Written by: Kolten

Compiled by: AididiaoJP, Foresight News

The U.S. CLARITY Act has sparked a discussion about the future of money and banking. A core provision of the bill is: prohibiting digital asset service providers, such as cryptocurrency exchanges, from paying yields to their customers solely for holding "payment stablecoins."

This ban on third-party platforms is actually an extension of the 2025 GENIUS Act, which already prohibited stablecoin issuers themselves from paying interest. The banking industry supports these measures to protect its lucrative "spread" income.

Simply put, the traditional bank model is: attract deposits with low interest rates, then lend or invest in assets like government bonds at higher rates. The difference between the interest earned and the interest paid is the bank's net interest margin (or spread).

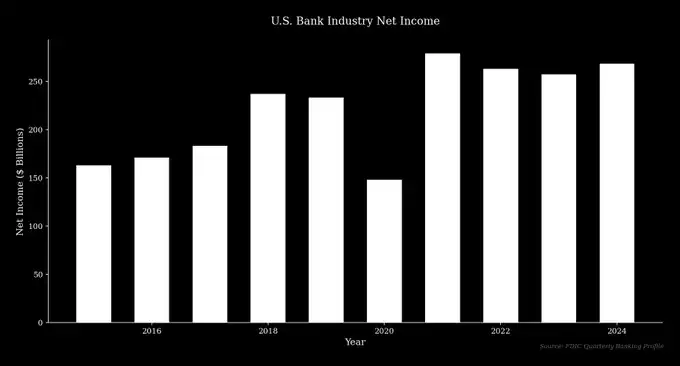

This model is highly profitable. For example, in 2024, JPMorgan Chase reported revenue of $180.6 billion and a net profit of $58.5 billion, with net interest income of $92.6 billion being the primary contributor.

Emerging fintech provides depositors with direct channels to obtain higher yields, introducing competitive pressure that the banking industry has long avoided. Consequently, some large traditional banks are attempting to protect their business models through regulatory means—a strategy that is both logical and has historical precedent.

The Division in Banking

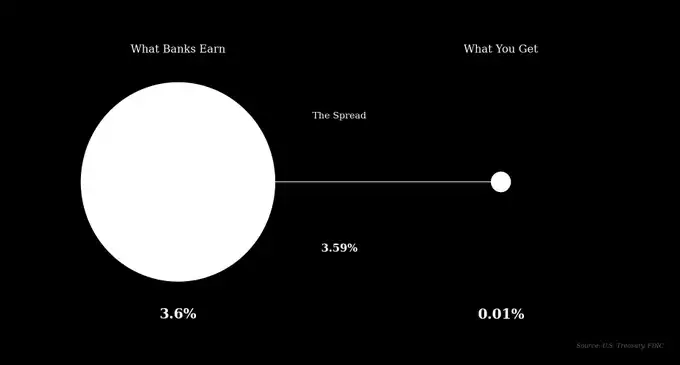

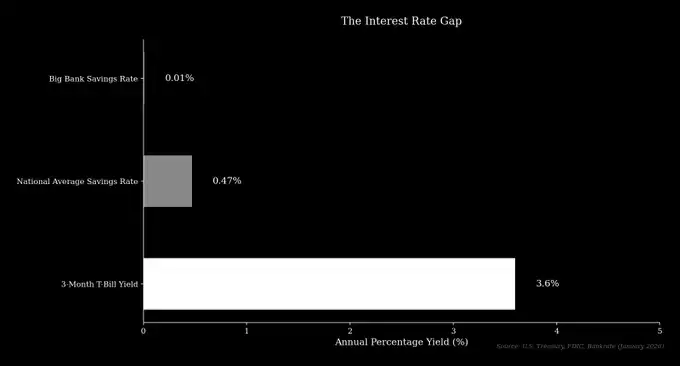

As of early 2026, the average annualized interest rate for U.S. savings accounts was 0.47%, while basic savings account rates at major banks like JPMorgan Chase and Bank of America were only 0.01%. During the same period, the risk-free 3-month U.S. Treasury yield was about 3.6%. This means major banks can absorb deposits, buy Treasuries, and easily earn a spread of over 3.5%.

JPMorgan Chase has deposits of approximately $2.4 trillion; theoretically, this spread alone could generate over $85 billion in income. While a simplified calculation, it sufficiently illustrates the point.

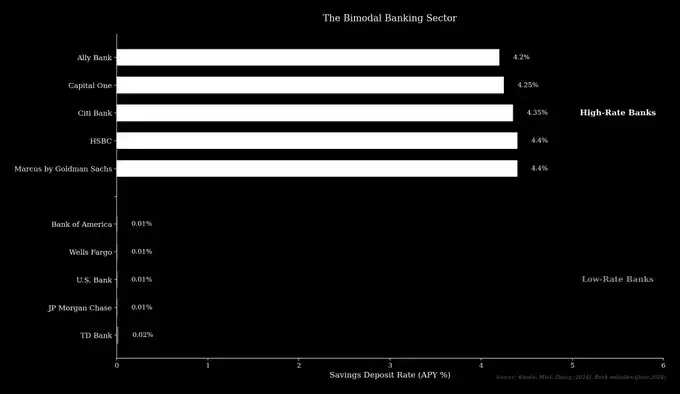

Since the global financial crisis, the banking industry has gradually divided into two types of institutions:

- Low-rate banks: Typically large traditional banks that attract deposits from rate-insensitive customers through extensive branch networks and brand recognition.

