Author: Xiaobing, Chaoxiang Research

June 1, 2026, Taipei Music Center. Wearing his signature leather jacket, Jensen Huang unveiled the Vera Rubin architecture and the blueprint for the next generation of AI factories. Beneath this highly anticipated keynote, a dominant theme for the first half of 2026 has become crystal clear:

NVIDIA is betting big on light.

In March, NVIDIA invested $2 billion each in Lumentum and Coherent, locking down capacity and technology roadmaps for next-generation silicon photonics lasers. In May, NVIDIA invested another $500 million, partnering with century-old fiber optic giant Corning, aiming to boost US domestic optical connectivity manufacturing capacity tenfold and increase fiber optic capacity by over 50%. On June 2nd, Jensen Huang publicly stated at the event, "Marvell has the potential to become the next trillion-dollar company."

Stand in the light, believe in the light. This once-memed phrase from the A-share market is now being turned into an industry consensus by Jensen Huang with real money.

Imagine building ten thousand skyscrapers in a vast city, each housing tens of thousands of genius mathematicians (GPUs) who are solving massive problems every second. The question arises: after these mathematicians finish their calculations, how do the answers get out? How do the buildings collaborate?

If you only built country lanes (traditional copper cables) for them, even the most brilliant minds would be left idle. No matter how fast they calculate, if the data gets stuck in transit, the entire city grinds to a halt.

This is the real dilemma facing AI data centers today.

Since the emergence of ChatGPT, AI has ignited GPU (computing power), HBM (memory bandwidth), and CPU (scheduling), birthing one trillion-dollar market cap company after another. But within AI infrastructure, there's another crucial component: data transmission.

And the core carrier for data transmission is the optical module.

As traditional optical modules also begin to lag behind AI's appetite, a next-generation technology called CPO (Co-Packaged Optics) is rising strongly.

This article will explain from "What is an Optical Module" to "Why CPO is the Future," to "Which Companies Upstream and Downstream Are Worth Watching," demystifying this trillion-dollar track in the simplest terms.

一、 Optical Modules: The "Simultaneous Interpreters" of Data Centers

1.1 Why Light?

Inside a data center, chips communicate using "electrical signals," much like the electrical impulses in the human nervous system. But electrical signals have a fatal flaw: they don't travel far, and they distort easily at high speeds.

Transmitting electrical signals over copper cables is like pushing water through a pipe; over long distances, the pressure drops; with narrow pipes, the flow rate is limited. Currently, copper cables have a maximum transmission distance of about 2 meters, with a bandwidth ceiling around 1.8 TB/s.

Optical signals are completely different. Light travels through fiber optics like a bullet through a vacuum tube, with almost no attenuation, extremely fast speed, and immunity to electromagnetic interference. A fiber optic strand as thin as a human hair can theoretically transmit dozens of Tbps of data simultaneously.

But here's the problem: chips only "understand" electrical signals, and fiber optics only "carry" optical signals.

Therefore, we need a "simultaneous interpreter" that translates electrical signals into optical signals for transmission and translates received optical signals back into electrical signals.

This interpreter is the optical module.

1.2 What's Inside an Optical Module?

If you disassemble an optical module, it's essentially a precision translation box, with several key components playing these core roles:

Transmitter Side (Electrical → Optical):

- Driver: It "steps on the gas" for the weak electrical signal from the chip, amplifying it to a strength sufficient to control the laser's light emission. It's like an amplifier in front of a microphone; without it, the sound is too soft for the laser to "hear."

- Modulator: It takes the amplified electrical signal and controls the brightness and timing of the light, "writing" the 0s and 1s of the digital signal onto the light. It doesn't generate light itself; it only "conducts" the light.

- Laser: The true "light source," continuously emitting a stable laser beam. The modulator controls its light to "write."

Receiver Side (Optical → Electrical):

- Photodetector / Photodiode (PD): Receives the optical signal coming from the fiber and converts it back into a very weak electrical current, much like the human retina converting light into neural signals.

- Transimpedance Amplifier (TIA): The current signal generated by the PD is too weak. The TIA amplifies it into a voltage signal that subsequent circuits can process, equivalent to amplifying a whisper to normal speaking volume.

Signal Restoration:

- Digital Signal Processor (DSP): Electrical signals "distort" over long-distance transmission. The DSP is like Photoshop, responsible for restoring a blurry image to clarity. It consumes significant power and is one of the most expensive and power-hungry components in an optical module.

- Clock and Data Recovery (CDR): Re-establishes the precise timing within the degraded signal, ensuring the intervals between 0s and 1s are accurate. Typically integrated into the DSP.

Optical Path:

- Waveguide: Microscopic optical fibers "printed" onto the chip's interior, guiding the propagation of optical signals.

- Fiber Optic Interface: The physical interface connecting the optical module to the external fiber optic cable.

In a nutshell: Optical Module = Light Source + Modulator + Photodetector + Driver/Amplifier Circuits + Signal Restoration Chips.

1.3 The "Rate Evolution" of Optical Modules

The speed development of optical modules can be compared to mobile communication iterations:

Each doubling in speed signifies a technological upgrade and value reassessment for the entire supply chain. Currently, we are at the critical juncture of transitioning from 800G to 1.6T. This is why the optical module sector has become the hottest track in the A-share market over the past year, with the Wind Optical Module Index rising over 500% from its 2025 low.

