Originally fromGalaxy

Compiled / Odaily Planet Daily Golem(@web 3_golem)

Who would have thought that Bitcoin creator Satoshi Nakamoto would one day face a lawsuit, with the 'ownership' of wallet addresses potentially being taken away. And you, reading this article right now, might also be one of the 'defendants,' as long as you have dormant Bitcoin addresses.

In March of this year, the New York State Supreme Court accepted a lawsuit: the plaintiff is attempting to confirm their ownership of over 3.7 million Bitcoins (approximately $274 billion) associated with 39,069 Bitcoin addresses. The plaintiff goes by the pseudonym Noah Doe and two unnamed Wyoming limited liability companies (pseudonyms 'ABC Company' and 'XYZ Company').

The plaintiff is requesting the New York State Supreme Court to confirm their ownership of these dormant assets through a declaratory judgment action based on New York State's lost and found laws. More importantly, among these 39,069 addresses are addresses suspected to belong to Bitcoin creator Satoshi Nakamoto (a total of 21,744 addresses, holding approximately 1.09 million Bitcoins, valued at about $83.7 billion at current prices).

Simply put, an anonymous individual and their company registered in Wyoming are trying to get a New York court to rule that Satoshi Nakamoto's Bitcoins (and many other cryptocurrencies) are lost property, and they should legally own them for 'finding' these Bitcoins. Galaxy analyzed the plaintiff's potential motives and identity, the impact on Bitcoin, and the plaintiff's likelihood of success.

Odaily Planet Daily has condensed and compiled the full text as follows, enjoy~

Case Overview and Analysis of Plaintiff's Strategy

The plaintiff has filed an application with the New York State Supreme Court, asking the court to declare that they own 39,069 dormant Bitcoin addresses and all assets within them. The legal basis is the declaratory judgment for confirming ownership under Article 3001 of the New York Civil Practice Law and Rules (CPLR), which is fundamentally based on New York State's lost and found law, specifically Article 7-B of the Personal Property Law. This provision states that a finder of lost property who turns it over to the police and does not face a denial from the owner within a specified waiting period may ultimately acquire ownership of the lost item. The plaintiff is attempting to apply this old framework to Bitcoin.

The specific strategy is: Noah Doe, as the finder, delivered a USB drive containing the addresses (not the private keys or proof of holding the addresses, just the public addresses) to the New York City Police Department's 17th Precinct, substituting this for turning over the lost property to the police; then issued notifications via OP_RETURN on the Bitcoin blockchain and published press releases, substituting this for contacting the owner; finally, had an expert appraise each address's value at under $10, allowing the entire case to enter the fastest process stipulated by that provision.

It is necessary to clarify that even if the plaintiff wins completely, they will only receive a piece of paper—a court declaration—nothing more. They will not receive any private keys, nor can they transfer any Bitcoin.

The real value of a New York judgment lies elsewhere. It would serve as a 'title defect': if any of these Bitcoins appear in any regulated venue in the future, the plaintiff could present this document to contest exchanges or custodians. This is the potential risk this case poses to Bitcoin holders and why this seemingly absurd lawsuit still warrants careful scrutiny.

Case Timeline

The following timeline consists of two parts: one is the plaintiff's factual narrative of discovering the addresses, and the other is the procedural history of the case in court.

- October 2024: Noah Doe claims he discovered 'security issues' with certain addresses and developed an 'algorithm' to tag abandoned addresses. (In reality, these addresses do not have 'security issues');

- December 26, 2024: Noah Doe first 'found' approximately 1,625 addresses. A USB drive containing the addresses was delivered to NYPD's 17th Precinct on January 1, 2025;

- February 2025: Noah Doe hired Solomon Brothers Strategic Advisors as a consultant;

- March 31 and April 14, 2025: Noah Doe again 'found' 546 addresses and 39,911 addresses respectively, delivering USB drives with addresses to the police precinct each time;

- June 30 to July 10, 2025: Noah Doe sent 'abandonment notices' to each address via OP_RETURN;

