Decentralization must permeate every aspect of any worthwhile blockchain, particularly the “Three D’s of Decentralization”:

1. Design

2. Distribution

3. Direction

3D decentralization.

Previous posts like Satoshi Plus Consensus have discussed Core’s design. This post begins the discussion around Core’s decentralized distribution, its effects on Core’s direction, and how Core is a 3D Blockchain.

2D Blockchains

Prior to Core, a 3D blockchain hadn’t been popularized in a long time. As described in The Merge is Here, new L1s have been scrambling for growth at all costs in order to win “The Layer One Race.” The results can often lead to centralized distributions.

Token price movements are one of the most visible negative effects of centralized distributions. Historically, centralized distributions have often preceded early token price booms. With powerful investors potentially drawing attention to rapidly ascending chains combined with a low circulating supply as a result of investor lock-ups, tokens may be primed for post-launch jolts. Nevertheless, the final result of this race to the top may be a steep race to the bottom as lock-up periods expire and early investors liquidate their holdings.

Aside from price (which is not necessarily reflective of a blockchain’s fundamental value), the picture may be no less worrisome. When the initial token-base is concentrated in the hands of a small group of insiders, decentralization can suffer at all levels, including design and direction.

Regarding design, a blockchain’s effectiveness often depends on the makeup of the token-base. For blockchains running on proof of stake and similar consensus mechanisms (as many new chains do), network security and censorship-resistance rely on the good faith of token holders. Thus, token-base centralization places the entire chain at risk of being manipulated, a concern first outlined in Core Blockchain Origins. This means that the measure of a blockchain’s success may more likely be defined by price rather than development. Price and development can be linked, but at the end of the day, investors tend to want to convert tokens into fiat. True builders envision a future in which that transfer is completely unnecessary. When those who passively purchase rather than utilize and build are at the wheel, as Jack Dorsey famously tweeted, “It will never escape their incentives.” Nevertheless, there is both a role and a place for investor participation. Rather than being inherently bad, it is a two-fold question regarding both the order of operations and the relative weight of distribution to properly and healthily introduce them. In designing Core, the users of the network have been prioritized on both of these vectors. At the time of mainnet, there has been no public or private sales of CORE tokens to investors.

Decentralized Distribution

The idealistic set of initial contributors built Core for three years without external funding, understanding the important philosophical distinction between builders and investors. As a result, Core’s distribution can focus on getting tokens into the hands of the actual builders and users of the network. In so doing, Core’s launch aims to be among the most decentralized in blockchain history.

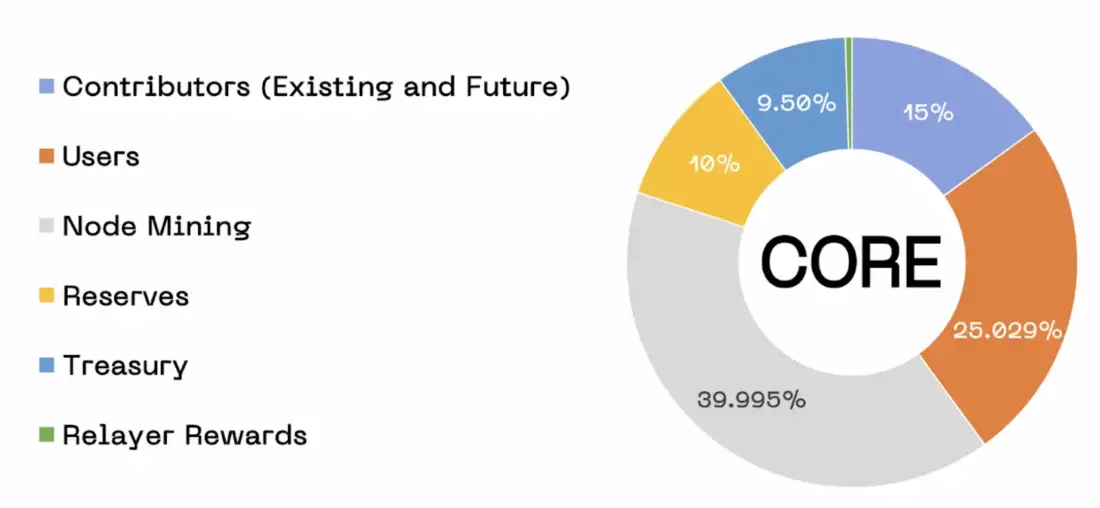

The following is an illustration of Core’s token distribution as it stands today:

Distribution Breakdown of the 2.1 billion total CORE tokens:

Node Mining (839,900,000 CORE tokens; 39.995% of the total supply):

To get Core off the ground, both miners and stakers who are securing the network must be compensated for their services. Node rewards will be distributed over an extended period of time (~81 years) to ensure long-term incentive alignment. Nodes can also receive rewards in the form of transaction fees.

Users (525,600,000 CORE tokens; 25.029%):

From the start, Core users should know that this chain is built for them. Airdropped CORE tokens will be allocated to a decentralized base of millions of users.

Contributors (Existing and Future) (315,000,000 CORE tokens; 15%):

Compensation will incentivize past, present, and future Core contributors.

Reserves (210,000,000 CORE tokens; 10%):

This reserve may be used over time in order to capitalize the foundation without centralizing the token supply.

Treasury (199,500,000 CORE tokens; 9.5%):

The Treasury will give the DAO the funds necessary to build out the ecosystem.

Relayer Rewards (10,000,000 CORE tokens; 0.476%):

Like nodes, relayers must be compensated for the services they provide to the chain’s security. Relayers also receive rewards in the form of transaction fees.

Token Functionality

A decentralized distribution is essential for CORE tokens because of the role it plays in the Core network. CORE is the utility and governance token of the Core Network with abilities including, but not limited to:

Paying for transaction/gas fees

Staking on the Core Network

Participating in Core network governance

Given these vital functions, CORE token holders bear great responsibility for upholding and directing the Core network. Nevertheless, Core’s tokenomics also contain certain indelible principles to uphold decentralization, self-sovereignty, and soundness.

Sound Supply

Following Bitcoin’s model of absolute scarcity, only 2.1 billion CORE tokens will ever exist. The hard supply cap is aimed at making Core maximally inflation resistant.

Emissions Curve and Schedule

The block rewards of CORE will be paid out over an 81 year period. These rewards will be paid out to network participants to promote the long-term success of the chain.

Each year, block rewards decrease by 3.6% over the last.

Decentralized Direction

Direction is often more important than speed, which is often lost in the chaos of crypto. The crypto industry’s volatility often appears to reward the fastest among us, but that volatility is a two-way street. Over a long enough time horizon, crypto punishes fragility and rewards antifragility. Projects with a sturdy foundation and direction are more likely to emerge from the worst wreckage. By deliberately targeting builders, users, and believers with the token launch, Core’s foundation is in perfect alignment with the vision of long-term decentralized governance.