二、CPO: "Soldering" the Interpreter Next to the Brain

2.1 Bottlenecks of Traditional Optical Modules

Traditional pluggable optical modules are like USB devices—plug and play, easy to replace. This design is flexible and convenient but faces three major bottlenecks in the AI era:

Bottleneck One: Bandwidth Ceiling

Traditional switch panels have limited space, and the size of pluggable optical modules is hard to shrink. Currently, a single module supports up to 1.6Tbps, with a single switch limit of 51.2Tbps. Future 3.2Tbps modules might push switch capacity to 102.4Tbps, but this is nearly the physical limit for the pluggable form factor.

Bottleneck Two: Power Explosion

Each GPU requires 6 pluggable optical modules, each consuming about 30 watts. Building a supercluster with 1 million GPUs would mean optical module power consumption alone reaches 180MW, equivalent to the electricity usage of a medium-sized city. Completely unsustainable.

Bottleneck Three: Signal Attenuation

Pluggable modules are installed at the edge of the switch panel, separated from the core ASIC chip by long PCB traces. The higher the transmission rate, the more severe the electrical signal attenuation over this "last mile," forcing the addition of more signal restoration chips (DSPs), further increasing power consumption and latency.

2.2 What is CPO?

The core idea of CPO (Co-Packaged Optics) is simple: place the interpreter right next to the brain.

Specifically, it involves integrating the "optical engine" responsible for optical-electrical conversion directly onto the same substrate or interposer as the switching chip (ASIC). It's no longer a pluggable peripheral but a chip-level "native integration."

Here's an analogy:

- Traditional Optical Modules: Like making a phone call with Bluetooth headphones. The signal goes from the phone, undergoes Bluetooth encoding, travels wirelessly, gets decoded by the headphones—loss and delay at every step.

- CPO: Like speaking directly into the ear, removing all intermediate steps—fast and power-efficient.

According to NVIDIA data, applying CPO can improve power efficiency by 3.5x. IDTechEx predicts the CPO market will grow at a 37% CAGR starting in 2026, exceeding $20 billion by 2036.

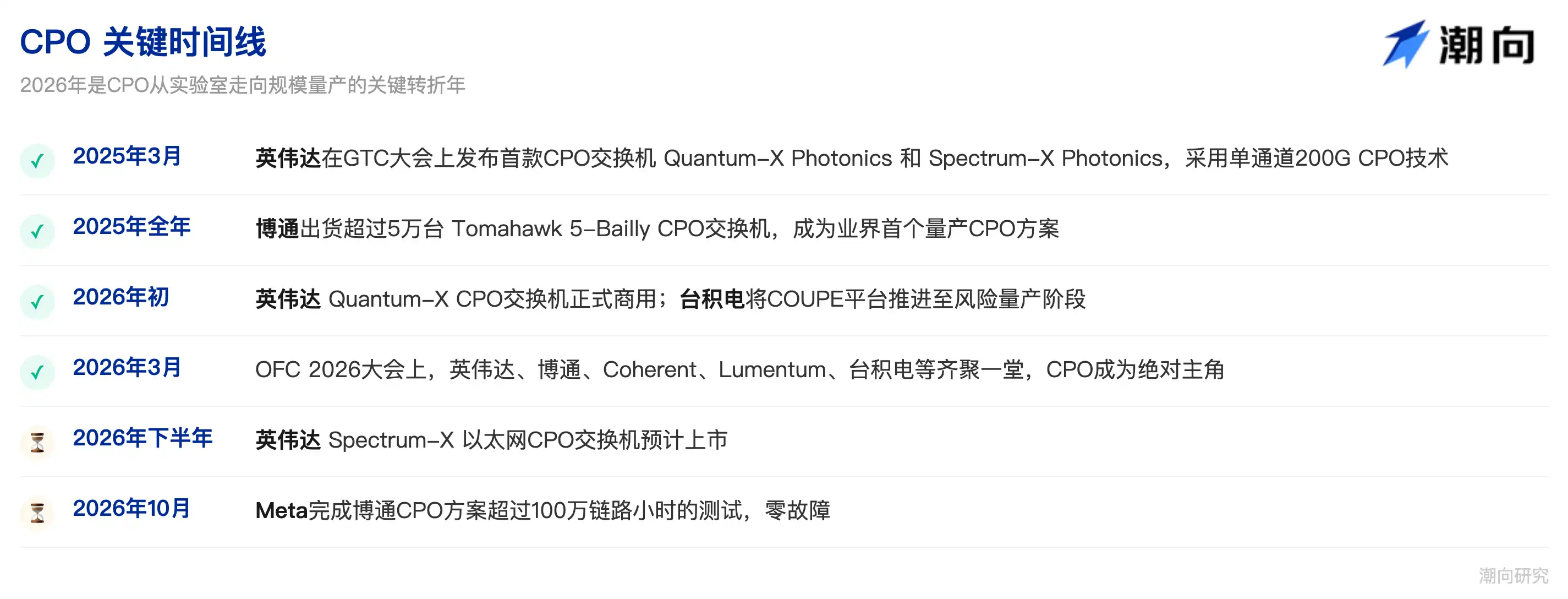

2.3 Key CPO Timeline

2.4 Challenges Facing CPO

Although CPO represents the future direction, it still has several hurdles to overcome:

Advanced Packaging Capacity: CPO requires "heterogeneous integration" of photonic circuits and electronic circuits. This requires cutting-edge packaging technologies like TSMC's COUPE/SoIC. Currently, capacity is limited, yields are improving, and costs are far higher than traditional solutions.