- August 7, 2025: Issued a press release to global media. CoinDesk, Bitcoinist, Yahoo Finance, Investing.com, and Galaxy Digital's research report all covered it;

- August 2025 to February 2026: Solomon Brothers received threatening emails, including over 50 emails containing only '4 8 15 16 23 42', demanding $1.5 million and 50 Bitcoins;

- October 10, 2025: The 90-day period for owner claims ended;

- December 2025: Noah Doe transferred these addresses to ABC Company and placed 98% of its interests into an irrevocable trust; ABC Company transferred 17.7% of its interests to XYZ Company;

- March 11, 2026: Original summons and complaint filed. Judge Arlene P. Bruce annotated the original order to show cause;

- March 23, 2026: Judge Emily Morales-Minerva recused herself from the case;

- March 25 to April 17, 2026: Judge Carlos J. Voltron signed the order to show cause (allowing use of pseudonyms) and an order authorizing alternative service via OP_RETURN (without notice to the opposing party);

- May 1, 2026: First amended complaint expanded the defendant scope to 1 to 39,069 individuals and attached a full list of addresses;

- May 21-22, 2026: On-chain service execution: 98 batch transactions in Bitcoin blocks 950,446 to 950,576;

- May 22, 2026: Carlos J. Voltron filed the affidavit of service, including verification reports for each batch and 39,069 lines of verification details (Documents 27-29).

Legal Basis and Strategy Proposed by Plaintiff

Article 7-B of the New York Personal Property Law (Sections 251-258) establishes a brief lost and found regime. It provides two distinct pathways for a finder to acquire ownership, both of which the plaintiff in this case invokes.

- Pathway A: Custody (Sections 252, 253/254, 257(1)). Section 252 requires a person who finds lost property worth $20 or more to return it to the owner or deliver it to police custody within 10 days; Sections 253(7) and 254 stipulate different police custody periods based on property value: under $100 for 3 months, $100-$500 for 6 months, $500-$5,000 for 1 year, and $5,000 or more for 3 years.

- Pathway B: The Under-$10 Shortcut (Section 257(2)). For lost property valued under $10, if the finder 'has made reasonable efforts to find the owner and return it, but has been unsuccessful,' ownership vests in the finder one year after finding, without requiring police delivery.

The complaint's (unnamed) 'independent expert' appraised the 'as-is' value of each address at under $10, citing low likelihood of recovery. This valuation determines the entire procedural progression of the case, as it places every address under the uniform one-year vesting period of Section 257(2). It also makes Pathway A's process shorter, as property valued under $100 requires only a three-month police hold per Section 254.

Plaintiff's Arguments

The complaint lists several arguments by the plaintiff, each must hold for the next to follow, forming a chain of logic.

- These addresses are lost property. Addresses are treated as property, akin to bank accounts. Under this view, losing a private key does not destroy the property; thus, its contents are merely 'lost' and can be reclaimed by a finder.

- Noah Doe is the finder, and NYPD's custody complies with the relevant statute. Section 252 of Article 7-B requires the finder to deliver the property to the police. The plaintiff argues that the USB drive containing address information delivered to the 17th Precinct satisfies this.

- Ownership has vested in the finder. For property valued under $10, Section 257(2) states ownership vests in the finder one year after finding if the finder has made reasonable efforts to locate the owner but failed. OP_RETURN notifications, press releases, and the 90-day claim period are considered reasonable efforts.

- These addresses have been abandoned. Noah Doe's 'algorithm' flags addresses that are in self-custody, unused for at least five years, and inactive during significant price increases. About 424 owners who reacted by moving tokens were removed from the list; the remaining 39,069 non-responsive owners became defendants.

- Service via OP_RETURN notification is lawful. Since the owners are allegedly unknown and cannot be located, the court authorized alternative service under CPLR 308(5) by sending an on-chain notice pointing to the complaint to each address.