- High-rate banks: Such as Goldman Sachs' Marcus, Ally Bank, etc., mostly online banks that compete by offering deposit rates close to market levels.

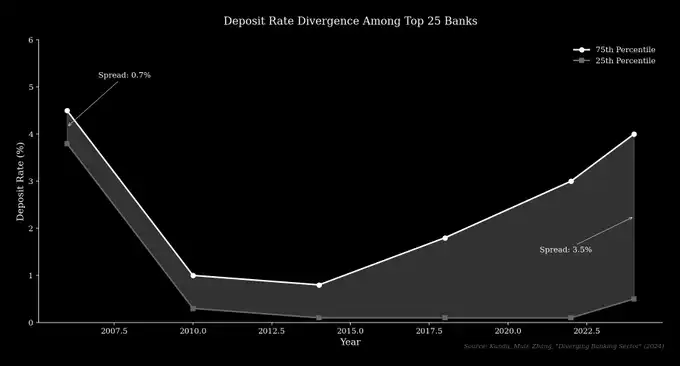

Research shows the deposit rate disparity among the top 25 U.S. banks has widened from 0.70% in 2006 to over 3.5% currently.

The profitability of low-rate banks is fundamentally based on depositors who do not actively seek higher returns.

The "$6 Trillion Deposit Drain Theory"

Banking groups claim that allowing stablecoins to pay yields could lead to "deposit outflows" of up to $6.6 trillion, draining credit resources from the economy. The CEO of Bank of America stated at a conference in January 2026: "Deposits are not just a conduit for funds; they are a source of credit. Outflows of deposits will weaken banks' lending capacity, forcing them to rely more on costlier wholesale funding."

He argued that small and medium-sized businesses would be the first affected, while Bank of America itself would be "less impacted." This argument equates stablecoins absorbing deposits with funds leaving the banking system, but this is not always the case.

When a customer buys stablecoins, dollars are transferred into the issuer's reserve account. For example, USDC's reserves are managed by BlackRock and held in cash and short-term U.S. Treasuries. These assets remain within the traditional financial system—the total amount of deposits may not decrease, they merely shift from individual accounts to issuer accounts.

The Real Concern

What the banking industry truly fears is: deposits flowing from their own low-interest accounts to higher-yielding alternatives. For example, Coinbase's USDC rewards or DeFi products like Aave offer yields far exceeding those of most banks. For the customer, it's a choice between keeping money at a major bank earning 0.01% or converting to stablecoins earning over 4%—a difference of more than 400 times.

This trend is changing depositor behavior: funds are moving from transactional accounts to interest-bearing accounts, and depositors are becoming more rate-sensitive. A fintech analyst points out: "The real competitor for banks is not stablecoins, but other banks. Stablecoins are merely accelerating competition among banks, ultimately benefiting consumers."

Research also confirms: when market interest rates rise, deposits flow from low-rate banks to high-rate banks. And high-rate banks are expanding their personal and business lending operations—the capital flows brought by stablecoins will likely have a similar effect, directing capital to more competitive institutions.

History Repeats Itself

The current debate over stablecoin yields closely resembles the controversy surrounding "Regulation Q" last century. This regulation set a cap on bank deposit rates, aiming to prevent "excessive competition." In the high-inflation, high-interest environment of the 1970s, market rates far exceeded the cap, harming depositor returns.

In 1971, the first money market fund was created, allowing depositors to earn market returns and support check payments. Similarly, protocols like Aave now allow users to earn yields without going through a bank. Money market fund assets surged from $45 billion in 1979 to $180 billion two years later, and now exceed $8 trillion.

Banks and regulators initially resisted money market funds as well, but the interest rate caps were eventually abolished for being unfair to depositors.

The Rise of Stablecoins

The stablecoin market is also experiencing rapid growth: its total market capitalization soared from $4 billion in early 2020 to over $300 billion in 2026. The largest stablecoin, USDT, saw its market cap surpass $186 billion in 2026. This reflects market demand for "digital dollars that are freely transferable and can earn yield."

The debate over stablecoin yields is essentially a modern version of the money market fund debate. The banks opposing stablecoin yields are primarily the low-rate traditional banks that benefit from the current system. Their goal is to protect their own business model, while this new technology clearly offers more value to consumers.

History shows that technology providing a better solution will eventually be embraced by the market. Regulators need to decide: whether to facilitate this transition or delay its progress.