Maintenance and Repair: A failed traditional optical module can simply be pulled out and replaced. But CPO is "soldered" onto the chip. Repairing it is extremely difficult if it fails, requiring redundancy design and fault tolerance mechanisms.

Thermal Management: High-density packaging of optical engines and chips together can cause local temperatures to exceed the laser's tolerance limits, necessitating more efficient cooling solutions.

Standardization: NVIDIA, Broadcom, and others are promoting their own solutions. A unified industry standard has yet to be established, making it difficult for the supply chain to develop and produce based on a common interface.

三、Technology Roadmap Panorama: CPO Isn't the Only Player

Alongside CPO, several related technology paths are advancing in parallel. Understanding these clarifies each company's competitive position.

3.1 NPO (Near-Packaged Optics)

NPO is a "simplified version" of CPO. Instead of integrating the optical engine into the ASIC's substrate/interposer, it's placed on the same PCB motherboard. The distance is closer but not "face-to-face" like CPO.

This is a pragmatic compromise, especially in the Chinese market, which lacks TSMC-level advanced packaging capacity. Alibaba, Huawei, and others are actively promoting NPO. Huagong Tech has already launched the world's first 3.2T NPO product, deployed with a leading customer.

NPO can be seen as a "transitional state" towards CPO, serving as the mainstay in the Chinese market in the short term but evolving towards CPO in the long run.

3.2 OIO (Optical I/O)

If CPO integrates the optical engine with the switching chip, OIO is a more radical version—integrating the optical engine directly with the computing chip (GPU/XPU) or even integrating it at the chip level.

OIO targets intra-rack scenarios (Scale-up), replacing copper cables. Ayar Labs is a pioneer in this field, having demonstrated a fully CPO-based Scale-up rack prototype with Wiwynn at OFC 2026.

OIO is expected to see scaled adoption in GPU interconnect scenarios around 2028-2030.

3.3 LPO (Linear-drive Pluggable Optics)

LPO is a "slimming down" of traditional optical modules, directly removing the power-hungriest DSP chip and relying on analog amplification. Benefits: lower power consumption and cost. Drawbacks: higher signal quality requirements, limited long-distance transmission, and potential bottlenecks above 1.6T.

LPO can be seen as a "life extension" for traditional modules but doesn't change the overarching trend towards CPO.

3.4 OCS (Optical Circuit Switch)

OCS is a special type of switch that doesn't perform optical-electrical conversion. Instead, it routes optical signals directly in the optical domain using "micro-mirror arrays"—like tiny, adjustable mirrors "bouncing" light in different directions.

Google is the biggest proponent of OCS, using it to replace traditional Spine switches. The advantage of OCS is extremely low power consumption (no optical-electrical conversion needed), but it can only "forward" light; it lacks "intelligence" (it can't unpack packets, read addresses, and decide routing). Therefore, OCS is only suitable for replacing the Spine layer and cannot fully replace Leaf switches.

CPO and OCS are more complementary than competitive: OCS handles all-optical forwarding at the Spine layer, while CPO handles optical-electrical conversion at the Leaf and server layers. They can coexist.

3.5 Technology Roadmap Summary

四、CPO Supply Chain Panorama: Who's Getting a Piece of the Pie?

CPO isn't a single product but a complex system engineering project involving numerous upstream and downstream segments. Understanding these segments is key to identifying investment opportunities.