- The plaintiff can proceed anonymously. Given the known kidnapping risks for large Bitcoin holders, the plaintiff was permitted to use pseudonyms in the lawsuit.

Who Are the Owners?

Galaxy analyzed the addresses claimed to be 'found' by plaintiff Noah Doe using their Bitcoin full node and internal research database.

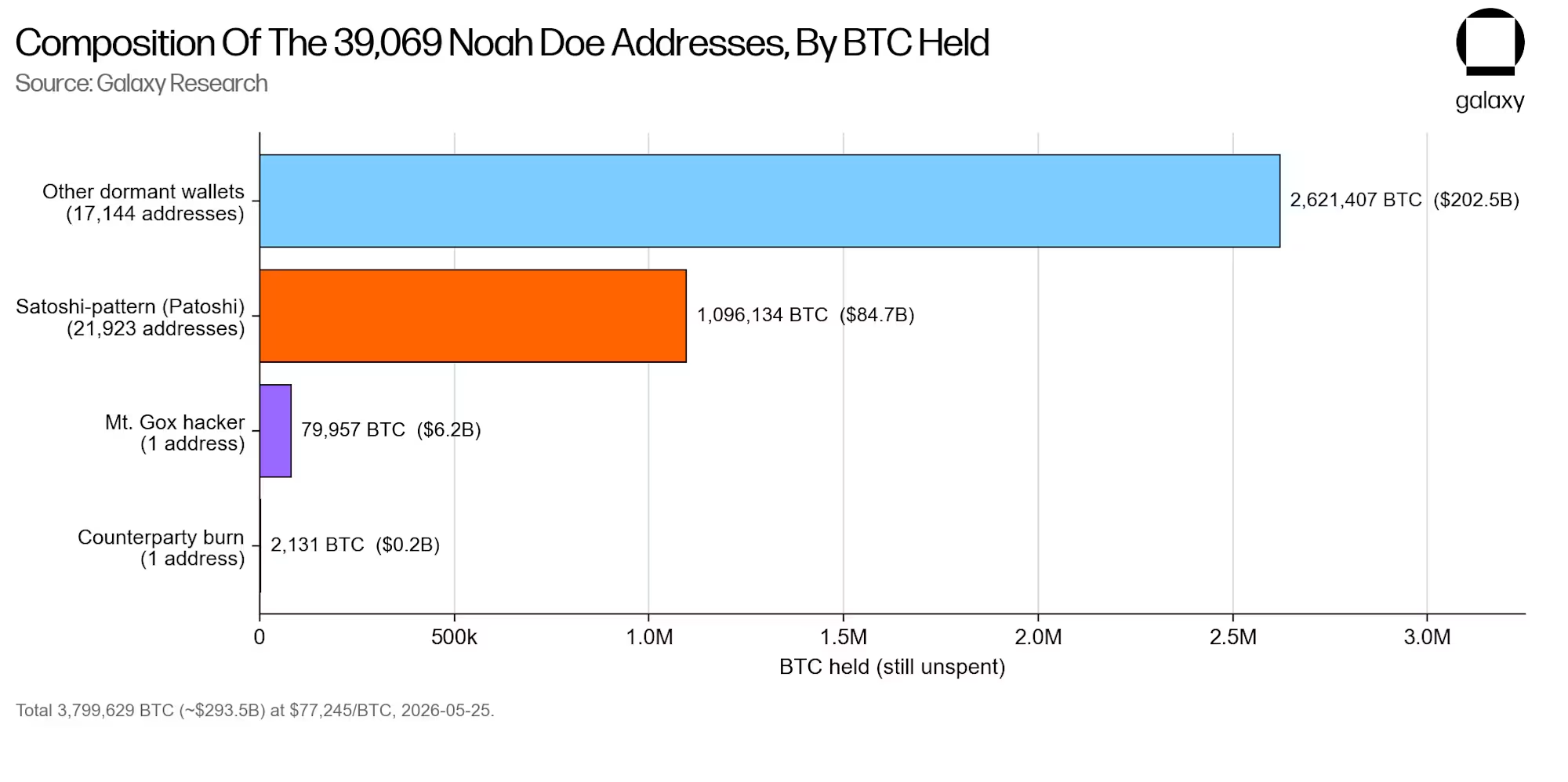

As of May 25, 2026, the 39,069 'Noah Doe addresses' hold 3,799,629 Bitcoins, valued at approximately $293.5 billion at $77,245 per Bitcoin. This value is not evenly distributed but concentrated in several distinct clusters, each telling a different story.

