Uniswap Has Lost Its Crown

Firstly, after the launch of Uni v3, Uniswap gives up its pricing power. What does that mean? For any asset traded among several exchanges, only 1 exchange can have pricing power.

Analogy:

ADR of a stock VS a stock in an exchange where it is mostly traded

In crypto, a token can be listed in multiple exchanges, CEXes or DEXes.

Why does Uniswap give up pricing power by launching v3?

It relates to how LPs provide liquidity in v3 - LPs select a price range where most liquidity is provided. This is called concentrated liquidity.

Why concentrated?

In Uni v2, liquidity is scattered evenly along the invariant curve of xy=k, but as most trading activities occur within a range at one time, liquidity in other parts of xy=k curve is not utilized, i.e. capital inefficient. v3 design is to tackle the issue.

v3 is more capital efficient than v2, but it entails LPs to actively manage their positions, as price range of trading pairs varies from time to time (except pegged assets). This deters new projects from setting up new liquidity pools of their native tokens in v3.

Why?

As price range of new tokens fluctuates a lot due to shallow initial liquidity, new projects with pools in v3 need to adjust the price range very often.

This poses huge cost of managing liquidity which is unaffordable to them. Thus, most new tokens aren't listed on v3.

With very few new tokens available on v3, it loses pricing power.

How? To look for prices of blue-chip tokens (eg $ETH), people refer to Binance. For tokens not listed there, as a lot more new tokens were listed on v2 before v3 launch, people often refer to v2 for price info

Due to huge cost of managing liquidity, pools on v3 are mostly blue-chip tokens which are liquid and less likely to fluctuate fiercely, and Uniswap's status as the primary source of price info falls apart.

SO WHAT?

LPs in DEXes without pricing power will suffer a lot from huge loses by being arbitraged against, and uninformed order flow is much less than exchanges with pricing power. Arbitrage is one main source of toxic flow that harms LPs a lot.

Why LPs suffer more in DEXes without pricing power?

ANS: less uninformed order flow (people trade mostly in the primary exchange) + more toxic flow (arbitrageurs take cues from primary source of price info, and take advantage of LPs in price discovery process of other AMMs)

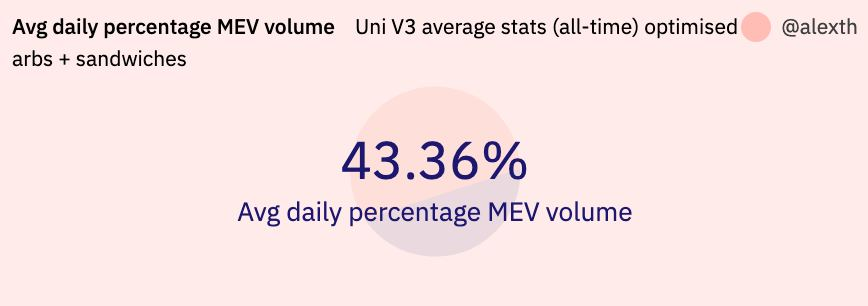

As pointed out by https://twitter.com/thiccythot_/status/1589022227437039616, v3 LPs lose $$ consistently due to huge toxic flow - ~43% of v3 trading volume is from MEV bots!

Why bother? It discourages users to be LPs of v3! This affects v3 profitability.

An exchange without pricing power is hard to take the lead of the sector, and it affects profitability.

CurveFinance Donimante The Stablecoin Market

By contrast, when one checks if a stablecoin has depegged, he will refer to CurveFinance not CEXes! With the comparison, importance of pricing power is self-explanatory

While CurveFinance takes 50% fees from LPs, Uniswap gives 100% fees to LPs; it earns nothing from all transactions. A business with no profits is never a good business, no matter how great the revenue seems to be.

Uniswap realises this, and proposes to take a cut from LPs

But things are not that easy. Uniswap could be in serious trouble by doing so. Without pricing power, LPs suffer more from toxic flow as said, and thus less incentivised to provide liquidity. If Uniswap now takes a cut, this further discourages LPs.

Again, SO WHAT?

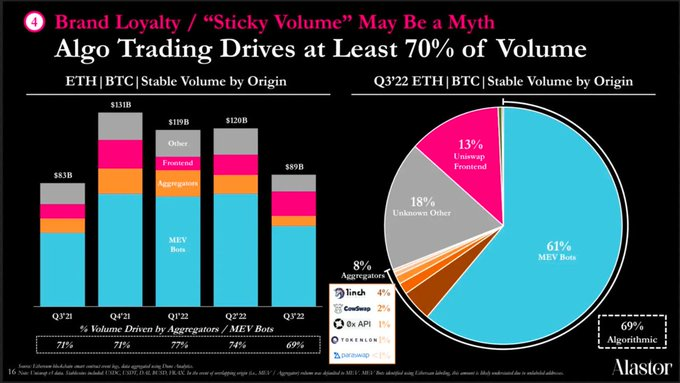

Most trading volume on Uni v3 isn't 'sticky', as >70% volume is driven by algos. Volume simply follows pricing.