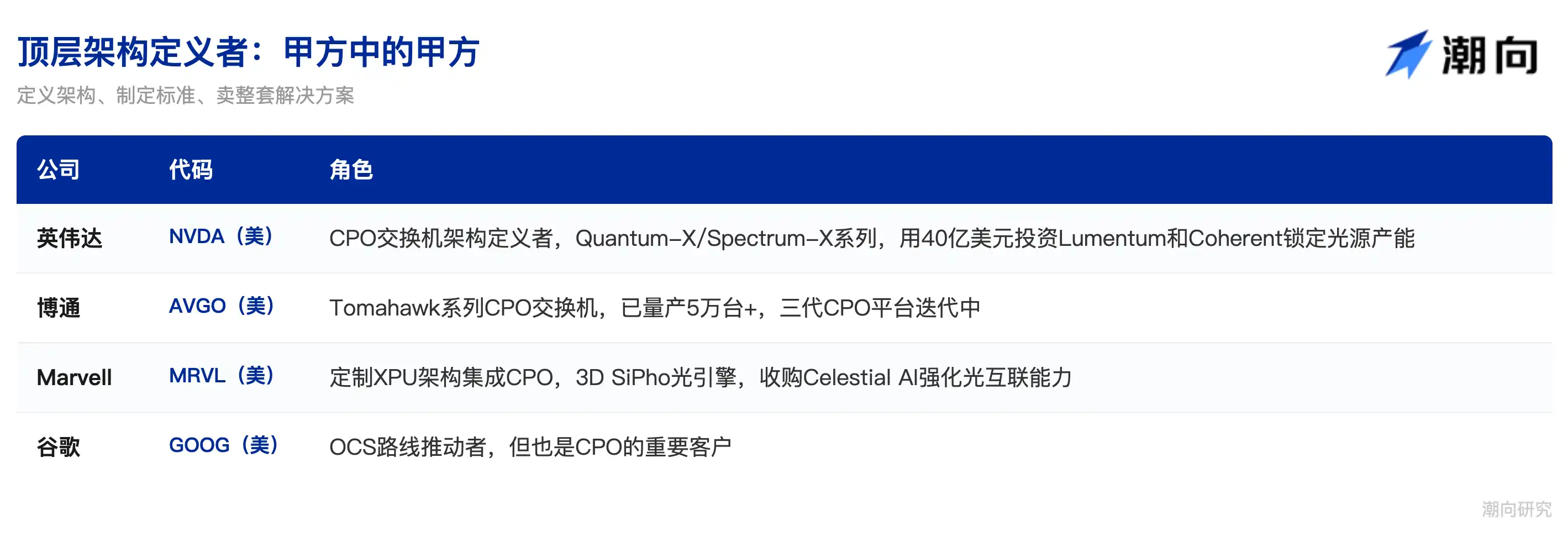

4.1 Top-level Architecture Definers: "The Clients of Clients"

One of the most profound changes in the CPO era is the shift in supply chain power.

In the traditional pluggable era, optical module makers could independently define products and ship them. CPO "solders" the optical engine into the chip package. Whoever defines the chip architecture defines CPO. Power shifts from optical module makers to platform providers and switch chip makers.

NVIDIA (NVDA): The most aggressive player advancing CPO today. It not only launched the Quantum-X and Spectrum-X CPO switch series at GTC 2025/2026 but also, in H1 2026, invested $4 billion to lock up upstream light source and fiber capacity through $2B each in Lumentum and Coherent and $500M in binding Corning.

Broadcom (AVGO): The practical pioneer in CPO mass production. Its Tomahawk CPO switch series started with the first-generation Humboldt in 2021. By 2025, Tomahawk 5-Bailly became the industry's first mass-produced CPO solution, shipping over 50k units that year. A third-generation 200G/lane platform is on the way. Broadcom's strategy leans towards "selling picks and shovels." It doesn't build complete systems but sells CPO switch chips to major cloud providers for assembly.

Marvell (MRVL): Pursues a customization route. Through acquisitions like Celestial AI, it integrates 3D SiPho optical engines into its custom XPU architectures, offering highly integrated CPO computing platforms to specific clients.

Google (GOOG): A unique entity. It's simultaneously the biggest promoter of OCS and a major CPO customer. Google uses OCS to replace Spine switches but still needs CPO for optical-electrical conversion at the Leaf and server layers. Thus, Google is both a "competitor" and a "buyer" of CPO.

4.2 Advanced Packaging & Manufacturing: Bonding Light and Electricity Together

The core technical challenge of CPO lies in heterogeneous integration packaging—bringing together photonic chips (silicon photonics or InP) and electronic chips (CMOS ASIC), made with different materials and processes, onto the same substrate or interposer. This isn't traditional "soldering components onto a board" packaging. It requires sub-micron precision hybrid bonding, akin to chip fabrication itself.

TSMC (TSM): The absolute core of this segment. Both NVIDIA's and Broadcom's CPO solutions rely on TSMC's COUPE platform and SoIC 3D packaging technologies. In February 2026, TSMC advanced COUPE to risk production. A 6.4T/package solution co-developed with AMD is expected to enter high-volume production in H2 2026. TSMC's advanced packaging capacity and yield directly determine CPO's mass production timeline.

ASE (ASX): As the world's largest packaging and test house, ASE is also a key player in CPO advanced packaging.

Amkor (AMKR): US-based Amkor is also vying for CPO foundry orders.

In A-shares, Huatian Technology (002185) and JCET (600584) are key beneficiaries in packaging. Huatian's packaging business directly benefits from CPO adoption. JCET participates in advanced packaging under its brand, possessing technical reserves for heterogeneous integration. However, it's important to note that the core CPO packaging segment remains highly concentrated with TSMC, while domestic packaging houses benefit more from peripheral support and lower-end packaging/testing.

Worth a separate mention is Fabrinet (FN), the EMS leader in optical precision manufacturing. High-end optical modules from Coherent, Lumentum, etc., are largely outsourced to it, similar to TSMC's role in semiconductors.