Composition of Addresses 'Found' by Noah Doe

Satoshi (Patoshi) Addresses

Comprising 21,923 addresses, approximately 1,096,134 Bitcoins (about $84.7 billion). These are early-mined Bitcoins linked to Bitcoin's creator through the 'Patoshi' nonce pattern. They have never moved.

Mt. Gox Hacker Address

Only 1 address, approximately 79,957 Bitcoins (about $6.2 billion). This is John Doe #1. These Bitcoins were stolen from the early Bitcoin exchange Mt. Gox and have been untouched since 2011. They are disputed property that investigators have tracked for years.

Counterparty Burn Address

Only 1 address, approximately 2,131 Bitcoins (about $160 million). This is John Doe #104, a provably unspendable 'burn' address. No one has ever held its key because, by design, such a key does not exist.

Other Dormant Addresses

7,144 addresses, approximately 2,621,407 Bitcoins (about $202.5 billion). These addresses contain a large number of early holders and exchange-era Bitcoins that have not moved for many years.

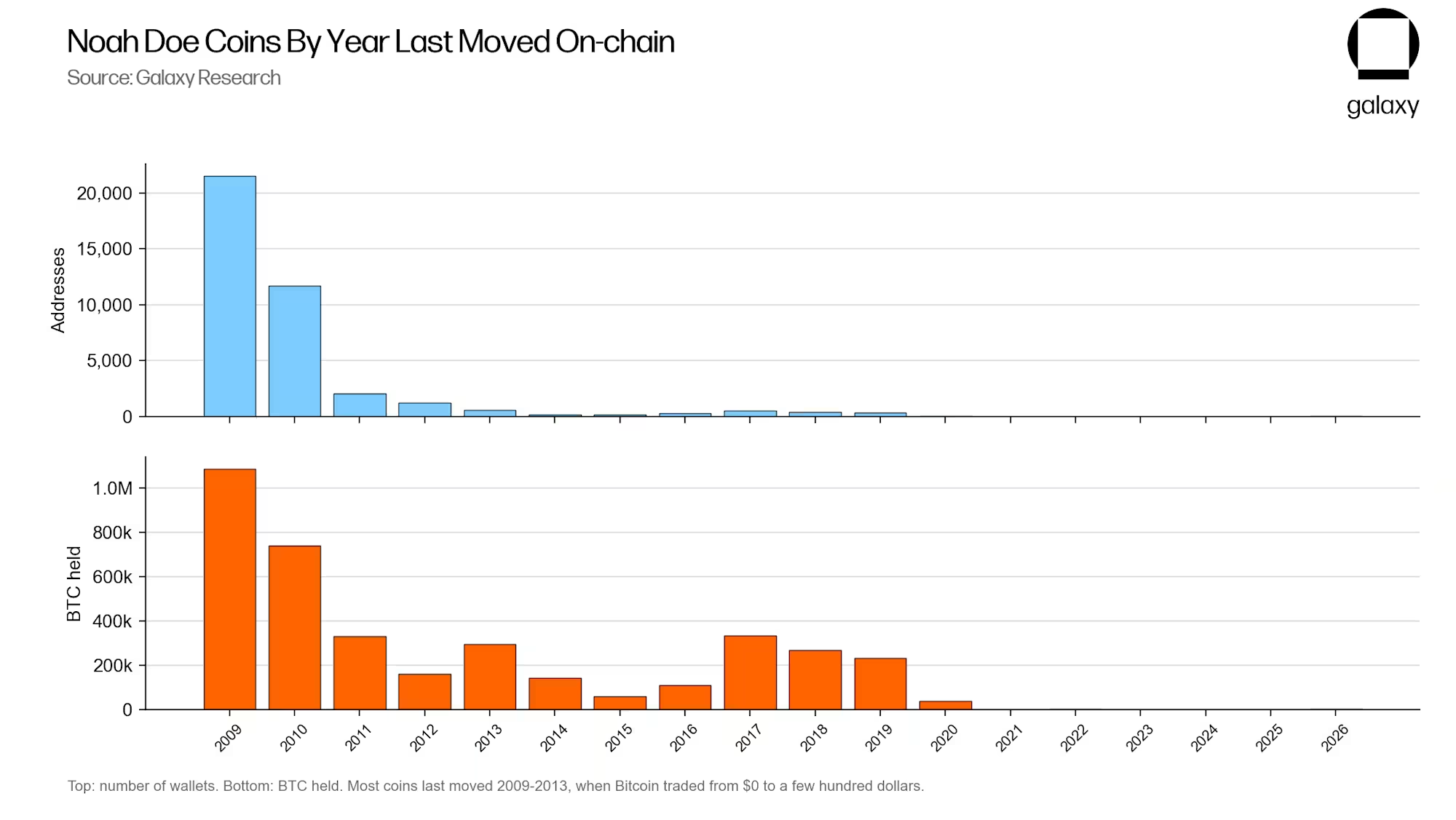

This dormancy is long-standing. If we sort each address by the year its Bitcoins last moved on-chain, we find most of the Bitcoins last moved in Bitcoin's early years. The vast majority of these Bitcoins last transacted between 2009 and 2013, during which Bitcoin's price soared from nearly zero to several hundred dollars.