So LPs less incentivised -> less TVL & liquidity -> higher slippage & worse execution price -> lower vol -> lower LP fees & LPs less incentivised

Death spiral.

How about raising trading fees for LPs to maintain TVL & liquidity?

Death spiral inevitable:

LPs less incentivised -> increasing trading fees for LPs -> worse execution price -> lower vol -> lower LP fees & LPs less incentivised

That's why Uniswap never push fee switch.

A lot of web2 tech businesses do not make profits in the very few years, but they are actually building 'moats' and enhancing customers' stickiness.

Uniswap makes no profits, but cannot cultivate sticky user behaviour, as only <15% trading volume is from its frondend...

Why CurveFinance prevails over Uniswap?

Can you imagine what happen to Uni v3 TVL and trading volume if it only gives 50% fees to LPs, just as Curve does?

Curve bootstrap liquidity via ve-model and empower $CRV with practical utility.

In contrast, $UNI has no utility at all, and is irrelevant to Uniswap business. If Uni v3 can take 50% fees from LPs and still maintain TVL & trading vol, Uniswap trumps Curve. But that’s not the case, because most of its trading volume is not 'sticky' or organic .

Uniswap cannot be excused by saying - "as time lapses, more users are used to our platform, causing more fees and more liquidity." Trading volume on Uniswap is not loyal, and unless it can drastically increase volume from its frontend, volume just leaves as fee switch launch.