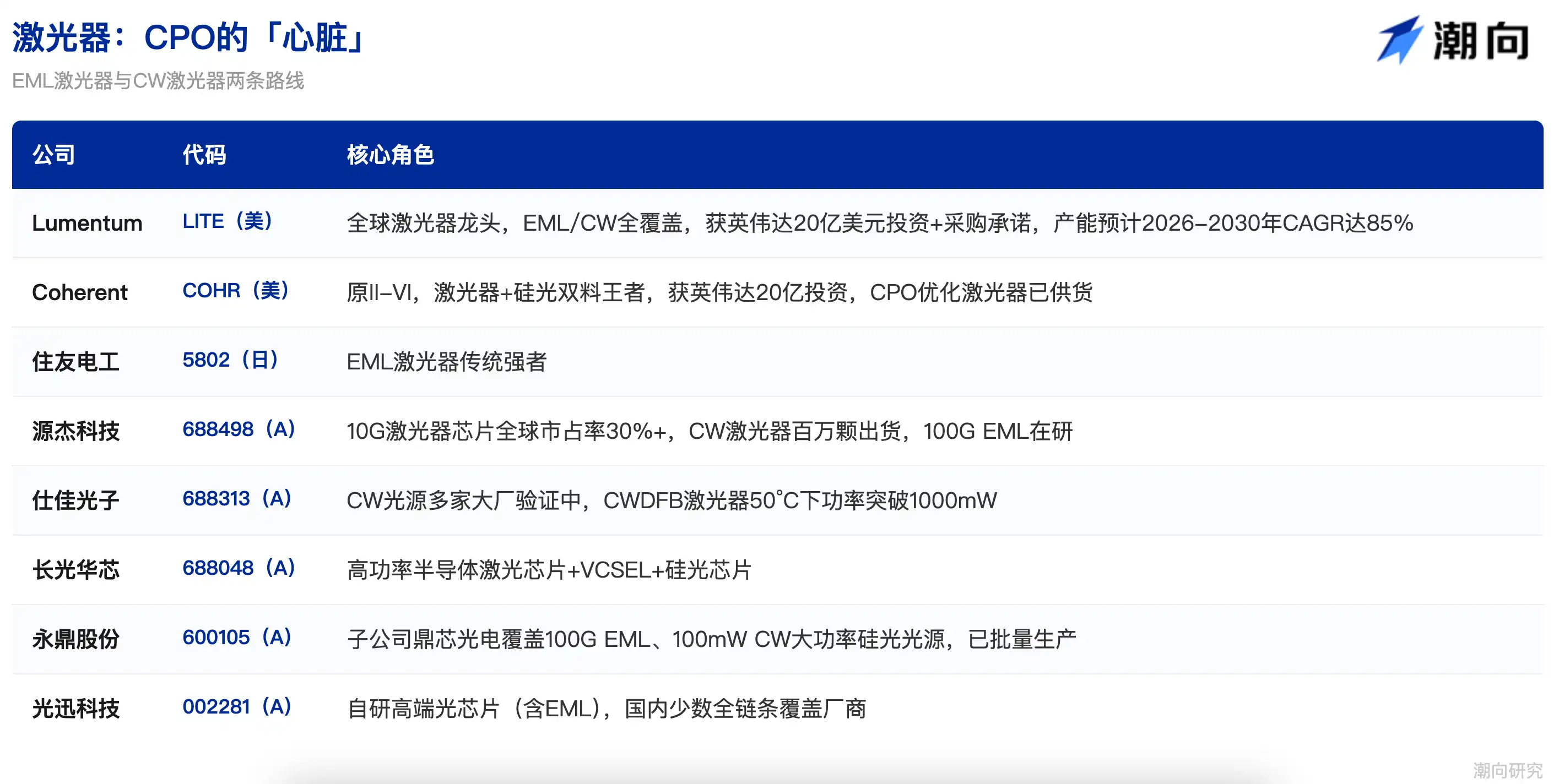

4.3 Lasers: The "Heart" of CPO

If the chip is CPO's "brain," then the laser is its "heart." Without a light source, all optical-electrical conversion is impossible.

The laser field features competition between two technology paths.

EML Lasers (Electro-absorption Modulated Lasers) are the traditional path, integrating light emission and signal modulation on a single chip, suitable for high-bandwidth, long-distance transmission. This path has extremely high technical barriers, with very few global suppliers. Lumentum (LITE) was first to mass-produce 200G EML in 2023 and demonstrated the world's first 400G EML in 2025. Coherent (COHR) follows closely. Together, they hold over 80% market share. Japan's Sumitomo Electric (5802.T) and Mitsubishi are also strong traditional EML players, but their capacity expansion lags far behind demand growth.

CW Lasers (Continuous Wave Lasers) are the emerging path. They completely separate "light generation" and "modulation." The laser only emits a continuous, stable beam, while the signal modulation work is handled by the modulator on the silicon photonics chip.

The CW path offers lower power consumption and better cost structure, naturally fitting CPO and silicon photonics architectures. Crucially, Chinese players have made breakthroughs on the CW path.

Yuanjie Technology (688498) holds over 30% global market share in 10G laser chips. Its CW lasers have achieved million-unit shipments, and 100G EML is in R&D/testing. Its Q1 2026 revenue growth was 321%, with net profit soaring over 11x, making it one of the most elastic upstream optical chip stocks.

Shijia Photon (688313) has its CW light source being validated and adopted by several leading clients. Its newly developed CWDFB laser achieved a power breakthrough of over 1000mW at 50°C.

Everbright Laser (688048) covers high-power semiconductor laser chips, VCSEL laser chips, and silicon photonics chips.

Yongding Co., Ltd. (600105) through its subsidiary Dingxin Photoelectrics has built a rare domestic IDM laser chip factory, with both 100G EML and 100mW high-power CW silicon photonics light sources in mass production. Accelink (002281) is one of the few domestic companies capable of self-developing high-end optical chips (including EML) with full-chain coverage.

In March 2026, NVIDIA invested $2 billion each in Lumentum and Coherent, with accompanying purchase commitments lasting from 2027 to 2030. Lumentum will use the funds to build a new wafer fab in the US, with laser capacity expected to grow at an 85% CAGR from 2026-2030. Coherent will invest in expanding Indium Phosphide (InP) capacity at its Sherman, Texas plant. These investments send a clear signal: Lasers are the segment with the largest supply-demand gap and highest strategic value in the CPO supply chain.

