Stock Trading

In this stock market热潮, "silver funds" have become a significant force in the South Korean stock market.

According to a report by Korean media Chosun Biz, recently, the business网点 of major South Korean securities firms have been packed with people, and the vast majority of investors coming in person to咨询开户 and place orders are seniors aged 60 and above. Some even plan to use their bank overdraft limits to buy hot stocks like SK Hynix. A securities firm employee感慨, "I really don't know where clients are getting so much money from. From young children to the elderly, it feels like there's no one who isn't trading stocks anymore."

Looking at margin data, investors aged 50 and above account for 62.3% of the total margin amount at the top ten securities firms; the margin balance for the group aged 60 and above激增 from about 3.95 trillion to 8.02 trillion won within a year.

To raise funds, many seniors have even提前解约 insurance products, investing their原本用于养老 savings into the stock market. In Q1 2026, the surrender amount at South Korea's three major life insurance companies reached 4.9 trillion won, a year-over-year increase of 16.3%, with savings-type life insurance surrenders growing over 23.2%.

In fact, besides stock trading, more and more South Korean seniors have also begun炒币. As of the end of 2025, the number of investors aged 70 and above among South Korea's top five crypto asset exchanges increased from 30,000 in 2022 to 116,000 in 2025, nearly quadrupling in three years.

However, the large-scale entry of seniors into stock trading also raises concerns.

Many newly entered高龄投资者 have very limited understanding of the basic processes and risks of stock trading. Some don't even understand the fund settlement mechanism after selling stocks but have already begun频繁买卖股票; many are not acting based on their own research and investment judgment but hastily entering the market after hearing about profits made by friends and relatives through popular stocks like Samsung Electronics and SK Hynix.