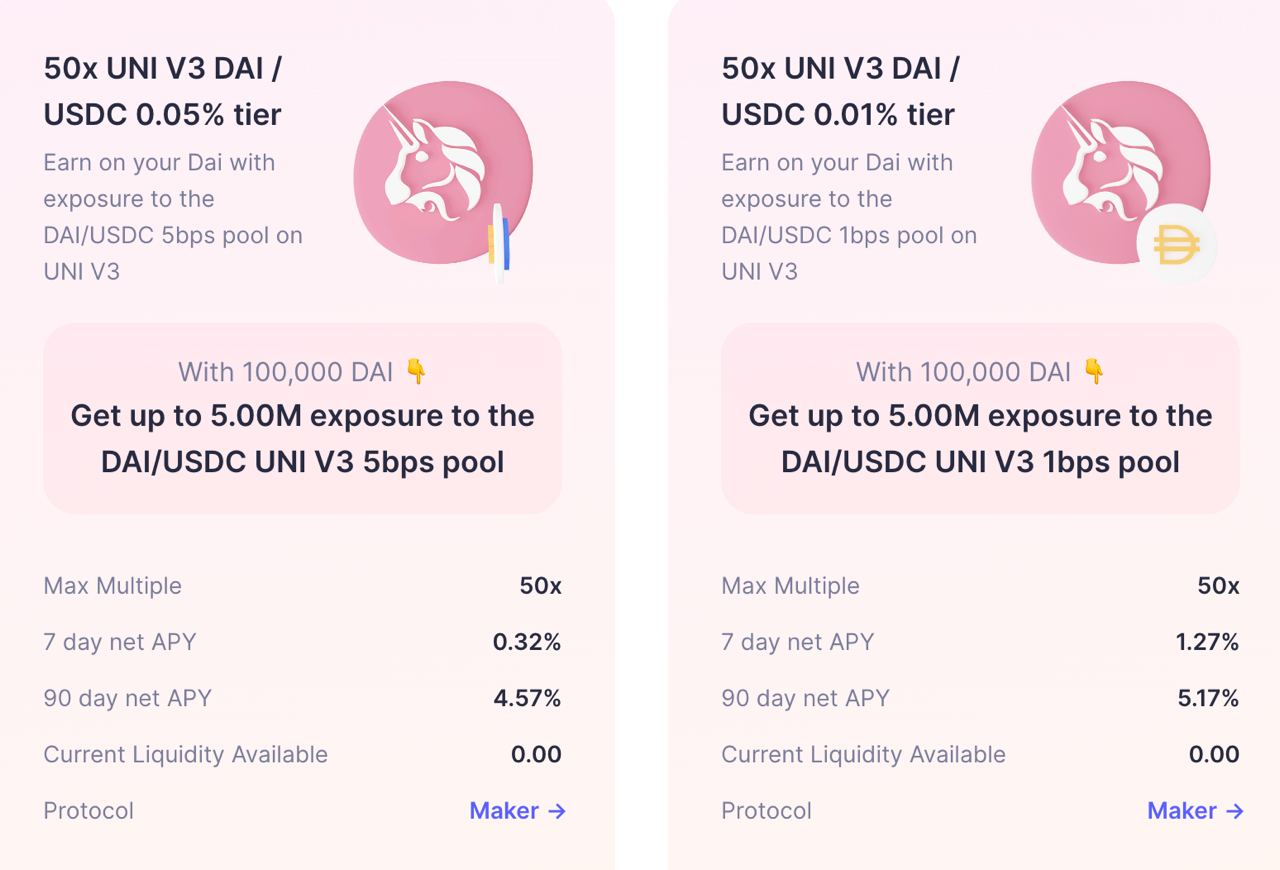

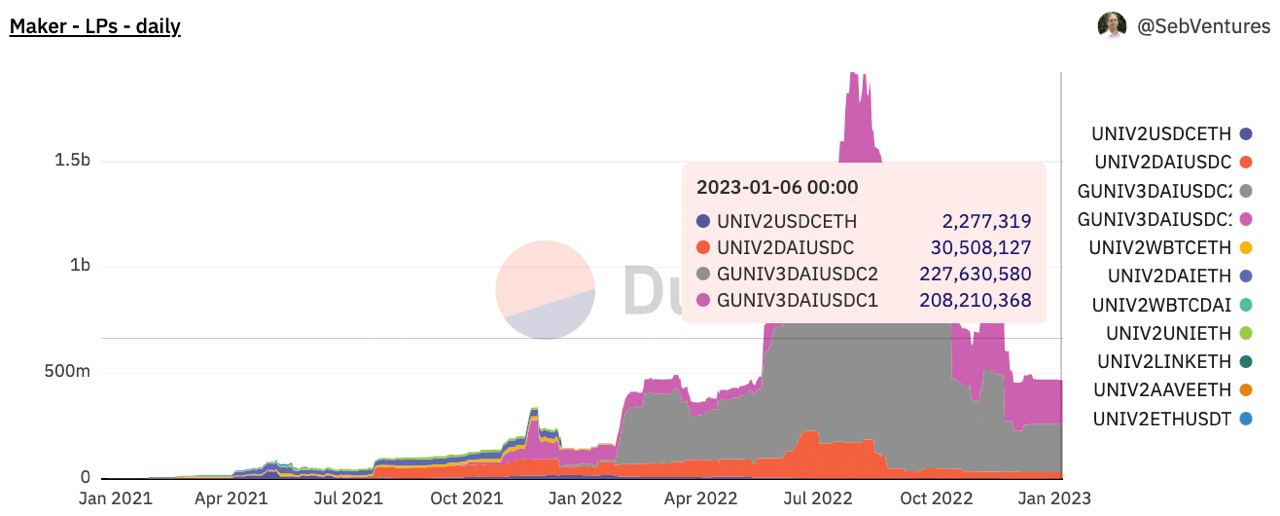

Moreover, Uniswap TVL is leveraged: out of $3.4B, ~435M is from $DAI/$USDC pair, which has been added leverage to up to 50x by MakerDAO, as it accepts Uni $DAI/$USDC LP token as collateral to mint $DAI! $DAI can then redeposited there in to get LP token to mint more $DAI!

Thus CurveFinance prevails over Uniswap because (i) it has the pricing power to be pegged assets' primary source of price info, and (ii) it takes 50% cut from LP trading fees but still can attract huge TVL without leverage by its exceptional ve-tokenomics!

If CurveFinance TVL depends so much on $CRV emission, once $CRV falls hard, TVL will drop very significantly due to lower APR.

This is true, but same for ethereum: if $ETH slumps, it's more prone to attack and less secure

To me, what makes web3 so special is the ability of every one of us to issue digital assets in a non-custodial manner, and bootstrap liquidity or other metrics by making good use of token issuance. So far CurveFinance epitomises how web3 projects can do it.

Lastly, why is Uni v3 a wrong move? It increases projects' cost of managing on-chain liquidity, and thus gives up its pricing power. Instead of improving capital efficiency of Uni v2 bonding curve by introducing several curves to cater for different crypto assets, it just...... creates a new model which imo is a worse version of orderbook. It is now distracted from being basic utility of the industry to being one of the competitive candidates in consumer sector by competing against aggregators (NFT or 1inch).If it could focus on making it inevitable for the issuance of all volatile crypto assets, it would be just like electricity and water - users couldn't avoid Uniswap when swapping tokens. This is the best path Uniswap should take imo, and obviously it chooses a different path.

That's it! I hope it can arouse some fruitful discussion of what these blue-chip DeFi projects should do next. Feel free to share to more people and leave comment to express your view!