4.4 Silicon Photonics Chips: The "Brain" of the CPO Optical Engine

Silicon photonics is the mainstream path for implementing CPO optical engines. The core idea is to use standard CMOS silicon processes to directly "draw" optical structures like waveguides, modulators, and photodetectors onto the chip—making optical components using semiconductor methods. The benefits are natural suitability for large-scale integration, sharing manufacturing platforms with electronic chips, and significant cost reduction with mass production.

Overseas players have deep silicon photonics experience.

Broadcom (AVGO) was one of the earliest semiconductor giants to invest in silicon photonics. Its CPO switch optical engine is based on a self-developed silicon photonics platform.

Intel (INTC) has over a decade of silicon photonics R&D through its Intel Photonics team. While less active in consumer markets, it remains a core player in data center optical interconnect.

Marvell (MRVL) integrated silicon photonics capabilities through acquisitions like Celestial AI. Its 3D SiPho optical engine supports 200Gbps optical interfaces. Cisco (CSCO) acquired Acacia Communications for ~$4.5B in 2019, gaining an industry-leading silicon photonics coherent technology platform.

Domestic players are also accelerating their catch-up.

Accelink (002281) has mass delivery capability for 400G and 800G silicon photonics chips and jointly launched a 1.6T silicon photonics optical module with Cisco at OFC 2026.

Yuanjie Technology (688498) provides high-power silicon photonics light source products, complementing silicon photonics modules.

Shijia Photon (688313), the PLC splitter and AWG chip leader, is extending its layout into silicon photonics chips.

Silicon photonics technology is highly versatile, compatible with CPO, LPO, thin-film Lithium Niobate (LiNbO3), and other advanced paths, making it a strategic focus for major players. InnoLight previously disclosed that the proportion of silicon photonics solutions in its 800G products is rapidly increasing, indicating silicon photonics is not exclusive to CPO but is also infiltrating traditional pluggable modules.

4.5 Fiber Optic Connectivity Components: New Pie Baked by CPO

While previous segments involve upgrades of existing markets, fiber optic connectivity components are pure incremental markets created by CPO. These components are barely used in traditional pluggable optical module solutions but become essential in CPO architecture, representing one of the most elastic segments in the supply chain.

(1) FAU (Fiber Array Unit)

In traditional modules, fiber plugs into a standardized interface. But CPO is different. Fiber needs micron-level precision alignment with waveguides on the optical chip's surface. Misalignment means light can't couple in. FAU accomplishes this, fixing multiple fibers in an extremely precise array, ensuring each aligns perfectly with its corresponding waveguide on the chip.

A traditional FAU costs about $15, but the polarization-maintaining FAU used in CPO sees its value soar to several tens or even $100. For an NVIDIA 115.2T switch, one unit needs 72 FAUs, bringing the total FAU value per switch to $6000-$7000. From 2025-2026, the FAU market is expected to grow from RMB 6-7 billion to over RMB 10 billion, with extremely fast growth. Moreover, FAU production is difficult to ramp, with high yield requirements, leading to tight supply.

(2) PMF (Polarization-Maintaining Fiber)

Traditional modules use direct modulation, insensitive to light polarization. But CPO uses external lasers. If the polarization state changes during transmission through the fiber to the optical engine, significant optical power loss occurs. PMF is the "dedicated channel" ensuring the polarization direction remains constant. Although costlier than regular fiber, it's the only choice in CPO architecture.

(3) Fiber Shuffle (Fiber Distribution Box)

Traditional modules typically have one transmit and one receive fiber—manual cabling suffices. But CPO involves dozens to hundreds of fibers, requiring high-density re-arrangement so each fiber correctly connects from the optical engine to the right external port. Fiber Shuffle is the data center version of a "cable organizer," indispensable in CPO architecture.

(4) MPO (Multi-fiber Push-On) Connector

For CPO reaching 400G+ rates, 8 or even 16 fibers are needed for parallel transmission, while panel space is extremely limited. MPO connectors are "multi-port plugs" connecting multiple fibers at once, experiencing explosive demand in the CPO era.

In this segment, US-listed Corning (GLW) is the absolute global giant in fiber optics and optical materials, a core supplier of FAUs and fiber, and the partner in NVIDIA's $500 million strategic collaboration. In 2025, Corning's Optical Communications segment revenue was $6.3B, up 35%, its largest and fastest-growing business. Non-listed players like US Conec and SENKO are also global core players in MPO/MTP connectors.

In A-shares, TFC Optical Communication (300394) is the absolute leader, covering FAU fiber arrays, LENS arrays, MPO connectors across the board, and serving as a core supplier for both NVIDIA's and Broadcom's CPO solutions. In H1 2025, the share of optical active devices in its revenue rose 8 percentage points year-on-year to 63.78%, mainly driven by growth in CPO-related packaging orders, with a gross margin of 42%.

Tai-Saw Technology (300570) is the domestic leader in MPO connectors, with products indirectly certified by NVIDIA.

Guangku Technology (300620), besides its Lithium Niobate modulator mainstay, has its 90-degree bend fiber arrays entering mainstream supply chains and unique layouts in OCS all-optical switching devices.

Longcore Innovation is an integrated photoelectronic device supplier covering MPO, AOC (Active Optical Cable), AEC, and has entered Google's and NVIDIA's supply chains.