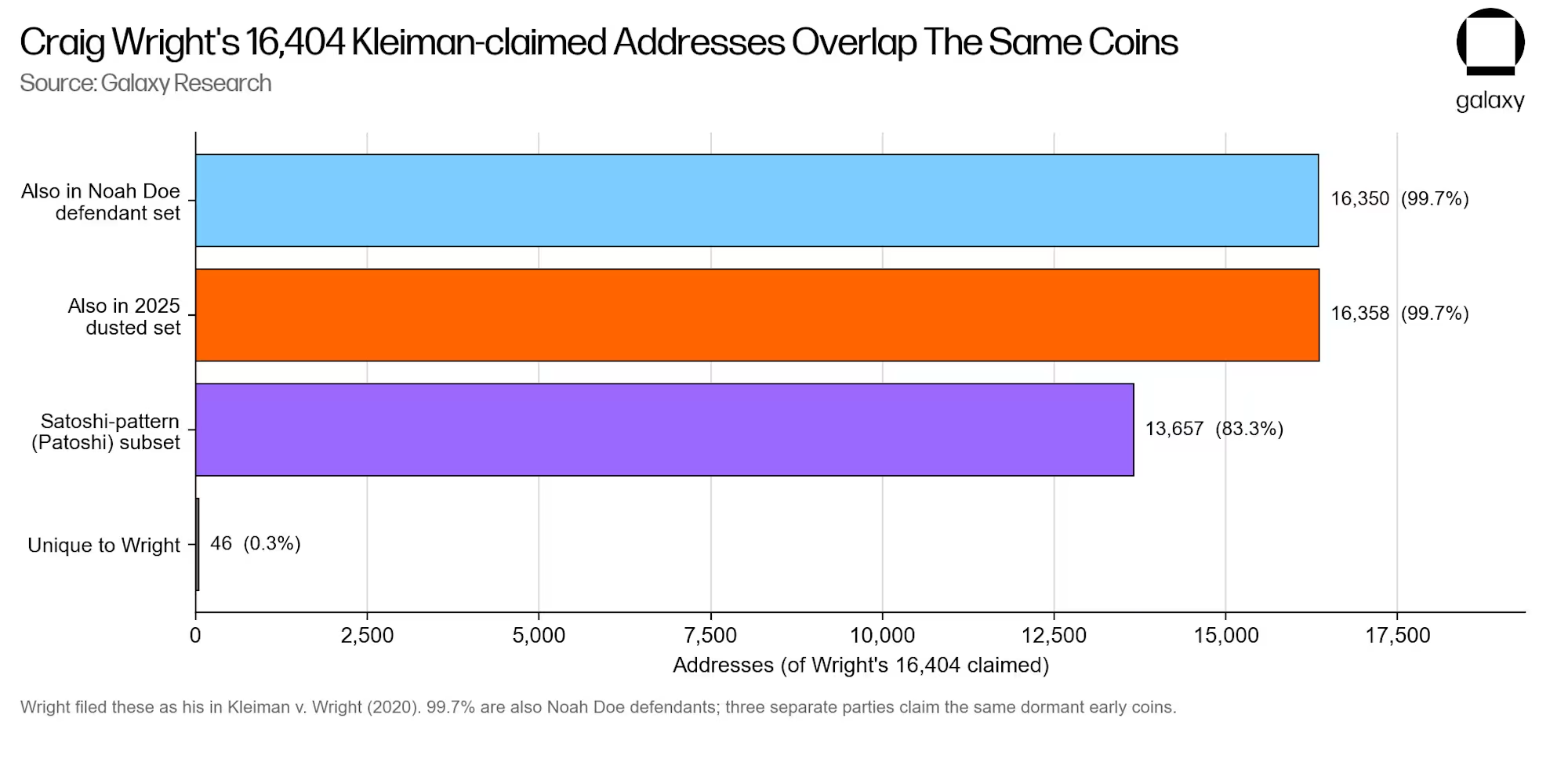

But many of these addresses have been claimed before. In Kleiman v. Wright (Southern District of Florida, 2018), Australian businessman Craig Wright submitted a list of 16,404 early-block addresses he claimed belonged to him as part of his later-dismissed claim to be Satoshi Nakamoto.

We compared the Bitcoin addresses Wright claimed to own in the Kleiman litigation with Noah Doe's addresses to see their overlap.

Address Overlap Between Noah Doe and Craig Wright

The overlap is almost identical. Of the 16,404 addresses Wright claimed, 16,350 (99.7%) are also claimed by Noah Doe's defendants, holding approximately 817,513 Bitcoins. We cannot determine if Craig Wright has any connection to the Noah Doe case, but the overlap is notable. Craig Wright has attempted for years to claim these Bitcoins through litigation but was found in contempt of court by a UK court in 2024.

Questionable Aspects of the Case

While we are not lawyers, just looking at the court record and relevant statutes, this case is full of doubts.

Does the Lost and Found Law Apply?

Before any valuation or service issues, there's a more fundamental question: the lost and found law was designed for physical objects that a finder picks up, holds, and delivers to the police. Noah Doe never held these coins or keys. He merely looked at public addresses on a ledger that anyone can read. Viewing a public address is far from holding lost property. Delivering a USB drive with listed addresses to the police is also different from actually delivering the lost item.

The statute envisions a finder who can return the item if the owner comes forward. But in this case, the finder never held the coins and could not possibly deliver them to anyone—neither to the police who allegedly have custody, nor to a claiming owner. The core issue goes beyond ownership; losing a private key does not deprive the true owner of any rights. The Bitcoin remains on-chain; the true key holder can move it at any time, which is exactly what hundreds of owners who lost their Bitcoin have done.

It seems clear that ownership cannot effectively transfer to a finder who can never touch the asset.

Valuation Is Not Credible

The average holding of a Noah Doe address is 97.25 Bitcoins, worth about $7.5 million; the median is 50.00 Bitcoins, worth about $3.86 million. Compared to these figures, the claim that each address is worth less than $10 is untenable. This appears to be a tactic to push these assets through the legal process at the fastest speed.