4.6 Fiber Optic Connectivity Components: New Pie Baked by CPO

Compared to traditional optical modules, CPO generates substantial new demand for precision fiber optic components. These components are barely used in traditional schemes but become essential in CPO architecture, representing one of the most elastic incremental segments.

(1) FAU (Fiber Array Unit)

In CPO, fiber requires micron-level precision alignment with waveguides on the optical chip surface; FAU handles this. A traditional FAU costs ~$15, but the polarization-maintaining FAU for CPO sees value surge to several tens or even $100. For an NVIDIA 115.2T switch, one unit needs 72 FAUs, worth $6000-$7000.

From 2025-2026, the FAU market is expected to grow from RMB 6-7B to over RMB 10B, with rapid growth.

(2) PMF (Polarization-Maintaining Fiber)

Traditional modules are insensitive to light polarization, but CPO uses external lasers. If polarization changes, significant optical power loss occurs. PMF is the "dedicated channel" ensuring constant polarization state.

(3) Fiber Shuffle (Fiber Distribution Box)

CPO involves a surge in fiber count, requiring complex high-density fiber re-arrangement, like a data center "cable organizer." Traditional modules have 1 transmit, 1 receive fiber—no need for this.

(4) MPO (Multi-fiber Push-On) Connector

For CPO reaching 400G+, 8 or 16 fibers are needed for parallel transmission. MPO connectors are "multi-port plugs" connecting multiple fibers at once, experiencing explosive demand in the CPO era.

4.7 Fiber Optic Cables: The Infrastructure Backbone of the CPO Era

While not a direct part of the CPO module, fiber optic cables are the physical carrier for the entire optical interconnect. Without fiber, optical signals have nowhere to go. The explosive construction of AI data centers is pushing fiber demand into a super-cycle.

This cycle features an extremely rare simultaneous volume-price increase. In March 2026, the price for China's G.652.D single-mode fiber soared to RMB 83.4 per core-kilometer, up over 160% from January, hitting a record high. The last similar price surge was during the 2018 "Broadband China" construction peak. On the demand side, the four major North American cloud providers plan combined 2026 CapEx of $725 billion, up 77% year-on-year. Meta alone signed a $6 billion long-term fiber cable contract with Corning.

US-listed Corning (GLW) is the global leader in fiber preforms, boosting US domestic optical connectivity manufacturing capacity tenfold with NVIDIA's $500 million support.

Dual-listed (HK/A) Yangtze Optical Fibre and Cable (06869/601869) is the world's largest fiber preform and fiber manufacturer. Its Q1 2026 net profit skyrocketed 226% year-on-year. At OFC 2026, YOFC demonstrated hollow-core fiber (single spool 91.2km, attenuation only 0.04dB/km), reaching world-leading levels and representing the next direction for fiber technology.

Zhongtian Technology (600522), with full-chain capabilities integrating submarine and terrestrial cables, is a leading domestic optical cable manufacturer.

Hengtong Optic-Electric (600487) covers a full range of fiber optic cable products with forward-looking layouts in F5G solutions.

FiberHome Telecommunication Technologies (600498) is a core enterprise in Wuhan's "Optics Valley" optical communication industrial chain, backed by China Information Communication Technologies Group.

4.8 PCB/Substrate: The Skeleton of CPO

Both traditional optical modules and CPO switches rely on high-performance PCBs and ABF substrates. But CPO era requirements for PCBs change qualitatively: higher signal integrity (optical engine adjacent to ASIC, stricter trace precision), low-loss materials become essential (high-end materials like Megtron 6/7 cost 5-8x regular FR-4), and stronger multi-layer stacking capability. Simultaneously, optical module PCBs themselves are iterating to higher speeds, with 800G/1.6T module PCBs having much higher value than previous generations.

Shenghong Technology (300476) is the undisputed AI leader in this segment. It's a core supplier of substrates for NVIDIA's GB200 servers, with AI server PCB revenue exceeding 50%. In optical communications, Shenghong has achieved mass production of 800G switch PCBs and industrial production of 1.6T optical module PCBs, covering both CPO and optical module demand scenarios. Its global share in AI computing PCB is leading, making it the stock with the broadest coverage in the "CPO+PCB" intersection.

Dongshan Precision Manufacturing (002384) pursues a dual-main business strategy of AI computing PCB and photoelectronic modules. Its Q1 2026 net profit grew 119%-152% year-on-year, driven by accelerated AI infrastructure investment.

Wus Printed Circuit (002463) is a traditional leader in high-speed data center PCBs, supplying global mainstream server and switch platforms.

Shennan Circuits (002916) differentiates with high-end IC substrate capabilities, covering higher-value segments from PCB to chip packaging substrates.

4.9 DSP & SerDes Chips: Segments Redefined by CPO

In traditional pluggable optical modules, the DSP is the single most power-hungry, costly component. It repairs degraded electrical signals from transmission—indispensable but also a "power hog."

One of CPO's most important power savings comes from eliminating the standalone DSP chip. But this doesn't mean signal processing disappears; it's redistributed: the DSP's core functions are integrated into the switching ASIC, while CDR is integrated into high-speed SerDes. SerDes (Serializer/Deserializer) resides inside the ASIC, responsible for parallel-to-serial conversion of internal chip data into high-speed serial streams for transmission, or deserializing received streams. CPO requires SerDes rates to advance from today's 112Gbps to 200Gbps and beyond, posing extreme demands on ASIC design capability.

Broadcom (AVGO) is the absolute leader in integrated switch ASIC and SerDes design. Its Tomahawk series chips have built-in high-speed SerDes directly driving the CPO optical engine, eliminating extra signal conditioning chips.

Marvell (MRVL) holds unique advantages in custom switch ASICs, able to tailor integrated CPO computing platforms for specific clients.

In specialized SerDes and connectivity chips, Astera Labs (ALAB) positions itself as an intelligent connectivity chip provider, covering PCIe/CXL Retimers and SerDes IP. Credo (CRDO) focuses on high-speed SerDes IP cores, holding a notable share in the data center connectivity market. London-listed Alphawave Semi (AWE) is another important player in high-speed connectivity IP.

4.10 Optical Module Manufacturers: From Protagonists to Transformers

In the traditional pluggable era, optical module makers were the absolute protagonists. They independently sourced optical chips, electrical chips, structural components, assembled them into complete modules, and sold directly to data center clients. But CPO integrates the optical engine into the ASIC package, weakening the standalone module's role. Module makers face a fundamental question: Is my pie being eaten?

The answer: Not in the short term, but long-term transformation is a must.

Short-term, pluggable modules remain in a super boom cycle. InnoLight (300308) Q1 2026 revenue reached nearly RMB 19.5 billion, up 192% year-on-year, net profit RMB 5.7 billion, up 262%. Before CPO fully replaces pluggables, demand for 800G/1.6T modules is still doubling. Eoptolink (300502) is also accelerating volume shipment of 1.6T products. Chinese companies hold 7 of the top 10 global optical module spots, with InnoLight firmly first.

Medium-term, module makers are advancing on multiple fronts for the CPO era. First, continue supplying 800G/1.6T/3.2T pluggable modules, maximizing current cycle profits. Second, provide transition solutions like NPO and LPO. Huagong Tech has launched the world's first 3.2T NPO product for a leading client. Third, transform into suppliers of CPO optical engines, shifting from selling "complete vehicles" to selling "engines." This path is logical, as optical engine core processes (optical chip packaging, fiber coupling, test/validation) highly overlap with modules. Fourth, enter the OCS all-optical switch business. InnoLight has adopted digital liquid crystal technology to enter this arena with support from Google and Amazon.

Accelink (002281), as a state-backed veteran optical communication giant, has a full chain from chip-device-module-subsystem, with 1.6T silicon photonics modules ready for mass delivery.

US-listed Coherent (COHR) and Fabrinet (FN) are also core players. Coherent is a dual giant in modules and chips. Fabrinet, as the "contract manufacturing king," handles nearly all high-end modules. Its management recently stated CPO is "more real than ever" and has begun generating related revenue.

五、Investment Map: The Full Supply Chain at a Glance

六、Timeline & Investment Rhythm

Short-term (2026-2027)

This is the "last feast" for pluggable modules + the "0 to 1" phase for CPO.

800G/1.6T pluggable modules remain in short supply, with leaders like InnoLight and Eoptolink seeing sustained explosive earnings. Simultaneously, CPO begins its first wave of scaled shipments (primarily at the Spine switch layer), driven by NVIDIA and Broadcom.

Core Beneficiary Segments: Optical Modules (InnoLight, Eoptolink), Lasers (Lumentum, Coherent, Yuanjie Tech), Fiber Connectivity Components (TFC Optical, Tai-Saw Tech).

Medium-term (2027-2029)

CPO expands from Spine to Leaf layers. Pluggable module share in Scale-out scenarios begins to be eroded by CPO. NPO as a transition solution peaks in the Chinese market. 3.2T modules commercialize.

Core Beneficiary Segments: Advanced Packaging (TSMC), External Lasers (value increases 3-4x), FAU/MPO (volume & price rise).

Long-term (2029-2032+)

CPO penetrates Scale-up (intra-rack). OIO technology commercializes in GPU interconnect scenarios, with copper cables largely replaced by optical interconnect. CPO penetration in AI data center optical communication modules is expected to reach 35% by 2030.

Core Beneficiary Segments: OIO-related players (Ayar Labs), Silicon Photonics Platforms, the entire optical interconnect supply chain.

七、Epilogue: Walking with Light

If GPUs are the "brain" of AI, HBM is "memory," and power is "food," then optical interconnect is AI's "nervous system." Without it, even the most powerful brain cannot connect with the world.

As Jensen Huang made clear: Energy is our most important resource. And the core value of CPO is precisely using light instead of electricity to fundamentally reduce the energy consumption of data transmission.

On this track, the US holds architecture definition power (NVIDIA, Broadcom) and high-end optical chips (Lumentum, Coherent). TSMC holds the key to packaging and manufacturing. Chinese enterprises have built strong competitive barriers in module assembly (InnoLight, Eoptolink), fiber connectivity components (TFC Optical), CW lasers (Yuanjie Tech), and fiber optic cables (YOFC).

In the coming years, the investment logic of this trillion-dollar track will gradually evolve from selling "picks and shovels" (optical modules) to building "highways" (CPO/OIO infrastructure). The ultimate winners will be those who can keep pace with technological iteration while securing critical supply chain bottlenecks.

Disclaimer: This article is solely for supply chain knowledge梳理 and does not constitute any investment advice. Companies and stocks mentioned are not recommendations. Investment involves risks; caution is advised.