Two other details further undermine this valuation. The expert proposing the 'under $10' figure is not named in the filings, so this single number dictating the entire timeline cannot be examined or challenged. If the 'as-is recoverable' logic is applied universally, then almost all self-custodied Bitcoin would be valued near zero, which is diametrically opposed to how any user, especially one going through the trouble of filing this lawsuit, treats their Bitcoin.

Anonymity of the Parties

Noah Doe's use of anonymity in this case is also highly questionable. He seeks anonymity to avoid being targeted as a large holder, yet the rights he seeks would force the actual address holders to reveal their identities to defend their cryptocurrency. The protection the plaintiff wants for himself is precisely what he seeks to strip from all defendants.

Even if an individual could present a genuine personal safety theory, that theory exists to protect natural persons. ABC Company and XYZ Company are shell LLCs. A corporation has no physical entity to be threatened and no privacy to expose, so the logic of fearing extortion does not apply. Allowing two companies to claim trillions in property under shell names is astounding.

Moreover, New York State does not favor anonymous entities. New York courts rarely allow pseudonyms. While New York historically permitted anonymous LLC ownership, the state's LLC Transparency Act now mandates disclosure of beneficial ownership, though federal law has narrowed its scope to foreign-formed LLCs.

Potential Development of Subsequent Litigation

Even setting aside these details, the 'audacity' of this lawsuit becomes apparent. It is unthinkable that a New York court would award legal ownership of approximately $293 billion worth of Bitcoin (including some belonging to Satoshi Nakamoto) to anonymous individuals based on a dubious 'lost and found' theory with an under-$10 valuation. Courts are typically reluctant to entertain such novel and far-reaching cases, especially when property is disputed and judgments could have broad implications.

Since this is a declaratory action about property ownership, under CPLR 1012(a)(3), the true owners of the addresses have the right to intervene directly in the lawsuit; non-owners with a related interest may apply for permission to intervene under CPLR 1013. However, while the principle allows intervention, there is a massive practical obstacle. To intervene, an owner must come forward and prove control over the registered address, which is precisely the de-anonymization that cautious Bitcoin whales have spent a lifetime trying to avoid.

The defendant addresses are all pseudonymous and deliberately not publicly listed. Therefore, by the end of June 2026, about 30 days after service, a technical default judgment is almost certain to occur. A motion for default judgment will likely be filed in the summer. However, for many reasons, the court is unlikely to swiftly grant a default judgment fully satisfying all plaintiff's demands.

First, a declaration of ownership is not a default service provided by the clerk for a fixed sum; it requires an application to the court, and the court retains discretion to require a hearing and demand actual evidence. Second, the theory is novel and the stakes are enormous—factors that often trigger judicial skepticism, not 'rubber-stamp' approval. Furthermore, the validity of OP_RETURN service itself is debatable, and a questionable affidavit of service gives the court reason to proceed cautiously. Finally, any actual holder who intervenes could turn a previously uncontested case into a real contest.

Galaxy estimates the likelihood of the court granting a full ownership declaration in a default judgment is low, and even if it does rule, it's more likely to be after a hearing and in a narrowed scope.

What if the Plaintiff Wins?

Even if the plaintiff wins completely, they still cannot seize any Bitcoin. All they would hold is a New York State declaration, not a set of private keys. The principle 'Not your keys, not your coins' applies to them as well.

Therefore, the danger is not that the plaintiff could seize Satoshi's Bitcoin or any other Bitcoin mentioned in the Noah Doe defendant addresses. The danger is that if any of these Bitcoins are transferred to a centralized exchange or custodian, the plaintiff could present their New York judgment to that institution and attempt to place a lien on those Bitcoins. Such action could freeze assets, spark years of litigation, and force the holder who moved the Bitcoin decades later to come forward to prove ownership, thereby compromising their own anonymity.

The paper ownership certificate is leverage against regulated intermediaries and those who rely on them. This almost certainly explains why, even though a judgment may never directly affect the Bitcoin itself, it is still worth pursuing for those behind this case.